Timing & trends

The commodity hedge funds are simply collapsing. This is one reason why you will also see the low in gold unfold. With all the ranting, screaming, claims of hyperinflation, threats of investigations, and prognostications that the dollar will end, not only has gold declined, but the appetite for investing in commodities in general.

The commodity hedge funds are simply collapsing. This is one reason why you will also see the low in gold unfold. With all the ranting, screaming, claims of hyperinflation, threats of investigations, and prognostications that the dollar will end, not only has gold declined, but the appetite for investing in commodities in general.

Clive Capital, who was once the largest Commodity hedge fund, announced it was winding down and returning $1 billion to investors after two years of losses. Being bullish on commodities (including gold) has not paid off in the last two years. Numerous hedge funds are closing. This has included Arbalet, Bluegold, Centaurus, and Fortress. Clive Capital wrote in their announcement to clients:

“We perceive there to be limited suitable opportunities at this point in the economic-demand and the commodity-supply cycles to enable us to utilise our directional, long volatility approach to generate the strong returns of the past.”

This is reflecting the collapse in liquidity and the general deflationary side of this implosion within the world economy. As the G20 continues to hunt money now on a global scale, they will force more and more capital into hiding and the economic contraction to become far worse the more they tax and seek to make illegal anyone with money outside their own country. They are lawyers – not economists or market traders. They only see their own side – power. They do not comprehend what they are doing to the world economy and how they are destroying the future for the next generation reflected in the more than 60% unemployment among the youth.

More From Martin:

Deflation + Inflation = Stagflation

New York Times reports President Obama has rejected a proposal from House Republican leaders to extend the nation’s borrowing authority for six weeks (raise debt ceiling). Yet both parties saw it as the first break in Republicans’ brinkmanship and a step toward a fiscal truce.

As the incompetence in Washington continues, crude oil prices have started to do the unexpected – at least to some folks anyway.

After falling during the initial stages of the crisis, oil prices have started to climb.

This morning WTI is up modestly, while Brent is continuing a trend of stronger prices that appears to be accelerating.

According to the “traditional wisdom,” none of this is really possible.

Given all of the financial uncertainty (and that is an understated way to describe the circus in DC), oil prices should be falling due to the associated decline in demand.

But in reality, the exact opposite has started to happen: Prices are rising, not falling off the cliff.

So what’s the reason behind this apparent disconnect in oil prices?

Here’s my take on crude, along with a developing opportunity in natural gas…

…..read more of “What’s Really Behind the Rise in Oil Prices”

This stainless steel car engine part to the right was created using a laser-sintering 3D printer.

This stainless steel car engine part to the right was created using a laser-sintering 3D printer.

While laser sintering printers are currently one of the priciest variety of 3D fabricators available, they also reduce waste as any unused metal powder can be reused.

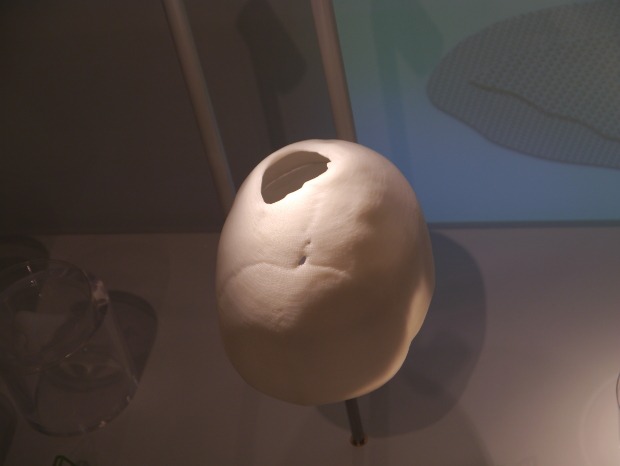

Professor Dietmar Hutmacher from the University of Queensland in Australia used 3D printing to help repair a hole in a nine year old girl’s skull.

The professor took a 3D scan of the girl’s skull and used it to design a 3D scaffold that could be placed in the missing piece of her skull.

The professor took a 3D scan of the girl’s skull and used it to design a 3D scaffold that could be placed in the missing piece of her skull.

Inside the scaffold was a precise network of channels that could hold bone cells and allow new tissue to grow. The scaffold was printed using biodegradable materials, which

meant after three years it dissolved, leaving new healthy bone that filled in the hole in her skull.

A new exhibition has opened in London to show off the multitude of uses that are being found for 3D printers. View 10 more astonishing images & descriptions of what 3D printers have done HERE

The impact of 3D printing on manufacturing will be as profound as the Industrial Revolution by the estimation of some tech industry pundits.

Today there are certainly a growing number of industries building 3D models, with fields as diverse as aerospace and biotechnology finding a use for 3D printing.

Lower cost 3D printers are beginning to find their way into homes too, with 3D printers priced at around £1,000 available in office and computer stores, as well as shopping hubs like Amazon.

There’s also a burgeoning community of hobbyists building their own 3D printers based on open source designs, such as RepRap, and sharing designs for a wealth of objects through the online portalThingiverse.

Even more exotic uses of 3D printers are being researched, including machines that build bone using stem cells and that create objects out of wood filaments, cement polymer and salt.

“3D printing is really reaching out and touching everything. It’s comparable to the web in that it’s a technology that can be applied to whatever you want it for,” said Dave Marks, media and content director for 3D Printshow, which provided the printers for the show.

The breadth of what 3D printers can build was on show at the Science Museum in London, which yesterday opened an exhibit of more than 600 3D printed objects ranging from satellite sensors to prosthetic arms.

3D printing has several advantages over traditional manufacturing techniques. Building a model doesn’t require spending thousands or more to set up machine tools and then thousands more when you want to change that model. It makes it financially viable to build one-off models and to tweak and customise 3D models in a way that would rapidly become hugely expensive using traditional manufacturing methods. Making simple repairs to old household appliances, rather than replacing them, also becomes more viable when spare parts can be printed off in your living room, rather than having to be tracked down and ordered online. Using a 3D printer also cuts down the supply chain: the network of factories, warehouses and shipping companies normally needed to get a product to an end user.

3D printing can also build objects using novel materials with complex shapes and structures that would be extremely difficult to reproduce using traditional methods. General Electric recently revealed a 3D-printed ceramic and carbon fiber jet engine whose lightweight design should allow for fuel economy unmatched by conventionally made counterparts. Waste can be reduced as the printer is generally using only the materials needed to build the object, rather than carving material out of a larger structure to create an object.

But in general 3D printers are also slow, two-inch high figurines printed out at the Science Museum exhibition took about one hour to print, are far more expensive than traditional manufacturing techniques for mass production and consumer grade 3D printers are only able to produce relatively simple plastic models.

How 3D printers work

3D printers work by taking a 3D computer model and slicing it into layers. The 3D printer then builds the object layer by layer using one of a number of methods.

Most home and hobbyist printers print using Fused Deposition Modeling (FDM), which basically builds a model out of molten plastic. FDM machines feed plastic thread into a printer head, where the plastic is melted and squeezed out of a nozzle called an extruder. The head traces the outline of each layer, gradually building the model using melted plastic.

The quality of the finished model depends on many factors, including the quality of the base material, how thinly sliced the model is, the mechanics of the 3D printer and the care taken in preparing the 3D computer model.

Yet the quality of 3D models produced by FDM generally don’t match those built by some other more costly 3D printing technologies used by industry. One such technology is laser sintering.

Laser sintering uses a laser to fuse powder together into the model. The process works by tracing the outline of each each layer onto powdered material using a laser to fuse the object together layer by layer. Laser sintering is able to reproduce fine details and build models out of a wider range of materials than FDM, such as ceramics, metals and glass.

While the FDM printers available to novice home users today generally produce relatively simple models in a single colour and material, more advanced machines are becoming available.

The quality of 3D printers available to home users is expected to take a leap forward from next year after patents run out on key technologies related to laser sintering, which in the long run may make sintering machines affordable for the home user.

View 10 more astonishing images & descriptions of what 3D printers have done HERE

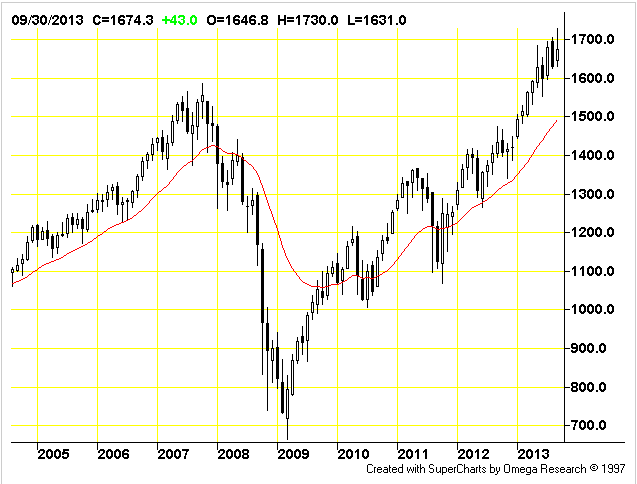

Every bull market must end at some point and the US market has rallied hard the past year. If you believe the market may have peaked momentarily, you have company in the name of Dr Faber. “We are in a bull market that is in the tail-end instead of the beginning but that does not mean prices will collapse. I don’t think that stocks are the greatest bargain anymore.” (click monthly chart on right for larger view)

Every bull market must end at some point and the US market has rallied hard the past year. If you believe the market may have peaked momentarily, you have company in the name of Dr Faber. “We are in a bull market that is in the tail-end instead of the beginning but that does not mean prices will collapse. I don’t think that stocks are the greatest bargain anymore.” (click monthly chart on right for larger view)

Shares of Casinos in Macau, Iraqi stocks & Physical Gold an Insurance against Mischief

(article source: HERE)

Legendary investor Marc Faber has shares of casinos in Macau interesting buys of Iraqi stocks and sees China’s currency as a serious competitor to the dollar.

Business Week : Mr. Faber, you have to buy gold?

Faber: Yes . Owning physical gold is for me personally an insurance against mischief , driving the governments . In the worst-case scenario …

with state bankruptcies … or hyperinflation …

governments … will not say : Oh, we have made a mistake. You will not find culprit.

And that will be the wealthy ?

I do not think that the individuals’ assets remain untouched.

Gold as an insurance against crises , this is the one . What if I want to speculate ?

As an investor, you can make more money with gold mining stocks . Were virtually destroyed the last price drop and are now favorable to have .

The turnaround in interest rates in the United States has failed , the Fed continues to print money. Is that good for stocks?

The Fed operates in 20 years a policy of monetary expansion . After the collapse of LTCM in 1997 , after the collapse of the Nasdaq and after the real estate crisis, interest rates were kept artificially low – at virtually zero percent today . In March 2009 the U.S. stock index S & P 500 reached its nadir with 670 points. Now we are at 1700 points – a tripling ! The artificially low interest rates and bond purchases have reduced the prices of stocks and real estate driven up . But the economic effect was relatively small . Milton Friedman wrote in ” Capitalism and Freedom “: The problem with government programs , they can always be started due to an emergency , but not abolished , when the emergency is over. Thus, the state is getting more bloated. For the Fed , it is becoming increasingly difficult to end their policy. And if they still do it one day , what will happen to the stock market ?

Which markets are still interesting because for stock investments ?

If you press me 100 million euro in the hand and say that you have to invest in stocks, then I would probably select emerging markets, which has dropped so dramatically lately . Malaysia, Thailand, Hong Kong , Singapore – there are plenty of stocks that have a dividend yield of five percent. That’s not huge, but still signaled that the cash flow of the company is okay. The Vietnamese market is interesting. Japan was not thrilled me, but the Nikkei could run better than other markets .

Sounds underwhelming .

We are in a sideways market. This was back in the seventies when I started my career like that. Nevertheless, there are of course opportunities. Some industries developed tremendously in this sideways market. Did you have gold or energy stocks, you were rich.Marc Faberis an international investor known for his uncanny predictions of the stock market and futures markets around the world.

- Marc Faber : Money left in The Bank loses Purchasi…

- I do not particularly like Chinese Companies . The…

- Responsible Investors Should own Gold

- GOLD is relatively Cheap right now

- Economic Collapse 2013 – Marc Faber Dutch TV Full …

- Faber: Chinese Growth may slow to 4%

- Marc Faber : I started to Invest in Iraqi Stocks …

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair