Daily Updates

Richard Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. HERE to subscribe. Amongst his achievements Richard was in cash before the 2008/2009 Crash and he has been Bullish Gold since below $300

Ed Note: Richard Russell is bullish Silver and holds one of the largest single positions he has held since the 1950’s in the precious metals.

Today, nobody’s got any cash. And if they do have cash, they don’t know what to do with it. We just sold the house I’ve been living in for the last 30 years. And I wonder what to do with the money we’ll receive on the sale. Should I try to bring in some income? Or should I play it as safe as I can? Thirty years ago I wouldn’t have had this “problem.” I could have bought government notes or bonds and received safe income. Today I will wait with the money and see what comes up. But waiting with dollars is a risk, because I have no faith in the dollar as a store of value.

Maybe I should just say, “The hell with it,” and buy more gold. With T-bills at a negative yield, I’m not sacrificing anything when I buy gold — at least gold can’t go bankrupt. And great — gold is outside of the banking system. No damn fool can devalue gold. But I don’t trust the government to refrain from devaluing the dollar (after all, Roosevelt did it, and Obama seems to follow Roosevelt’s lead, although FDR was a conservative compared with O-bummer).

I watch what Bill Gross, master-mind of PIMCO, is doing. He runs the world’s largest bond fund, and he must think in terms of both safety and income. So what is he doing? From what I gather, he’s getting rid of US government debt and buying non-dollar bonds. Somehow, bonds of any kind don’t appeal to me. Gross likes the preferred of some banks, and that’s not a bad idea. But it sounds a bit risky and mysterious. After all, who knows what these banks will come up with next? I just don’t trust them, and I’m convinced they’re still loaded with toxic assets which they refuse to mark to market.

I think I’ll do what I’ve been recommending all along. I’ll sit with mostly gold and the rest in cash. Cash isn’t worth much these days, but it does allow you time to think. And best of all, and miracle of miracles, people continue to accept cash (Federal Reserve notes) for items of intrinsic value such has gold, silver, real estate, diamonds, guns, art objects, all items that should be worth something 25 years from now.

I’ve said this before. Up to now the goal in investing was to produce a profit. You hoped that whatever you bought could be sold in a year or so for more than you paid. I don’t think that way any more. I think in terms of how I can avoid losing purchasing power. It’s a true reversal — from how to win it — to “how not to lose it.”

The 85 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold. There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

NO BUBBLE, EH?

Toronto, the largest housing market in Canada, started the year off with a bang, with existing home sales jumping 87% year-over-year from last January (albeit from a very depressed level). Median home prices climbed 15% YoY and average prices saw an evenbigger 20% jump to nearly $410,000. Inventories of active listing declined 41% YoY and homes sold more quickly (average of 28 days versus 49 days last January).

The national housing market has also seen a rebound in recent months and has gotten the attention of government officials (although most say we are not in a bubble — shades of the U.S. denial circa 2005-06). There has been some chatter in the media that the Finance Minister, Jim Flaherty, may increase the current down payment requirement (currently 5%) and decrease the amortization length of a mortgage to 25 years in order to cool the housing market.

Click HERE or on the Banner for topics below:

.

Trends for Stocks & Commodities: Gold, Oil and Indexes

Stocks and metals have been on a steady rise this week. The US Dollar drifting lower has helped to add fuel to the oversold bounce in equities and metals we are seeing.

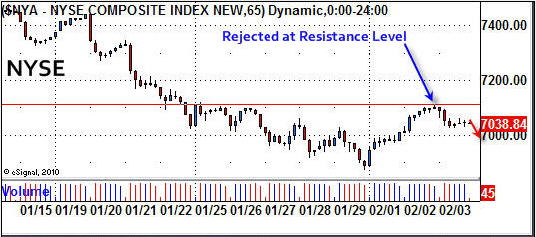

Stocks – NYSE 65 Minute Chart

Stocks have started to show signs of a possible reversal to the upside. So far this week we have seen the major indices form a higher high and as of today are stuck under the key resistance level shown on the chart below. The rally seen this week has been on light volume indicating there is not much strength behind it at this time.

If buying volume picks up and we see the NYSE break this resistance level then money should start to pour back into the market as the first set up of higher highs and lows will have formed and that is the definition of an up trend.

Gold – 24 Hour Trading Chart Using 8 Hour Bars

This chart allows us to look far enough back to see key support and resistance levels. Today we saw gold sell down with rising volume which is bearish.

Oil – 10 Hour Candle Chart

The Oil fund is currently in the same situation as gold. It had a nice rally/bounce which was expected from the rather large sell off over the past couple weeks.

US Dollar Index – 2 Hour Chart

This chart shows the dollar rally that triggered the recent sell off in gold & silver from Jan 25th to Jan 31st. So far in February, the dollar has drifted lower into a support level and bounced sharply on Wednesday. This is very bullish price action and points to higher dollar prices in the near future.

Stock & Commodity Trading Conclusion:

In short, stocks and metals rallied on light volume which is a sign of weakness. They are both stuck under a key resistance level and selling volume has started to pickup. To add more logs to the fire, the US Dollar appears to be picking up speed for another surge higher in the next couple days.

All of this leads me to believe this weeks rally is just a dead cat bounce and lower prices are just around the corner. But, because the 60 minute intraday charts have made a higher high, the down trend is now in question. When in doubt, just stay out. During possible tops or bottoms I find it best to stay clear of the market, even for day traders unless there are very strong price and volume surges occurring.

If you would like to receive these free trading reports please visit my website:

My name is Chris Vermeulen, founder of TheGoldAndOilGuy newsletter. I provide you with unparalleled trading newsletter with charts, signals and email support. Unlike other investing newsletters, I’m a one man show. That’s because I don’t want some hired hand giving you advice while I take it easy on a beach somewhere. You ALWAYS get precise, valuable information DIRECTLY from ME.

Interview: Trading Expert Helps Investors Learn the Ropes

Testimonial: Chris, Your reports are technical and thoughtful and above all you are cautious. I learn something from every report. WH Toronto.

I believe this is the perfect trading service for active traders who want a conservative yet highly profitable trading strategy and signals. The GLD Gold exchange traded fund allows for very accurate signals when used along with the price of gold, HUI, USD, bullish percent charts and gold stocks. I also focus on Oil, Silver, Natural Gas, Index & Sector ETFs. When these factors are used together with technical analysis and my proven trading strategy, b

Quotable

“I refuse to join any club that would have me as a member.” – Groucho Marx

FX Trading – The Gold Club (or religion of gold)

My father in law wrote yesterday to give me grief about my recent gold forecast/guess as laid out in a recent Currency Currents. So happy he was with the recent bounce off the support level in the yellow metal (see weekly gold chart below).

I’m used to the well-deserved harangues from him. But I think he is way too complacent about his position. I have concluded that most who like gold do not like it for its investment quality—it is pure and simple a religion. Thus, negative talk about one’s religion cannot be tolerated.

Nothing seems to deter gold believers. I expect my father in law will ride it all the way down. (Okay, I know what you’re thinking, gold has already put in a big correction, down from its high; it can’t go much lower is the complacent consensus complaint when we say that.) I am not talking about the corrective-move type of stuff; I’m talking about the type of hit gold takes when the US dollar enters a multi-year bull market.

Empirical evidence that every major bull market in the dollar has been met by a big sell off in gold, since currencies began floating back in 1971, won’t deter my father in law, and I know it won’t deter those who worship at the altar of GOLD. [There is an economic reason why this occurs; gold is priced in the world reserve currency—the US dollar. It must maintain global purchasing power when the world reserve currency falls in value relative to other currencies. Thus, the dollar gold price moves lower when the world reserve currency increases in value relative to other currencies. It is this way it is and has to be in a world still dominated by the dollar, with no alternative on the horizon.]

In the chart below, gold is represented by the red line and the US$ index the black line. This slide is a bit old…and was done just before gold broke out and surged to its new high on the back drop of plenty of liquidity flowing back into the market, pushing all other risky asset higher i.e. liquidity-driven risk asset classes—gold is now a risk appetite asset given the way it is acting. It is not acting as a safe haven.

….read page 3 HERE (start at the 38 year notated Chart)

Jack Crooks was a speaker at the World Outlook Financial Conference January 22,33

Register HERE for the FREE Daily Currency Currents Newsletter.As a subscriber to Currency Currents you stay tuned-in to our current global-macro view and our analysis of key investment themes driving currency prices. Nothing is off limits to us in this free-wheeling look at the markets. Some days you’ll receive ramblings on trading psychology, while other days we may take an academic approach in explaining esoteric economic issues. Ultimately we have one goal in mind: to help you get a handle on the key investment themes driving global capital flow. Because if you know where the money is going, it increases the probability that yourposition in the market will be a profitable one.

I wrote about Greece in last week’s letter. Then I ran across this column in the Financial Times by my friend Mohammed El-Erian, chief executive of Pimco, and someone who qualifies to be introduced as one of the smartest men on the planet. It is short and to the point.

Then, somehow my London partner, Niels Jensen of Absolute Return Partners found the time to write a letter while we were running around Europe. As we had a lot of conversations with some very key players, and a lot of debate, the letter reflects a lot of what we learned, as well as further documents the serious straits that European nations face in the coming years due to their debt and deficits. It is not just a US or Japanese problem. I have worked closely with Niels for years and have found him to be one of the more savvy observers of the markets I know. You can see more of his work at www.arpllp.com and contact them at info@arpllp.com.

And finally, many of you are probably familiar with TED Talks. If you are not, you should be. They basically get very smart, creative people to come in and do short talks Tiffani just sent me one of their latest videos. 13 minutes. It blew me away. The world of Minority Report is here, 40 years ahead of schedule. All I could do was just say “Wow!” Its young men like this that should make us all optimists that somehow we will figure out how to get through all this. http://www.ted.com/talks/view/id/685

John Mauldin, Editor

Outside the Box

Ed Note: Why Stocks Go Up (below) is connected with this piece below you may already have read:

Greece part of unfolding sovereign debt story

By Mohamed El-Erian

Global investors worldwide are starting to pay more attention to what is unfolding in Greece. Yet most still think of Greece as an isolated case, just as they did for Dubai a few months ago.

With time, they will see Greece as part of a much larger investment theme that is a direct outcome of the global financial crisis: the 2008-09 ballooning of sovereign balance sheets in advanced economies is consequential and is becoming an important influence on valuations in many markets around the world.

As realisation spreads of this key sovereign investment theme, it is important to be clear about what Greece is, and what it is not.

At the simplest level, think of Greece as Europe’s big game of chicken, with the operational question for markets being two-fold: who will blink first, the Greek authorities, donors or both; and will they blink in time to avoid truly disorderly debt and market dynamics that also entail significant contagion risk.

Let us start with Greece where, under any realistic scenario, a meaningful internal adjustment is needed.

There is no solution to the country’s debt issues without a deep and sustained policy effort. Yet, given the initial conditions (including the size and maturity profile of its debt) and the existing policy framework (anchored on adherence to a fixed exchange rate via the euro), such adjustment is difficult and not sufficient.

If unaccompanied by extraordinary external assistance, it would entail such contractionary fiscal measures as to raise legitimate socio-political problems.

External assistance is needed to support the meaningful implementation of internal policies. And it has to be consequential in scale and durability, as well as timely and well-targeted.

Understandably, such assistance faces headwinds on account of donors’ moral hazard concerns (vis-à-vis Greece and beyond); of donors’ understanding that a Greek bail-out would not be a one-shot deal; and of donors’ own domestic budgetary considerations.

Because of this, I suspect that at least three of the following four conditions are needed to force the hand of European donors, and that is assuming that Greece provides them at least with the fig leaf of commitment to meaningful internal policy actions.

- First, evidence that Greek markets are being severely impacted by funding concerns. With the recent surge in borrowing costs and the disruptions in the normal functioning of government and corporate markets, this condition is clearly already met.

- Second, evidence that other peripherals in Europe – such as Ireland, Italy, Portugal and Spain – are also being impacted. This is happening, as signalled by the gradual widening in market risk spreads.

- Third, evidence that other providers of capital are sharing the burden of financing Greece. Tuesday’s €8bn bond issuance to private creditors is consistent with this.

- Fourth, evidence that the Greek financial disruptions are starting to undermine core European countries. Evidence here is limited to the weakening of the euro, which, as yet, cannot be viewed as disruptive (indeed, some view it as helpful for Europe).

- Notwithstanding this last condition, we are much closer today to the point where donors’ hands will be forced. Yet investors should remain wary, as this would offer, at best, only a short-term tactical opportunity. Greater clarity as to what Greece can deliver in internal adjustment should remain the primary driver for long-term investment opportunities.

Investors should also remember that “market technicals” remain tricky and now constitute a meaningful marginal price setter. The shift in the investment characterisation of Greece, from being primarily an interest rate exposure to a credit exposure, has happened in such a way as to allow for little orderly repositioning. Many investors are trapped and the phenomenon has been accentuated by the recent evaporation of market liquidity.

Where does all this leave us?

Over the next few days, we are likely to get some combination of Greek and European donor announcements aimed at calming markets, reducing volatility, and reducing contagion risk. But the impact on markets is unlikely to be sustained as both sides face multi-round, protracted challenges which contain all the elements of complex game dynamics.

No matter how you view it, markets in Greece will remain volatile and more global investors will be paying attention. In the process, this will accelerate the more general recognition that sovereign balance sheets in many advanced economies are now in play when it comes to broad portfolio positioning considerations.

Ed Note: Excerpt from Niels Jensen’s piece. (you can red the whole article by registering with Outside the Box HERE

If PIIGS Could Fly

By Niels Jensen

The Absolute Return Letter – February 2010

“A democracy is always temporary in nature; it simply cannot exist as a permanent form of government. A democracy will continue to exist up until the time that voters discover that they can vote themselves generous gifts from the public treasury. From that moment on, the majority always votes for the candidates who promise the most benefits from the public treasury, with the result that every democracy will finally collapse due to loose fiscal policy…”

Alexander Fraser Tytler, Scottish lawyer and writer, 1770

Ed Note: Excerpt below. (you can red the whole article by registering with Outside the Box HERE)

Why stock markets go up

“Despite the grim outlook, the world’s stock markets have produced brilliant returns over the past nine months. This has provoked some of the best and brightest in our industry (most recently Mohamed El-Erian, CEO of Pimco[4]) to declare that there is a dis-connect between the economic reality and the picture painted by Wall Street.

I am not convinced. Firstly, global equities reached extremely depressed levels back in February 2009, and the recovery, however muted it may ultimately turn out to be, has stopped the bleeding in most large companies, giving investors an excuse to accumulate stocks again (smaller companies is a different story altogether, but that is a story for another day). What matters to the likes of Coca Cola, Rolls Royce and Volkswagen is not so much how the domestic economy performs, because the leading lights of industry today are becoming increasingly detached from the domestic economy. Ever more important to those companies is the global stage, and the global outlook is considerably more upbeat than, say, the US, UK or German growth prospects.

Secondly, equities usually do very well in the very late stages of recession and early stages of recovery. I refer to our July 2006 Absolute Return Letter for an in-depth analysis of this, which you can find HERE.

Thirdly, valuations are not prohibitively high. Many bears refer to the stock market (whether European or US) as being very expensive at current levels, but that is plainly untrue. Based on 2010 projected earnings, most OECD markets are either in line with or 10-20% below historical averages (see table 3). Only in emerging markets can you reasonably argue that current P/E levels are not cheap relative to the long term average.”

Ed Note: Larger Chart at Outside the box

In 2009 there have been massive flows of capital towards emerging markets – and towards Asia in particular – and valuations have been driven up as a result. It is hard to argue that those markets are yet in bubble territory, if one uses the valuations in table 3 as a benchmark; however, by pegging their currencies to the US dollar, Asian countries have effectively adopted a monetary policy which is entirely unsuitable for economies growing as fast as they do. That is how bubbles have been created in the past and why Asian equity markets should be monitored closely for signs of overheating in the months to come.

Conclusion

Summing it all up, the fate of global equity markets is very much in the hands of bond investors. Under normal circumstances, this is the best time to be in equities. But these times are not normal, so do not expect that the outstanding performance of 2009 will be repeated in 2010. If international bond markets calm down again – and that may happen, at least temporarily – equities can probably post further (but modest) gains in 2010; however, the end game is approaching. If bond investors do not revolt in 2010, they probably will in 2011, so playing the economic recovery through equities is a dangerous game.

As far as the bond market is concerned, as often pointed out by Martin Barnes at BCA Research, if you want to know where the next crisis will be, then look at where the leverage is being created today. And nowhere is there more leverage being created at the moment than on sovereign balance sheets. What is happening is an experiment never undertaken before. As John Mauldin puts it, we are operating on the patient without anaesthesia.

The big challenge will be to get the timing right. These situations can run for longer than most people imagine. Japan’s crisis has been widely predicted for almost a decade now, and the ship appears to be as steady as ever. As I suggested earlier, the key to predicting the timing of Japan’s demise – because there will be one – may very well be embedded in the savings rate, which could quite possibly turn negative in the next few years.

The Dubai crisis taught us that markets are in a forgiving mode at the moment and, before long, Greece could very well find some respite from its current problems. But then again, ultimately, governments will find – just like millions of households have found over the years – that you cannot spend more then you earn in perpetuity. The enormous debt levels being created at the moment will haunt us for many years to come and we may have to wait a long time to see the PIIGS fly again.

Excerpt from If PIIGS Could Fly by Niels Jensen – Absolute Return Partners LLP

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair