An excerpt from the Bond King, Pimco’s Bill Gross’s Investment Outlook for November

An investment segue is a tough one this month: markets whistling past the graveyard? A vampire economy? A ghostly correction ahead? Pretty lame, so I’ll jump straight into a discussion of why in a New Normal economy (1) almost all assets appear to be overvalued on a long-term basis, and, therefore, (2) policymakers need to maintain artificially low interest rates and supportive easing measures in order to keep economies on the “right side of the grass.”

Let me start out by summarizing a long-standing PIMCO thesis: The U.S. and most other G-7 economies have been significantly and artificially influenced by asset price appreciation for decades. Stock and home prices went up – then consumers liquefied and spent the capital gains either by borrowing against them or selling outright. Growth, in other words, was influenced on the upside by leverage, securitization, and the belief that wealth creation was a function of asset appreciation as opposed to the production of goods and services. American and other similarly addicted global citizens long ago learned to focus on markets as opposed to the economic foundation behind them. How many TV shots have you seen of people on the Times Square Jumbotron applauding the announcement of the latest GDP growth numbers or job creation? None, of course, but we see daily opening and closing market crescendos of jubilant capitalists on the NYSE and NASDAQ cheering the movement of markets – either up or down. My point: Asset prices are embedded not only in our psyche, but the actual growth rate of our economy. If they don’t go up – economies don’t do well, and when they go down, the economy can be horrid.

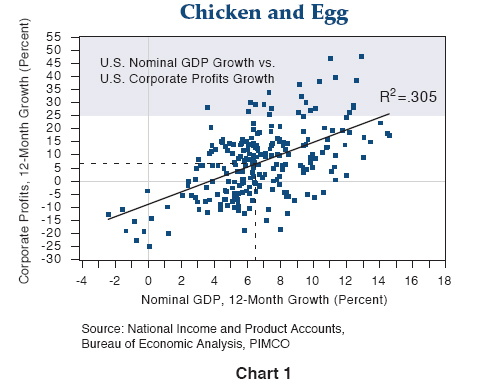

To some this might seem like a chicken and egg conundrum because they naturally move together. For the most part they do – and should. As pointed out in a recent New York Times article titled “Dow Bubble?,” stocks and nominal GDP growth should be correlated because profits and nominal GDP are correlated as well. Witness the PIMCO Chart 1, researched by Saumil Parikh, which covers a time period of 50 years. Granted the R2 correlation is only .305, but that is to be expected – profits are also a function of the respective entities that feed at the GDP growth trough – corporations, labor, government and other countries – and when corporations and their profits are ascendant they do well; when not, they fall below the best fit line appearing in the chart. Notice as well that in a normally functioning economy growing at 6-7% nominal GDP, that profits grow at the same rate. (At growth distribution tails there are substantial distortions.) And if long term profits match nominal GDP growth then theoretically stock prices should too.

Not so. What has happened is that our “paper asset” economy has driven not only stock prices, but all asset prices higher than the economic growth required to justify them. Granted, one must be careful of beginning and ending data points in any theoretical “proof.” Such is the fallacy of Jeremy Siegel’s Stocks for the Long Run approach which begins at very low PEs and ends most long-term time periods with much higher ones, justifying a 6.5% “Siegel constant” real rate of return for U.S. equities over the past 75 years or so. It may also be a weakness of the New York Times “Dow Bubble” article where the authors claim that since the Dow Jones average was at 4,000 in 1995, that a 100% step-for-step correlation with nominal GDP growth since then would produce a reasonable valuation of 7,800 – not the current 10,000.

Having said that, let me introduce Chart 2 a PIMCO long-term (half-century) chart comparing the annual percentage growth rate of a much broader category of assets than stocks alone relative to nominal GDP. Let’s not just make this a stock market roast, let’s extend it to bonds, commercial real estate, and anything that has a price tag on it to see if those price stickers are justified by historical growth in the economy.

This comparison uses a different format with a smoothing five-year trailing valuation growth rate for all U.S. assets since 1956 vs. corresponding economic growth. Several interesting points.

…..read the rest HERE. (scroll down to the second chart above to continue, the first three paragraphs are also interesting writing)

by

William H. GrossManaging

Director

“PIMCO’s Mission is to Preserve and Enrich Client Assets and Provide the Highest Quality Investment Management Service.”

Who We Are

We are PIMCO, a leading global investment management firm with more than 1,200 employees in offices in Newport Beach, New York, Amsterdam, Singapore, Tokyo, London, Sydney, Munich, Toronto and Hong Kong.

We manage investments for an array of clients, including retirement and other assets that reach more than 8 million people in the U.S. and millions more around the world. Our clients include state, municipal and union pension and retirement plans whose beneficiaries come from all walks of life, from educators to healthcare workers to public safety employees. We are also advisors and asset managers to central banks, corporations, universities, foundations and endowments.

We are dedicated to our clients. From our founding in 1971, PIMCO’s global team of investment professionals has been dedicated to client service, allowing our portfolio managers to focus on returns. We serve individual investors through pooled and mutual funds in the U.S. and Europe and offer institutional clients mutual funds as well as privately managed separate accounts

We are committed to being the best provider of global investment solutions in the world. Our thought leadership, talent, technology and long-term investment approach drive our abilities around the globe. We offer a continually evolving set of solutions across all asset classes in an effort to provide investors with consistent returns, superior risk management and topflight client service.

We are a trendsetter in the asset management industry, and have been throughout our 38-year history. We remain at the forefront today, pioneering the use of innovative solutions for our clients, including portable alpha and absolute return strategies. Our investment process and operational structure drive our ability to anticipate client needs and respond quickly to ever-changing economic, market and policy environments.