Personal Finance

By Azizonomics

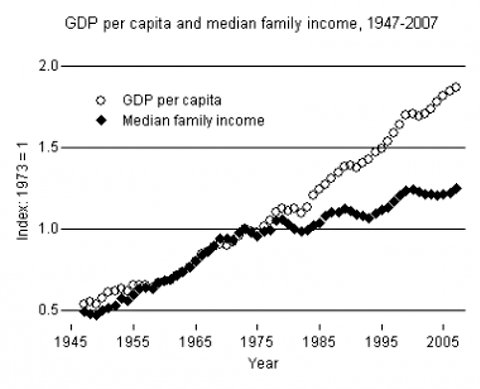

There is a widely-held notion on the political left that the key economic problem that our civilisation faces is income inequality.

To wit:

America emerged from the Great Depression and the Second World War with a much more equal distribution of income than it had in the 1920s; our society became middle-class in a way it hadn’t been before. This new, more equal society persisted for 30 years. But then we began pulling apart, with huge income gains for those with already high incomes. As the Congressional Budget Office has documented, the 1 percent — the group implicitly singled out in the slogan “We are the 99 percent” — saw its real income nearly quadruple between 1979 and 2007, dwarfing the very modest gains of ordinary Americans. Other evidence shows that within the 1 percent, the richest 0.1 percent and the richest 0.01 percent saw even larger gains.

By 2007, America was about as unequal as it had been on the eve of the Great Depression — and sure enough, just after hitting this milestone, we plunged into the worst slump since the Depression. This probably wasn’t a coincidence, although economists are still working on trying to understand the linkages between inequality and vulnerability to economic crisis.

I mostly agree that income inequality is a huge problem, although I believe that it is a symptom of a wider malaise. But income inequality is an important symptom of that wider malaise.

Here’s the key chart:

However it is just as important, perhaps more important to identify the causes of the income inequality.

I have my own pet theory:

The growth in income inequality seems to be largely an outgrowth of giving banks a monopoly over credit creation. In 1971, Richard Nixon severed the link between the dollar and gold, expanding the monopoly on credit creation to a carte blanche to print huge new quantities of dollars and give them to their friends.

Unsurprisingly, this led to a huge growth in the American and global money supplies. This new money was not exactly distributed evenly. A shrinking share has gone to wage labour.

To Read More CLICK HERE

Eric Fry

Derivatives are the “meat and meat by-products” of the financial markets. They look, smell and taste just like regular securities, but almost no one understands why we need them in the first place. After all, what’s wrong with actual meat? Or to re-phrase the question: Is Spam really an advancement over ham?

More importantly, can we trust the derivatives markets? Or might they be toxic? Might they subject the financial markets to devastating side effects?

No one really knows…and since lab rats refuse to eat them, we must assess the risks of derivatives by relying on suppositions, theories and conjecture. Therefore, as a public service, your California editor will offer a few suppositions, theories and conjectures about the rapidly expanding derivatives markets.

The worldwide marketplace of financial derivatives is enormous. No one disputes that fact. But the potential destructive impact of these arcane, opaque securities is very much in dispute.

The apologists for financial derivatives usually say something like, “Sure, the derivatives markets are huge on a gross basis, but relatively small on a net basis.” According to this logic, a bank that purchased $1 trillion worth of Spanish interest rate swaps from one-party, but also sold $1 trillion worth of Spanish interest rate swaps to another party, has zero “net exposure.”

Mathematically, that statement is correct. Realistically, it is a delusion. If the financial markets should hit a pothole or two, that “zero net exposure” has the potential to behave a lot more like the $2 trillion of gross exposure. How could that happen? Very simple. One or more of the parties to these enormous transactions would have to renege on its obligations, thereby triggering a domino effect. Very simple…and not difficult to imagine.

In fact, we’ve already seen the trailer for this horror film. The bankruptcy of Lehman Brothers in 2008 was not only the demise of a prestigious investment bank, it was also the demise of a major counterparty to numerous derivatives contracts. Without Lehman, billions of dollars’ worth of “zero net exposure” suddenly became billions of dollars of plain, old exposure — i.e., unhedged risk.

But that’s when the US Treasury stepped into the path of the falling dominoes with trillions of dollars of newly printed cash and government guarantees. As a result, the dominoes did not merely stop falling, but Wall Street banks were also able to take their fallen dominoes to the Fed and trade them for cash. Pretty nifty, no?

To Read More CLICK HERE

By John Rubino on April 17, 2012

The in-laws own a gas station in Miami that they’ve wanted to sell for years. But they dithered when the market was hot and ended up being stuck with it when interest evaporated in 2009.

Lately, though, the phone has begun to ring again. It’s not exactly a feeding frenzy but real offers are coming from legitimate buyers for the first time in three years.

That’s actually a pretty good description of real estate in general, where low interest rates have convinced a growing number of people that it’s time to buy. See this upbeat story on the home builders:

Pulte, Lennar jump as survey shows housing rebound

NEW YORK (MarketWatch) — Shares of U.S. homebuilders rallied on Wednesday after a Wells Fargo analyst’s research report said data from 20 select markets nationwide are showing strength across the board.

“For the third consecutive month, our survey points to an improvement in orders suggesting 2012 may be the long-awaited recovery year for housing,” the note said.

PulteGroup PHM -1.39% added more than 8%, Lennar Corp. LEN -1.47% gained 5%, D.R. Horton DHI -2.44% rose 4.2% and Toll Bros. TOL -0.86% gained 3.8%.

The bellwether industry ETF, the iShares Dow Jones U.S. Home Construction Index Fund ITB rose 3.4%.

Wells Fargo’s monthly Neighborhood Watch Survey, which tracks 150 sales managers at housing tracts in 20 markets, showed that March results were strong across all measured metrics. In particular, the survey noted that March’s numbers surpassed poll participants’ expectations by the widest margin since the survey started, in 2001.

Wells said that pricing in the 20 markets also improved, both month-to-month and over year-ago figures. Sales managers’ commentary on market activity indicated that buyer confidence seems to be improving as inventory shrinks.

“Sales managers suggested there is a sense of urgency in the marketplace as buyers anticipate higher home prices and/or mortgage rates,” the report said.

Bidding wars are even returning to some markets:

Market squeezing homebuyers

Home shopper Dian Schneider was four houses in on a whirlwind tour of local homes for sale Friday when her real estate agent issued her a warning.

“Now if you like this one you’ll need to move today because there are already two offers on it, and they’re both above list price,” said Anna Hernandez of McKinzie Nielsen Real Estate. “They’re not crazy high, but you’ll have to go in high, too, if you’re serious about it.”

Schneider nodded knowingly as she peeked inside closets, flushed toilets and opened cabinet doors.

The 50-year-old single mom had already missed out on two homes she’d made offers on. She was outbid on one, and pulled out of a second over concerns about its dated electrical system.

“In hindsight, I probably should have taken that one,” Schneider said.

Almost all the available inventory in her price range is badly in need of repairs, and upgrading the electrical on the home she passed up wouldn’t have cost as much as she’d assumed, she later learned. But back then, she didn’t fully appreciate how lucky she’d been to find something.

The Bakersfield area had only 583 single-family homes for sale in March, about a third fewer than in March of last year.

Bidding war return

The result has been fierce bidding wars and almost immediate turnover for anything of quality that’s priced reasonably, whether it’s a modest starter home or a mansion.

“Everybody’s pretty much in the same boat right now, regardless of price,” said Robert Morris, who sells for Watson Realty ERA. “The supply keeps dropping and dropping and there’s nothing replacing it.”

Broker Nancy Harper of Nancy Harper Realty recalled listing a home the day before Easter. By Easter Sunday, it had six offers on it, and when she called the losing agents to tell them their offers had been rejected, two of them burst into tears.

“They told me they’d written something like 14 offers for clients and just couldn’t get one accepted,” Harper said. “When you have agents bursting into tears, boy, that’s low inventory.”

So is the housing bubble back?

To Read More CLICK HERE

Diane Francis at the Financial Post

Conventional wisdom is that this is the market at work. This is not the market at work. This is manipulation of a government system of open-ended mortgage insurance that is poorly supervised.

Nearly three times’ more condo high-rises are being built in Toronto than are being built in New York City and nearly seven times’ more than in Chicago, according to Bloomberg News.

This development boom, and accompanying price increases, is not about housing to meet a sudden surge in population. It is not about an economic boom. If it was, Calgary and Edmonton would have 128 cranes, like Toronto does, building housing and pushing up all prices. Instead, this is taking place in Toronto and Vancouver where economies are moribund.

What is going on here is a deluge of hot money from abroad that is creating an artificial and potentially dangerous real estate bubble

Conventional wisdom is that this is the market at work. This is not the market at work. This is manipulation of a government system of open-ended mortgage insurance that is poorly supervised. What is going on here is a deluge of hot money from abroad that is creating an artificial and potentially dangerous real estate bubble. This mania happened in several other countries — where it was shut down — and has spread to Canada. Officials here have been urging restraint but that is not the solution. A ban on foreign buying of residences is the only solution.

This is what is happening. For example, a modest bungalow in Toronto sold last month for $1,180,800, $400,000 more than the asking price of $759,000. Canadian bidders were furious and deserved to be. The winning bid was made by a university student whose parents have a business in the United States but who live in China. I don’t know if there was a mortgage involved, but student housing — even for foreign students — is now liberally insured by CMHC, in other words, by the Canadian taxpayer.

To Read Full Article CLICK HERE

By Marin Katusa, Casey Research

My most recent trip to Calgary gave me a welcome chance to catch up with friends and colleagues in Cow Town’s oil and gas sector. I found out about new projects, investigated companies of interest, and came away with an improved feel for the current state of affairs – what’s hot, what’s not, and why.

I also came away reminded of one of the dangers that lurk within troubled markets – and today’s markets are troubled. Since mid-March, North America’s exchanges have struggled, with the Dow Jones losing all the momentum that had propelled a spectacular 17% gain over the previous five months while the Toronto Stock Exchange also sputtered and slid, turning downward to lose its slight gains from January and February. Fundamental economic problems remain unresolved in the United States and Europe, while uncertainty grows over China’s ability to control inflation and maintain growth.

The outlook from here is not great. When markets turn bearish, investment strategies often turn toward income stocks, and rightly so: if market malaise is expected to keep share prices in check, dividends become a very good place to look for profits. But whenever a particular characteristic – such as a good dividend yield – becomes desirable, it also becomes dangerous. The sad truth is that scammers and profiteers jump aboard the bandwagon and start making offers that seem too good to refuse.

It was just such an offer that reminded me of this danger. In the question-and-answer period following my talk in Calgary at the Cambridge House Resource Conference, an audience member asked my opinion of a new, private company that was offering a 14.7% monthly dividend yield.

Yes, you read that right: a 14.7% monthly yield, from a new, private, natural gas company.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair