Daily Updates

“Crude oil is holding near its high of three weeks ago. It’s very strong above $77, and a close above $81.50 would be a new high and very bullish. It would then follow gold up to possibly the $90 level.” – Aden Forecast

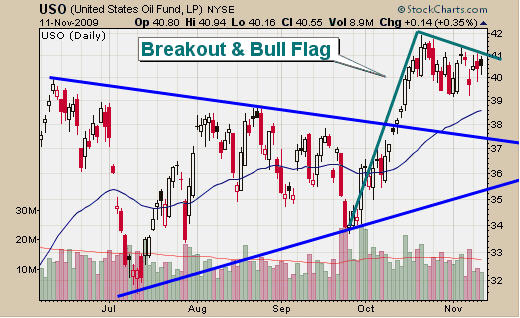

Chart courtesy of TheGoldandOilGuy Chris Vermulen – his full article HERE

Oil: future world shortages are being drastically underplayed, say experts

A leading academic institute has urged European governments to review global oil supplies for themselves because of the “politicisation” of the International Energy Agency’s figures.

Uppsala University in Sweden today published a scathing assessment of the IEA’s annual World Energy Outlook, saying some assumptions drastically underplayed the scale of future oil shortages.

….read more HERE.

Ed Note: This massive oil deposit the Bakken Formation lies underneath Saskatchewan and North Dakota. There are estimates it holds more Oil that Saudi Arabia (250 Billion Barrels) and the quality of the Crude makes sought after Saudi light look like Heavy Crude.) This is a BIG Story with many angles.

“The Bakken is economic at any price level,” said Crescent Point chief executive officer

Scott Saxberg. “And the Lower Shaunavon is probably similar.”

….read Discovery Investing’s Michael Berry’s whole analysis and investment strategy HERE.

You can sign up for Dr. Berry’s free Morning Notes HERE.

Michael Berry has been a portfolio manager for both Heartland Advisors and Kemper Scudder where he successfully managed small and mid cap value portfolios. Dr. Berry has specialized in the study of behavioral strategies for investing and has been published in a number of academic and practitioner journals. His definitive work on earnings surprise, with David Dreman, was published in 1995 in the Financial Analysts Journal.

Previously, Dr. Berry was a professor of investments at the Colgate Darden Graduate School of Business Administration at the University of Virginia and has also held the Wheat First Endowed Chair at James Madison University.

Dr. Berry is a respected and dynamic speaker. He regularly presents around the world on topics such as value investing, the role of Austrian Economics in investment management, behavioral investing strategies and is a specialist in developing case studies to teach investors how to invest. While a professor, he published a case book, Managing Investments: A Case Approach.

An excerpt from the Bond King, Pimco’s Bill Gross’s Investment Outlook for November

An investment segue is a tough one this month: markets whistling past the graveyard? A vampire economy? A ghostly correction ahead? Pretty lame, so I’ll jump straight into a discussion of why in a New Normal economy (1) almost all assets appear to be overvalued on a long-term basis, and, therefore, (2) policymakers need to maintain artificially low interest rates and supportive easing measures in order to keep economies on the “right side of the grass.”

Let me start out by summarizing a long-standing PIMCO thesis: The U.S. and most other G-7 economies have been significantly and artificially influenced by asset price appreciation for decades. Stock and home prices went up – then consumers liquefied and spent the capital gains either by borrowing against them or selling outright. Growth, in other words, was influenced on the upside by leverage, securitization, and the belief that wealth creation was a function of asset appreciation as opposed to the production of goods and services. American and other similarly addicted global citizens long ago learned to focus on markets as opposed to the economic foundation behind them. How many TV shots have you seen of people on the Times Square Jumbotron applauding the announcement of the latest GDP growth numbers or job creation? None, of course, but we see daily opening and closing market crescendos of jubilant capitalists on the NYSE and NASDAQ cheering the movement of markets – either up or down. My point: Asset prices are embedded not only in our psyche, but the actual growth rate of our economy. If they don’t go up – economies don’t do well, and when they go down, the economy can be horrid.

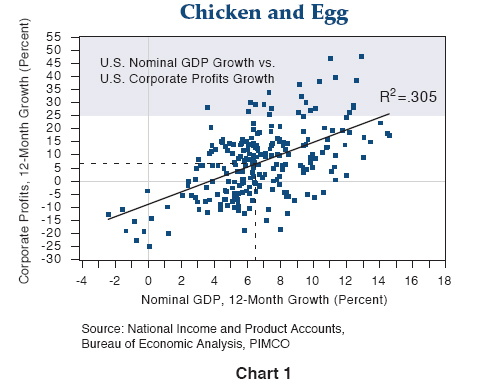

To some this might seem like a chicken and egg conundrum because they naturally move together. For the most part they do – and should. As pointed out in a recent New York Times article titled “Dow Bubble?,” stocks and nominal GDP growth should be correlated because profits and nominal GDP are correlated as well. Witness the PIMCO Chart 1, researched by Saumil Parikh, which covers a time period of 50 years. Granted the R2 correlation is only .305, but that is to be expected – profits are also a function of the respective entities that feed at the GDP growth trough – corporations, labor, government and other countries – and when corporations and their profits are ascendant they do well; when not, they fall below the best fit line appearing in the chart. Notice as well that in a normally functioning economy growing at 6-7% nominal GDP, that profits grow at the same rate. (At growth distribution tails there are substantial distortions.) And if long term profits match nominal GDP growth then theoretically stock prices should too.

Not so. What has happened is that our “paper asset” economy has driven not only stock prices, but all asset prices higher than the economic growth required to justify them. Granted, one must be careful of beginning and ending data points in any theoretical “proof.” Such is the fallacy of Jeremy Siegel’s Stocks for the Long Run approach which begins at very low PEs and ends most long-term time periods with much higher ones, justifying a 6.5% “Siegel constant” real rate of return for U.S. equities over the past 75 years or so. It may also be a weakness of the New York Times “Dow Bubble” article where the authors claim that since the Dow Jones average was at 4,000 in 1995, that a 100% step-for-step correlation with nominal GDP growth since then would produce a reasonable valuation of 7,800 – not the current 10,000.

Having said that, let me introduce Chart 2 a PIMCO long-term (half-century) chart comparing the annual percentage growth rate of a much broader category of assets than stocks alone relative to nominal GDP. Let’s not just make this a stock market roast, let’s extend it to bonds, commercial real estate, and anything that has a price tag on it to see if those price stickers are justified by historical growth in the economy.

This comparison uses a different format with a smoothing five-year trailing valuation growth rate for all U.S. assets since 1956 vs. corresponding economic growth. Several interesting points.

…..read the rest HERE. (scroll down to the second chart above to continue, the first three paragraphs are also interesting writing)

by

William H. GrossManaging

Director

“PIMCO’s Mission is to Preserve and Enrich Client Assets and Provide the Highest Quality Investment Management Service.”

Who We Are

We are PIMCO, a leading global investment management firm with more than 1,200 employees in offices in Newport Beach, New York, Amsterdam, Singapore, Tokyo, London, Sydney, Munich, Toronto and Hong Kong.

We manage investments for an array of clients, including retirement and other assets that reach more than 8 million people in the U.S. and millions more around the world. Our clients include state, municipal and union pension and retirement plans whose beneficiaries come from all walks of life, from educators to healthcare workers to public safety employees. We are also advisors and asset managers to central banks, corporations, universities, foundations and endowments.

We are dedicated to our clients. From our founding in 1971, PIMCO’s global team of investment professionals has been dedicated to client service, allowing our portfolio managers to focus on returns. We serve individual investors through pooled and mutual funds in the U.S. and Europe and offer institutional clients mutual funds as well as privately managed separate accounts

We are committed to being the best provider of global investment solutions in the world. Our thought leadership, talent, technology and long-term investment approach drive our abilities around the globe. We offer a continually evolving set of solutions across all asset classes in an effort to provide investors with consistent returns, superior risk management and topflight client service.

We are a trendsetter in the asset management industry, and have been throughout our 38-year history. We remain at the forefront today, pioneering the use of innovative solutions for our clients, including portable alpha and absolute return strategies. Our investment process and operational structure drive our ability to anticipate client needs and respond quickly to ever-changing economic, market and policy environments.

The story below is via Peter Grandich who wrote the following:

Despite being an aggressive gold bull from about $325 on gold, I’ve not publicly commented on everyday rumors that always are floated. But after hearing from some very astute contacts (who have been quite reliable sources in the past) that there’s a reasonable chance we could see a short squeeze in gold, I found this commentary worthy of notation. I don’t think it’s far-fetched given the story (Ed: Note I posted below) as well.

It would be poetic justice if true given the fact that the most notorious bears have inaccurately claimed actual weak demand and a rise in gold production. Whether or not we see a squeeze, gold remains in a strong uptrend with $1,200 doable before years-end.

Stay tuned!

Ed Note: Here is the story Peter refers to.

As world gold supply runs out – Barrick shuts hedge book

by Ambrose Evans-Prichard Telegralph.co.uk

Global gold production is in terminal decline despite record prices and Herculean efforts by mining companies to discover fresh sources of ore in remote spots, according to the world’s top producer Barrick Gold.

Aaron Regent, president of the Canadian gold giant, said that global output has been falling by roughly 1m ounces a year since the start of the decade. Total mine supply has dropped by 10pc as ore quality erodes, implying that the roaring bull market of the last eight years may have further to run.

“There is a strong case to be made that we are already at ‘peak gold’,” he told The Daily Telegraph at the RBC’s annual gold conference in London.

“Production peaked around 2000 and it has been in decline ever since, and we forecast that decline to continue. It is increasingly difficult to find ore,” he said.

Ore grades have fallen from around 12 grams per tonne in 1950 to nearer 3 grams in the US, Canada, and Australia. South Africa’s output has halved since peaking in 1970.

The supply crunch has helped push gold to an all-time high, reaching $1,118 an ounce at one stage yesterday. The key driver over recent days has been the move by India’s central bank to soak up half of the gold being sold by the International Monetary Fund. It is the latest sign that the rising powers of Asia and the commodity bloc are growing wary of Western paper money and debt.

China has quietly doubled holdings to 1,054 tonnes and is thought to be adding gradually on price dips, creating a

market floor. Gold remains a tiny fraction of its $2.3 trillion in foreign reserves.

Gold exchange-traded funds (ETFs) – dubbed the “People’s Central Bank” – have accumulated 1,778 tonnes, making them the fifth biggest holder after the US, Germany, France, and Italy.

Ross Norman, director of theBullionDesk.com, said exploration budgets had tripled since the start of the decade with stubbornly disappointing results so far.

Output fell a further 14pc in South Africa last year as companies were forced to dig ever deeper – at greater cost – to replace depleted reserves, not helped by “social uplift” rules and power cuts. Harmony Gold said yesterday that it may close two more mines over coming months due to poor ore grades.

Mr Norman said the “false mine of central banks” had been the only new source of gold supply this decade as they auction off reserves, but they are switching sides to become net buyers.

Barrick is moving fast to wind down the remaining 3m ounces of its infamous hedge book over the next twelve months, an implicit bet on rising gold prices over time.

Mr Regent said the company had waited too long to ditch the policy, which has made the company enemy number one among ‘gold bug’ enthusiasts. The hedges oblige Barrick to deliver part of its gold into futures contracts set long ago at levels far below today’s spot prices.

The strategy worked well in the falling market of the 1990s, but has cost the company dear in lost profits this decade. “Hindsight is always 20/20,” said Mr Regent, who was appointed from the outside earlier this year.

Barrick bit the bullet in the third quarter, taking a $5.7bn charge against earnings on hedge contracts. Liberation is at last in sight. In 2001 the hedge book topped 20m ounces.

Mr Regent said the hedge policy has weighed badly on the share price and irked investors, becoming a bone of contention at every meeting. The financial crisis brought matters to a head as markets fretted about counterparty risk. “It was clear to me that there were a significant number of institutions who wouldn’t invest in Barrick because of the hedge book,” he said.

Barrick produced 1.9m ounces of gold last quarter, down from 1.95m a year earlier. Costs have been “trending down” to $456 an ounce, though rising energy prices pose a fresh threat. Total reserves are 139m ounces, far ahead of rival Newmont Mining at 86m.

The hedge book venture has not been a happy one, but those who predicted that Barrick would eventually “blow up” on its contracts may owe the company an apology.

Read Gold: How High Can the Price Go? in the Telegraph HERE.

Ambrose Evans-Pritchard has covered world politics and economics for 25 years, based in Europe, the US, and Latin America. He joined the Telegraph in 1991, serving as Washington correspondent and later Europe correspondent in Brussels. He is now International Business Editor in London.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

To HERE Peter speak and others speak on Trading go HERE:

….go to visit Peter’s Website.

November 11th 1:39pm I’d like to thank everyone at Maverick Business Adventures for allowing me to speak to you today. While I truly appreciated the time afforded to me, there is so much more to discuss. I encourage you to visit this blog at your leisure. You can registered to receive a free daily email of the blog posts, capsulizing all that’s been posted the previous day.

A good place to start to get a feel for my long-term outlook is my 25th anniversary issue from last month. I believe two movies available on the Internet are “must-see” views. They are:

www.iousathemovie.com – I believe it’s the most accurate account of the true fiscal status of the United States. The host of the video is my #1 financial guru, Mr. David Walker.

“The Third Jihad -Radical Islam’s Vision for America”. The recent horrific incident at Ft. Hood is sadly just a small preview of what this film strongly believes is underway here in the U.S. It’s very politically incorrect, but I believe this is just part of a far bigger event that I’ve called the number one factor for all plans for the future. I wrote about it recently and urge you to watch this video within the report.

A quick summary of my views are as follows:

U.S. Stock Market – A mini melt-up has been underway that’s forcing professional investors in whether they like it or not. While fundamentals are mixed at best, the “Don’t Worry, Be Happy” crowd is in control and appears on track in delivering me a wonderful gift of DJIA 10,500 – 11,000 to get bearish in again. It just may be a white Christmas!

It’s important to note that a renewed bearish stance will not likely be worldwide. I believe the future of the U.S. stock market will look like Japan has for the last twenty years – greatly under-performing most world markets and an economy that sputters along at best.

U.S. Interest Rates – The question you have to ask yourself looking out past the next few months and instead concentrating on the next few years is this: Are 3%-4% interest rates worth locking in now for the next 10 -30 years? It’s my firm belief that the FED is the sole reason rates remain so low and inevitably the day of reckoning for massive debts, deficits and a terminally ill currency will result in much higher interest rates down the road. Bonds in general are clearly the lesser of two evils but are evil never-the-less.

U.S. Dollar – Back when the U.S. Dollar Index was well above 100 (it’s now around 75), I began pounding the table that the only party that doesn’t know the U.S. Dollar is dead was the U.S. Dollar. I said more and more governments would move away from the dollar as the world’s reserve currency. I constantly stated this would occur because America has been robbing Peter to pay Paul and Peter was tapped out.

Despite being terribly oversold, the U.S. Dollar can’t even mount a bear market rally. A close below 74 should bring on a quick decline to new lows, an event that should lead me to lock in tremendous profits. This may include suggesting those who converted savings in U.S. Dollars into Canadian dollars back when the Loonie was well under 80 to convert back again. Stay tuned.

Precious and Base Metals – I’ve greatly favored over-weighting precious metals over base metals and still believe that’s the way to go. I do think both groups are overextended for the very short-term and a healthy consolidation now versus another leg up now would actually be better for much higher prices in the future. I’m in no way suggesting any sales but instead proposing new buyers not approach these markets with wild abandonment.

Gold continue to be in the mother of all secular bull markets that despite new nominal highs after another, the vast majority of professionals have either missed or worse, bet against. Until such time when these wrong way bears wave the white flag, we at best should only see periods of consolidation and pullbacks limited to 5-10%.

Oil and Natural Gas – I remain dead neutral on both. Oil has been mostly a dollar driven market. I’ve targeted the $85+ area as a possible area to go short so stay tuned. The world is awash in natural gas so I think it’s best to just stand aside in this market.

Summary – Once again, I’d like to thank the members of Maverick Business Adventures for allowing me to speak to you today. While I’m not optimistic about the long-term economic, social, political and spiritual future of America, I still believe there are areas of the world that offer great investment opportunity. Commodities in general remain in a secular bull market. There are dramatic shifts underway worldwide and while one of them may be politically incorrect to speak openly about, it never-the-less will have a major impact on all long-term investments.

Geopolitical concerns worldwide, with special emphasis in the Middle East, appear ready to move to the forefront and should have a big impact on one’s investments as well. Sadly, I believe it’s not a question of if, but when Israel and Iran’s conflict becomes a military event.

The one group of Americans who will be most impacted by all that has happened and what I envision are seniors. This will have major political implications as there are now more Americans over the age of 65 than under 18. Seniors are the single biggest voting block and control most of the wealth in America. Like it or not, they will become a major force in the social, political economic and spiritual battle that is now fully underway in America.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

To HERE Peter speak and others speak on Trading go HERE:

Off to Toronto for BNN tomorrow then Montreal Investment Conference.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair