Daily Updates

THE NEW YEAR, LITHIUM IDEAS

by Michael Berry

Even with the looming problems discussed above, I still like discovery opportunities because they are inherently cheap. I have become active in the lithium market. I have reduced a position in Western Lithium (WLC TSXV) after a significant run-up in WLC shares last week.

Solares Lithium Inc. (LIT TSXV) is a new and interesting incubator company with very large lithium properties in Chile.

…..read more of Michael’s report on Solares HERE as well as his commentary on unemployment and the markets

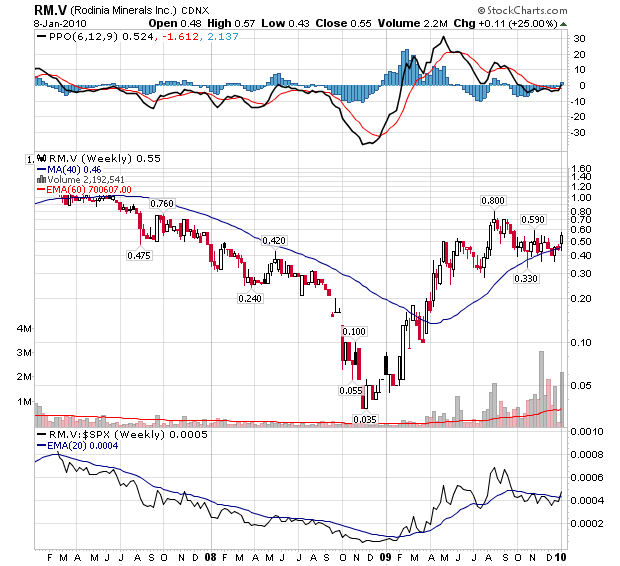

Rodinis Minerals, A Key Player for Made-In-America Bateries and Electric Cars

As noted in my initial commentary, one of the key reasons I am especially high on Rodinia Minerals is the smart strategy by which management is building the business. Rodinia’s management team believes the lithium bonanza is only beginning as the forecasted demand for lithium far outweighs the known availability of supply. As lithium-ion batteries become increasingly important in the automobile industry’s plans to reduce the use of fossil fuels, the green-car revolution could make lithium one of the planet’s most strategic commodities. Rodinia, and its focus on becoming a low-cost lithium producer in the near-term, appears well positioned to deliver into this supply-demand gap.

In my view, the risk/reward pendulum has swung a little more in Rodinia’s favor after two important announcements at the end of last week validated management’s lithium demand believes:

GM Builds First Lithium-ion Battery for Chevrolet Volt (Thursday)

Obama Announces $2.3 Billion in Clean Energy Tax Credits (Friday) in Follow-Up to $2.4 Billion in Grants for Batteries and Electric Cars

Currently, there exists only one producing lithium operation in North America and it is encompassed by Rodinia’s flagship Clayton Valley Project in Nevada. These announcements appear to only begin to define the demand for lithium in the United States but they go a long way towards possibly positioning Rodinia as the supplier of choice for made in America batteries and electric cars!

GM Builds First Lithium-ion Battery for Chevrolet Volt

On January 7, 2007, GM launched the Chevrolet Volt electric car concept. Since that time, the focal point of its advancement has been the development of a long-lasting, quick-charging lithium-ion battery. Exactly 3 years from its debut, GM successfully manufactured the first advanced lithium-ion battery for a mass-marketed electric vehicle at its Brownstown Battery Pack Assembly Plant.

“The development of electric vehicles like the Chevy Volt is creating entire new sectors in the auto industry – an ‘ecosystem’ of battery developers and recyclers, builders of home and commercial charging stations, electric motor suppliers and much more,” said GM Chairman and CEO Ed Whitacre. “These companies and universities are creating new jobs in Michigan and across the U.S. – green jobs – and they’re doing it by developing new technology, establishing new manufacturing capability, and strengthening America’s long-term competitiveness”, he went on to say.

In order for the Volt to reshape the automobile industry and become a prominent fixture on our streets, GM will need a reliable, low-cost source of lithium to build the lithium-ion battery. Rodinia’s Clayton Valley can represent an ideal American solution for procuring this key ingredient.

48 Different Projects Will Share the Loot from Obama’s $2.4 Billion in Grants for Batteries and Electric Cars

President Obama recently announced the allocation of $2.4 billion dollars from the Recovery Act to be divided up amongst 48 different battery and electric vehicle projects. “With these investments, we’re planting the seeds of progress for our country and good-paying, private-sector jobs for the American people,” he said. The majority of grant winners are familiar names, with Detroit firms obtaining a substantial share.

The money is going to three main categories of projects:

1 – $1.5 billion to US-based manufacturers for production of batteries and their components

2 – $500 million to US-based manufacturers producing electric drive components for vehicles and

3 – $400 million in grants to purchase plug-in hybrid and all-electric vehicles to test demonstrations in several locations.

It is becoming quite clear that we are going to push forward with great might to make the era of the electric car a reality. While 48 different projects have been awarded funding, the bulk of the money, and the near-term success of the initiative, seems to revolve around the lithium-ion battery.

Last Friday, President Obama broadened his stimulus package to include $2.3 billion in clean energy tax credits focused on renewable energy production and storage (batteries).

Bottom Line

The electric car era is still very much in its infancy, but it is undoubtedly coming. GM appears to be staking its future on it, and President Obama has opened up the coffers for $2.4 billion to see it happen.

The development of renewable/alternative power sources is also becoming a reality. As this occurs, we will need batteries to assist in the storage of alternative power generated during peak production time.

Lithium-ion batteries appear to be the leading battery technology. They also represent the single largest limiting factor in the development of electric cars and alternative energy storage. In order for these initiatives to succeed, I believe we need lithium to build batteries.

Rodinia Minerals is a potential source of low-cost lithium ideally situated to serve the U.S. market from its flagship asset in Nevada.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

As long as it stays above the rising 200 week-moving average, the increase is 18% per year

“The State is that great fiction by which everyone tries to live at the expense of everyone else.” ….. Frederic Bastiat.

“Those who buy the dips and ride the waves will prosper” Richard Russell.

The bullish case for gold continues to build. The old adage ‘more dollars chasing fewer goods’ is particularly apt for gold.

- For the first time in history practically every Central Bank is adding to the money supply of its respective country.

- Despite a record high gold price, new supply from mines is declining, due to the fact that the ‘easy to find gold’ has already been found.

…..read reasons 3-15 and view charts HERE.

Editor Note: Money Talks highly recommends that you make a regular trip to this monday morning site to this Don Vailoux monday report where he analyses an astonishing 40 to 50 Stocks, Commodities and Index charts and, provides a “Bottom Line” and some very interesting commentary.

– a few of the 40+ charts and commentary below. Full site HERE.

Be sure to check out Don’s bottom Line at the bottom of his chart analysis HERE.

Economic news is mixed this week.

The November U.S. Trade Deficit to be released on Tuesday at 8:30 AM EST is expected to increase to $34.5 billion from $32.9 billion in October.

December Retail Sales to be released on Thursday at 8:30 AM EST is expected to increase 0.5% versus an increase of 1.3% in November. Ex autos, retail sales are expected to increase 0.3% versus an increase of 1.2% in November.

November Business Inventories to be released on Thursday at 10:00 AM EST is expected to increase 0.2% versus an increase of 0.2% in October.

December Consumer Price Index to be released on Friday at 8:30 AM EST is expected to increase by 0.2% versus a 0.4% increase in November. Ex food and energy, CPI is expected to increase 0.1% versus no change in November.

December Capacity Utilization to be released on Friday at 9:15 AM EST is expected to increase to 71.8% from 71.3% in November.

December Industrial Production to be released on Friday at 9:15 AM EST is expected to increase 0.6% versus a 0.8% increase in November.

The January Michigan Sentiment Index to be released on Friday at 9:55 EST is expected to increase to 73.8 from 72.5 in December.

Earnings News This Week

Fourth quarter earnings start to trickle in this week. Focuses are on Alcoa, Intel and JP Morgan.

Monday sees Alcoa

Tuesday sees KB Homes

Wednesday sees Cogeco

Thursday sees Intel and Shaw Communications

Friday sees JP Morgan

Equity Index Trends

The ratio of S&P 500 stocks in an uptrend to a downtrend (i.e. the Up/Down ratio) increased last week from 4.37 to (381/63=) 6.05. The ratio remains intermediate overbought.

Bullish Percent Index for S&P 500 stocks increased last week from 79.40% to 82.40%. The Index remains intermediate overbought and above its 15 day moving average.

The Up/Down ratio for TSX Composite stocks advanced from 6.54 to (166/24=) 6.92. The ratio remains intermediate overbought.

Bullish Percent Index for TSX Composite stocks increased last week from 79.70% to 81.68%. The Index remains above its 15 day moving average. The Index remains intermediate overbought.

……read more and be sure to check out Don’s bottom Line at the bottom of his chart analysis HERE

Recovery in auto market, new ETF add to demand

Platinum has a period of seasonal strength from January to May. What are the prospects for a profitable seasonal trade this year?

…..read more HERE.

In the past few decades,the specter of the “double-dip recession” has established itself in the collective consciousness of the American public as a sort of phantasm that lurks just around the corner of every economic recovery. Judging by the frequency and intensity of the media attention that it garners, the fear of this economic menace has become deeply ingrained in the American public.

How justified are these fears? How likely is it that such an event will occur in 2010?

A History of Double-Dip Recessions

To compute the odds of a given event occurring, it helps to understand when and how such events have occurred in the past.

We should first define what a double dip recession is. For purposes of this article, we shall adopt the most common definition utilized by economists — and one which also happens to make common sense: A double dip recession is an occurrence whereby the US economy enters into a recession within a period less than 12 months following the end of the previous recession.

According to the National Bureau of Economic Research (NBER), the most authoritative source of information regarding business cycles, there have been 33 recessions registered in the US since 1854. Over this entire time frame, there have been only three recorded instances of a double-dip recession by this standard definition. The first one was in 1913, the second in 1920, and the third in 1981.

(Note: If we make the definition of a double-dip more expansive, including all recessions within 18 months of the end of the previous recession, the number of occurrences of double-dips rises only slightly to five.)

So let us summarize the history of double-dip recessions according to the standard definition: There were two instances of double-dips in the 91 year period from 1854 to 1945, which comprised a total of 22 business cycles. And there was just one instance a double-dip in the 11 business cycles that took place during the 65 years that have transpired since 1945.

That’s it.

So, what can we surmise from this information? Historically speaking, a double-dip recession is an extraordinarily rare occurrence; almost insignificant from a statistical point of view.

Furthermore, from an analytical standpoint, it’s doubtful whether a “double-dip recession” is even a distinct category of economic event that’s worthy of study, or even mention. For there’s virtually nothing which the three double-dip recessions share in common that could identify them as belonging to a distinct category of economic phenomena. The nature and causes of the three recessions were so disparate that they appear to be entirely isolated events.

Conclusion: Double-dip recessions have been extremely rare and isolated events. There are virtually no historically derived indicators that could help one foresee such an unlikely phenomenon at this time.

Some Good Old Common Sense

Why have double-dips been so rare? Fortunately, the explanation happens to jive with common sense understandings and basic intuitions of how economies work.

First of all, most folks understand that the process of economic growth is a cyclical phenomenon.

Second, most folks can intuitively understand that the acceleration and deceleration of aggregate economic activity exhibits properties that are akin to the concept of momentum. Folks understand that the flow of activity in a large economy simply can’t and doesn’t turn on a dime. The reason for this inertia is, in part, that a large economy is comprised of millions of interrelated actors performing millions of interlinked transactions, most of which require considerable lead times to manifest (e.g. demand to design to financing to production to distribution through to final sale).

The key insight to take away is this: Once an economy has hit bottom and starts growing (even from a very low base), inertial forces take over and it’s extremely unlikely that the momentum will be halted in the early phase of the “bounce” off the trough. Furthermore, due to the low statistical baseline established during the trough, it’s overwhelmingly likely that economic growth will be reflected in the statistics in the period immediately following.

(Note: Just because an economy is growing doesn’t mean that it’s necessarily healthy or that its people are prosperous. It just means that the economy is growing.)

All of this brings us back to double-dips. A double-dip requires an abrupt halting and reversal of economic momentum immediately after passing through the trough and during the early part of the “bounce” phase. As such, conceptually speaking, such an event is highly unlikely by its very nature. And as we saw earlier, this basic prediction has been amply confirmed by the historical record.

Why Are We So Fixated on the Menace of a Double-Dip

….read page 2 HERE (wraps up with a percentage risk of a Double Dip)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair