Stocks & Equities

WEEKLY COMMENTARY

Perspectives for the week ending July 8, 2013

Stockscores Market Minutes Video

This week’s Market Minutes video shows what a hot stock is and the critical element for finding them. Watch it on YouTube by clicking here.

This Week’s Trading Lesson

The start of July has been very slow for trading but the action should pick up this week as the market focuses on earnings announcements. Any recent action has been more concentrated in the US market over the Canadian but there is starting to be some interest in the Energy sector as Oil is back up over $100 a barrel. In the US, the Biotech and Solar sectors have been the strongest.

This week, I share some basic thoughts and rules on trading:

Don’t apply logic to the stock market.

So often I see people make decisions in the market on what makes sense to them. It makes sense to buy stocks when the company insiders are buying. It makes sense to buy stocks that are making positive announcements. It makes sense to listen to what the President has to say about the company’s prospects. However, all that matters is what the market thinks of the company and whether the buyers are more motivated than the sellers. So often, the market does things that do not make any sense until we later learn of what motivated the market to do what it did. Remember, the market is forward looking, most times, what makes sense is judged on what has happened in the past.

Never average down on a losing position

Buying more of a bad thing is not much different than continually betting on a losing horse. Winners win for a reason, and until your stock starts to show that it is a winner, don’t add more to a bad situation. If you like a company whose stock is losing you money, sell it. You can always buy it back later when the market starts to like it again.

Successful investing is not about being right, it is about making money

Most good traders are usually wrong. They will lose small amounts often and make big amounts occasionally. What matters is how much they make over a large number of trades. Don’t try to always be right, simply work to make money.

Resist doing what feels comfortable

We have a tendency to look for the market to prove our decision is a correct one before we make our move. The problem is that this often means we are too late to capitalize on the opportunity. We have to move before the crowd, and that often feels like a dangerous thing to do.

Anyone can get lucky in the short term, only good traders succeed in the long term

Don’t confuse making money in the stock market with knowing what you are doing. It is easy to get lucky on a stock or on a sector and enjoy gains that give credence to your analysis method. However, short term winners often give back all of their gains because they fail to recognize their success as luck.

Be patient with your winners, not with your losers

The natural tendency is to sell your winners too early and hold on to your losers, hoping for a turnaround. A simple, but not easy, thing to do is reverse this tendency. When the market proves you right, wait to sell on a signal that indicates the stock is likely to go lower. When the market proves you are wrong, let the trade go and take the loss.

Publicly available information is priced in to the stock, don’t rely on it to make decisions

Once information, no matter how good, is made public, it loses its usefulness to you.

Public information is priced in to the stock by the market of investors. Information only has value to you if the market has not priced it in.

Make sure your trading strategy has an edge

A trading strategy is only worth trading if it can be shown that it consistently makes money. Establish your trading rules and test them over a variety of market conditions so you know that it is effective. Time spent testing a strategy to prove it is a money maker can save you a lot of money in the market.

People lie, markets don’t

I have learned the hard way to never trust what people say, their actions say much more. Learn to read the market and understand it’s message. No matter how much insight a person may have, recognize that they have a bias based on their own emotional attachment to money.

It is easier to trade with the trend than against it

Understand the mood of the market and trade with it. Don’t chase euphoria, but seek to buy stocks that are in the control of the buyers. Don’t sell on fear, but seek to sell stocks that are under seller control.

STRATEGY OF THE WEEK

This past week was very quiet for the market because of the holidays but here is one stock that is worth considering.

STOCKS THAT MEET THE FEATURED STRATEGY

1. T.SGY

T.SGY made a good cup and handle break. The chart is good but I like the stock better on a pull back. The company recently did a financing at $5 which means there is some cheap stock out there that could be sold in to this strength. The longer term outlook for the chart is very good.

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

Almost everyone I talk to thinks the European sovereign debt crisis has passed. All is on the mend in Europe, they say.

But as far as I’m concerned, nothing could be further from the truth.

First, severe austerity measures continue to this day, and they are hollowing out Europe’s economic growth.

The proof is in the numbers. Before the Greek crisis flared up, debt-to-GDP in Greece stood at 113 percent. Today, even after all the write-offs, Greece’s debt-to-GDP is a whopping 157 percent.

In Spain, pre-crisis debt stood at 40 percent of GDP. Today it’s 84 percent.

In Italy, it was 106 percent. Now it’s 127 percent.

In France, it was 68 percent. Now it’s 90 percent.

Even Germany’s debt-to-GDP is worsening, leaping from almost 67 percent in 2008 to 82 percent today.

Debt-to-GDP is as much as 44 percent higher than it was at the beginning of the crisis, and the austerity measures are causing the entire European continent to implode, creating some of the worst social chaos we have seen in modern times.

Second, Italy, Portugal, Spain, and Greece remain hotbeds for massive social unrest.

Second, Italy, Portugal, Spain, and Greece remain hotbeds for massive social unrest.

Each and every one of these countries is in way over its head. And each and every one of them is in the depths of a nightmare caused by austerity measures. Just last week, two Portuguese cabinet ministers resigned over the harsh austerity measures the country has had to endure.

Spain’s unemployment just hit 26.9 percent. Portugal’s, 17 percent. Italy’s, 12.2 percent.

Unemployment among youth is off the charts. Spain’s under-25-year-old unemployment rate is 56.5 percent. In Greece, it’s even worse at 59.2 percent.

Corporate and personal bankruptcies are surging. Social discontent is on the rise again. And tensions between countries within Europe are higher than ever.

Third, European banks are a disaster in the making. According to Weiss Ratings, 202 financial institutions in Europe with capital of more than $16.1 trillion are rated D+ or lower.

I repeat, that’s $16.1 trillion of capital — equal to our country’s GDP — at risk of going up in smoke.

It’s the ugliest economic picture for Europe since the 1930s, when 17 countries went belly up, sending hundreds of billions of dollars worth of francs, marks, lira, and more flooding into the U.S.

That, in turn, sent the U.S. stock markets exploding higher. It sent the dollar and gold simultaneously into a moon shot as well. And it’s all about to happen again.

Why? Because …

Fourth, Europe’s economy as a whole is sinking fast. Eurostat, the European Union’s statistics office, said unemployment in the euro zone hit a record high of 12.2 percent in May. A total of 19.34 million people are unemployed.

Figures due out next month are expected to show that the euro zone continued to shrink in the second quarter, the seventh quarter in a row.

With growth sharply slowing, plus uncertainty over which dominoes will be the next to fall, there’s a very real chance of a massive bear-market collapse in Europe this year, one that could take down the entire European Union.

Fifth, deflation is high. With austerity measures squashing growth all over Europe, deflation is starting to run rampant.

According to the latest data, prices that euro-zone producers charged for their goods fell for the third straight month in May, while producer prices in the 17 countries that use the euro declined 0.3 percent. That may not sound like a lot, but annualized, it’s a 3.6 percent deflation rate.

On top of that, Europe is facing more hits to economic growth, more debt going bad, more unemployment and more social discontent in the months ahead.

In short, nothing, and I mean nothing, has been solved in Europe. The crisis will soon escalate with a vengeance.

So what does all of this mean for you and your investments? A heck of a lot!

When, not if, Europe’s economy roils again, likely later this summer:

First, you’re going to see trillions of euros stampede for the exits. That’s going to send several large European financial institutions down the tubes.

Second, that will likely send global interest rates rocketing higher. The U.S. will not escape rising interest rates. In fact, our rates are already heading higher.

Third, it’s going to send the U.S. dollar into rally mode, right along with gold. Just like it did in the early 1930s when Europe last went bankrupt.

Fourth, it’s also going to send our stock markets roaring higher. Just like it did between 1932 and 1937, when the Dow Jones Industrials soared 387 percent as Europe went under.

Fifth, it’s going to give you many profit opportunities to potentially make more money that you ever dreamed of. In stocks. In commodities. In the dollar. And in gold and silver.

My suggestions right now are …

- Keep your eyes on Europe. And keep most of your liquid funds in cash, ready to be deployed on a moment’s notice, but as safe as can be right now.

The best way, in my opinion: A short-term Treasury-only fund in the U.S., or the equivalent.

- Earmark a portion of your cash for speculation. Not too much, and not too little. I recommend 25 percent of your total investable funds. Funds that you do not need for anything else.

Finally, pay particular attention to gold and silver. They now offer more profit potential than they have in at least the past two years.

Best wishes,

Larry

Everyone loves making gains while markets rise, and we always hope that the good times will continue, even though we know deep down that markets simply don’t work that way. Right now, we have a clear dichotomy between the investment positioning of Institutional Managers (with Fiduciary Duty), and the recommendations of retail advisors.

Everyone loves making gains while markets rise, and we always hope that the good times will continue, even though we know deep down that markets simply don’t work that way. Right now, we have a clear dichotomy between the investment positioning of Institutional Managers (with Fiduciary Duty), and the recommendations of retail advisors.

Many big-money managers with Fiduciary Duty to their clients are taking their portfolio risk down by selling to those late-comers who are kicking themselves for not having bought during the previous panics. The buy and hold crowd including most mutual fund sales people are singing the same tune as always. Remember, mutual fund sales people only get paid their trailer fee if they keep you invested (no conflict of interest there, eh?)

As with every aspect of your life, you should make your decisions based upon your own priorities, not upon what others think is “the right thing to do.” In these silly markets, be Mindful of Your Priorities.

In this context, here’s the critical question: Is it more important for you to try and squeeze a few more percent of possible gains from equity markets, or is it more important for you to focus now on preserving your capital from the emerging risk?

When asked the above question near market highs, prudent tactical investors answer in exactly the opposite way that the majority do. “The Masses are always wrong at the extremes, but help create the trend in between.”

While the mainstream financial press is yammering on about whether or not the Federal Reserve will actually follow through on its recent musings about “tapering” its $85 billion of monthly market stimulus, here are some things to consider:

- Europe’s currency, stocks and peripheral bond markets are showing signs of FINALLY falling apart,

- Precious Metals are failing to rally with any strength and thereby foreshadowing more declines,

- Q2 Earnings Estimates are being significantly downgraded globally, and

- For 19 specific reasons to be concerned about the Global Economy, Click Here: http://www.zerohedge.com/news/2013-07-05/19-reasons-be-deeply-concerned-about-global-economy

Meanwhile, stocks are already priced for perfection. Over the next couple months, does this strike you as a time to stay in, or get your capital to safety?

In these silly markets, be mindful of your priorities, and follow through with a specific plan that matches them. If your advisor tries to impose their agenda over your priorities, just remember whose money it is.

Patience and Discipline are accretive to your wealth, health and happiness; Fear and Greed are destructive.

As a general rule, the most successful man in life is the man who has the best information

Illusions trick us into perceiving something different than what actually exists and the mainstream media is very good at creating them. Currently they have the herd convinced there is an economic recovery underway.

We all need to understand that to have a real, and sustainable recovery for an economy that relies on consumer spending for 70 percent of its activity we need to have a jobs recovery.

Okun’s Law holds that an economy, it’s GDP, must grow above its potential to reduce the unemployment rate. Year-on-year economic growth of two percent above the trend (considered to be 2–3 percent) is needed to lower unemployment by one point.

A third downgrade of U.S. economic growth for the first quarter 2013 showed the country’s GDP grew at just a 1.8 percent annualized pace.

Bloomberg and IHS Global Insight estimate the U.S. economy will grow by 1.6 percent this year.

Industrial production was unchanged in May, the second straight weak monthly report. Capacity utilization – a measure of how fully the nation’s mines, factories and utilities are deploying their resources – fell to 77.6 percent, well below the average of 80.2 percent experienced from 1972-2012.

The Commerce Department revised growth in private investment to 7.4 percent in the first quarter, down from its original estimate of 12.3 percent.

Imports were originally reported as growing by 5.4 percent but the revised number is now 0.4 percent.

Sequestration – what remains of the ‘fiscal cliff’ after the U.S. Congress passed the American Taxpayer Relief Act – could trim economic growth in 2013 by 0.6 percentage points by cutting $85 billion worth of Federal government spending this year. Over its ten year life sequestration will cut $600 billion of government spending from the economy.

“The drop in growth rate is not temporary, but over the span of at least 10 years in which the sequestration will take effect. And its impact will be more strongly felt in later years, once the fiscal sequestration translates through its negative multiplier effects.” Benjarong Suwankiri, ‘After Fiscal Cliff, Sequestration’ nationmultimedia.com

Hourly pay for U.S. nonfarm workers fell a record 3.8 percent annualized in the first quarter, the largest decline since records started being kept in 1947. This record first quarter decline was on top of the 2012 third weakest annual increase in hourly pay since 1947. Hourly worker pay rose only 1.9 percent in 2012, barely keeping up with the 1.8 percent gain in the fudged downward and much maligned consumer price index.

The growth rate of consumer spending was revised downward to 2.6 percent annualized in the first quarter from an earlier estimate of 3.4 percent.

The labor force participation rate is the percentage of working-age persons in an economy who:

- Are employed

- Are unemployed but looking for a job

“Working-age persons” is defined as most people between the ages of 16-64. Excluded are students, homemakers, and people under the age of 64 who are retired.

According to the Bureau of Labor Statistics the labor force participation rate dropped 0.2 percentage points to 63.3 percent. This is the lowest rate in 34 years.

Considering population growth in the U.S. is positive and is one of the highest rates in developed countries, you’d think labor force participation would be growing, not dropping. The U.S. economy needs to add 150,000 to 250,000 jobs per month just to absorb the workforce’s new entrants never mind make up for what’s been lost since the Great Recession.

“February’s headline unemployment rate was portrayed as 7.7%, down from 7.9% in January. The dip was accompanied by huzzahs in the news media claiming the improvement to be “outstanding” and “amazing.” But if you account for the people who are excluded from that number—such as “discouraged workers” no longer looking for a job, involuntary part-time workers and others who are “marginally attached” to the labor force—then the real unemployment rate is somewhere between 14% and 15%.” Mortimer Zuckerman, ‘The Great Recession Has Been Followed by the Grand Illusion,’ wsj.com

U.S. labor force participation is now down to where it was in 1979. The unprecedented 2.5 percentage point decline in labor force participation under President Obama amounts to 6.2 million Americans being pushed out of the job market – 6,200,000 have stopped looking for work, these people have been forced to give up.

Many of the jobs that are being created are part-time low wage second or third jobs going to those already working. The average work week is now a very short 34.5 hours because employers are shortening workers’ hours or asking employees to take unpaid leave.

“The financial crisis destroyed some $16 trillion in household wealth. Americans have only recovered 45 percent of that amount…But when you break down that wealth recovery by income level, it gets worse. The Fed estimates that 62 percent of that wealth people have regained since the depths of the recession has come in the form of higher stock prices. And 80 percent of stock wealth is held by people in the top 10 percent of the income distribution.” Erika Eichelberger, ‘Sorry, There’s Been No Economic Recovery for Poor and Minority Households’

Here’s a few facts:

- Medium household income has declined. Adjusted for inflation household incomes are now back to levels last seen in the 1990s – average per capita wage is around $26,000, household median income is at $50,000

- Few Americans own any significant amount of financial wealth. The bottom 80 percent of Americans hold roughly 5 to 8 percent of all financial wealth (non-housing related)

- U.S. Employment rate is not recovering, one in 12 Americans are jobless

- The number of Americans living in poverty has now reached a level not seen since the 1960s. There are 50 million poor people in America. There are more than 146 million Americans considered either poor or low income

- There are over 47 million Americans on food stamps

- The banking system backs $7.4 trillion in insured deposits with $32 billion, that’s just .43 percent

- 1 out of 3 Americans have no savings

- Nearly half of American’s die broke

- There are less Americans working manufacturing jobs today than in 1950 even though the country’s population has doubled

- The U.S. has run a trade deficit with the rest of the world of more than 8 trillion dollars since 1975

- The U.S. Social Security system is facing a 134 trillion dollar shortfall over the next 75 years

“The employment trend in manufacturing is overwhelmingly negative and has been for nearly twenty years. This country does not simply lack manufacturing jobs, it lacks entire industries.

The Manufacturers Alliance for Productivity and Innovation (MAPI) released a report in January 2013 detailing the generational decline in manufacturing output and capacity in the United States. In general, for every two new plants that come on line, three others are shut down. For every two jobs created at one plant, three are lost somewhere else.

The companies that make up our so-called “manufacturing base” often survive, but they do so by moving jobs and production overseas. The MAPI report shows dramatic increases in overseas production and sales by the foreign affiliates of American multinationals alongside virtual stagnation of domestic metrics in the United States.” Craig Harrington, The Continued Decline of American Manufacturing, economyincrisis.org

Global

According to the Organization for Economic Co-operation and Development (OECD), the combined government debt held by the world’s advanced economies is at its highest point since the Second World War. In 1945, the debt topped out at 116 percent of GDP; at the end of 2012 it hit 114.4 percent. The OECD says we’ll hit a new high in 2013.

Global trade has slowed. According to the World Trade Organization (WTO) international trade rose 5.2 percent in 2011, two percent in 2012 and growth has been revised downward to 3.3 percent in 2013 instead of the 4.5 percent the WTO predicted last September.

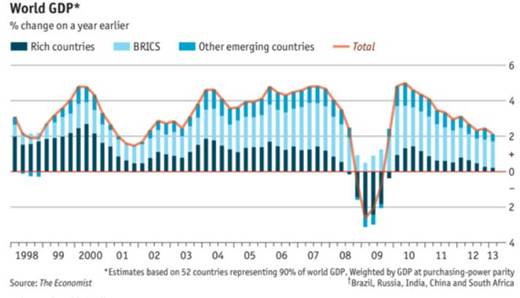

According to The Economist world GDP grew by just 2.1 percent during the first quarter of 2013. The UN Department of Economic and Social Affairs (DESA) says growth of world gross product (WGP) is now projected at 2.3 per cent in 2013, the same pace as in 2012.

In a report titled ‘Update to Global Macro Outlook 2013-14: Loss of Momentum,’ Moody’s, an international credit rating agency, expected the euro area economy to experience a deeper and lengthier recession than previously thought. Moody’s also expects the real GDP growth of developed economies in the G20 countries to stand at around 1.2 percent in 2013 followed by 1.9 percent in 2014.

Unemployment in the euro area has reached an all-time high and is forecast to average 12.8 per cent in 2014.

“A prolonged period of subdued growth and fiscal austerity in many economies has added about 4 million more to the ranks of the unemployed.” Assistant Secretary-General for Economic Development Shamshad Akhtar

Chinese May exports rose by just one percent year on year – the lowest rate since last July – while imports fell by 0.3 percent. Exports to Japan were down by 5.7 percent, exports to the US decreased by 1.6 percent and by 9.7 percent to the European Union. Exports to both the U.S and EU have been falling for three months in a row.

Two gauges of China’s manufacturing fell in June – an official Purchasing Managers’ Index dropped to 50.1 from 50.8 – 50.1 is the lowest level in four months. The PMI report showed declines in sub-categories including output, new orders, input prices and employment – the export orders sub-index was reported at 47.7, the lowest reading since February.

A private PMI from HSBC Holdings Plc and Markit Economics was 48.2, the weakest since September – readings above 50 signal expansion.

The June HSBC/Markit PMI for the services industry (the services sector accounted for 46 percent of China’s economy in 2012) inched up to 51.3 in June from May’s 51.2. Growth in new orders hit a 55 month low and business confidence slumped to 2005 levels.

“China’s President Xi Jinping said over the weekend that officials should no longer be evaluated against economic growth but with consideration to other indicators including welfare and ecological improvements and social development.” Reuters, ‘China June HSBC services PMI expands modestly’

Growth in India has slowed significantly over the last two years while Markit factory gauges for South Korea slipped to the lowest level since November 2012.

Japan, the world’s third largest economy, would seem to be an economic ray of sunshine as its economy grew at an annualized 4.1 percent in the first quarter. A closer look under the hood reveals it was done by flooding the system with money. The flood of fiat has depreciated the yen by 25 percent against the U.S. dollar since the start of the year. A weaker yen has helped boost exports and drive local stock exchanges higher, to five year highs.

“In Japan, a dynamic relaxation of macroeconomic policy has sparked an uptick in activity, at least over the short-term.” The Japan Times News, ‘Japan growth estimate gets World Bank boost’

Abenomics is failing because:

- Consumers in Japan remain convinced the threat is deflation, not inflation, they are not spending

- Japan’s debt is 240 percent of GDP limiting government spending

- The Prime Ministers own party is against structural reforms

- Japanese corporations are not buying into ‘Abenomics’ – corporate investment fell by 4.9 percent in the first quarter

- Abenomics is nothing more than a policy of beggaring your neighbor.

Conclusion

The world’s four largest economies – the U.S., China, Japan and the EU – face extremely strong headwinds on their way to recovery; the lack of jobs and consumer spending, a liquidity crisis and an insolvency crisis. The much ballyhooed recovery is simply an illusion bought and paid for by the world’s central banks with loose monetary policy – money printing has driven the rise in stock markets and house prices.

“The global financial crisis that began in the United States in the summer of 2007 was triggered by a bank run, just like those of 1837, 1857, 1873, 1893, 1907 and 1933.” Yale economist Gary Gorton’s Misunderstanding Financial Crises, Why We Don’t See Them Coming

Gorton writes the 2007-2008 crisis was systemic, spreading from one institution to another, and set off by a run on “repos and asset backed commercial paper” which are“forms of bank debt that grew to significant amounts and were vulnerable to being run on.”

Panic set in, selling becomes widespread – everyone was trying to squeeze out a narrow exit at the same time – from shorter term instruments like repos and commercial paper to longer term obligations like bonds, stocks, commodities and real estate.

Firms thought too big to fail, like Merrill Lynch, Lehman Brothers, Bear Stearns, Wachovia, Washington Mutual and Countrywide Financial disappeared.

In this author’s opinion it’s going to happen again.

It certainly couldn’t be a bad thing to have a little gold and silver tucked away for a rainy day. The recent drop in bullion prices makes for perfect timing.

Is establishing an easily accessible rainy day fund consisting of cash, gold and silver on your radar?

If not, maybe it should be.

Richard (Rick) Mills

Richard is the owner of Aheadoftheherd.com and invests in the junior resource/bio-tech sectors. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, ninemsn, ibtimes, businessweek.com, moneytalks and the Association of Mining Analysts.

If you’re interested in learning more about the junior resource and bio-med sectors, and quality individual company’s within these sectors, please come and visit us atwww.aheadoftheherd.com

If you are interested in advertising on Richard’s site please contact him for more information, rick@aheadoftheherd.com

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Good morning! Here’s what you need to know.

Good morning! Here’s what you need to know.

- U.S. futures are pointing to a higher trading day with Dow futures up 140 points. European markets are slightly lower. Asia rallied overnight led by a 2.0% surge in Japan’s Nikkei.

- It’s jobs day in America. At 8:30 a.m. ET, the Bureau of Labor Statistics will publish its June employment situation report. Economists estimate that the U.S. companies added 165,000 nonfarm payrolls in June, causing the unemployment rate to fall to 7.5%.

- The Bank of England had its first Monetary Policy Committee meeting with Canadian Mark Carney at the helm. In its statement, the BoE said it would look into giving forward guidance. The dovish tone of the statement caused the British pound to tank.

- The European Central Bank straight up gave forward guidance after its monetary policy meeting on Thursday. “Looking ahead, our monetary policy stance will remain accommodative for as long as necessary,” said ECB president Mario Draghi during his press conference. “The Governing Council expects the key ECB interest rates to remain at present or lower levels for an extended period of time.”

- “The risks surrounding the economic outlook for the euro area continue to be on the downside,” added Draghi. “The recent tightening of global money and financial market conditions and related uncertainties may have the potential to negatively affect economic conditions.” The euro tanked on that commentary.

- German factory orders unexpectedly fell 1.3% in May, missing economists’ expectation for a 1.2% gain. This is yet another reminder that Europe’s economy remains deeply troubled, and any economic activity is fragile.

- Investment dollars continue to leave the Emerging Markets. “Emerging Markets debt-dedicated funds recorded net outflows of $960MM (0.40% AUM) for the week ending on July 3, 2013,” said Morgan Stanley’s Robert Habib citing data from EPFR.

- Protestors continue to take to the streets in Egypt following the military-led removal of democratically elected president Mohamed Morsi. “We declare our unequivocal rejection of the military coup against the elected president and the will of the people and refuse to participate in any action with usurpers of power,” said the Muslim Brotherhood in a statement.

- A 4th of July celebration in southern California went awry when fireworks started going off sideways toward a crowd of viewers. 28 people were reportedly injured.

- American Joey Chestnut ate a record 69 hot dogs in 10 minutes to win the annual Nathan’s Hot Dog Eating Contest. This is Chestnut’s seventh time taking home the title

Read more: http://www.businessinsider.com/opening-bell-july-5-2013-2013-7#ixzz2YAuVvNpe

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair