Stocks & Equities

North American equity markets are in the final stages of their current period of seasonal strength. Short term technical evidence of a top has appeared, but is inconclusive. Preferred strategy is to hold seasonally strong equity positions for now, but start to plan an exit strategy to be triggered on additional technical evidence of a possible downtrend.

Other Issues

A key reversal by the S&P 500 Index and Dow Jones Industrial Average on Friday is a short term bearish technical signal for U.S. equity markets.

First quarter corporate reports start to flow late this week. Initial focus is on the U.S. financial services sector. Consensus shows that year-over-year comparisons for S&P 500 and Dow Jones Industrial companies will be slightly negative. On the other hand, first quarter reports frequently are released during annual meeting that often include good news (increased dividends, stock splits, share buy backs). In addition, many companies are expected to report positive second quarter guidance relative to first quarter, weather weakened results.

Short and intermediate technical indicators remain overbought for most equity markets and sectors.

Economic news this week is expected to be quiet. Focus is on release of the FOMC minutes for the March 19th meeting.

Political focuses this week are on election results from Quebec and Afghanistan.

Seasonal influences for U.S. equity markets and sectors normally are positive during the first half of half of April followed by underperformance in the second half of April

Historically, during U.S. Midterm election years, the S&P 500 Index and Dow Jones Industrial Average reach a significant medium term peak in the second half of April followed by a significant intermediate correction lasting until the beginning of October. Tipoff is the start of mid-term election ads.

Economic News This Week

March Canadian Housing Starts to be released at 8:15 AM EDT on Tuesday are expected to increase to 193,000 from 191,200 in February.

February Wholesale Inventories to be released at 8:30 AM EDT on Wednesday are expected to increase 0.5% versus a gain of 0.6% in January.

Minutes from the FOMC meeting on March 19th are released at 2:00 PM EDT on Wednesday

Weekly Initial Jobless Claims to be released at 8:30 AM EDT on Thursday are expected to slip to 325,000 from 326,000 last week.

March Producer Prices to be released at 8:30 AM EDT on Friday are expected to increase 0.1% versus a decline of 0.1% in February.Excluding food and energy March PPI is expected to decline 0.2% versus a drop of 0.2% in February

April Michigan Sentiment to be released at 9:55 AM EDT on Friday is expected to improve to 81.0% from 80.0.0% in March.

Equity Trends

The S&P 500 Index gained 7.47 points (0.40%) last week despite the 1.25% drop on Friday. Note the negative key reversal on Friday when the Index also touched an all-time high. Intermediate trend remains up. The Index fell below its 20 day moving average on Friday. Short term momentum indicators are overbought and showing early signs of rolling over.

The TSX Composite Index added 132.38 points (0.93%) last week. Intermediate trend remains up (Score: 1.0). The Index recovered back above its 20 day moving average (Score: 1.0). Strength relative to the S&P 500 Index remains neutral (Score: 0.5). Technical score based on the above indicators improved to 2.5 from 1.5 out of 3.0. Short term momentum indicators are overbought and showing early signs of rolling over.

…..more HERE including 45 Charts

It’s no secret to anyone following the Canadian stock market that the TSX Venture exchange has fallen on hard times over the last three years. Comprised largely of speculative, junior resources stocks, the exchange has lost over 55% of its value over this period. Fortunately for the exchange this loss has been somewhat mitigated by the few small cap stocks that are actually producing real earnings and growth. But for the people who have made a habit of buying heavily into the speculative junior resource plays, it would appear that a mere 50% loss (however nauseating this may be) is the least of their worries when liquidity has dried up to the point where they can’t even sell the shares they have (essentially equating to a 100% loss).

It is no secret what KeyStone thinks of revenue-less and profitless, capital-sucking predators. In our view, the junior resource sector in Canada has been fought with what are essentially shell companies, never generating a penny of economic value and existing solely for the purpose of raising capital from unsuspecting investors and then funneling this money into management salaries and corporate expense accounts. With very few exceptions, they have been nothing but capital-destroyers and essentially represent the antithesis of our fundamental, cash flow based investing strategy.

After years of collapsing share prices and deteriorating liquidity, most of these so-called companies are largely losing their ability to raise additional capital with many now sitting on the verge of financial destitution. But in the wake of their darkest hour, a glimpse of light has risen on the horizon…or as the case may be…a puff of smoke. Sweeping regulatory changes with respect to the production and distribution of medical marijuana have taken effect this month. The industry is becoming industrialized and many people smell an opportunity for businesses that can take advantage of the change. This transition has piqued the interest of investors and speculators which has prompted dozens of “resource companies” to issue new releases over the past few months outlining their intentions to investigate the prospects of being reborn into the new marijuana industry.

After years of collapsing share prices and deteriorating liquidity, most of these so-called companies are largely losing their ability to raise additional capital with many now sitting on the verge of financial destitution. But in the wake of their darkest hour, a glimpse of light has risen on the horizon…or as the case may be…a puff of smoke. Sweeping regulatory changes with respect to the production and distribution of medical marijuana have taken effect this month. The industry is becoming industrialized and many people smell an opportunity for businesses that can take advantage of the change. This transition has piqued the interest of investors and speculators which has prompted dozens of “resource companies” to issue new releases over the past few months outlining their intentions to investigate the prospects of being reborn into the new marijuana industry.

Of course almost none of these three dozen or so companies actually have a plan for entering an industry which essentially has little to no similarities to their own. But thankfully for them, in many cases that doesn’t seem to matter. The mere mention of a strategic refocus into medical marijuana has resulted in a significant increase in the share prices for many of these companies. It is completely unknown to us how these companies plan to leverage what experience and expertise they have into this completely new marketplace. But speculation surrounding the new industry has created a new buzzword in the stock market and simply replacing the word “gold” (just for example) with “medical marijuana” in a corporate presentation may be exactly what some of these nearly destitute corporate capital-killers need in order to hit the street for a few quick capital raises.

What we do know about the industry right now is that there are approximately 40,000 individuals that are licenced to use medical marijuana in Canada and this number is expected to grow. Up until now, most of these people were able to grow their supply in their own homes or else contract another individual (who is licensed) to grow it for them. But these rules changed as of April 1st under a federal government initiative to industrialize marijuana grow operations into commercial facilities. Health Canada has so far received thousands of applications for licenses to grow commercial marijuana and (to our knowledge) to date has issued only 12. The number of licenses issued to public “resource-to-marijuana” companies is currently exactly zero. This may be an industry with good long-term potential but currently there are too many unknowns to actually conduct a fundamental analysis. First off, none of the public companies that are planning to be in medical marijuana have generated a dime of profit or revenue. They are unproven at best and many are simply opportunistic (and not in a good way). Government regulations, costs, distribution, and a plethora of other factors are all currently unknowns as well. Plus there is price sensitivity…how much money are these 40,000 patients (many of whom are on disability) able to pay for medical marijuana when many are accustom to growing it themselves. The list of uncertainties goes on. There is currently one single company which recently became public (not a resource convert) that does have a federal license and plans to build out a production facility. But once again, this particular company has yet to produce a dime of revenue to prove out its business model but still somehow commands a market capitalization of almost $100 million.

In spite of all these unknowns, investor interest and the prospects for further speculation appears to be increasing. Over the next several months, we expect to see many more new releases from unsuccessful companies in unrelated industries, announcing their intentions to pursue a medical marijuana focus. Our advice to investors is to be cautious (or in plain English…don’t buy them). Getting wrapped up in the “hype” of a sector or technology, without consideration of the underlying fundamentals, typically proves to be disastrous over time. This becomes especially true when many of the companies have a track record of doing little more than destroying investor capital.

KeyStone’s Latest Reports Section

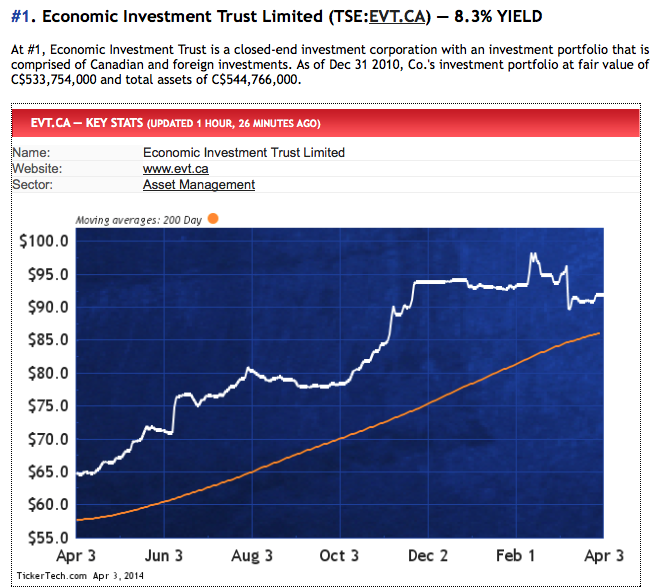

With an 8.3% Yield it is no surprise that this was the top pick of Canada Stock Channel this week. All these stock picks are Canadian listed dividend stocks paying between 3.2% & 8.7%. These companies operate in a variety industries from Oil & Gas & Transportation through to Real Estate & Entertainment. These are stocks for the income minded investor – Editor Money Talks * Note: Click on “Back to slide 9” to see dividend paying Corus Enterainment which broadcasts Michael Campbell’s Money Talks!

With an 8.3% Yield it is no surprise that this was the top pick of Canada Stock Channel this week. All these stock picks are Canadian listed dividend stocks paying between 3.2% & 8.7%. These companies operate in a variety industries from Oil & Gas & Transportation through to Real Estate & Entertainment. These are stocks for the income minded investor – Editor Money Talks * Note: Click on “Back to slide 9” to see dividend paying Corus Enterainment which broadcasts Michael Campbell’s Money Talks!

![]()

Not Yet! Here’s when investors should start worrying about another major correction and & market in stocks. Ironically, says Financial Sense Newshour host Jim Puplava, when things start to get better, not worse – Editor Money TalksIn his recent Big Picture broadcast, “Yelling Yellen and the Change in the Fed’s Direction,” Puplava explains the four primary phases of monetary policy and how they’ve influenced the stock market and economy over the last half century.

In phase 1, the Federal Reserve is transitioning from a low interest rate environment to gradual tightening. This happens as the economy starts to improve and inflation begins to rise. Think 2004 as Greenspan started to raise interest rates in quarter point increments from extremely low levels. In this phase P/E multiples and the bond market begin to peak with the historical mean return on stocks around 10%.

In phase 2, monetary policy is now much more restrictive and well into tightening mode. The economy is doing quite well and inflation is running much higher. Commodity prices begin to climb steadily and profit margins are beginning to get squeezed with rising input costs. Think 2006 and 2007 as interest rates rose to 5%. This is a deadly combo for stocks and the economy, and typically the time when investors should start worrying. (Note: We’re not yet in this phase with low economic growth and inflation.) The historical mean return for stocks in this phase is around 2.5%.

In phase 3, policy is tight, interest rates have peaked and may now be rolling over. The stock market has corrected and the economy is either in or very near recession. Think 2008. In this phase, the historical mean return of stocks is -9%.

In phase 4, monetary policy is loose once again, the economy is in recovery mode, and inflation is running low. This is the best phase for stocks with a mean return around 23%.

So which phase are we in? Given the above, Puplava says the U.S. is near the latter stages of phase 4, with Yellen’s recent remarks of possibly raising rates in 6 months serving as a signal when we transition into phase 1 of the Fed rate raising cycle.

Is it time to be worried then? As you’ve probably heard over and over again, a bull market climbs a wall of worry. Yet, given the ebb and flow of the economy, stock market, and interest rates over the last half century, investors really need to start worrying, ironically, once things are doing much better: the economy is running on all cylinders, inflation is high, and the Fed has been raising interest rates for quite some time. That’s when the bubble bursts.

Right now, Puplava says, we’re just not there yet.

Click here to listen to his recent Big Picture broadcast, “Yelling Yellen and the Change in the Fed’s Direction.”

The Dow rose 74 points yesterday. Gold dropped $3 an ounce.

What do you expect? Yesterday was April Fools’ Day.

This should be a good quarter for stocks, according to economist Richard Duncan. He believes “excess liquidity” – cash and credit in excess of what borrowers and spenders actually need – drives asset prices.

We haven’t been able to connect every tarsal, hallux and tibia of Duncan’s theory. But the skeleton, as he presents it, is serviceable… even attractive. The more excess liquidity, the more people use it to bid up asset prices. As excess liquidity goes down, so do asset prices – particularly stocks.

Duncan expects the coming quarter to produce a record of excess liquidity. The Fed is still pumping liquidity into the market at the rate of $65 billion every month. Meanwhile, it is tax time, so the government’s needs for borrowing will be relatively low. And according to Duncan, the difference between the available liquidity and the need for it in the regular economy has to go somewhere.

But after this quarter, the outlook changes. The Fed is scheduled to wind down QE by the end of the year. And the federal government’s rosy budget scenario will begin to fade – meaning more government borrowing. That means the third quarter is expected to produce only a slightly positive excess of liquidity. And in the fourth quarter, says Duncan, the excess turns into a shortage.

If the Fed persists in its plans to taper QE, in other words, the third quarter will likely see a selloff in the US stock market. This will give the Fed’s forward guidance a kick in the rearward quarters.

Instead of continuing to taper, the Fed will panic. Its entire theory of life… its philosophy… and its sacred religion will be challenged. In its view, credit, prices and stocks must ALWAYS go up.

There was a time when the Fed was merely charged with making sure the value of the nation’s money was stable. It failed miserably. So it was rewarded with more responsibility. Its mission creeped toward making sure the nation had full employment.

At that, too, it fails regularly. So, now it has taken upon itself (Congress never authorized it) to hold interest rates down and push consumer prices up.

Actual consumers prefer lower, not higher, prices. But such is the hubris of central bankers that they are willing to contradict 100 million households. They insist on dollar earners and savers losing about 2% a year of their buying power.

As we have been saying, it is an odd recovery that leaves the average American with less income than he had before it began. But it is an odd recovery that we have.

Stock prices – not to mention prices for antique guitars and gaudy modern “art” – have soared. Incomes, meanwhile, have limped downward. This leaves the typical American feeling richer… but with less money in the bank.

At $81 trillion, total US household wealth has never been higher. But it is supported by precious little household income.

Duncan tells us the ratio of household disposable income to household wealth is important. That’s because wealth must be supported by income… or it disappears.

This is exactly what happened – twice – in the last 15 years. From 1952 until the 1990s, the ratio of household wealth to disposable income was fairly stable – at about 525%. Then it rose above 600% – on two occasions. At the end of the 1990s, before the dot-com crash. And in 2006-07, before the global financial crisis.

Today, once again, the ratio is above 600% – for only the third time in history. And once again, we should be prepared for a crash – or at least a substantial bear market – in US stocks.

That will probably happen in the third or fourth quarter of this year. And it will probably be followed by an announcement by the Fed that, instead of taking QE off the table, it will continue the program.

And instead of allowing short-term rats to rise six months after QE ends, as Janet Yellen suggested in her recent post-FOMC press conference blooper, the target rate will stay at zero for this year… and all of 2015, too.

Duncan believes “QE 4” will produce the same results as QE 1, 2 and 3: It will send stocks flying again. If so, we could be looking at another big run-up in the stock market… after, of course, a substantial decline.

Our advice: Get out of the US stock market now. This market is manipulated, overpriced and dangerous.

Regards,

Bill

P.S. Will has put together a detailed report on the coming central bank-induced crash… and how to protect your savings. To learn more, follow this link.

Two Ways to Protect Yourself

from Modern-Day “Mohawk Indians”

From the desk of Braden Copeland, Editor, Building Wealth

If you saw the latest 60 Minutes bit about Michael Lewis’s new book, Flash Boys: A Wall Street Revolt, you’re probably eager to know how you can avoid being exploited by the nasty trading activity the book exposes.

Here you will find your answer…

Flash Boys goes behind the scenes to reveal certain truths about high-frequency trading (HFT). This is where computers trade billions of dollars in and out of the market at lightning-fast speeds.

Their goal is to scalp money off of investors by taking advantage of inefficiencies in the electronic execution of trades. Think of them as modern-day “Mohawk Indians.”

Lewis’s show-stopping quote at the start of the 60 Minutes segment was, “The stock market’s rigged. The United States stock market, the most iconic market in global capitalism, is rigged.”

Lewis went on to explain how HFT operators are abusing investors. (To see the entire segment, go here. The video will open in a new window so you may close it and easily return here to finish reading.)

In case you have any doubt, I want to tell you Lewis is right. The proof is undeniable. But I also want to tell you this…

If you are an individual investor managing your own account – and making investments with time horizons of months or years instead of seconds and days – this big Lewis reveal does not matter, as long as you:

1. Use “limit orders” when buying and selling

2. Use “stops” based on closing prices and do not enter them in the market

First, let me explain what “limit orders” are. They are orders that include instructions for your trade to be placed only at a certain price or “limit.”

For example, when you want to buy a stock trading for about $20, entering a “limit order” with a limit price of $19.80 will tell your broker not to buy the shares unless they are trading at or below that price.

Entering a “market order” will tell your broker to make the trade at the best market price he can get when he places your trade. It could turn out to be more than you expect (or want) to pay – $20.20, for instance.

Sell limit orders work exactly the same way. The limit price in this case tells the market the minimum price you are willing to accept for your shares.

Placing a simple market order would again put you at the mercy of the market. And that, in turn (although practically guaranteeing your order will be completed) puts you closer to the situation Lewis’s story exposes.

A limit order keeps you in control.

Now, let’s turn to the second rule about “stops.”

Stops are something I discuss in detail in my upcoming special report, “Two Simple Ways to Keep the Wealth You Build.” (You can learn how to find out more about it below.) A stop in this case is a trigger – a price you have set that, should the price of shares fall below it, signals it is time to sell.

To protect yourself from the situation Lewis has outlined, there are two simple parts to the rule about using stops that you need to follow:

1. Only let closing prices trigger your stops. (Don’t let intraday volatility – much of it caused by HFT scalpers – stop you out of your positions.)

2. Don’t enter your stops in the market. (Keep them away from your broker and monitor them yourself.)

Properly managing your stops this way will help you avoid nasty, unexpected surprises. It will keep you in control of your trades. It’s that simple.

If you follow the rules here with your independent investing – use limit orders for buying and selling and make sure to follow both parts of the stop rule – you’re set. Lewis’s revelation about the market’s modern-day “Mohawk Indians” will not be your problem.

Editor‘s Note: To learn more about Braden’s new report, “Two Simple Ways to Keep the Wealth You Build,” you can email him at bwfeedback@bonnerandpartners.com. Include “Two Simple Ways” in the subject. You can also follow him on Facebook atfacebook.com/braden.copeland or Twitter with @BradenCopeland.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair