Daily Updates

In This Issue..

* Oil surges to a three month high…

* Bernanke is confident US consumers will spend again…

* RBA keeps rates on hold…

* Silver outshines Gold….

Good day… When you have been in this business as long as I have, certain patterns become apparent; and one of those patterns showed back up yesterday. In the 20+ years that I have been working with Chuck, it always seemed the currencies rally whenever Chuck spends a week or two away from the desk. We call it ‘Chuck’s vacation rally’. Yesterday we saw the dollar drop and the currencies bounce back up beginning what looks like another leg in the long term trend.

The biggest gainer in the currency market yesterday was the Norwegian krone, which shot up nearly 2% vs. the US$. The krone got help from oil prices which rose for a third day in a row and moved through $81 for the first time since May. Signs that the global economic recovery is progressing have increased demand expectations, while the upcoming hurricane season and increasing tensions with Iran have traders worried about supply. The Energy department will release their crude oil supply report later today; but a Bloomberg survey indicates that oil supplies fell by 1.5 million barrels last week.

Higher oil prices will benefit Norway’s economy, adding to their already strong economic fundamentals. The Norwegian krone continues to be one my favorite currencies, with very strong underlying fundamentals and increasing demand for their commodity exports.

Another country which benefits from higher oil prices is the UK; and the pound sterling increased 1.26% vs. the US$ over the past 24 hours. The increase put the pound at the highest level vs. the dollar in almost six months. A report showed UK manufacturing expanded in July a bit faster than most expected. Another factor which boosted the pound was the announcement that the govt. owned lender Northern Rock Asset Management Plc turned its first profit, boosting confidence in the UK recovery.

Technical analysts at Commerzbank predicted the pound could reach $1.597 if it breaches a key technical level. The strong move overnight saw the pound push above $1.59, and it certainly seems to be well on its way to test the $1.60 figure.

But long term I am still bearish on the Pound sterling. The reason is all of the quantitative easing which the UK has used, and the tremendous amount of liquidity this has unleashed into the markets. While inflation has remained in check for now, I just don’t believe the Bank of England will be able to successfully drain all of this liquidity from the markets when the time comes. I think we are in for a volatile time in the UK, and the US is probably right behind.

But a lot of very smart people are actually calling for additional QE programs here in the US. Our own St. Louis Fed President James Bullard was all over the news wires the last few days after suggesting the FOMC should be doing much more to stimulate the economy. Mr. Bullard had been considered a centrist, and was traditionally one who kept a keen eye on the inflationary threat. But his recent comments clearly put him over into the camp of San Francisco Fed President Janet Yellen who continues to call for additional QE spending. This makes the August FOMC meeting a bit more interesting, as there are real possibilities that the Fed will tilt their words toward the risk of deflation, and away from their more traditional tough talk on inflation.

Ben Bernanke was in the news again yesterday, after taking a back seat to his predecessor over the weekend. The current Fed Chairman sounded a bit more upbeat on the economic prospects than Big Al Greenspan. Bernanke is convinced rising wages will probably spur household spending in the next few quarters. I think Bernanke may be holding his employment graph upside down! From my view in the cheap seats, employment isn’t picking up here in the US, and looks to be a continued drag on the economy. With an expected period of high unemployment, I just don’t see where Bernanke is seeing the possibility of rising wages.

As I said earlier, there is obviously a split among members of the FOMC, with some suggesting the US economy is spiraling into a deflationary spiral while Bernanke is saying he expects rising wages and more consumer spending. The divide will most likely keep the FOMC from making any kind of move, and rates will stay where they are for an extended period; waiting for additional signs the US economy is moving one way or the other.

The RBA kept rates on hold for a third month after slower inflation and a recovery in Asia made it prudent to just keep rates where they are. The non-move was expected by all of the economists surveyed, so it really didn’t have much of an impact on the Aussie dollar. The RBA is still leaning toward higher rates, and we expect another couple of increases before year end, which should give the Aussie dollar another push up toward parity with the US$.

The NZD dollar or kiwi as it is know in the currency markets, has had a nice run up in the past month, as investors have moved back into the higher yielding currencies. The kiwi held steady above .73 yesterday and seems to be forming a nice base for another move higher. With the global recovery well established in Asia (the biggest export market for NZD) the kiwi is well positioned and could be an attractive alternative to the lower yields found in Europe.

And Gold held fairly stable yesterday, while Silver had a nice run higher. As usual, the press has been focused on Gold as the precious metal of choice, but Silver has been making a nice run higher recently. Silver has moved nearly 3 percent higher during the month of July, while gold has sold off by just over 2 percent. On a year to date basis, Silver is up over 9% while Gold is about 1% behind with an 8% appreciation. We always encourage investors to keep a well diversified portfolio, and that goes for your precious metals holdings as well as currencies. Many investors shy away from silver because of the costs involved in holding it, but our unallocated accounts are a perfect way for you to hold silver at minimal costs.

Another great alternative for those looking for good diversification in the metals is our current MarketSafe CD which is evenly distributed between Gold, Silver, and Platinum.

To recap: Oil surged to a 3 month high and pulled the NOK and GBP with it. Bernanke is confident in the ability of the US consumer to spend our way out of trouble. The RBA keeps rates unchanged, but leans toward further tightening, and Silver has outshone gold recently.

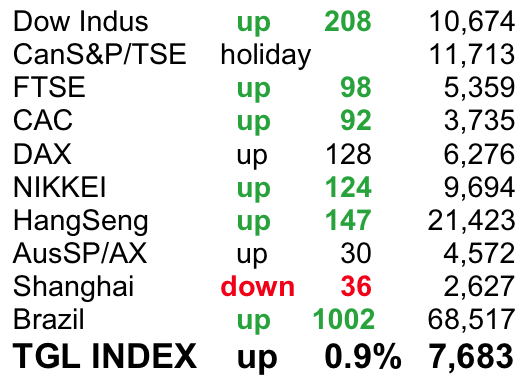

Currencies today 8/3/10: American Style: A$ .9123, kiwi .7338, C$ .9771, euro 1.3249, sterling 1.5957, Swiss .9654, … European Style: rand 7.2802, krone 5.952, SEK 7.0619, forint 212.69, zloty 3.0141, koruna 18.6356, RUB 29.73, yen 85.83, sing 1.3510, HKD 7.7623, INR 46.16, China 6.7734, pesos 12.587, BRL 1.752, dollar index 80.506, Oil $81.77, 10-year 2.91%, Silver $18.42, and Gold… $1,186.56

That’s it for today… It was a hectic day on the desk yesterday, as computer problems gave us a late start and Monday mornings are always one of our busiest times. But Jennifer pulled together the trading with help of Christine and Lori and the rest of the team handled all of the phone calls. I was in meetings most of the day, so I wasn’t able to be much help. I sure will be happy once we get this new computer system tested and installed, so I can get back out to the desk! Kristin brought in a surprise this morning, this Starbucks is just what I needed today! Hope everyone has a Terrific Tuesday!!

Chris Gaffney, CFA

Vice President

EverBank World Markets

1-800-926-4922

1-314-647-3837

08/02/10 Ouzilly, France – The stock market in the US was flat on Friday. Gold rose $13. China edged out Japan to become the world’s second largest economy. Bonds rose. And the dollar fell.

The Bloomberg report:

The Institute for Supply Management-Chicago Inc.’s business barometer rose to 62.3 this month, exceeding the median forecast of economists surveyed which anticipated the measure would drop to 56. The June reading was 59.1 and figures greater than 50 signal expansion.

The Thomson Reuters/University of Michigan final index of consumer sentiment declined to 67.8 this month from 76 in June. A preliminary measure issued earlier this month was 66.5.

The Standard & Poor’s 500 Index fell 0.1 percent to 1,100.07 at 12:12 p.m. in New York. The yield on the 2-year Treasury note drop to 0.55 percent from 0.58 late yesterday and touched a record-low 0.546 percent.

The worst US recession since the 1930s was even deeper than previously estimated, reflecting bigger slumps in consumer spending and housing, according to the Commerce Department’s annual revisions also issued today.

The world’s largest economy shrank 4.1 percent from the fourth quarter of 2007 to the second quarter of 2009, compared with the 3.7 percent drop previously on the books, the report showed. Household spending fell 1.2 percent in 2009, twice as much as previously projected and the biggest decline since 1942.

Consumer Slowdown

Consumer spending, which accounts for about 70 percent of the economy, rose at a 1.6 percent pace last quarter, compared with a 1.9 percent rate the previous three months that was smaller than previously estimated, today’s report showed. Job gains have been slow to take hold, curbing household purchases.

The economy lost 8.4 million jobs during the recession that began in December 2007, the biggest employment slump in the post-World War II era. So far this year, company payrolls grew by 593,000 workers, according to Labor Department figures earlier this month.

More than 7 out of 10 Americans say the economy is still mired in recession, and the country is conflicted over how to balance concerns over joblessness and the federal budget deficit, according to a Bloomberg National Poll.

Just like the experts, Americans are torn about whether the federal government should focus on curbing spending or creating jobs, the poll conducted July 9-12 shows. Seven of 10 Americans say reducing unemployment is the priority. At the same time, the public is skeptical of the President Barack Obama’s stimulus program and wary of more spending, with more than half saying the deficit is “dangerously out of control.”

At this stage in the typical post-war recovery, the economy should be steaming along with GDP growth of about 6%. The latest reading, alas, came in at only 2.4% for the second quarter. Growth has been cut in half from the end of last year. The recovery – if there ever was one – is now faltering.

Of course, you, Dear Reader, know that there never was anything resembling a real recovery. You can recover from a fall. You can recover from a broken heart. You can recover from a head cold. You cannot recover from death. You can only become a zombie. The US economy merely became more zombified, after the crisis of ’07-’09.

Houses are underwater. People are living on food stamps and unemployment compensation. The feds control major industries. Banks are kept alive with tax money. And GDP ‘growth’ was pushed up by boondoggles, bamboozles and bailouts.

But now, even the zombies are beginning to shuffle. They need more flesh…more blood…

In this regard, Federal Reserve Governor Bullard has let the cat out of the bag. He says the best remedy at this stage would be further doses of quantitative easing. He’s right – at least within the strange context of central banker thinking. If your goal is to get the zombies moving…you need to give them some juice. And when you’ve already cut your rates to zero (the current rate is actually 0.25%), and you’ve run a deficit of $1.5 trillion, what else can you do? You’ve got to print money, right?

There are some very smart people who believe inflation rates are going up – soon. They’re urging investors to dump the dollar and US bonds. Their logic is very clean and very solid:

The US government owes more than it can pay. When a debt cannot be paid by the borrower, someone else must pay. Typically, it’s the lender who pays when the borrower defaults. But the US government doesn’t have to default. It has another alternative, the aforementioned quantitative easing – monetary inflation, in other words. Instead of defaulting on its debts directly, the federal government can inflate them away.

We have no real argument with this line of thinking. We have a hunch, however, that it won’t work out that way. It’s too obvious. Instead, we see the zombies staggering on for years…

Bill Bonner

for The Daily Reckoning

It’s hard to believe that more than ten years have gone by since we began writing The Daily Reckoning out of a Paris office back in July of 1999…

Since then, a lot has changed. We have seen the dot com boom and bust…a massive expansion of credit…real estate mania and meltdown…and epic highs and lows in the markets.

Nothing about the past ten years has been boring. And we have been there throughout, trying to help readers make some sense out of our global economy. And hopefully providing a few laughs along the way.

In short, we pen The Daily Reckoning each day – for free — to show you how to live well in uncertain times. We aim to make each article the most entertaining 15-minute read of your day.

If you haven’t signed up yet, I urge you to do so right here. And don’t worry. It’s 100% free – no credit card is required.

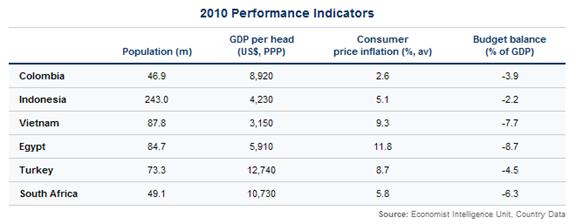

When countries get grouped together for economic or political purposes, an acronym or other shorthand device is soon to follow. OPEC, EU and G7 are a few of the old standards, while G20, PIIGS (European nations with dangerously large sovereign debt burdens), and of course BRICs are newer examples.

Now The Economist is getting into the game with “CIVETS”: Colombia, Indonesia, Vietnam, Egypt, Turkey and South Africa – six countries that could be the next wave of emerging markets stardom.

The Economist’s basic case: these six have large and young populations, diversified economies, relative political stability and decent financial systems. In addition, they are for the most part unhampered by high inflation, trade imbalances or sovereign debt bombs.

We didn’t think up the acronym, but we have liked the long-term prospects for most of these countries for quite a while. Here are some of our thoughts and observations.

Start with Colombia, which has had a hard time getting people to forget about its narcoterrorism past and look at its promising pro-business government policies.

I met with former President Alvaro Uribe and it was fascinating to observe his policies for social stability and job creation. Five years ago, he changed the rules and began to encourage companies to come in and help develop their oil resources. He has taken those petrodollars created and reinvested them back in the country’s infrastructure and created jobs.

That is in complete contrast to what Hugo Chavez is doing in Venezuela, or even Mexico and its energy policy. Both of those countries are watching their reserves deplete, but there’s no policy to bring in intellectual capital like you’re seeing in Colombia.

Turkey’s economy is dynamic and currently supported by strong underlying trends that point to long-term growth ahead. Its economy is the sixth largest in Europe and in the top 20 worldwide with a 2009 GDP of $615 billion. Turkey’s per capita GDP of just over $8,700 is greater than any of the BRICs. Industrial output leaped by 21 percent in the 12 months ending March 2010, inflation fell to 6.1 percent last year from double-digit levels a year before, and public debt is less than 40 percent of GDP.

And while Europe still makes up more than half of Turkey’s exports, the current government has taken steps to increase exports to Middle East trading partners – Saudi Arabia, Iraq and Egypt – as a hedge against economic volatility in Europe.

Indonesia’s demographics, natural resources and relatively stable politics have set up the country for what could be a very strong decade of growth. Its economy doubled in the past five years and in greater Jakarta – the world’s second-largest urban area with roughly 23 million people – per-capita GDP grew by 11 percent each year from 2006 through 2009.

More importantly, this growth was driven by the private sector, not by government spending – the private sector accounts for roughly 90 percent of the country’s GDP. Over the past five years, the average income has doubled to $2,350 a year and Deutsche Bank thinks that figure can rise another 50 percent by the end of next year.

Despite this income growth, Indonesia still has the lowest unit labor costs in the Asia-Pacific region, according to JP Morgan. This has attracted manufacturing activities from China. Employment growth is key because half of Indonesia’s population is 25 years old or younger, so the workforce as a portion of total population will rise over the next 20 years. This should increase the country’s consumption levels and fuel further economic growth.

Vietnam has seen rapid economic growth in recent years. It too has picked up some manufacturing base that was formerly in China. The country’s per-capita income of $1,050 last year was nearly fivefold higher than it was in the mid 1990s, and in Hanoi, the income level is closing in on $2,000 per person, according to government figures.

That new wealth is showing up in gold purchases. Net retail gold investment in Vietnam exceeded 500,000 ounces during the first quarter of 2010, up 36 percent year-over-year, the World Gold Council says. Add to that a 20 percent increase in gold jewelry demand.

Beyond the CIVETS, we see some potential in other places. Malaysia’s economy, for instance, grew more than 10 percent in the first quarter of 2010, and the country has plans to slash its budget deficit and at the same time invest more heavily in infrastructure. And in Chile, despite February’s earthquake, public debt is just 7 percent of GDP and the economy is expected to see 5.5 percent growth this year and 6.5 percent in 2011 as resource exports to emerging markets in Asia accelerate.

We see the global growth story – led by key emerging market countries like the BRICs, the CIVETS and others – as the most powerful long-term investment opportunity.

For more on this theme, I invite you to visit our website to read through the Emerging Markets archives on the “Frank Talk” blog and to look at our interactive “What’s Driving Emerging Markets” presentation.

Advanced G-20 economies references members of the G-20 whose economies are considered by the IMF to be developed. This includes Canada, United States, Austria, Belgium, France, Greece, Ireland, Italy, Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, United Kingdom, Australia, Japan and Korea. Emerging G-20 economies references members of the G-20 whose economies are considered by the IMF to be emerging. This includes Brazil, India, Indonesia, Hungary, Russia and Saudi Arabia. BRIC refers to the emerging market countries Brazil, Russia, India and China.

Please consider carefully the fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Gold funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The price of gold is subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in gold or gold stocks.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The index benchmark value was 500.0 at the close of trading on December 20, 2002. The NYSE Arca Gold Bugs Index (HUI) is a modified equal-dollar weighted index of companies involved in major gold mining. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index (DXY) provides a general indication of the international value of the U.S. dollar.

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail: dennis@thegartmanletter.com For a Trial Subscription go to The Gartman Letter)

STOCK PRICES ARE QUITE STRONG, and we are quite bullish, but today is “Turnaround Tuesday” and with the late collapse in Chinese shares earlier today we can expect to see a good deal of yesterday’s strength corrected. A correction following the recent strength is reasonable and rational and perhaps even overdue. Tuesday’s have tended to be corrective days, and we look for today to be precisely that. Those who have not yet gotten long of equities…and especially of those equities that produce or move the “things that if dropped on your foot shall hurt” should use today’s weakness… or more properly today’s close… to become long of equities. Otherwise, we intend to sit tight with our positions as we have them presently:

For a Trial Subscription go to The Gartman Letter)

“My guess is that gold has bottomed. Too many investors and too many cental banks are potential buyers of gold. And they are ‘bottom-fishing.” – Richard Russell July30th/2010 Dow Theory Letters –

What’s unravelling is gold price suppression

“So investors have bought a record amount of “physical gold,” which is actually paper gold that they have never seen, and only about 2.3 percent of what has been sold actually exists. The bullion banks are “awash” with liabilities for the record amount of gold they are supposed to be holding. Investors are now distrusting the bullion banks and are asking for delivery…” – Adrian Douglas August 1st/2010

“When 45 ounces of gold are sold but only 1 ounce is sourced, the result is a massive suppression of the gold price. But the converse is also true: When 45 ounces of gold are demanded for every 1 ounce that is in the vault, the price explosion is beyond imagination.” Adrian Douglas

….read the whole article HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair