Currency

In the current high-inflation environment, investors are picking value stocks over bitcoin, according to a new survey.

Based on results from 900 investors surveyed by Bloomberg Markets Live, value stocks were ranked as the best inflation hedge with 35% of the vote. Bitcoin, the largest cryptocurrency by market value, garnered a meager 4% of the tally, the data showed, with gold and inflation-linked bonds also far behind the top pick.

Inflation — which is at its highest in 40 years — is running rampant in the US, touching every corner of the economy. Last month, prices consumer rose 7.9% over the last 12 months, according to the US Bureau of Labor Statistics. Gasoline prices, which have risen amid Russia’s war in Ukraine, contributed to most of last month’s increase, the bureau said.

Bloomberg’s survey also found that 73% of respondents said central banks aren’t doing enough to fight inflation. The US Federal Reserve, for its part, began attempting to combat rising prices with an interest-rate hike last week. Even so, investors are still looking for ways to hedge inflation, and to them, value stocks may be the best bet…read more.

The best weekly equity market rally in two years was “setup” by extremely negative sentiment

The Vanguard Total Stock Market ETF (VTI) had its lowest weekly close in nearly a year last Friday – down ~14% from January’s All-Time Highs. In last week’s TD Notes, I wrote: Equity market sentiment is currently very negative. If/when prices turn higher, the rally could be dramatic.

It was.

Extreme negative sentiment persisted early this week. The major stock indices fell on Monday, but sentiment reversed in the Monday overnight session, and the indices began to surge higher. DJIA futures rallied >2,000 points from the Monday overnight lows to Friday’s close. All of the leading American Indices closed Friday at their best levels in over a month, the Dow Jones Transportation index had its best weekly close in four months, and the (commodity heavy) Toronto Stock Index closed at All-Time Highs.

The DJIA, S+P and VTI indices have recovered ~50% of their declines from ATH; the NAZ has recovered <38%. (The different recovery levels hint at the “rotation” since November.)

Extreme commodity market sentiment also “set up” dramatic price reversals

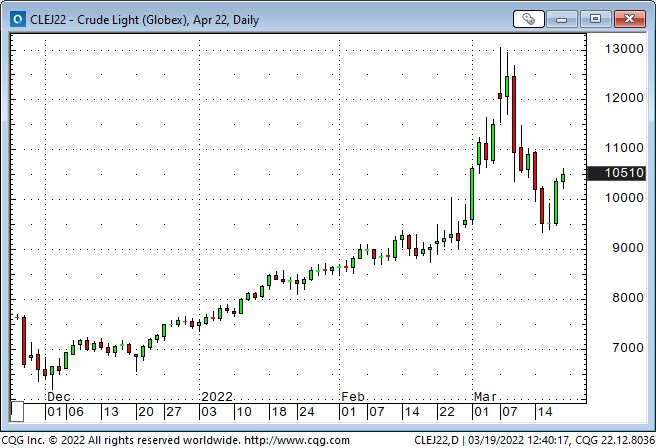

WTI crude oil futures and the broad commodity indices surged to 14-year highs last week; Chicago wheat and New York copper surged to All-Time Highs. The concern was “supply shortages,” but uncertainty, poor liquidity and volatility created fears of existential systemic risk – a grand Minsky moment – when over-levered “Big Shorts” might trigger this market’s version of a Lehman failure.

The peak in the commodity surge was in sync with the “Nickel” publicity, and markets reversed sharply after that.

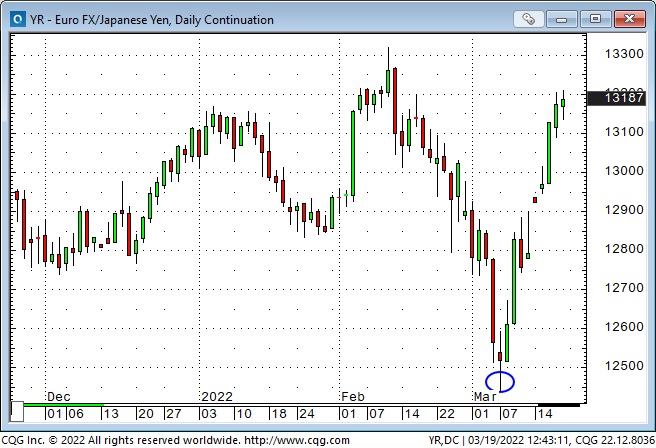

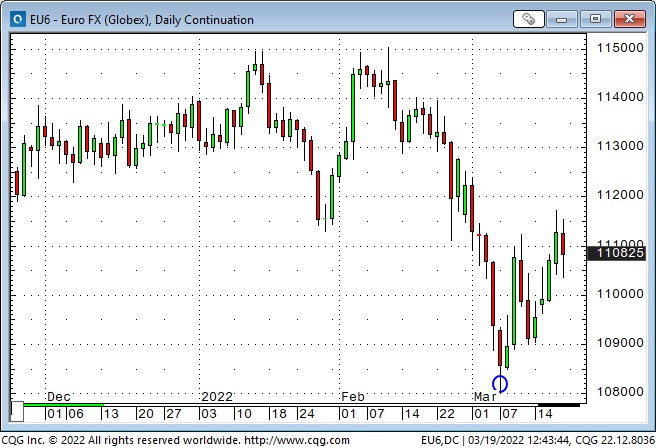

Currency markets also had dramatic sentiment-driven reversals

The US Dollar Index hit a 22-month high last week, but the real “action” was in Euro spreads. The Euro plunged against the Yen, the Swiss Franc, the British Pound and the USD in February / early March, but reversed higher against all currencies on March 7th.

The Euro Vs the USD:

The Japanese Yen fell to a 6-year low against the USD this week. The prospect of rising US interest rates while Japanese rates stay flat and the possibility of soaring commodity prices apparently paints a dim future for the Yen, and speculators are (not unexpectedly) hugely net short. What could possibly cause the Yen to rally?

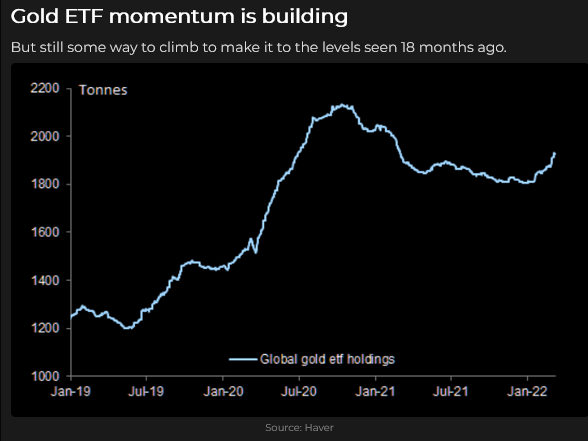

Gold spiked and fell back

Comex gold futures spiked to new All-Time Highs on March 8th but were nearly $100 lower within 24 hours. This week, gold briefly traded $185 below last week’s highs.

Gold ETF holdings have risen ~192 tonnes YTD, after falling ~ 287 tonnes in 2021. In 2020 gold ETF holdings increased ~ 751 tonnes.

Interest rates had a different kind of reversal

Interest rate futures rallied briefly around the beginning of March (maybe the Fed would “back off” from raising rates because of the war), but expectations reversed from those levels as the war seemed to be increasing inflationary pressures. Short rates have been rising faster than long rates, creating “inverted yield curves,” which may foreshadow a recession.

The Fed has been following, not leading the market.

My short term trading

I started this week flat, but I was looking for a bounce from last week’s extremely negative sentiment. I made ten trades, beginning Sunday afternoon, buying S+P, Dow and Euro futures. Three of the trades lost money; seven produced gains. I was trading small size with tight stops. I covered my last position on Thursday’s close and stayed flat into the weekend. My P+L was up ~1% on the week.

On my radar

“What are we trading?” is an existential question. Uncertainty, volatility and thin liquidity make it challenging to define/quantify risk. Headline risk is relentless. The possibility/inevitability of another “Nickel” debacle is ever-present. Inter-market correlations continue to shift. Broken supply chains are likely to sustain high inflation, while political risks limit arbitrage that could dampen price spikes and volatility. It’s a Brave New World.

Sentiment drives prices. Extreme sentiment = extreme price action = a set up for extreme price reversals.

This week, the 2,000 point rally in the Dow may have been the beginning of a charge to new All-Time Highs, or it may have been a classic bear market rally. I don’t know, but I’m leaning towards a bear market rally.

I’ll be looking for opportunities to trade price action rather than “hunches” about what “should” happen.

Thoughts on trading

In the January 29th Notes, in the Quotes from the notebook section, I quoted Bruce Kovner from the 1989 edition of The Market Wizards:

“What I’m really looking for is a consensus that the market is not confirming.”

I keep that in mind when I see “retail” rush into some part of the market. The late 1990s Dot-Com boom and the subsequent crash was a classic, but so was the rush in cannabis, ESG, work-from-home, and lately, commodities – except that commodities haven’t crashed yet – and they may not crash, but the bullish “narrative” has been robust. If the bounce-back following the correction from the March 8th highs rolls over, I’ll look for opportunities to fade bullish commodity enthusiasm.

Quotes from the notebook

“The best traders have evolved to the point where they believe without a shred of doubt or internal conflict that “anything can happen.” Mark Douglas, Trading in the Zone, 2000

My comment: I used to have a Post-it note taped to one of my screens that said, “Anything Can Happen.” I had never heard of Mark Douglas when I taped the note to my screen, but I kept it there after reading his book.

I once had a senior lawyer from a big law firm interview me to do some trading for his client. Years later, he told me that he decided to recommend me to his client when he saw that Post-it on my screen!

“The trader’s job is to imagine the future different than what it is now – find a trade that will profit from that change, and manage the risk of that trade.” Ben Melkman, RTV, 2017

My comment: I agree 100%.

The Barney report

It’s hard to pay attention to my screens when Barney wants to play – so I take him for a long walk, which keeps me from getting too wired, and when we return home, he falls asleep at my feet, and I can get some work done!

Chicago dyes the Chicago River Green on St. Patrick’s Day! I’ve seen it and I love it!

A Request

If you like reading the Trading Desk Notes, please forward a copy or a link to a friend. Also, I genuinely welcome your comments, and please let me know if you would like to see something new in the TD Notes.

Listen to Victor talk markets

I’ve had a regular weekly spot on Mike Campbell’s extremely popular Moneytalks show for 20 years. The March 19th podcast is available at: https://mikesmoneytalks.ca. Mike’s closing editorial – he calls it his “Goofy” – is a scathing review of the Government’s hypocrisy around the freezing of bank accounts near the end of the Trucker’s Convoy protest.

This week I also did a 30-minute interview with Jim Goddard on Howe Street Radio. We talked about the wild market action, my trading, and what I think may happen next in different markets. The Youtube link is:

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.

There was little expectation going into 2022 that B.C. would be able to maintain last year’s surge of economic growth following in the wake of initial pandemic paralysis.

But the province now appears to have become a “victim of its own success,” according to TD economists who forecast growth will fall a full point to 3.8 per cent in 2022 compared with a year earlier.

“A strong recovery from the pandemic has fuelled intense labour shortages. This challenge is likely to keep the province from achieving even stronger growth this year,” Friday’s report stated.

Earlier this month the Bank of Canada hiked its overnight rate for the first time since 2018 – a vote of confidence for the strength of the economy as well as an effort to tamp down on record inflation.

Central banks across the globe slashed rates to record lows in the wake of the pandemic to inject cheap capital into the economy and keep investment flowing. But that flood of capital, coupled with unprecedented supply chain disruptions, helped drive Canada’s annual rate of inflation to 5.7 per cent as of February – a level not seen since August 1991…read more.

Rising prices: Canada’s inflation rate hit a new three-decade high in February, adding pressure on the Bank of Canada to raise rates, the Globe reports.

The Consumer Price Index (CPI) rose 5.7 per cent in February from a year earlier, up from 5.1 per cent in January, Statistics Canada said Wednesday. That was the highest inflation rate since August, 1991, and it marked the 11th consecutive month that inflation has surpassed the Bank of Canada’s target range of 1 per cent to 3 per cent. Households are feeling the pinch on several fronts. Shelter costs rose 6.6 per cent for the largest annual increase since 1983. Groceries rose 7.4 per cent, the most since 2009. And gas prices jumped 6.9 per cent in a single month. The average of the central bank’s core measures of inflation – which strip out volatile components and give a better sense of underlying price pressures – rose to 3.5 per cent, also the highest since 1991.

Hungrier: In the Star, Heather Scoffield observes that food prices, which have already gone up, will also be affected by the war in Ukraine.

The Russian invasion of Ukraine, which not only throws Ukrainian farming into question but also has meant the closure of key shipping routes from the region, compounds the trouble — with devastating effects for food security in developing countries writ large, and among low-income populations around the world. “The end game is, a lot of people are going to be hungrier,” says agri-food consultant Ted Bilyea, a former executive at Maple Leaf Foods Inc…read more.

Each week Josef Schachter gives you his insights into global events, price forecasts and the fundamentals of the energy sector. Josef offers a twice monthly Black Gold newsletter covering the general energy market and 30 energy, energy service and pipeline & infrastructure companies with regular updates. We also hold quarterly webinars and provide Action BUY and SELL Alerts for paid subscribers. Learn more.

Russia/Ukraine War Update:

Diplomatic talks to create an extended ceasefire are being worked on by delegations of Ukrainians and Russians. The talks to open safe routes for refugees to exit war-torn cities are making progress and some routes have opened. It appears that over 3M Ukrainians have reached safety in NATO countries and the largest exit route appears to be through Lviv to Poland (50% of total refugees). Massive global humanitarian aid is assisting this migration, the largest since WWII.

Just yesterday President Zelensky made what could be a critical concession to end the invasion. He stated that they would be willing to not enter the EU or NATO if they got security guarantees from its neighbors (who are members of NATO). Negotiating this may take some time and what is included in the guarantees may not be amenable to Russia. In the meantime the Russian invasion is being more destructive. Tsar Putin is planning to add to his invasion force with experienced fighters from Syria and Chechnya. The numbers range from 16,000 to 40,000 fighters. These are fighters who fought in urban environments and Putin would need them for the takeover of Kyiv and Odessa, if that is still his plan.

President Zelensky continued his diplomatic offensive and spoke to Canada’s parliament yesterday and to the US Congress today. He is thankful for all the military and humanitarian assistance given so far but continues to push for the countrywide no-fly zone. This is a non-starter for many NATO countries with the US and Germany the most vociferously against the proposal. They see a direct confrontation with Russia leading to a broader European or even world war. A proposal for a non-fly zone for the refugee exit routes might get some traction.

If Putin does not accept Zelensky’s Austria-like option of an independent state then the war is likely to enter a more vicious and deadly phase in the coming weeks. Once Putin’s additional fighters enter the Ukrainian arena we may see an escalation of pressure on the unconquered cities. Russia’s willingness to attack bases in western Ukraine and calling aid convoys from the west as legitimate targets shows where his focus is heading. If he cuts off food and munitions aid to Kyiv then the war from his perspective could be won in just a few more weeks. The failure to make faster progress in taking over the country is impacting Putin’s diatribes. He seems to be losing his cool in interviews. That is why the EU is worried he will use his foreign fighters to rubblize the cities not captured and may use WMDs including thermobaric bombs and chemical or biological weapons. If a diplomatic solution is not seen in the coming days then the risk of the war escalating becomes more likely.

Interestingly business continues. Russia increased exports of natural gas this month to its EU buyers as pipeline sales are not disrupted by the sanctions. Exports rose by 30% over February and this has pulled European spot prices down to US$40/mmBtu.

EIA Weekly Oil Data: The EIA data of Wednesday March 16th was moderately bearish for domestic energy prices. US Commercial Crude Stocks rose 4.3Mb to 415.9Mb versus the forecast of a decline of 1.38Mb. It could have grown by 3.6Mb more if not for Exports rising by 514Kb/d last week. Motor Gasoline Inventories fell 3.6Mb while Distillate Fuel Oil Inventories rose 0.3Mb as heating oil needs slows down with the warmer weather. Refinery Utilization rose 1.1 points to 90.4% as refiners work to add more product to offset the cut-off of Russian products. US Crude Production remained steady at 11.6Mb.

Total Demand fell 558Kb/d to 20.65Mb/d as Distillate Demand fell 883Kb/d to 3.71Mb/d as winter demand peaked. Other Oils consumption fell 311Kb/d to 4.62Mb/d. Motor Gasoline usage fell a modest 19Kb/d to 8.94Mb/d. Jet Fuel Consumption rose 93Kb/d to 1.45Mb/d. Cushing Crude Inventories are now rebuilding and rose 1.8Mb last week to 24.0Mb.

OPEC February Monthly: On March 15th OPEC released their March 2022 Monthly Forecast Report (February data). It now appears that OPEC is reacting to moral suasion from its customers and has added more supply. While in January they added only 64Kb/d, in February they added 440Kb/d to reach 28.5Mb/d. However this still remains below the 29.4Mb/d produced in December 2019 before the pandemic hit. So they still have nearly 900Kb/d to bring on just to get back to pre-pandemic levels. Saudi Arabia and the UAE alone could add 2.5Mb/d if they wanted to.

The increases came from Saudi Arabia at 141Kb/d, followed by Libya at 105Kb/d (as supply disruptions ended) by Iran at 44Kb/d an additional 36Kb/d by Iraq, Kuwait increasing by 32Kb/d and the UAE an additional 26Kb/d. Venezuela saw a rise of 21Kb/d to 680Kb/d as they got sufficient diluent this month from Iran, China and Russia. OPEC sees 2022 consumption at 100.8Mb/d, up 4.15Mb/d from the 96.63Mb/d consumed in 2021.

OPEC has now started to be concerned about world economic health and sees some risk in its forecast of demand growth this year of 4.1Mb/d to a 100.9Mb/d average. If a global recession hits this year there may be no growth in demand and that is what concerns us.

EIA Weekly Natural Gas Data: Weekly winter withdrawals continue but at a much slower pace as winter nears its end. Last week’s data showed a withdrawal of 124 Bcf, lowering storage to 1.519 Tcf. The biggest US draws were in the East (41 Bcf) Midwest (40 Bcf), and in South Central (38 Bcf).

The five-year average for last week was a withdrawal of 38 Bcf and in 2021 was 52 Bcf due to the warming weather and the end of winter consumption at the end of this month. April starts the new injection season. Storage is now 16.0% below the five-year average of 1,809 Tcf. Today NYMEX is US$4.70/mcf due to milder weather. AECO is trading at $4.56/mcf. After winter is over natural gas prices typically retreat and as the general stock market continues to decline, a great buying window should develop at much lower levels for natural gas stocks in Q3/22.

Baker Hughes Rig Data: The data for the week ending March 11th showed the US rig count rose 13 rigs to 663 rigs (unchanged last week). Of the total rigs working last week, 527 were drilling for oil and the rest were focused on natural gas activity. The overall US rig count is up 65% from 402 rigs working a year ago. The US oil rig count is up 71% from 309 rigs last year at this time. The natural gas rig count is up a more modest 47% from last year’s 92 rigs, now at 135 rigs. Texas added 12 rigs last week with six of those rigs added to the Permian fleet which now has 316 rigs, up 49% from last year’s 212 rigs.

Spring break-up and road bans have returned to Canada. Last week 11 more rigs were removed from activity (down seven rigs last week) to 206 rigs. The rig count level will continue to fall over the next few weeks. Only rigs staying on location drilling pad wells will be active shortly. Canadian activity however is still up 78% from 116 rigs last year as more activity moves to pad drilling. There was a seven rig decrease for oil rigs and the count is now 127 oil rigs working. However this is up from 58 working at this time last year. There are 79 rigs (down three on the week) working on natural gas projects now, but still up from 58 rigs working last year. Staffing of rigs in Canada is a problem and adding significantly more rigs this summer may be problematic. While rig and frack day rates are rising, so are costs and therefore margin improvements are not what one should expect as the industry activity picks up. Service industry margins need to rise materially in 2H/22 if drilling and completion activity is to rise.

The overall increase in rig activity from a year ago in both the US and Canada should translate into rising liquids and natural gas volumes over the coming months. The data from many companies’ plans for 2022 support this rising production profile expectation. We expect to see US crude oil production reaching 12.0Mb/d in the coming months. Companies are taking advantage of attractive drilling and completion costs and want to lock up experienced rigs, frack units and their crews as staffing issues are difficult for the sector. The EIA forecasts US production reaching 12.5Mb/d before the end of this year. From a focus on paying down debt and then increasing shareholder returns we see companies adding growth to their 2H/22 plans as national and continental energy security of supply concerns change the focus of Board directed spending plans.

Conclusion:

Bullish pressure on crude prices:

- Russia’s invasion of Ukraine and the severe destruction of the country has rallied European nations against Russia. Even though imports into Europe of crude oil and natural gas are allowed, oil tanker companies are finding getting insurance difficult and have abandoned this business. Now only tankers owned by Russia, India and China handle the trade that can be done. It appears that 2.0-2.5Mb of Russian crude is finding buyers but 2Mb/d+ is not finding buyers even at US$20-25/b discounts.

- Exports have problems from insurance to lack of shipping by the buyers and the lengthy time it takes to get Urals oil from western Russia to the buyers countries. Travel time may be five times longer. India is now contemplating paying for Russian crude in Rupees or Rubles.

- Saudi Arabia, UAE and Kuwait have not responded positively to President Biden’s pressure to increase production by 2-3Mb/d immediately. In the case of the Crown Prince of Saudi Arabia, Biden will not even talk to him (just to his father) as he calls him a ‘pariah’ for the murder of his citizens and his flawed war in Yemen.

- EU countries and the US have not gone on a war footing to replace Russian crude oil supplies. President Biden has not made one speech asking the US oil industry to focus on adding as many new oil barrels as possible, and as quickly as possible. He remains in his climate focused bunker even though the industry would respond to a patriotic call to action. Canada’s capability to increase crude exports is being ignored as a policy choice, as the Biden administration continues talks with Iran and now has started dialogue with Venezuela. It seems buying oil from despotic murdering thugs is more palatable to Biden for US consumers, than buying from us.

Bearish pressure on crude prices:

- Covid is picking up around the world and lockdowns are restarting. China is seeing the most lockdowns with 60M people from the eastern cities of Shanghai, Shenzhen, Hong Kong etc, are under lockdown and their economies are non-functional. Demand for energy in the country of 14.5Mb/d (2021 data) could decline by 1.5-2.0Mb/d during the lockdowns. Europe is also seeing rising caseloads. The biggest increases seem to be occurring in Asia with South Korea adding 283K new cases and Vietnam with 210K. World death rates now exceed 6.046M of which 965K are US deaths. A new variant has been discovered in Israel which has the highest vaccination rate in the world.

- The Iran nuclear negotiations are working towards sealing a deal and having sanctions removed so that they can sell their oil around the world. President Biden may be giving away more concessions to Iran in order to have sanctioned Iranian oil available. One complication in finalizing the deal is that Russia wants its trade with Iran allowed going forward or they will not acquiesce to it. If a deal is concluded and Iran receives sanction relief, they could increase production by 1.3-1.5Mb/d quite quickly. Iran also has over 100Mb in floating storage around the world near its buyers and another 100Mb ready to sell.

- Venezuela appreciates the olive branch offered by the US and released two imprisoned Americans after their initial talks with US officials. Will this be a thaw in the relationship? Will the US just give them sanction relief but not require a unity government formed? It looks like barrels may win. Venezuela could increase production by over 2Mb/d (from 680Kb/d in February) but how quickly is not known due to the poor maintenance of their fields and infrastructure.

- The US and allies are releasing 60Mb of crude from their strategic reserves to meet short term needs. The US will supply 30Mb of the volumes in April and May to meet near term needs.

- The likelihood of a worldwide recession is rising. The high cost of energy is lowering consumers and industry’s capacity to handle the cost pressures. Many businesses are closing or limiting their hours in Europe. Food costs are exploding! Russia and Ukraine produce one-third of global wheat and barley production. Ukraine provides European livestock farmers with corn and other grain additives. None of this is being shipped now from the Black Sea ports. Nickel prices have exploded to the upside (doubled to US$100,000/ton) and the London Metal Exchange (LME) suspended trading and canceled trades as producers who presold production got margin calls that they couldn’t meet. This exchange remains closed. This may be a multi-billion dollar disaster and could be the ‘Lehman event’ of this financial and military crisis.

- Inflation is now exceeding 10% in the US and around the world (Italy the worst hit with PPI up 32.9% in January 2022) and will box Central Banks in. Do they fight inflation by raising rates and lowering liquidity or do they provide accommodation during this war event. In either case the world faces a moderate or possibly a severe recession once hostilities end.

- US Retail Sales out today were terrible. Ex-Gas/Auto’s, they fell by 0.4% (prior month +5.2%) and this is before knowing that consumer prices rose 0.8% in the month. Consumption is likely to decline in the coming months as the burden of higher food, energy and housing costs rise and leave less spending for other items. The likelihood of a recession in the US in the coming months now exceeds 50%.

CONCLUSION:

The invasion of Ukraine has spiked up crude prices. We expect that higher energy costs will knock down crude demand by 4-5Mb/d later this year resulting in a global recession. When global recessions unfold, crude prices plunge sharply. One bank energy forecaster predicted today that we may see Brent exceed US$200/b in the coming weeks as the next painful phase of the war is initiated by Russia, but will fall rapidly to US$50/b once recession takes over. In 2008-2009 during the financial crisis demand fell by over 5Mb/d (from over 88Mb/d to 83Mb/d). The price of crude fell from US$147.27/b to US$33.55/b in eight months. During Iraq’s invasion of Kuwait prices rocketed from US$16.16/b in July 1990 to a high of US$41.15/b in October and then plunged in four months to US$17.45/b as recessionary demand destruction occurred. WTI today is at US96.49/b.

Energy Stock Market: The stock markets around the world are gyrating with large daily price moves. Today the upside is 380 points (as the market awaits the Federal Reserve rate increase and the more important hawkish or dovish commentary). The S&P/TSX Energy Index has retreated 11 points over the last week to the 205 level (down 25 points from the 2022 high of 230) due to the recent pullback in crude oil prices.

Our March Interim SER Report comes out tomorrow Thursday March 17th. It will include a detailed review of the economic impact and likely difficult recession the world will be facing in the coming months. Previous recessions, after parabolic energy and other commodity inflationary price spikes, have been severe and stock markets have been crushed. The current market declines are just the tip of the iceberg. Downside for the Dow Jones Industrials is the 24,000-25,000 during Q3/22 (today 33,900 – down from the high at the start of this year of 36,953). We expect violent market swings in the coming weeks with over 1,000 point down and up days for the Dow Jones Industrials as it works its way through this inflation and war-induced bear market.

In our Interim report we go over in detail the financial and operating results of 13 companies that have reported. The financial results have been fabulous given the war premium in commodity prices. Our models have this windfall cash flow removed from Q3/22 data onward. Stocks are trading at or close to our one-year targets so the upside is limited.

If you want access to this encompassing and timely market update report and to know which energy sector stocks provide the most attractive returns (when the energy Bull Market re-commences) then become a subscriber. Go to https://bit.ly/3jjCPgH to subscribe.

Please feel free to forward our weekly ‘Eye on Energy’ to friends and colleagues. We always welcome new subscribers to our complimentary energy overview newsletter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair