Stocks & Equities

BY CHRIS CIOVACCO

As we mentioned Tuesday, the reaction to Wednesday’s Fed statement is important to the market’s intermediate-term direction. However, Apple’s (AAPL) strong earnings have provided investors with a reason to step up to the buyer’s plate. From Bloomberg:

Apple Inc. (AAPL) profit almost doubled last quarter, reflecting robust demand for the iPhone in China and purchases of a new version of the iPad, allaying the growth concerns that sliced shares 12 percent in two weeks.

Since Europe continues to be the possible “fun sponge” for the bullish party, and Germany tends to pay the uncomfortable European clean-up tabs, the German DAX Index has served as a good proxy for the tolerance for risk assets. Germany has had a strong start to trading on Wednesday. Later in this article, we review the longer-term technical backdrop for the German stock market.

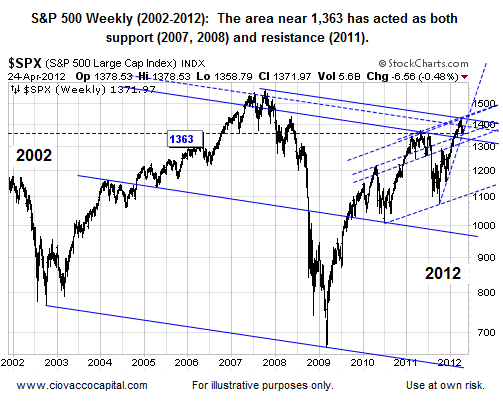

Picking market tops and bottoms is difficult at best. It is better to think in terms of a probabilistic bottom or top. One way to help discern if it is probable for a market to move higher is to look at long-, intermediate-, and short-term trendlines on both an absolute and relative basis.

When reviewing the charts below ask yourself, “Does this market seem to be at a logical point where a reversal could take place?” If the answer is “yes”, then we become more open to a possible buying opportunity. A few weeks ago we identified 1,363 as a possible point of inflection for stocks. The S&P 500 has been testing 1,363 for two weeks. On April 10, the S&P 500 closed at 1,358, which thus far has represented the lowest close during the current pullback. While we want to see some real conviction from buyers, the chart below seems to have a reasonable probability of producing a reversal to the upside.

To Read More CLICK HERE

Jack Crooks

“I guess I should warn you, if I turn out to be particularly clear, you’ve probably misunderstood what I’ve said.”

– Alan Greenspan

Are there no limits whatsoever to monetary policy? It is beyond pathetic that a rising stock market seems the only substitute for real policy from our “best and brightest.” Why doesn’t it matter to them that it isn’t working? Are they that intellectually bankrupt and corrupt? Is it odd that very smart people outside the government continue to bet on QE 3,4,5,6…? Or is it the only bet? What in the world is going on here?

Orders for U.S. durable goods fell in March by the most in three years, indicating manufacturing will contribute less to growth this year.

Bookings for goods meant to last at least three years dropped 4.2 percent, the biggest decrease since January 2009, after a revised 1.9 percent gain the prior month, data from the Commerce Department showed today in Washington. Economists forecast a 1.7 percent decline, according to the median estimate in a Bloomberg News survey.

Now, would throwing more money into the banking system “help” this problem of slowing US growth momentum?

To Read More CLICK HERE

All eyes are on the Federal Reserve this week as they convene their latest Open Market Committee meeting on Tuesday and Wednesday to discuss monetary policy. A primary focus of investors is whether the Fed will hint about any future policy action.

Such news is important, as the stock market has proven keenly sensitive to the influences of monetary stimulus since the outbreak of the financial crisis several years ago. But while another round of policy support may help stabilize the stock market at current levels, Fed stimulus alone may no longer be enough to drive stocks to new highs. Moreover, it may now be insufficient to offset the forces of a major downside shock.

A reflection on the movements of the stock market since October 2011 is informative in this regard. The U.S. stock market as measured by the S&P 500 Index (SPY) initially exploded higher at the launch of Operation Twist. Having touched a fresh cycle low at 1075, the stock market suddenly reversed and didn’t look back for the entire month. From the second day to the second to last day of October, the stock market advanced roughly +17%. But what is surprising is that since the end of October, the net impact of Operation Twist by itself has actually been fading lower from its peak.

The first sign of breakability associated with Operation Twist came on Halloween, as the market became spooked by the collapse of MF Global. By Thanksgiving, the U.S. stock market had bled nearly -10% and was only +5% above the early October lows. The market response to the MF Global bankruptcy was notable, for stocks prior that point had shown the resilience to continue rising during periods of Fed stimulus regardless of the risk. Such was not the case in November 2011.

Stocks thrashed back and forth into December until the week before Christmas. It was at this point on December 21 that the European Central Bank executed the first of its two planned Long-Term Refinancing Operations (LTRO) to support the at risk banking system across the continent.

It was upon the launch of LTRO that the stock market propelled itself into another euphoric melt up phase. This continued until the second planned LTRO on February 29. Along the way, the stock market advanced +14% in a virtually uninterrupted rally that included stocks rising on nearly 70% of trading days over this time period. This is well above the historical average of 52% and is exceptionally rare to occur over any sustained period of market history.

To Read More CLICK HERE

It appears that when it comes to mocking consensus groupthink emanating from lazy career ‘financiers’ who seek protection from their lack of imagination and original thought, ‘creation’ of negative alpha and general underperformance (not to mention reliance on rating agencies, only to jump at the first opportunity to demonize the clueless raters), in the sheer herds of other D-grade asset “managers” (for much more read Jeremy Grantham explaining this and much more here), David Rosenberg enjoys even more linguistic flexibility than even us. Case in point, his just released trashing of the latest Barron’s permabull groupthink effort titled “Outlook: Mostly Sunny.” And just as it so often happens, no sooner did those words hit the cover of that particular rag, that it started raining, generously providing material for the latest “Roasting with Rosie.”

From Gluskin Sheff:

Consensus Creates A Contrary Call

When the experts and forecasts agree, something else is going to happen.”

Bob Farrell’s investment rule #9.

Did the folks at Barron’s intentionally lob a ball right into my wheelhouse? The front cover says it all — Outlook: Mostly Sunny. Check it out. Any perma-bull out there right now should be trembling by the front cover effect. This is no different than the fabled Death of Equities in the 1979 Businessweek, the Economist front cover calling for oil prices to basically head towards zero circa 1998, and the front cover of Barron’s a decade ago saying That’s All, Folks when it came to interest rates supposedly bottoming out. Come to think of it, Barron’s ran with Dow 15,000 on its front cover back on February 13, 2012, and last we saw, at the nearby peak in early April, the blue-chip index closed 1,700 points below that threshold (and has been roughly flat since the date of that article).

What Barron’s is referring to here is the latest Big Money poll that it conducts semi-annually. The actual title of the article (on page 25) is Reason to Cheer. Reason to cheer? About what? Margins being squeezed? Profit growth practically evaporating? Earnings downgrades still significantly outpacing upgrades? The recovery so excruciatingly slow that senior members of the Fed are contemplating QE3? Insolvency of Spanish banks? Hard landing risks in China? The 2013 fiscal cliff? The fact that over 60% of the data in the past two months have surprised to the downside?

The results of the Big Money Poll were startling:

55% of the portfolio managers are either bullish or very bullish. Only 14% are bearish or very bearish.

Financials and technology are the favourites, with 31% citing both as being the top performers in the next six to 12 months.

Favourite stock … Apple (surprised?).

Utilities are seen as the worst performer — by 30% of those polled.

With respect to Treasuries, 81% are bears, just 2% are bulls. How can yields rise in such a lopsided environment? I mean, who is there left to sell? This is a classic bullish contrary signpost.

Bonds of all types are detested — 33% bearish on corporates while 14% are bullish; 35% are bearish on munis while only 12% are bullish.

But … 41% are bulls on real estate; only 10% bears are left.

For gold, 39% bears and 30% are bulls. That is great— the one asset class that has been in a secular bear market for 12 years is adored (equities), and the two that have actually made you money over this time span (the bond- bullion barbell) is to be avoided. Go figure!

To Read More CLICK HERE

By Alex Daley, Chief Technology Investment Strategist

“What made Instagram worth $1 billion to Facebook?”

When asked this question recently, I responded with an immediate, “Nothing.”

I’m not usually so terse or emphatic with my answers, as any longtime reader knows. But in this case, there really was nothing inherently valuable inside Instagram that made them worth the unbelievable sum Facebook agreed to pay. Yet they did it anyway. Clearly, there’s something missing from a traditional valuation analysis here.

That missing piece is what Instagram could have become in the hands of a competitor or even on its own, had Facebook not gone ahead with the marriage. Nearing its IPO, Facebook was willing to overpay in order to quash any potential risks that Instagram posed, both to the company’s reputation and its content stream.

Instagram by the Numbers

On the surface, Instagram might look like small potatoes. It has only one product: an application for smartphones that can take square, Polaroid-style throwback images, run them through a few cool filters to make them look snazzy, and share them with other users. Even though it has some sharing capability built into its own app, the overwhelming majority of photos are instead posted to Facebook (or Twitter or Posterous or other social network) with the app’s simple integration.

There is no magical computer science involved. The app – minus some intricacies that allowed it to scale to millions of users without buckling under its own weight – is simple enough that most any solid mobile developer could have thrown it together. This is not to dismiss the hard work the twelve-person company put into it – I am sure many late nights were spent on the finer details, squashing bugs, and the like – but it’s not exactly a fighter-jet simulator or climatology model. Facebook obviously didn’t want the company for its cutting-edge patents, code, or other intellectual property.

So maybe it had to do with the user base? True, the application is insanely popular, having been downloaded more than 30 million times according to the App Store statistics from Apple, and another 5 million on Android. (Of course, Apple and Google have it in their best interests to overcount those users, by including updates, reinstalls, upgraded phones, etc. But it is the best proxy we have, and we can reasonably assume Instagram still had tens of millions of users.) Plus, it was named “application of the year” by Apple for 2011, which was bound to further boost its appeal and draw in new users.

But Facebook already counts 850 million registered users, according to its most recent press releases. Even adding 30 million to that number would cause barely a ripple. And given that the most popular use of the application is to upload to your existing Facebook account, we doubt that it will bring many, if any, new users to Facebook. This was not about adding instant market share.

Nor did the two-year-old Instagram bring much in the way of revenue to the table. In fact, the company has no revenue stream at all; it was living off of $7 million in venture capital funds it managed to raise on the back of its early success, having garnered 1.75 million downloads just four months after its launch. (The product, by the way, was built on just $500,000 in seed funding pre-launch.)

No revenue, little money in the bank… you might think a company like that would come cheap. That instead, Facebook believed it justified a $1-billion pricetag tells us that Facebook values the company for something more than Instagram’s application, audience, or earnings.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair