Daily Updates

In September 1929, if a stock market forecaster had publicly proclaimed that the Dow was about to lose 90% of its value, would he have been subjected to ridicule.

“Nobody wants to hear bad news let alone believe it, even if it’s true. So when a virtually unknown financial and economic historian, such as myself, suggests a seemingly outrageous Dow target of 1,000, it is essentially dismissed as a prognostication of a ‘know nothing crank’. And everyone continues to buy stocks for the long term – isn’t that what the experts are telling them to do?”

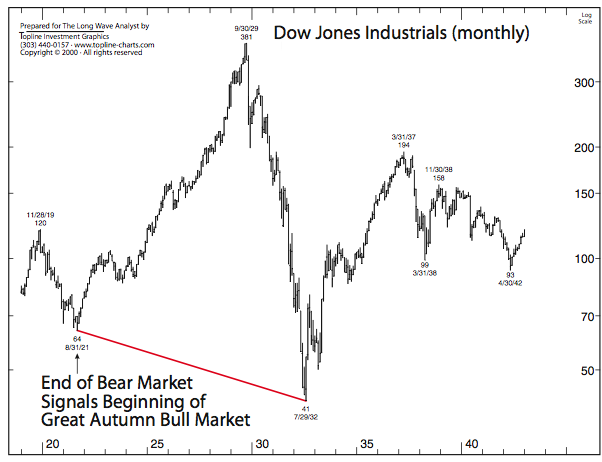

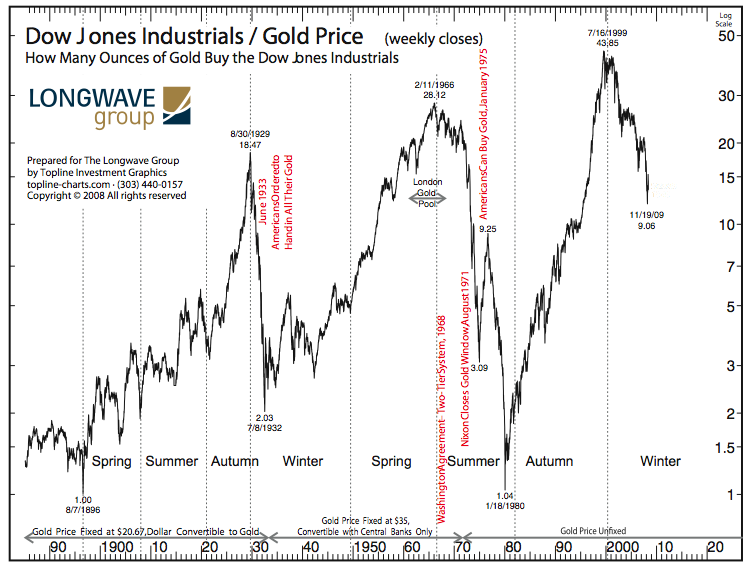

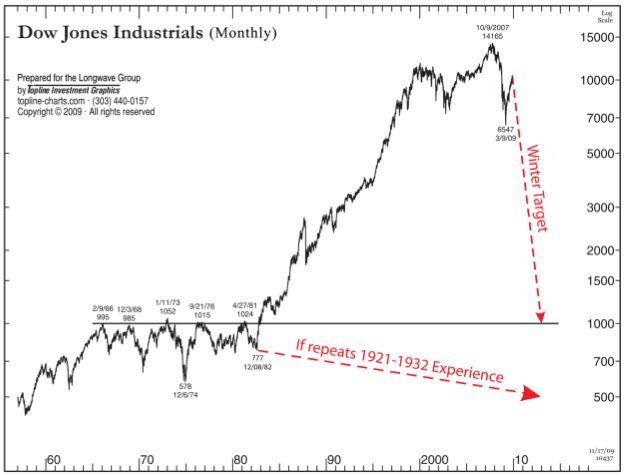

(Ed Note: an example of only three of the charts in this report)

History has recorded very few financial bubbles. Charles Mackay in his famous Extraordinary Popular Delusions and the Madness of Crowds, which was first published in 1841, covers three: The Mississippi scheme initiated in France by John Law in 1719-1720; The South Sea Bubble, an English experience, 1720-1721; and Tulip Mania, an extraordinary Dutch bubble in 1636. In his book, A Short History of Financial Euphoria, John Kenneth Galbraith writes about the same three bubbles and several American bubbles, including the crashes of 1837, 1873 and 1929, which ended the speculative manias of the 1st, 2nd and 3rd Kondratieff autumn periods and were followed by their respective winter depressions. Charles Kindleberger, in the latest edition of Manias, Panics and Crashes, published in 2005, lists 10, including the three discussed in Galbraith’s and Mackay’s books, the 1920s autumn stock price bubble, and the Japanese stock and real estate bubbles that burst in 1990.

What is yet to be documented in any detail are the mania markets of the 1980s and 1990s, which far surpassed the bubble of the 1920s in both size and diversification. There were no derivatives of any consequence in the 1920s. The real estate bubble that was fostered by the past chairman of the Federal Reserve, Alan Greenspan, far outdid the real estate bubble of the 1920s, which was centred on the development of suburbs outside the cities and the building of skyscrapers close to the city centres.

“Nobody likes a bear. Most people have too much money invested in stocks. They can’t afford to lose money and they don’t like people telling them that they are going to lose. They are linked together in a common interest. As such, they form part of a crowd and are governed by a collective psychology that is essentially irrational. “From the moment they form part of a crowd the learned man and the ignoramus are equally incapable of observation.” Le Bon, P. 23. “

…..read the whole analysis HERE.

A globally renowned economic forecaster, author and speaker, our founder, Ian Gordon, has garnered praise from many notable sources, including Robert Prechter in his book ‘Conquer the Crash’ and Eric Sprott, Chairman of Sprott Asset Management Capital. A student of economic and investment history and former investment advisor, Ian provides strategic investment advice to international and domestic fund managers, and numerous gold companies. Ian also travels internationally speaking about the Longwave Principle and his predictions in relation to the stocks, bond, real estate, commodities and gold markets. Visit the website HERE.

As fears of a dollar meltdown have loomed ever larger in recent years, major investors, including central banks, have moved significant portions of their cash reserves into the euro, the currency of the European Union (EU). And while it is true that the euro offers some shelter from the American economic catastrophe, the currency does come with baggage that investors should not ignore.

Introduced as an accounting medium in 1990, the euro became an actual currency in 1992. It is currently issued by 16 of the 27 EU member countries, representing some 329 million people. With almost $1 trillion in circulation, it is the world’s largest physical currency.

The birth of the euro was a stunning example of putting the cart before the horse. When it was first issued as a physical currency in 1999, the major states that participated were not yet united. Many believe that this premature introduction was done to hasten the political union. In hindsight, the strategy was successful. The single currency removed a key psychological barrier towards unification.

As soon as it made its debut, the euro quickly became the second largest currency held in the official foreign reserves of central banks. Major corporations and investors followed suit. By September 2007, former Fed chairman Alan Greenspan said it would be “absolutely conceivable that the euro will replace the dollar as the dominant foreign reserve currency, or will be traded as an equally important reserve currency.”

However, the structural problems that were so heavily debated at the birth of the EU remain unresolved. These uncertainties may undermine the euro as a viable dollar-alternative. Should recent economic strains continue unchecked, investors, institutions, and central banks may move heavily into gold as an ultimate “safe haven.”

In the U.S., monetary union depends upon political union. When California faces a crushing debt burden, it can neither print its own highly inflationary currency to ease the pressure (though its “IOU’s” are a haphazard attempt) nor leave the union to avoid this constraint. Thus, crises in U.S. states tend to push states toward the central government as they seek assistance from Uncle Sam. EU member states similarly lack their own printing presses and are therefore unable to monetize their problems. But in Europe, the emergency exit is always open – states can leave if they believe their interests are not being considered.

The EU does not have a common fiscal policy, so countries are free to bankrupt themselves according to their own decree. But when they do, there is no formal option of seeking a bailout from the pan-European government. Even if such a road were available under the EU treaties, the European Central Bank, modeled on the famously inflation-wary German Bundesbank, would be unwilling to monetize the additional spending.

Partially because of this stringent monetary policy, the euro has risen by some 40 percent against the dollar since its launch. This has severely hurt eurozone export economies like Spain, Portugal and Italy, who have long relied on currency devaluation to subsidize their manufacturers.

While countries like Germany, the world’s largest exporter, have been successful in utilizing the benefits of a strong currency to continue selling products at a real profit, others have failed. Indeed, both Italy and Greece now have government debts in excess of GDP (115% and 113%, respectively). Furthermore, Greece, with a budget deficit of some 12.7 percent of GDP, is now threatened with default.

Although the EU, by and large, currently spurns talk of a bailout for Greece, the debate will intensify if the economy deteriorates further. If, in order to preserve union, the EU does decide to bail out an individual member state, what precedent would that set?

Germany, the strongest EU economy, found it a Herculean task to bail out just 17 million people in the former East Germany. Could it even contemplate bailing out not one, but several other EU member states, without attendant political control?

There seems little room to move forward under the status quo. Though the Lisbon Treaty (read: EU constitution) just came into effect, it was passed without the mandate of citizen referenda. The member states remain culturally distinct, the citizens have little allegiance to the behemoth in Brussels, and, therefore, it seems far-fetched that the EU would go to war to compel one of its members to remain in the club. With little to glue it together, investors are questioning whether the eurozone is strong enough to withstand the shocks that would accompany a dollar collapse.

As the credibility of the U.S. dollar has eroded and that of the euro is now suspect, it is likely that investors will continue their quiet rush into gold. If so, silver is likely to become a store of value for smaller investors and the small change of the rich. In such a world, the price of silver could rise even faster than that of gold.

Investors are bullish because China’s exports are recovering, says the new analysis. Meanwhile, celebrated short-seller Jim Chanos says China is going to blow up. It’s going to be “Dubai times 1,000,” he says. Jim Rogers disagrees. He thinks Chanos hasn’t looked long enough or deeply enough into the China story. He thinks China is a buy. The debate between Chanos and Rogers is captured below:

BEIJING (Commodity Online): Is the Chinese economy is caught on the verge of a bubble? That is the heated discussion these days among global analysts, investing pundits, hedge fund managers and economic experts.

In the last two months, the booming gold price was the epicenter of another bubble debate with celebrated investors such as Jim Rogers, Jim Sinclair, Nouriel Roubini and Marc Faber passionately discussing their arguments and counter arguments on whether gold price was in a bubble or not.

China has, indeed, been the fastest growing economy in the 2000-2009 period. There has been a boom in commodities production and consumption in China. China has overtaken several countries including India, US, Australia and South Africa in the consumption and production of several commodities including base metals and bullion.

There has been a flood of bank lending in China that has been boosting the Chinese appetite for manufacturing, gold mining, agriculture, farming etc. But is it all over?

Will this economic boom in China end soon? Noted global hedge fund manager Jim Chanos says China is in a bubble that will burst soon. He says there are some serious problems with Chinese disbursement of bank lending.

Chanos says that China’s economy is overheated and thus will burst badly. According to him the Chinese economy is being over-stimulated by its stimulus program of $586 billion dollars. Most of this money is going into speculation and overproduction of goods that China will not be able to sell.

Chanos names this as: “Dubai times 1000 — or worse.” Saying that China is cooking its books, and faking its spectacular growth of more than 8%, Chanos has predicted: “Bubbles are best identified by credit excesses, not valuation excesses.”

Will the Chinese economy collapse the way Chanos is forecasting? Please note that Chanos is not a newcomer to the world of short selling. He accurately predicted the collapse of Enron and several other shaky companies over the past several years. He is one of a breed of “short sellers.”

But global commodities investing guru Jim Rogers has blasted Chanos for what he has said on China. Rogers, who has been passionately investing in China for the last few years, says that China is not in a bubble as Chanos has predicted. Rogers, who shifted his residence to Singapore two years back as he felt that Asian countries like China have huge investment potential, says that Chinese economy is on strong and sound foundations.

Rogers points out that Chanos may not know the fundamentals of the Chinese economy and the basics of ‘bubbles.’

Recently, Rogers had a war of words with Roubini on gold bubble. Roubini had predicted that gold price is sitting on a bubble and the ideal price for gold was around $1,000 per ounce. Roubini’s comments came as gold price zoomed to touch a historic record of $1,227 per ounce in November last year.

Rogers lambasted Roubini’s lack of fundamentals on gold and said that the yellow metal was set to cross $2,000 per ounce in the next decade.

Now that Jim Rogers and Jim Chanos are warring over the China bubble, who will be the winner in bubble forecasting game? Let us wait and watch for their next utterances.

….more great articles at Commodity Online

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

Again, for simple comparison’s purposes, the previous year saw America’s farmers growing 162.9 bushels of corn/acre, and the year previous it was 153.9… and remember, it was not that many years ago that we were growing less than 100 bushels/acre, and indeed as the chart included here this morning… one of our truly favourite charts given that it shows the enormous productive gains enjoyed by America’s farmers but barely understood by America’s consumers…it was only in the 80’s that we broke above and have remained permanently above that figure!]. How much of that corn was left in the fields is anyone’s guess, and it is indeed a guess, for even once we have a strong figure on the sum of acreage left there it is a further guess as to how much of that corn is truly lost.

GOLD IN STERLING TERMS:

New Highs Lie Just Ahead: We are and have been bullish of gold, but in non‐US$ terms and that risk aversion has served us well for as gold broke more than 11% in US dollar terms in the December market-clearing correction, it fell by half that in EUR terms. In other words, rather than facing a material loss of funds that might have been debilitating, we lost a much more amenable sum which we far more readily survivable and we’ve been well served being so. The market has advanced; it has consolidated; it has advance and it has consolidated again and again. We are heavily involved and we intend to remain so.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

There are very few “mainstreet” people I take the time to listen to but ironically, two of them both had long careers at Merrill Lynch before moving on. One is economist David Rosenberg and the other is Technical Analyst Walter Murphy – Peter Grandich

IS THE CANADIAN HOUSING IN SOME SORT OF BUBBLE?

Well, when price-to-rent and price-to-income ratios are between 15% and 35% overvalued, you know that something isn’t quite normal. Not to mention the fact that mortgage debt relative to after-tax income and homeownership rates have hit all-time highs. And even with extremely low interest rates, affordability is tied for its lowest level on record because of the fact that average home prices have exceeded wage growth by such a wide margin over the past year.

But until recently, most housing markets were tight in terms of sales-to-listing ratios and the like. The catalyst to any bubble is usually the supply response, which is why the 5.9% bounce in Canadian housing starts in December, to 175k (annualized) units, was less “optimistic” than it seems on the surface — notwithstanding the boost to current GDP estimates. Canadian housing starts are now up 47% from their 2009 lows and there is likely more construction in the pipeline because residential permits soared 9.7% alone in November and are up four months in a row — and up 72% from their 2009 lows.

As an aside, when central bank officials begin to dismiss the possibility there being at the least excesses in the real estate market (the word “bubble”, we can assure you from our previous life in the U.S.A., is extremely emotive), it conjures up the image of all the folks at the Fed who said the same thing back in 2004, 2005 and 2006. Go back and read the speeches by the Fed officials during those years and you will probably end up chuckling.

Ed Note: other topics in Today’s Breakfast with Dave below or just read more HERE.

• While you were sleeping — equity markets overseas posting declines today in the aftermath of Alcoa’s miss; economic data globally were actually constructive

• Three major risks to the outlook — energy prices, mortgage rates and home prices

• Sentiment on the U.S. equity markets very bullish … from a contrarian standpoint, this is bearish

• Valuation estimates on the S&P 500 — a combination of valuations and technical factors imply that the level on the S&P 500 ranges from a low of 840 and a high of 1,350

…..read more HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair