Uncategorized

When will they ever learn?

Great Britain has instituted tax on incomes and it failed to generate the expected revenue.

So it only missed its target by 50%. Not bad for government work.

The same thing happened in Illinois and New York when they raised taxes on the supposed rich. The result was less revenue than they expected. And in the case of New York, the flight of thousands of millionaires to friendlier climes.

….read more HERE

As the global economy plunges and retirement portfolio shrinks, many Canadians are worried more than ever for their financial well being after retirement. Some retirees will be able to maintain their expected living standard regardless of how the economy does. However, this may not be the case for everyone. If you need to work or are thinking of working after retirement, here are some tips to help you with your decision.

1. Some of the government programs for retirees such as Old Age Security (OAS)credit, the government pension plan (CPP), and so on may be affected if you work full- or part-time after retirement.

2. The best way to handle your clawbacks or drawbacks to government benefit programs is to consult a financial planner or tax specialist. They have tools andcalculators to show you exactly what your own numbers will look like based on your unique situation (as everyone’s scenarios are different)

3. There are free online tools and calculators available as well to help you with your retirement planning. Such online tools and calculators are available here: Retirement Tools and Calculators

4. Service Canada offers Canadian Retirement Income Calculator to generate retirement income information and post retirement benefit information, including CPP benefits and OAS.

5. Regardless of how much research you do on your own, my suggestion would be to still sit with a retirement professional and discuss your situations. Due to the complex nature of retirement benefits and clawbacks, it is worth paying for advice and take action based on accurate and updated information.

More A Dawn Articles:

Why Multitasking Does Not Work

5 Best Android Free Live Wallpapers

How to Read free eBooks on Amazon Kindle

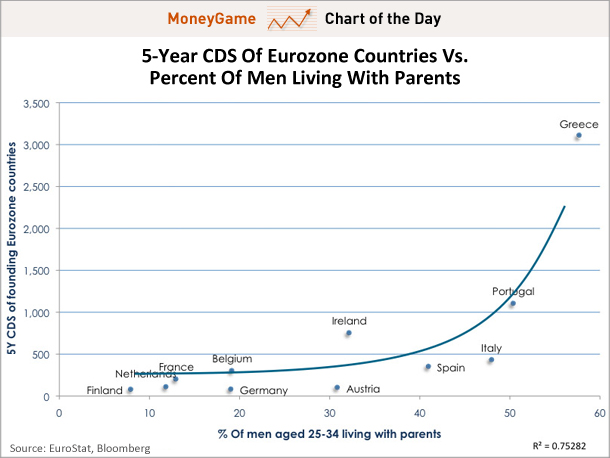

The chart below depicts the correlation between 5-year CDS (a form of insurance to protect against a credit event) of eurozone countries and the percentage of men ages of 25 to 34 still living at home with their mom and dad.

It’s pretty obvious what the pattern is…

Turkey and cheese sandwich, banana, potato chips, and apple juice not good enough. State Agent inspects sack lunches, forces pre-schooler to purchase fried chicken nuggets, sends parents the bill.

A preschooler at West Hoke Elementary School ate three chicken nuggets for lunch Jan. 30 because the school told her the lunch her mother packed was not nutritious.

The girl’s turkey and cheese sandwich, banana, potato chips, and apple juice did not meet U.S. Department of Agriculture guidelines, according to the interpretation of the person who was inspecting all lunch boxes in the More at Four classroom that day.

The Division of Child Development and Early Education at the Department of Health and Human Services requires all lunches served in pre-kindergarten programs – including in-home day care centers – to meet USDA guidelines. That means lunches must consist of one serving of meat, one serving of milk, one serving of grain, and two servings of fruit or vegetables, even if the lunches are brought from home.

When home-packed lunches do not include all of the required items, child care providers must supplement them with the missing ones.

Mark Steyn: The home-made lunch having been ruled illegal by officials*, the preschooler was given a federally-approved lunch, for which her mother has been sent a bill. The girl didn’t care for the substitute lunch, ate only the three chicken nuggets, and left everything else on her tray untouched. It may not have worked out all that nutritious for her, but at least it’s compliant with DCDEE/DHHS/USDA paperwork, and that’s what matters.

….read the whole horror story HERE

Political rather than economic Republicans want to pay Unemployed Americans income they need to maintain their current economic status.

Congress Rushes to Help?

Until very recently, many members of Congress were anxious to marry any increase in federal expenditures with budget cuts to offset them. That changed suddenly as leaders in the House and Senate agreed to arrangements that would extend unemployment benefits and payroll tax cuts, as well as drop provisions to pay doctors less for services they provide under Medicare. Republicans apparently got a minor concession for agreeing to the large compromise. There will be modest changes to federal pension payments. Overall, the deal is a signal that perhaps Congress realizes austerity alone will not solve either the deficit problems or the trouble with restarting the economy.

One theory shared by many economists is that an increase in payroll taxes will remove money from consumer accounts and put it into the Treasury. In the process, these experts say, the consumer will have less to spend and that will hurt GDP improvement. Whether most members of the House and Senate agree with that exactly is not as important as the fact that the consumer portion of the economy will have a chance to expand because of their votes.

The theory about unemployment benefits has similarities to one about personal income taxes, in that people who lose benefits completely can no longer be consumers. The federal government may save money at first, but the economy overall will pay a price. The more people who cannot consume, the worse off many American businesses will be. Those businesses pay taxes, but they will pay fewer if their profits fall.

The reasons for Congress’s decision may be almost entirely political rather than economic. Republicans may want to avoid a public fight over whether they have robbed Americans of income these people need to maintain their current economic status, which has been eroded already by a lack of pay increases going back several years. Democrats could have claimed they wanted to help financially struggling citizens while Republicans did not.

In the end, the reasons for the compromise are not as important as the fact that they add stimulus to the U.S. economy at a time when a recovery has begun but is still tentative.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair