Uncategorized

In its most recent annual ranking of “business friendly” states, Forbes magazine had some blunt advice for investors. “Forget about California.”. Whereas Utah and Colorado have maintained strong business climates.

Californians like to dismiss such assessments of the Golden State and instead point to its natural beauty and quality of life. They tend not to worry what people in other states think. But they should. California is no longer the economic miracle it once was. Silicon Valley no longer has a monopoly on high-tech talent and innovation. Hollywood has to compete for movie locations with Utah and Morocco. Real estate investors see better development prospects in states with fewer foreclosed and abandoned homes. And SoCal porn producers know they don’t need huge wardrobe containers to move to Nevada.

Californians tend to be complacent about these competitive risks. On the surface, things don’t look too bad. Sure, the state’s finances are in shambles and the Legislature in disarray. But median personal income ($42,578) is well above the national average ($39,945).

These things can’t compensate for some disturbing recent trends. The growth of the state’s $2-trillion economy has slowed dramatically. Since 2000, the state’s economy has grown significantly more slowly than the rest of the nation. Last year, California ranked 34th in real GDP growth. That sluggish growth has burdened it with among the highest unemployment rates (10.9%) in the nation. If businesses heed Forbes’ advice to avoid the state, the situation will only worsen.

So what is it that makes California unfriendly to business? For starters, it’s very expensive to do business in the state. Corporate taxes are high, as are energy and labor costs, according toMoody’sAnalytics and the Tax Foundation. In the Forbes rankings, the state also comes in at No. 40 in the category of regulatory environment. To compute the state’s regulatory score, Forbes looks at the Pollina Corporate Real Estate Index, Pacific Research Foundation’s Tort Liability Index, PRI’s Economic Freedom Index,Moody’sbond ratings, transportation infrastructure and right-to-work laws. Thank goodness it didn’t also look at the Los Angeles City Council’s proposed new regulation of the porn industry’s safe-sex practices — a proposal that increases both regulation and costs in an economically important industry in the state. California also ranks a disappointing No. 32 in the “labor supply” category, based largely on its low high school and college graduation rates. This ranking represents a precipitous decline from the days when California’s colleges were ranked among the best in the world.

Forbes is not the only naysayer about California’s business climate. The Canadian-based Fraser Institute compiles a similar ranking for the 50 states and the 10 Canadian provinces. Fraser’s ranking is based on 10 statistical indicators that more narrowly focus on business concerns (tax rates, minimum-wage levels, unionization rates, public-sector employment and the like). The Fraser rankings came out in January. In that ranking, California scores even worse — a dismal No. 44 among the 50 U.S. states. South Dakota, Delaware and Texas top the Fraser list, while Vermont, New York and Alaska reside at the bottom.

California’s dismal showing in the Fraser rankings of business climate stem primarily from the state’s relatively high income tax rates, high minimum-wage thresholds at both the state and local levels, and a high rate of unionization among public-sector employees. The state also scores poorly on its high ratios of public-sector spending and income transfers because of such things as its workers’ compensation system, unemployment insurance costs and fat public pensions.

Although many Californians take pride in some of these wage and spending policies, Fraser emphasizes the effect they have on business decisions — especially decisions about locating new businesses in the state or expanding existing enterprises. According to Fraser, these rankings are crucial to economic growth. States that have improved their rankings have grown per capita incomes faster than other states. States whose rankings have declined have experienced more sluggish growth. The Fraser survey found government growth, higher taxes, minimum-wage hikes and increased unionization to be significant impediments to economic growth.

By those measures, it’s no wonder California is declining. L.A.’s intrusions into the porn industry, San Francisco’s new highest-in-the-nation minimum wage ($10.24 an hour) and Gov. Jerry Brown’s relentless push for higher taxes, more regulation, increased public spending and a $100-billion railroad augur poorly for future rankings.

It’s tempting to dismiss these rankings as biased or inconsequential. But that would be a mistake. If California is to prosper again, it’s got to attract new business. And having a business-unfriendly reputation works against its ability to do that.

Bradley R. Schiller is a native Californian who now teaches economics at the University of Nevada, Reno. He is the author of “The Economy Today.”

You need ID to rent a hotel room, drink in a bar (if you look young), get married but not to vote for the President of the United States. Project Veritas launched its investigation into Voter Fraud in America. By March 7th, as a direct result of Project Veritas’ work, the New Hampshire State Senate voted and passed a new Voter ID bill.

{youtube}PLSjL–qvsw{/youtube}

The Property Time Machine

“I wish I had a time machine”. Those were almost the first words out of Mary’s mouth when I met her. Her husband nodded in agreement. I did too. Who wouldn’t want a time machine?

I could picture myself going back in time and snapping up Microsoft shares before they became a household name…or priceless Van Goghs, back when the painter, himself, couldn’t even sell one of them…or choice properties in prime locations before they boomed.

And Mary’s mind was on property too. She wanted to buy a beach house where she could retire. She considered Panama and Costa Rica 10 years ago, checking out listings and even traveling through both countries to get a feel for them.

But she decided that her retirement was too far in the future. She left her savings in the bank. Ten years back, her savings would have bought her a beach house in Panama or Costa Rica. But her savings haven’t grown very much, while the cost of beach property in Costa Rica and Panama had soared. Today, she’s priced out of both markets.

But she hasn’t given up her dream of a beach home. She doesn’t want to compromise by buying a home a short drive from the beach. She doesn’t want a tiny studio. She wants a spacious house with ocean views in a beachfront community. She’s worried that she won’t find it anywhere on her current budget.

But she can — and she won’t need a time machine. She simply needs to look to Ecuador…

You see, while coastal property prices in both Costa Rica and Panama rose sharply in the last ten years, Ecuador’s coast was a sleeping giant.

A surge of foreign investors triggered the real estate booms in Costa Rica and Panama. Those foreign investors didn’t make it to Ecuador. So property prices on Ecuador’s coast are pegged to the price that local buyers can afford to pay for a home.

So what we’ve seen on Ecuador’s coast is a slow but steady appreciation in prices rather than a rapid spike upwards. Most local buyers pay cash for a second home, too, so the market isn’t frothy and filled with speculators. Ecuadoreans buy beach homes for personal use. Most don’t buy property to flip or as a buy-to-let investment.

And that means you can still buy a home on Ecuador’s coast for less than half of what you’d pay for a similar property in Costa Rica or Panama. And one location offers the most bang for your buck — in terms of value and appreciation potential.

Ecuador boasts hundreds of miles of Pacific coastline. But we’ve found the sweet spot…a section of coast that we think holds the most promise.

I first scouted Ecuador’s coast back in 2008. And when I say scouted…I spent a month on the ground. I explored in off-road vehicles and tiny fishing boats. I burned up boot leather to get the real skinny on off-the-beaten-track locations. I spent time in towns where a foreigner was a novelty. I ate in roadside stops filled with local truckers. I poked around every beach, cove and bay I came across.

And at the end of that month I knew I’d found the sweet spot. (You can see it on this map here; it’s between Canoa and Pedernales.) The problem was; it was really tough to get to.

Since that first trip, I’ve lost track of the number of scouting trips I’ve done on Ecuador’s coast. And each time I’ve gone back, it’s been easier to get to the sweet spot.

Finally, in 2011, this piece of coast opened up. It hit a milestone. And it’s now poised for major growth. Already, we’re seeing more local tourists and buyers, mainly from Quito…and growing interest from foreign buyers looking for a second or retirement home.

In January 2011, a new coastal highway opened. It winds its way from Quito, Ecuador’s capital city, through the mighty Andes Mountains. Driving this route, you can’t help but appreciate the mammoth engineering task involved in carving this road through the mountains.

The new road is smooth and easy to drive. It’s much quicker too, cutting the journey time in half. It now takes 3.5 hours to drive from Quito to this section of coast. That makes this piece of coast the closest beach area to Quito.

That’s an important point. Previously, the closest beach area was a town called Atacames. But Atacames is a 6-7 hour drive from Quito…compared to 3.5 hours to get to Pedernales.

I love this piece of coast. It’s got so much to offer. Travel further south on Ecuador’s coast, and the climate gets very dry, with scrubby vegetation. Travel further north, and it becomes sticky and humid. This place is somewhere in between. It’s not bone-dry or shirt-soaking damp. There’s enough rain to keep the hills and forests green and fresh for most of the year.

It’s unspoiled here too: No high rises, no mega-malls, no sprawl of subdivisions. Lack of access has preserved the natural beauty of this coast. Empty beaches run for miles. Howler monkeys call to each other in the forests covering the hills behind the coast. In the bright blue Pacific, giant whales breed and play with their young. Bright butterflies dance in the ocean breeze. Fishermen land their day’s catch and sell it fresh from the boat for $1 a pound.

This coast has everything that Mary wants. She wants natural beaches, forests and lots of wildlife. She wants year-round warm weather. She’d like a low cost of living and lots of locally-grown produce and fresh seafood. She’s not looking for brand-name coffee houses, fast food chains, or fashion malls. You won’t find any of those on this coast. What you will find are raw beauty and low property prices.

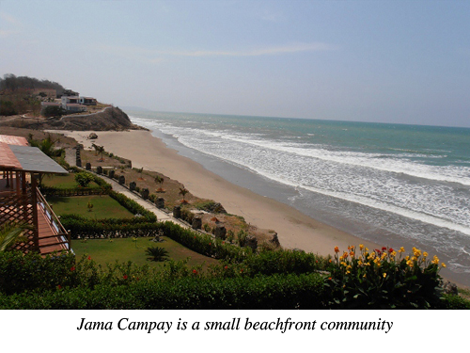

One of the nicest residential communities on this section of coast is Jama Campay.

Jama Campay is a small beachfront community of lots, houses and condos. The development sits on low cliffs overlooking the ocean, with forest-covered hills providing a lush backdrop.

A 20-minute ride from Jama Campay takes you to a town where you can buy groceries and gas, go to the bank, or dine in one of the local restaurants. The restaurants aren’t fancy, but neither are their prices. You can get lunch for as little as $2.

Just south of Jama Campay, there’s a fun town called Canoa. It’s a little Margaritaville with lots of rustic bars, cafes, restaurants and clubs. Its wide beach and good waves attract a young international set of surfers and backpackers.

But Jama Campay contrasts with the party atmosphere in Canoa. It’s tranquil. Most of the buyers are well-heeled locals from Quito. They come here to relax with family and friends. Few rent their homes when they’re not here. They prefer to keep their homes for private use. One owner who is renting is earning $250-$300 a night for their house. There’s a shortage of accommodation on this coast, and that shortage is growing as more tourists visit.

The homes in Jama Campay tick all the right boxes for Mary. They’re a spacious 1800 square feet with an open-plan layout…they offer wide ocean views…and they’re priced at $134,600. You’ll enjoy the wide outside terraces, where you can dine to the sound of the waves…

And (to tick another box on Mary’s wish list) it’s only a few minutes’ walk from your home to the beach…

I’m going to tell you what I told Mary. Go and take a look at this coast. Sometimes a place will tick all the right boxes on paper. It has everything you want. But then when you go there, it doesn’t feel right for you.

The developer of Jama Campay, Francisco del Castillo, knows this. That’s why he runs chill weekends…mini breaks on this coast that let you check it out first-hand and see if it fits.

Francisco’s team will plan a custom chill weekend for you. They’ll meet you at the airport and drive you down to Jama Campay where you’ll spend a few nights. You’ll see the new road up close…stop for breakfast in a cloud forest town that’s famous for bird watching…and reach Jama Campay in time for an afternoon dip…

Francisco’s team will show you Jama Campay, discuss the different types of property available in the community and help you decide if it’s right for you.

Don’t worry, you’ll get plenty of time to relax and soak up the atmosphere…and before you head back to Quito, you’ll enjoy dinner in Canoa, the fun beach town.

Regards,

Margaret Summerfield,

for The Daily Reckoning

Abound Solar, the lucky winner of a $400 million tax dollars is going broke. Abound just announced layoffs of nearly 300 employees (70 percent of its work force, article HERE)

Not to different from Solyndra which got $535 million of taxypayer dollars in 2009 only to file for bankruptcy in Sept. 2011.

Doesn’t seem that Government should be trying to pick winners does it? It gets even stranger with Wind Power.

“Over the past two decades, the US federal government has prosecuted hundreds of cases against oil and gas producers and electricity producers for violating some of America’s oldest wildlife-protection laws: the Migratory Bird Treaty Act and Eagle Protection Act. Despite laws that can result in a fine of up to $250,000 and imprisonment for two years, the Wind Industry has never been prosectued despite graphic examples of vastly more rare birds being killed by windmill projects. For example, last June, the Los Angeles Times reported that about 70 golden eagles are being killed per year by the wind turbines at Altamont Pass, about 20 miles east of Oakland, Calif. A 2008 study funded by the Alameda County Community Development Agency estimated that about 2,400 raptors, including burrowing owls, American kestrels, and red-tailed hawks—as well as about 7,500 other birds, nearly all of which are protected under the Migratory Bird Treaty Act—are being killed every year by the turbines at Altamont.”

Good heavens, seems there’s a double standard in effect for Wind Projects (odd enviromenalists would overlook this) and a giant sinkhole for tax dollars in Solar Panel Manufacturers.

Pictures of GOLDEN EAGLES THAT FACE EXTINCTION IN U.S. AS NUMBERS PLUMMET killed by windmills

At a time when the US has a $1.5 TRILLION deficit, why are they spending $770 million program to fix up mosques in Egypt? Can you imagine a $770 million program to fix up Christian churches (or even a $7.70 program)? Why are we spending $770 million in money we don’t have to fix up mosques in other countries around the world?

{youtube}tlI_A64sEF4{/youtube}

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair