On the heels of Washington desperately moving to buy more time to deal with its financial crisis, today Canadian legend John Ing warned King World News that China is preparing to unleash the “worst nightmare” for the United States. Ing, who has been in the business for 43 years, also stated that the Chinese are about to make a “major move” which will enable the timetable for this “nightmare” to be greatly accelerated.

On the heels of Washington desperately moving to buy more time to deal with its financial crisis, today Canadian legend John Ing warned King World News that China is preparing to unleash the “worst nightmare” for the United States. Ing, who has been in the business for 43 years, also stated that the Chinese are about to make a “major move” which will enable the timetable for this “nightmare” to be greatly accelerated.

Timing & trends

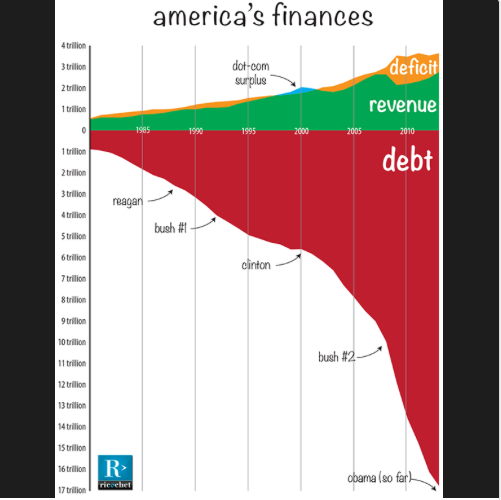

The D.C. press corps was giddy last night, declaring that the fiscal crisis had ended. Senators praised “honorable friends” from “great states,” congressmembers gave standing O’s to their stalwart leaders, and the president saluted bipartisanship while ridiculing Republicans, bloggers, activists and pretty much anyone else who dared oppose him.

If the whole thing seemed a bit surreal, it’s because the whole thing was a bit surreal. America’s fiscal crisis is not that our debt ceiling isn’t quite high enough — it’s that we have too much debt.

With the fiscal negotiations kicked down the road for a couple of months and the idea of tapering pushed further out as well the S&P Futures made new all time highs!

The S&P is going into the close on its highs at 1728.50, rising an impressive 88.5pts since the recent low on October 9th.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

Ing: “Washington kicking the can down the road doesn’t solve the debt problem. Apparently this process has been so fun they are going to do it all over again, and the markets are getting pretty jaundiced about it. But standing back, the fact is that the US debt is still escalating….

Continue reading the John Ing interview HERE

During the early morning of Oct. 16, 2013, Chairman of Berkshire Hathaway, Warren Buffett appeared on CNBC for a few hours with Becky Quick. There are a series of video clips posted below as well as a full transcript HERE

During the early morning of Oct. 16, 2013, Chairman of Berkshire Hathaway, Warren Buffett appeared on CNBC for a few hours with Becky Quick. There are a series of video clips posted below as well as a full transcript HERE

Buffett sounded fairly optimistic on CNBC noting he had made a billion-dollar acquisition this morning in the UK and also noting that it is not a mistake to buy stocks now, reaffirming stocks are not selling at “bubble” valuations. Buffett also weighed in on Carl Icahn’s proposed Apple (AAPL) buyback as well as FED policy, the debt ceiling, the future of J.C. Penney (JCP) and a few other things of interest.

It’s a perfectly okay debt to buy securities. We bought a $1 billion business about five hours ago. i think over at the uk. and we did not buy it with a condition in it that we could call off the deal if there was a no vote on the deficit change. limit change. so if you can own a good business, a good farm, a good apartment house, you know the united states is going to be around five or ten years from now and you know it will be more prosperous. it’s not necessarily a mistake to buy stocks because you don’t know the outcome of something that’s happening in congress. that’s a great long-term view. and your view has always been no matter what happens, we will get through it. we got through the great depression. we got through world war ii. but what about the immediate? people are really concerned about what’s happening in washington right now. it’s a mess. and if you think about it, i used to tell my children when they were young, it takes 20 years to build a reputation and 20 minutes to ruin it. we’ve been building a reputation for 237 years. the united states has become the reserve currency in the world in the process and people all over the world hold our paper. so to do anything to damage the 237 years of good behavior is idiotsy. i don’t think it will happen. but if it does happen, it’s a pure act of idiotsy.

i am fought worried in the sense of those treasury bills being paid. i’m worried about damage to an asset that we carefully cultivated for years. those short-term treasury bills, though, the rates have spiked on them, especially in the last couple of days. bill gross said he’s a buyer over at pimco. are you? they’ve spiked, but you’re talking about going from zero yield to 35 basis points. but 35 basis points for three or four days does not amount to a bunch of — in other words, you’re not scraping for cash? i’ve got better things to have had although that date looked pretty good. have you changed anything you’ve done at berkshire as a result of what’s been happening in washington? no. we have been at a derth when it comes to getting any signs of the economy, any reading on what is happening because you don’t have any economic numbers coming out. you have a lot of numbers coming out every day. in your opinion, has the u.s. economy been hurt by what’s been happening in washington and does it show up in your receipts? it has not shown up. but what will show up is in the world, united states citizens lose some faith in the full faith and credit promise of the united states. that would be a momentous event. even if we said, well, we’re slowing it for a week or we’re putting out script or whatever, that would be huge. we have been spent 237 years building up our reputation for billing our bills on time.

But a 1% real gdp growth per capita over a long period of time, one does wonder. are you telling us that we need to get used to this or is this a temporary rare thing and we’re going to get back to what we used to expect? i don’t know. i think it’s very possible we get back to higher rates of growth, but i will tell you that this is not a disaster. i mean, if you — just think about each generation living 20% better than the generation before them. that is not terrible. it’s not terrible and it’s not a disaster. but if you’re looking for 3% versus 3.5% growth versus what whooefb getting, you’re fought going to have the problems we’ve been dealing with today in washington. that takes care of itself. it takes care of itself unless we start making new promises. we tend to make big promises. we’re like a very, very, very rich family and then we don’t stop getting rich at quite the same rate. but our promises, we just went

The country should have a “sustainable path,” says Warren Buffett, Berkshire Hathaway chairman & CEO, but Congress should “fight it out” without putting the nation’s credit at risk.

Issues. what’s going on at benjamin moore now? we heard an employee was you fired. benjamin moore has been around over a hundred years. i made a promise to the dealers that we were going to stick with that and would not go with the big boxes. meaning the home depots and so on. that was enormously important. i did a video so there wouldn’t be any question. i found we were about to sign with one of the big boxes. i had to make a change. we have a commitment toll to the dealers. we take care of them; they take care of us. i encouraged who was put in. recently we had to make a change for a reason i can’t get into.

Basically i’m buying businesses and bank stocks for that matter in terms of what’s going to happen in the future not for what’s happened in the past. i can go back with bank of america. i read a book 55 years ago. i can go back to the san francisco earthquake. they thought it was a down day and turned out to be a good day for bank of america. what really counts is the future. in the future, banks will have to carry, particularly larger banks are heavier capital. banks are in the best shape i can remember. they’ve built up capital enormously. portfolios are in good shape. big problem they have now is getting out more money. they have more money around than they would like. they are not reluctant to loan.

Speaking of investors, let’s see a what carl has been saying to apple. what do you think about his requests or demands to buy back the incredibly large church of stock? the apple management did a nice job running the company. i wish i bought the stock years ago. i did advise the stock years ago. they’ve got a lot of money that’s not trapped over seas. they’d have to pay a big tax to bring it back. they hope for free trade at some point so they won’t have to pay the tax. carl is suggesting they borrow money to buy back the big chunk of stocks. companies have done that including coca-cola. they’re buying in stock. i’ve got — i think the apple management and directors have done a good job running the company. i vote with them. versus what carl is saying? i do not think that companies should be run primarily to please wall street and largely shareholders going to sale. i prefer shareholders going to

Do you agree with that opinion. i have no idea. the economy has been getting better. how they make a decision on whether to pull back — it doesn’t enter into my thinking. i’ll put it that way. ben bernanke did make comments after the last fed meeting and said the trouble in washington was the reason they were standing pass for now. obviously he was right. look at what happened since then. at this point you try to figure out what pd in washington will have a serious impact on the economy. you haven’t seen it in ub ins, but what’s your guest in terms of if we were to get a resolution by the end of the week, how big the impact would be on the economy? if they get a resolution today, i think opinion of congress still will have diminished significantly. i don’t think that will change the world or certainly won’t change the people’s feeling about the reserved currency. what would do the job, both parties say this is a weapon of mass destruction. we’re not going to use it. we’ll fight in trenches but not going to blow up the world to get our way. that doesn’t sound like conventionalism in washington.

When we set up the energy leadership council, this group of retired four star admirals, generals and ceo of oil using companies we were importing about 60% of our oil everyday. what happened to the light? today it’s less than 40%. much progress. i know it’s your job and a lot of guys that protect our nation, that’s your job to worry. we are in a better position now to some day take that weapon away from opec and people that don’t like us? it must be gratifying. joe, that’s well said. it is before. trend lines are encouraging. as fred mentioned we’re still importing 40% of the requirement today. we believe that as a nation, we’ve got to work on it. eventually we’ll achieve the energy security. i want to point out joe, when opec instituted the oil embargo 40 years ago to punish the united states in particular for support of israel during the war, we were only importing 35% of our oil. withholding oil supplies through the united states economy and complete chaos.

sflieth. supplier in many respects. fruit of a loom. and also supply jewelry to them. there’s a lot of questions about the health of the company. you as a former retailer yourself in the department store and now somebody that has a lot of retail business, you’ve been watching this. what do you think about what’s been happening? it’s very tough. the trouble with retailing is the competitor is always moving. getting your act together which they’re doing is important. at the same time all others keep moving. it’s just very tough. i have this huge rooting interest. i worked there when i was 16 selling shirts $1.98. i sold men’s clothing, childrens and i loved it. i have always loved the company. it’s tough to run it. of course when you have to do something like selling out whether 38% or a large number of shares it makes it very tough. coming from behind in retail is very tough.

The stock market compared to most asset classes in my view is the most attractive place to have your money over the next 20 years. over 20 days or 20 weeks i don’t know. we have our money in businesses. we all all of some businesses, parts of some. we call those stock. we think that’s where value lies. we had mark as a guest on the show yesterday. he laid out the argument about just by looking at formulas, playing the averages, that we are due for another correction at some point. you never know when or how that’s going to happen. it was an argument for not getting caught up in the euphoria of the market and making sure you were diversified. do you think we’ve reached the stage in this market people have to worry about bubble levels? no. we could at some point. no. stocks are not selling at bubble levels. i think it’s a terrible investment compared to equities. so you’re going to have your assets in something. good businesses held for a long period of time are certain to deliver good results from this

What advice would you give to the republicans this morning? i would give this advice to republican because they’ve dug the hole. i’m not saying the democrats haven’t done it in the past but this particular hole belongs to the republicans. i think if they were wise, they do not want to be remembered as the party that destroyed a reputation that americans built up more than two centuries. i think i would tell them to follow herman hickman’s advice. when he was a coach at yale, i believe it was herman who said if you’re getting run out of town, turn around and make it look like you’re leading a parade. i would suggest the republicans do that. how do you do that? i know we’re almost out of time. it’s the hardest line in the world but they made a mistake. they can fight out the budget, they can fight out obama care, everything they want, on other grounds but they can’t do it by holding a nuclear weapon, which in the end they can’t use.

About the author:

I am working towards the CPA & CFA designations, and would love to manage an investment partnership in the future. I am a self taught investor through Warren Buffett, Charlie Munger, Ben Graham, Peter Lynch, Joel Greenblatt, David Einhorn, Seth Klarman, Howard Marks, Phillip Fisher and Thornton O’Glove. My focus is a bottoms up Value-GARP strategy with a mix of top down contrarianism.

“When you find yourself on the side of the majority, it is time to pause and reflect.” – Mark Twain

Personally, I think even attempting to call a top on this character of an equity market is an exercise in the self-infliction of pain for now. It has been a long time since I’ve seen this type of speculation, but it’s been never since I’ve seen this type of monetary largesse. Moreover, when was the last time both the Fed and politicians have meaningfully attempted to “shape” societal perceptions, let alone hoped for economic outcomes, via manipulation of the financial markets? We know capital is “concentrating” right now, and the repository is US and large global equities. The Fed has been 100% successful in forcing capital into equities and real estate, exactly as their years ago game plan detailed. Likewise, with the tapering genie now out of the bottle, we are watching a rescission of global capital that originally spread out across planet Earth as QE went to ever greater heights since 2009. The outgoing tide is now coming in. These two forces, domestic investment concentration in one asset class and an incoming tide of liquidity from broader global risk assets (think emerging markets, commodities and the metals) characterizes the moment. And for now, liquidity and the weight and movement of global capital trump strict fundamentals. Nothing new, we’ve been here before.

But a funny thing happened on the way to new equity highs recently, for the first time in many a moon we’ve begun to see more than a few noticeable technical divergences. Remember, technical analysis is a suggestion, not a hard and fast mandate. It suggests to us what might be, as opposed to definitively speaking to what will. Technical signals, especially in this character of a market, can change meaningfully and fast in both directions. A lot of tried and true historical “systems” have simply broken down for now. After all, technical analysis is tough enough in a free market environment, let alone the type of one in which we now find ourselves. As always, adaptability is essential for survival.

I promise, the last thing I’m trying to do in this discussion is call a top. This is merely an attempt to provide perspective. I’ve seen many a market that was a “no lose” environment…until the losses started. I’ve seen markets where complacency reigned for an extended period…until it didn’t. You know the routine. So rather than pontificate about where equities are headed next, primarily because I have no idea (and neither does anyone else), I thought I’d simply let a number of charts do the talking. Again, perspective, not predictions.

One very apparent divergence we’re seeing right now is the NYSE advance/decline line relative to the S&P itself. The cumulative AD line has been in a range since mid-May, while equities have journeyed to recent new high territory.

….read more and view 8 more charts HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair