Daily Updates

I’ve seen a lot of big bull markets, but this gold bull market contains probably the most persistent and relentless advance I’ve ever seen – Richard Russell December 3rd/09

In a world of paper currencies and paper promises, I can think of many reasons right off the top of my head why the price of gold will continue to go up in the long term, however, because this essay’s length is limited, I’ll just mention five of them.

In short, while it may feel like a bubble to some, I believe we are just warming up.

Last week I mentioned a few of such reasons, but I’d like to expand this topic this week. Below I have featured five of the many points that currently point to higher value of the gold price in the long run.

1. The smart money is already piled into gold.

Some of the world’s savviest money managers have taken large positions in gold. I mentioned John Paulson, David Einhorn, Paul Tudor Jones, and Jim Rogers but I forgot to mention George Soros, who increased his holding in gold in the third quarter with gold mining stocks and the SPDR Gold Trust ETF (GLD). This week the Wall Street Journal reported that John Paulson is launching a new gold fund, which will include $250 million of his own personal investment.

Other well-known fund managers publicly piling into gold include Bill Gross, Kyle Bass (Hayman Capital), Paolo Pellegrini (PSQR), John Burbank (Passport Capital), Evy Hambro (Blackrock), Donald Coxe (Coxe Advisors), and David Tice (Prudent Bear Fund). I’d expect other major mutual funds, hedge funds, and pension funds to follow their lead.

2. Central banks are net buyers of gold for the first time in 22 years.

This is a major secular change. According to a report by precious-metals research firm GFMS, for the first time since 1987, central banks around the world bought more gold in the second quarter than they sold. India recently bought 200 tons of gold from the IMF and China is expected to purchase the other 200 tons offered for sale.

3. In June there was an item in Bloomberg about Northwestern Mutual Life Insurance Co., the third-largest US life insurer, having bought gold for the first time in the company’s 152-year history.

According to the report, the insurance company has accumulated about $400 million in gold. I’d expect that other insurance companies might follow suit.

4. China holds two trillion dollars in Foreign Currency reserves and only 2% in gold, versus a 10% worldwide average.

The Chinese are seeing the value of their foreign currency reserves turning to dust every day. If China makes the logical move to increase its gold reserves and reduce its fiat currency exposure to even just the worldwide average, gold prices could move substantially higher.

5. Gold is scarce.

The gold industry hasn’t replaced gold reserves mined in over a decade, meaning near-term shortages.

We might get to a situation where there is simply not enough physical gold available to cover the massive quantities of gold that has been pledged.

This situation could push the price of gold to the stratosphere. Hong Kong has recently pulled all its gold holdings and deposits from London and brought them home.

While investors chase gold to get into something more stable than the dollar, producers aren’t keeping up. Gold production was down 3% last year, and it was flat in the most recent quarter.

Although mining companies are spending more on new production, especially in China and Russia, that’s not enough to offset dwindling output from mature mines.

Central banks hold a lot of gold, but they’re not interested in selling and in any case, they’re bound by an agreement that imposes limits on sales.

However, the road to the top won’t be a straight line, which means it makes sense to take advantage of the inevitable corrections.

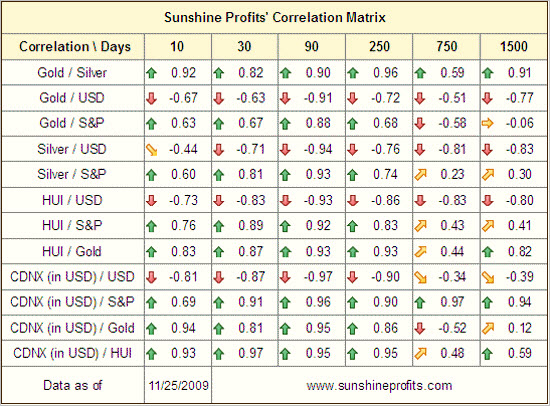

Let’s examine the chart of gold to check if we’re close to another buying or selling opportunity. In this essay, I’ll focus on the precious metals stocks.

The precious metals stocks are very close to their key resistance levels created by the March 2008 and July 2008 highs. The HUI Index has just moved above the latter resistance, so it’s likely to correct soon. The 500 to 525 area is still a possible target for this rally, but the risk of a sell-off has increased significantly after the very recent developments on this market.

Additional confirmation comes from the main stock indices.

Much has been written about how overvalued the general stock market is, and how likely it is that it will plunge immediately, after which stocks moved lower for a few days, but in the end rallied again and again.

However, the strength of the bearish signals has increased even further in the past few days. The divergence created by the NIKKEI Index moving visibly lower has become even bigger, but the most important bearish signal comes from the analysis of volume. The volume has been declining in the past several weeks along with rising stock prices, and the scale of this phenomenon has been remarkable.

Could this mean that the main stocks indices are likely to follow and move lower in the not-too-distant future?

Historical performance of the financial sector relative to other stocks confirms this, so the precious metals investors and speculators should at least take this possibility into consideration, especially that for now, precious metals remain positively correlated with the general stock market.

The values of the correlation coefficient are low in the long- (750 trading days) and very-long-term (1500 trading days) columns, but the analogous values in the short- (30 trading days) and medium-term (90 trading days) are positive. In other words, a plunge in the general stock market may have a negative impact on the precious metals market in the short term, but it won’t be the key driver of the precious metal prices in the long run.

Summing up, the precious metals stocks have moved very high very rapidly and this fact by itself suggests that a correction is to be expected. Since the HUI Index is just reaching its key resistance levels, a breather may materialize very soon. (See also, How to Capitalize on Gold’s Popularity)

Additional confirmation (the general stock market appears to be highly correlated with the precious metal stocks) comes from the general stock market, which may — finally — move lower.

Additional details are available in the full version of this essay, including the detailed short-term GDX chart along with projection of the next cyclical turning point.

To make sure you’re notified of new features (like the newly introduced Free Charts section), and get immediate access to my free thoughts on the market, including information not available publicly, sign up for my free e-mail list. Sign up today and you’ll also get free, seven-day access to the Premium Sections on my website, including valuable tools and charts dedicated to serious precious metal investors and speculators. It’s free and you may unsubscribe at any time.

Thank you for reading and have a great and profitable week!

Want more in-depth information, analysis, commentary and trading ideas? Minyanville offers subscription products designed to help you trade and invest with more intelligence from some of the best minds in the market. All come with 14 day free trials, so there’s nothing to lose.

We also offer great discount prices when you buy two or more products at the annual rates. Subscribe to any two annual products and get 20% off your total order. Subscribe to all three on an annual basis and get 25% off. Discounts will be reflected in your cart and at checkout.

For questions or more information about subscription products, please email support@minyanville.com or call 212-991-9357. If you wish to cancel your subscription during the trial period, you must email support@minyanville.com or call 212-991-9357

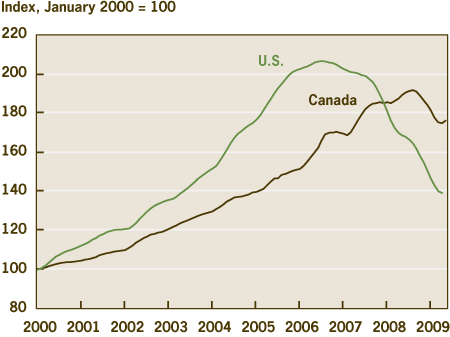

Housing markets in the United States and Canada are similar in many respects, but each has fared quite differently since the onset of the financial crisis. A comparison of the two markets suggests that relaxed lending standards likely played a critical role in the U.S. housing bust.

Despite their many points of similarity, housing markets in the United States and Canada have fared quite differently since the onset of the financial crisis. Unlike the U.S., Canada has not experienced a dramatic increase in mortgage defaults, nor has any Canadian bank required a government bailout. As a result, observers such as The Economist have pointed to Canada as “a country that got things right.”

The different housing market outcomes in Canada and the U.S. can tell us something about the underlying causes of the housing boom and subsequent bust. In particular, they can be used to evaluate the roles that low interest rates and relaxed lending standards played in the boom and bust.

Some observers blame monetary policy for lowering interest rates over 2002–2005, pushing up housing demand, increasing residential investment, and raising housing prices. In this view, the monetary-policy-induced housing boom thus set the stage for an inevitable housing bust.

Others contend that relaxed lending standards, highlighted by the rise in subprime lending, played a critical role. This loosening of standards led to an increase in housing demand, as mortgages were issued to households that were likely to have trouble making the mortgage payments. This extension of credit to risky borrowers helped fuel a housing boom and set the stage for the resulting surge in defaults, which were a big factor in the housing “bust.”

The Canada and U.S. housing market comparison suggests that relaxed lending standards likely played a critical role in the U.S. housing bust. Monetary policy was very similar in both countries from 2000 to 2008, but housing prices rose much faster in the U.S. than in Canada. This suggests that some other factor both drove the more rapid appreciation in U.S. prices and set the stage for the housing bust. A likely candidate is cross-country differences in the structure and regulation of subprime lending markets. That mortgage delinquencies began to climb before the recession in the U.S. but only began to rise recently in Canada (after the economic slowdown began), points to the significance of those structural and regulatory differences in explaining the U.S. housing crash.

Canadian and U.S. Housing Market Trends

Canada and the U.S. experienced significant increases in house prices and residential investment from 2000 to 2006, though prices in Canada appreciated more slowly. Figure 1 plots the S&P/Case-Shiller 20 city composite index and the (Canadian) Teranet-National Bank 6 city composite index. Both series are based on repeat sales, making these series a closer approximation to a “constant-quality” price index of nominal home prices than average house price sales. The Case-Shiller and Teranet series indicate that over 2000–2006, U.S. prices appreciated nearly twice as much as Canadian houses. However, Canadian house prices continued to appreciate until late 2008, and are now nearly 80 percent higher than in 2000.

1. Housing Prices

…..read more HERE.

As resource-hungry China scours the world for crude oil and natural gas supplies, it has managed to corner the global market for a group of obscure metals used to make iPods, wind farms and electric cars.

China supplies at least 95 percent of the world’s rare earths – 17 chemical elements with hard-to-pronounce names such as praseodymium and yttrium – essential for a wide range of high-tech devices and green technologies.

The nation has long recognised the value of these metals, with the late paramount leader Deng Xiaoping noting the Middle East had oil but China had rare earths.

And, as the Organization for the Petroleum Exporting Countries does with oil, China is tightly controlling the supply of these vital natural resources.

“China’s goal is to create jobs in China and create goods in China,” Jack Lifton, a US-based independent rare earths analyst, told AFP.

“We need to start producing these metals here (United States) as we did in the past. If we don’t do that, China will be the only country manufacturing devices using rare earths by the year 2015.”

A single mine in China’s northern Inner Mongolia region produces half of the world’s rare earths, with the rest coming from smaller mines in southern China as well as Russia, India and Brazil.

China keeps most of the minerals within its borders by restricting foreign shipments.

Authorities have been increasingly restricting exports in recent years as China seeks to prop up prices, ensure supply for its own needs and create jobs for millions of migrant workers by luring foreign companies to its shores.

“The government hopes that the restrictions could prompt the transfer of advanced rare earth processing technologies into China,” said Ren Xianfang, a Beijing-based economist with IHS Global Insight.

“Whether this resource-in-exchange-for-technology strategy will work in favour of China remains to be seen.”

Alarm bells started ringing this year amid reports that China’s State Council, or cabinet, was considering further tightening restrictions and even banning the export of certain elements as well as closing mines.

Foreign companies and governments fear the new rules, if implemented, will deny them access to the metals used to make everything from hybrid vehicles to missiles, and force manufacturers to shift their plants to China.

“It’s crunch time,” Dudley Kingsnorth, an Australian-based independent rare earths consultant, told AFP.

“In the next few years we are going to be in a situation where (export and production) quotas are reduced and unless we have sources outside China, more companies are going to have to relocate to China to secure access.”

On top of the minimal rare earth production in Russia, India and Brazil, deposits being developed in Australia and the United States will be able to produce about 50,000 tonnes of rare earths by 2014.

But with total demand expected to double to around 180,000 tonnes within five years and China shutting the door on foreign buyers, analysts fear this may not be enough to meet global needs.

“Supply and demand are going to start to be fairly tight from 2012 to 2014,” said Kingsnorth.

“If there’s a delay in those projects (in the United States and Australia), we are going to have real issues. There won’t be enough rare earths.”

Ed Note: Also see:

This trickle is sure to become a flood. Automaker of rechargeable batteries, Sanyo Electric, has got support for its lithium-ion batteries by winning the first two customers for its plug-in hybrid vehicles.

Though not the first automobile firm to cosy upto plug-in models and electric cars that use lithium-ion cells, that are lighter and more powerful, Sanyo joins the elite group of firms that are sourcing customers across the world who are `green’ in their outlook, and don’t mind paying a bit more for their creature comforts.

Russell, I need income. Is there any place where I can get a decent yield?

Answer — I agree with Bill Gross. If I wanted yield, I’d go to the unloved utilities, a sector containing some of my long-time favorites – Richard Russell Dow Theory Letters

The Federal Reserve’s policy of pegging interest rates to the floor is having a slew of consequences. It’s driving down the dollar. It’s helping fuel new asset bubbles. It’s leading to the misallocation of economic resources.

And perhaps most importantly for you, it’s punishing savers. By cutting the federal funds rate to a range of zero percent to 0.25 percent, the Fed has forced rates on short-term Treasuries, short-term certificates of deposit, and money market accounts into the gutter. You can’t earn squat on these safe, cash-like investments.

So where can you turn for the income you need to pay your bills … support your family … and maybe someday help put your grandkids through college?

You know I don’t like long-term Treasuries because Washington is torpedoing this nation’s balance sheet. And I’m not a big fan of most longer-term U.S. debt, including corporate and junk bonds. They’ve rallied so far, so fast that they’re looking dramatically overvalued.

Instead, I have three alternatives that are worth considering. Let’s talk about them now …

Income Alternative #1:

MLPs Offer a Nice Way to Hunt For

Yield in the Energy Sector

We’ve seen a sharp rally in the price of all kinds of energy products. Crude oil prices have surged 139 percent from last December. Gasoline is up 157 percent. Heating oil costs almost twice what it did last winter. Even lowly natural gas has climbed from around $2.40 per million British Thermal Units to around $4.50 now.

But let’s be honest … the business of exploring for, producing, and trading energy is relatively high risk. You can spend years and hundreds of millions of dollars drilling for oil and gas. If the price tanks somewhere along the line, your investment can blow up in your face!

Yet consumers and businesses never completely STOP using energy, regardless of the cost. That means the industry still needs to store and transport gas, oil, and other petroleum-based products around the country each and every day.

That’s where energy Master Limited Partnerships, or MLPs, come in. These companies own many of the storage and distribution networks that energy companies use to get their products to market.

They get paid whether energy prices rise or fall. And because of how they’re organized (in the corporate sense), they spin off handsome dividends. It’s not unusual to see yields of 5 percent, 6 percent, 7 percent, or more in the sector.

Don’t get me wrong: MLPs still trade like stocks. So there’s definitely price risk involved. But I believe they’re a solid alternative for yield-starved investors.

Income Alternative #2:

Utilities Spinning Off More Income

Than Any U.S. Treasury

Another sector that offers juicy yields: Utilities. That includes natural gas providers, electric companies, and even telecommunications firms.

These businesses clearly aren’t recession proof. When the economy tanks, so does demand for power and telecommunications services. But the swings are typically much less severe than what you see in housing, technology, or manufacturing. And even during the worst downturns, those core businesses still tend to spin off healthy amounts of cash.

Again, you don’t have to look very hard to find handsome dividend yields in the sector. Many leading utilities yield at least 5 percent or 6 percent. That’s better than you can get anywhere on the Treasury curve, considering that even 30-year bonds yield just 4.31 percent.

That’s not all, either. I’m seeing a heck of a lot of healthy stock charts in the sector, with breakouts all over the place. Buy the right stock at the right time and you can earn a juicy yield AND rack up some capital gains.

Income Alternative #3:

Go West … East … South

Anywhere but Here!

Of course, you don’t have to keep all your fixed income money in the U.S. if you don’t want to. In fact, you probably shouldn’t!

Why? The dollar has been falling virtually nonstop for months now. That hurts foreign owners of our debt. But the process works in REVERSE for U.S.-based investors.

If you buy a foreign, fixed income security, and the dollar falls, the dollar value of your holdings RISES. Any principal and interest payments you receive in the foreign currency translate back into more dollars when you repatriate the money.

On top of that, foreign yields are much more attractive than those offered here in the U.S. Two-year Treasuries yield just 0.77 percent here in the U.S. But the same maturity security yields 1.16 percent in Canada … 1.35 percent in Germany … and 1.65 percent in Spain. In New Zealand, you’re looking at 4.03 percent. In Australia, 4.32 percent. In Indonesia, 5.2 percent.

Bottom line: You can earn higher yields AND get a currency “kicker” by investing in foreign, fixed income securities. Foreign dividend-paying stocks are another alternative. Many yield much more than their U.S. counterparts.

Until next time,

Mike

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

“U.S. President Barack Obama announced the broad structure of his Afghanistan strategy in a speech at West Point on Tuesday evening”.

The strategy had three core elements. First, he intends to maintain pressure on al Qaeda on the Afghan-Pakistani border and in other regions of the world. Second, he intends to blunt the Taliban offensive by sending an additional 30,000 American troops to Afghanistan, along with an unspecified number of NATO troops he hopes will join them. Third, he will use the space created by the counteroffensive against the Taliban and the resulting security in some regions of Afghanistan to train and build Afghan military forces and civilian structures to assume responsibility after the United States withdraws. Obama added that the U.S. withdrawal will begin in July 2011, but provided neither information on the magnitude of the withdrawal nor the date when the withdrawal would conclude. He made it clear that these will depend on the situation on the ground, adding that the U.S. commitment is finite.

Related Special Topic Page

In understanding this strategy, we must begin with an obvious but unstated point: The extra forces that will be deployed to Afghanistan are not expected to defeat the Taliban. Instead, their mission is to reverse the momentum of previous years and to create the circumstances under which an Afghan force can take over the mission. The U.S. presence is therefore a stopgap measure, not the ultimate solution.

The ultimate solution is training an Afghan force to engage the Taliban over the long haul, undermining support for the Taliban, and dealing with al Qaeda forces along the Pakistani border and in the rest of Afghanistan. If the United States withdraws all of its forces as Obama intends, the Afghan military would have to assume all of these missions. Therefore, we must consider the condition of the Afghan military to evaluate the strategy’s viability.

Afghanistan vs. Vietnam

Obama went to great pains to distinguish Afghanistan from Vietnam, and there are indeed many differences. The core strategy adopted by Richard Nixon (not Lyndon Johnson) in Vietnam, called “Vietnamization,” saw U.S. forces working to blunt and disrupt the main North Vietnamese forces while the Army of the Republic of Vietnam (ARVN) would be trained, motivated and deployed to replace U.S. forces to be systematically withdrawn from Vietnam. The equivalent of the Afghan surge was the U.S. attack on North Vietnamese Army (NVA) bases in Cambodia and offensives in northern South Vietnam designed to disrupt NVA command and control and logistics and forestall a major offensive by the NVA. Troops were in fact removed in parallel with the Cambodian offensives.

Nixon faced two points Obama now faces. First, the United States could not provide security for South Vietnam indefinitely. Second, the South Vietnamese would have to provide security for themselves. The role of the United States was to create the conditions under which the ARVN would become an effective fighting force; the impending U.S. withdrawal was intended to increase the pressure on the Vietnamese government to reform and on the ARVN to fight.

Many have argued that the core weakness of the strategy was that the ARVN was not motivated to fight. This was certainly true in some cases, but the idea that the South Vietnamese were generally sympathetic to the Communists is untrue. Some were, but many weren’t, as shown by the minimal refugee movement into NVA-held territory or into North Vietnam itself contrasted with the substantial refugee movement into U.S./ARVN-held territory and away from NVA forces. The patterns of refugee movement are, we think, highly indicative of true sentiment.

Certainly, there were mixed sentiments, but the failure of the ARVN was not primarily due to hostility or even lack of motivation. Instead, it was due to a problem that must be addressed and overcome if the Afghanistation war is to succeed. That problem is understanding the role that Communist sympathizers and agents played in the formation of the ARVN.

By the time the ARVN expanded — and for that matter from its very foundation — the North Vietnamese intelligence services had created a systematic program for inserting operatives and recruiting sympathizers at every level of the ARVN, from senior staff and command positions down to the squad level. The exploitation of these assets was not random nor merely intended to undermine moral. Instead, it provided the NVA with strategic, operational and tactical intelligence on ARVN operations, and when ARVN and U.S. forces operated together, on U.S. efforts as well.

In any insurgency, the key for insurgent victory is avoiding battles on the enemy’s terms and initiating combat only on the insurgents’ terms. The NVA was a light infantry force. The ARVN — and the U.S. Army on which it was modeled — was a much heavier, combined-arms force. In any encounter between the NVA and its enemies the NVA would lose unless the encounter was at the time and place of the NVA’s choosing. ARVN and U.S. forces had a tremendous advantage in firepower and sheer weight. But they had a significant weakness: The weight they bought to bear meant they were less agile. The NVA had a tremendous weakness. Caught by surprise, it would be defeated. And it had a great advantage: Its intelligence network inside the ARVN generally kept it from being surprised. It also revealed weakness in its enemies’ deployment, allowing it to initiate successful offensives.

All war is about intelligence, but nowhere is this truer than in counterinsurgency and guerrilla war, where invisibility to the enemy and maintaining the initiative in all engagements is key. Only clear intelligence on the enemy’s capability gives this initiative to an insurgent, and only denying intelligence to the enemy — or knowing what the enemy knows and intends — preserves the insurgent force.

The construction of an Afghan military is an obvious opportunity for Taliban operatives and sympathizers to be inserted into the force. As in Vietnam, such operatives and sympathizers are not readily distinguishable from loyal soldiers; ideology is not something easy to discern. With these operatives in place, the Taliban will know of and avoid Afghan army forces and will identify Afghan army weaknesses. Knowing that the Americans are withdrawing as the NVA did in Vietnam means the rational strategy of the Taliban is to reduce operational tempo, allow the withdrawal to proceed, and then take advantage of superior intelligence and the ability to disrupt the Afghan forces internally to launch the Taliban offensives.

The Western solution is not to prevent Taliban sympathizers from penetrating the Afghan army. Rather, the solution is penetrating the Taliban. In Vietnam, the United States used signals intelligence extensively. The NVA came to understand this and minimized radio communications, accepting inefficient central command and control in return for operational security. The solution to this problem lay in placing South Vietnamese into the NVA. There were many cases in which this worked, but on balance, the NVA had a huge advantage in the length of time it had spent penetrating the ARVN versus U.S. and ARVN counteractions. The intelligence war on the whole went to the North Vietnamese. The United States won almost all engagements, but the NVA made certain that it avoided most engagements until it was ready.

In the case of Afghanistan, the United States has far more sophisticated intelligence-gathering tools than it did in Vietnam. Nevertheless, the basic principle remains: An intelligence tool can be understood, taken into account and evaded. By contrast, deep penetration on multiple levels by human intelligence cannot be avoided.

Pakistan’s Role

….read more HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair