Personal Finance

»» Strong U.S. earnings continued to prop up a number of equity markets. U.S. stocks outperformed for the week, but Asian indices lagged.

»» China has become a bigger swing factor for earnings results of multinational companies.

»» First-quarter U.S. GDP growth of 2.2% indicates the economy remains locked in a sub-par zone, making dividend investing and stock selection that much more important. (page 2)

»» Global Roundup: Updates from the U.S., Canada, Europe, and Asia. (pages 3-4)

By: Bloomberg

Bill Gross of PIMCO spoke to Bloomberg TV’s Trish Regan this afternoon and said that he is doubtful of another round of quantitative easing in June, but “if we see some weak employment reports over the next two months, then QE3 is back on.” He also said that there’s a risk of a double-dip recession “if liquidity disappears.”

Gross went on to say that “euro land is a dysfunctional family…more dysfunctional than Democrats and Republicans in Washington, DC.”

Courtesy of Bloomberg Television WATCH VIDEO HERE

Gross on whether he’s betting on another round of quantitative easing:

“I don’t at the moment. I am willing to listen and I did listen intently at the press conference and to prior speeches from Janet Yellin and Mr. Dudley in New York. The big three at the Fed I think have moved closer to the middle in terms of the need for additional QE. They in the market are going to wait for the next eight weeks for two key employment Friday reports between now and then, as well as tomorrow’s GDP number, which I think should be judged in my opinion by nominal growth as opposed to real growth. The Fed does not target nominal GDP. They target inflation though. They want lower unemployment, which requires 3% real growth. So the 2 plus the 3 equals a 5% nominal GDP growth target, which the Fed really wants to shoot for. So watch tomorrow’s numbers and don’t be dissuaded by the 2.5% number or the 3% real growth number. It’s the nominal growth number that is key.”

On whether the Federal Reserve will resist an additional round of quantitative easing:

“I think so. The Fed does want unemployment to come down. It has been coming down. As a matter of fact, it’s lower than their prior projections were. There’s little doubt in my mind that a target for unemployment of at least 7% and perhaps lower is what they’re shooting for and that is going to require, 6, 12, 18 months, in my view. It might and probably will require, maybe not on June 30, additional quantitative easing. Quantitative easing is basically writing checks. The Fed’s been writing checks, the ECB has been writing checks, the Bank of England has been writing checks, even the Bank of Japan has been writing checks. This is $2-3-4 trillion worth of check writing that has supported financial markets, but in turn has allowed for employment growth and lower unemployment. I really think that it’s required. I don’t welcome it from the standpoint of the negative consequences, but I think it is required.”

On whether he would rule out QE3 down the road:

To Read More CLICK HERE

Doug Casey, Chairman

(Interviewed by Louis James, Editor, International Speculator)

L: Doug, we’ve had a lot of people write in with questions about Argentina since the government moved to nationalize YPF. First, I have to tell readers that we saw la presidenta going off the deep end some time ago and sold all the Argentina plays in our portfolio. But you live there, have invested there, and are a famous contrarian – so what do you think? Is the market’s understandable reaction to the expropriation overdone, making it time to buy, or would you still stay out of Argentina plays?

Doug: I’d first like to distinguish between living in a country and investing in a country, which are two totally different things. As a general rule, I’d say that right now I have very little interest in investing in companies doing business in Argentina – though I’ve got to say that the Argentine stock market is yielding about six percent in dividends and selling at about eight times earnings. That makes it one of the cheapest markets in the world. It’s been heavily discounted due to corruption, government stupidity, and a generally poor business environment.

L: So is that discount appropriate or overdone? I suspect that Argentine companies are in no danger of being nationalized, so they might be excessively discounted. On the other hand, the folks behind the curtain, pulling the levers on the machinery of the state in Argentina are clearly fools or knaves – I’m not sure any business is safe in Argentina.

Doug: Unfortunately, that’s true. Argentina’s politicians have been just terminally stupid ever since Juan Perón. Even though he was a criminal personality, an overt admirer of Mussolini, and openly sympathetic to Hitler, Perón has become such a cultural icon that you can’t do anything in Argentina today without at least calling yourself a Perónist. It’s rather like in the US, where, if you don’t think that FDR was a hero for getting the US out of the Great Depression, you’re persona non grata. Perón is Argentina’s Roosevelt.

More recently, former president Nestor Kirchner – late husband of Cristina, the current president – was a total disaster. All of his policies were completely wrong-headed and destructive, but he had the good luck to get elected just as the commodities boom got under way, and demand for Argentine agricultural and mineral products soared. That paid for a lot of social spending and made him look like a hero, even though everything he did was the exact opposite of what needed doing.

This is true of Cristina too, but she’s actually outdone her husband in implementing economically suicidal policies. Every single week, her government does something that’s bizarre, counterproductive, or absurd. The most recent and serious blunder, of course, was the nationalization of YPF – but just a few weeks ago, her government tried to ban the importation of books. It wasn’t because they cared what was in the books, it was part of the effort to limit imports in general.

L: I read about that – the excuse was that foreign printers might use ink that could be dangerous. I remember thinking that was crazy, and she does seem to check into hospitals a lot…

Doug: They had to back down on the books. That would have been just too much, to deprive a very literate country of about 85% of books in Spanish and almost 100% of those in other languages. Although it would have been a boon for Kindle – something they probably didn’t even think about. But importing anything to Argentina is a huge hassle these days.

Nationalizing YPF actually make no sense on any basis. She says she did it because the company didn’t invest enough in Argentina – but there’s a reason for that: the current regime has made it very dangerous to conduct any sort of productive business in Argentina. As a result of its policies, Argentina has gone from being self-sufficient in oil and gas – and an exporter – to being an importer. She’s telling everyone that nationalizing YPF will result in more investment in Argentina and hence more production, but that’s a fantasy. Like any national oil company, YPF under its new management is going to be horribly inefficient and riddled with graft and corruption. If they do somehow generate any earnings, they’ll just be wasted by the government on social programs that buy votes but don’t make any lasting improvement in the country.

Of course, YPF started out as a parastatal in the ’20s, so the company has always been a political football. Under Perón it accumulated scores of thousands of unneeded employees. In Argentina they’re called “gnocchis,” after the heavy, doughy, inexpensive pasta that kind of just lies on your plate and does nothing. In fact, Argentines traditionally eat gnocchi on the last day of each month, partly because it’s cheap and money is short at month’s end and partly because it’s a joke about useless government employees. The average guy in Argentina is well aware of how corrupt the system is. It’s why Argentines are always making jokes about themselves – lots of black humor.

On the other hand, there’s an explanation for these actions other than insanity. Rumor in Argentina has it that when Nestor was first elected, the Kirchners had a net worth on the order of ten million dollars. That’s not a lot for a governor…

L: [Chuckles] Yes, what a couple of slowcoaches; any self-respecting Latin-American politician ought to have been able to abscond with at least a hundred million.

Doug: [Laughs] Yes, at least a hundred million. Over his entire term, Carlos Menem is said to have walked away with as much as $15 billion. Why should anyone settle for less?

L: So you’re suggesting that maybe she’s not crazy, but rather a successful political entrepreneur who may yet set a new record at enriching herself at the expense of the people she claims she’s trying to help?

To Read More CLICK HERE

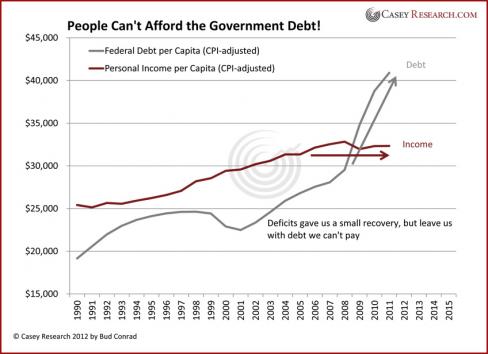

The Social Security Trust Fund (SSTF) 2012 report to Congress is now out (link). It’s 242 pages and contains a great deal of information. I have reviewed a number of sections in the report that I consider to be key measures of SS’s health. Not one of those variables showed any improvement. Some highlights:

-The Net Present Value of the unfunded liabilities at SS is now a staggering $20.5 Trillion. One year ago this was $17.9T ($2.6T increase – 15% YoY). This yardstick grew at more than double the rate of the entire national debt 12/31/10 = $14T, 12/31/11 = $15.2T, total increase = $1.2T).

This deterioration is staring policy makers in the face. The burden that SS will put on future generations is growing exponentially.

+

-The “Drop Dead Date” where the SSTF is exhausted has been moved up three years to 2033. This is a number that the MSM will focus on. It is a bogus deadline. The SSTF must maintain at least one year’s worth of benefits. The year that TF assets will equal one year of payments will be ~2026. This means that anyone who is age 53 today can expect to get 75% of the value that a baby boomer will get. (Under current law, when the TF is exhausted, benefit payments must be cut.)

Fourteen years is not a very long time for people to plan and adjust for what’s coming. The Politicians will have to address this reality sooner versus later. It is already passed the time where it is unfair to those who will be affected.

+

-The Drop Dead Date for the Disability Fund has been changed from 2017 to 2016. This is important as the TF has confirmed that the next President will HAVE to bailout one component of SS. It is crucial to ask the candidates what they will do if elected. They better have an answer. When the debate on the future of Disability Insurance (DI) gets going, it will be marked with a sharp divide of opinions. It could easily be a factor in the election.

To Read More CLICK HERE

By David Galland

Dear Reader,

If history has taught one certain lesson, it is that the less fettered an economy, the better humankind is able to do what it does best: run from trouble and run toward opportunity. In this way mistakes are quickly resolved and progress assured.

Conversely, the deeper the muck of regulation, mandates, taxes, subsidies and other bureaucratic meddling, the slower we humans are in following our natural instincts until the point that progress is slowed or even stopped.

It is said that history doesn’t repeat itself, but it often rhymes. In the current circumstances, it appears that enough time has passed that current generations have completely forgotten the critical connection between the ability of humans to freely pursue their aspirations and economic progress.

You can see this ignorance in the popular demand for even more, not less, meddling in the affairs of humankind. Should this trend continue – and for reasons I will touch on momentarily, I firmly believe it will – then the aspirations of the productive minority will soon be dampened by ever higher taxes and other attempts to “level the playing field” and the global economy, already in tatters, will fall off the edge.

There is no more timely nor acute example of this growing trend than what is currently going on in France. I refer, of course, to the first round of the presidential election process, scheduled for this weekend.

In France, if no candidate attracts no better than 50% of the vote, then the two leading candidates go to a decisive runoff vote, this time around to be held on May 6.

The current president, Nicolas Sarkozy, a conservative in name only, was running at a fairly steady gait toward re-election (thanks to the head start awarded all incumbents), when leading socialist candidate Francois Hollande came out with a proposal to tax anyone with an annual income of over one million euros at a rate of 75%. He also promised to add a tax on all financial transactions and increase taxes on France’s biggest companies to 35% – securing bragging rights as levying the world’s third-highest corporate taxes, the US being #1. This all on top of a 25% VAT, one of the world’s highest. By some calculations, the result of Hollande’s new taxes is that effectively 100% of all incomes over one million euros will now be stripped away by the state.

For good measure, Hollande also promised to reverse the recent modest increase in retirement age from 60 to 62 pushed through by Sarkozy. While I am sure it is mere coincidence, I found it noteworthy that Mssr. Hollande’s campaign slogan is “Change – Now!”

Remarkably, at least for those with some small understanding of economics, as a result of leaning into the microphone with these proposals Hollande has galloped ahead of all other potential contenders and is now projected to finish nose by nose with Sarkozy this weekend.

After which the also-rans will be removed from the race, freeing their supporters to share their affections elsewhere. Given that the leading contender for third place with an estimated 14% of the vote is one Jean-Luc Mélenchon – charitably categorized as “far left”, a label that can be applied to most of the other candidates – it is projected that the “conservative” Mssr. Sarkozy will go down in double-digit flames come May 6.

Bringing to mind the prophetic utterance of Louis XV: “Après moi, le deluge.”

The deluge in Louis’ case manifested as the murderous affair commonly known as the French Revolution. In the case of Mssr. Hollande taking up residence in the Palais de l’Élysée, the deluge is likely to manifest in the form of rising interest rates as investors look to protect against an acceleration in the country’s debt to GDP ratio, already projected to hit almost 90% this year, exacerbated by a flight of capital, investors, entrepreneurs and large businesses.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair