Timing & trends

Get-rich-quick investment advice is a fantasy. Get-rich-slow is a validated strategy for real wealth.

Today, it is more important than ever to keep the long-run perspective firmly in mind…

Lest you’ve forgotten, world financial markets are in a state of unparalleled disorder. More capital has been drained from markets, thanks to the irresponsibility of politicians and the acquiescence of naive citizens, than at any time in modern history. The damage done by bombers and tanks in world wars has been matched by the unintended consequences of central planning and bureaucracies.

Fortunately, however, the political and philosophical trend lines are all pointing to true long-term reform. The pendulum’s swing cannot be stopped, and the coming decades will be unmatched in terms of technological progress and wealth creation.

This is exactly the time to be investing in the future. Metaphorically, and sometimes actually, there is blood in the streets. You’ve probably heard that Baron Rothschild, the famously successful 18th-century British investor, said, “The time to buy is when there’s blood in the streets.” In fact, some believe the original quote was, “Buy when there’s blood in the street, even if the blood is your own.”

Remember, investors who bought and held a diversified portfolio of disruptive technologies before and during the Great Depression got rich. Those who lost confidence because they weren’t seeing the quarterly gains typical in bull markets missed their golden opportunity to “buy low.”

This, I repeat, is a chance of historic magnitude to buy the companies that are going to change the world and power the recovery — like the one I am going to tell you about today.

One company has accomplished a major milestone: The demonstration that the company can produce purified cell populations…

As I’ve explained in discussions about other stem cell companies, the ability to produce pure cell populations is critical. The FDA is extremely concerned that the introduction of unpurified stem cells might cause inappropriate cell growths, or even cancers. Geron’s nonpurified stem cell lines did, in fact, produce microcysts in early tests.

For liver or any other stem cell therapy, therefore, it is critical that the cells used in a therapy are only the type needed for that therapy.

While I had little doubt that this company would solve this problem, I had no idea what the solution would be.

I spoke to the leading researcher who helped me understand this breakthrough technology. Essentially, this company has discovered how to replicate a feature of early embryonic development that begins the process of cell differentiation. Known as the “primitive streak,” it is the initial division of undifferentiated embryonic cells into “bilateral symmetry.” Some bioethicists, in fact, consider this event the “ensoulment” or beginning of life.

Regardless, the primitive streak has unique characteristics that provoke very specific movement of cells within the embryo. The important thing to know is that this company has created artificial primitive streaks. Therefore, they can provoke purified cells to migrate into purified cell populations.

This company also enrolled the first US-based donor in its program to establish the clinical-grade human parthenogenic stem cells capable of immune-matching most humans.

It has already gone through the rigorous bureaucratic and regulatory process to assure that the cells created by these donor cells are acceptable to the FDA.

Regulatory approvals were obtained from the Institutional Review Board (IRB) and the Stem Cell Research Oversight (SCRO) Committee. Cell lines have already been collected offshore, but the American side is critical to the company’s road map.

Highly purified stem cells are not just effective replacement cells; they are young. People who use these cells for therapies will have organs and tissues with life spans that will extend for as much as a hundred years or more.

This will change the nature of medicine as we know it…

It’s the future of biotech. And I believe this amazing technology could eventually improve… and extend… every life of every person on earth…

Regards,

Patrick Cox,

for The Daily Reckoning

Joel’s Note: We’re always eager to learn where Patrick’s latest investigation has taken him. Though we admit an impressive ignorance in the field of disruptive technologies ourselves, Patrick has amassed a rather impressive track record for both identifying and capitalizing on opportunities in this realm for readers of his Breakthrough Technology Alert.

In his most recent report — which just hit the virtual shelves this past weekend — Patrick claims he’s identified the “Last Stock You’ll Ever Need.”

That’s a big claim, you’ll surely agree.

Naturally, we’re skeptical…a trait our vocation and various avocations demand. That said, Patrick’s report is a fantastically, characteristically intriguing write up…even if you do decide to buy a stock or two after this one. Check it out here.

In my market comments last year I frequently referred to the KEY turn dates of May 2 and Oct 4…when the directional trends of a number of important markets changed. For instance, the S+P 500 and Crude Oil both made important highs on May 2 (and the US Dollar made an important low) while on Oct 4 the S+P 500 and Crude Oil both made important lows (and the US Dollar made an interim high.)

Last year, as markets approached the KEY HIGH turn date of May 2, 2011, bullish enthusiasm was very strong across asset classes….silver was charging to $50 an ounce and the VIX traded down to a 4 year low…the COT data indicated that speculators were very aggressive buyers. I was anticipating that the (bear market) rally from the March 2009 lows was reaching a crescendo…but I was waiting for a confirmation that a top had been made.

May 2, 2011 turned out to be a significant high in a number of markets and prices declined into late June. There was a “bounce back” rally into July (which took a few markets like AUD, CAD, Copper to marginal new highs) but then most asset prices (except for gold) fell sharply through the August/September period into the KEY Oct 4 lows. During that break the VIX rose sharply and by Oct 4 it hit 46%…three times what it had been at the May 2 highs…a great indicator of a bearish extreme. Since the Oct 4 lows in stocks and commodities the VIX has tumbled to 17% this Friday….its lowest level since July of last year….as rising asset prices have dampened the market’s anxiety.

Over the past several weeks asset markets have “wanted” to go higher…a “risk on” environment….especially since the Euro joined the party and turned higher in mid-January.

This Friday the DJI registered its highest weekly close since May 2008 while the Nasdaq index closed at its best levels since December 2000. The S+P 500 and other broad indices of American stocks are still below the highs they made last year, as are the major European, Canadian and global stock market indices….however, nearly all of the major stock market indices around the world (Shanghai is a notable exception) have been trending higher since their KEY Oct 4 lows. Once again I am anticipating that the asset rally is reaching an extreme and will soon make an important turn lower.

For the past several weeks I have been “cautiously” participating in the “risk on” asset rally in my short term trading accounts. From time to time I have taken long positions in the S+P 500 and the CAD futures markets, not on a “buy and hold” basis, but on a “short term trading” basis. I have been cautious because I have been concerned that the rally was “running on fumes” and that there was a real risk of a significant downturn. At the end of last week I had closed out my long CAD futures position and I started this week flat in my trading accounts…anticipating a possible downside break in asset markets, but waiting for confirmation that a break was actually happening before establishing short positions.

Asset prices started this week on a soft tone but there was no real confirmation that the rally was over and a break was developing. I waited. By mid-week the “risk on” tone was re-established and markets went bid. On Friday the US employment data was interpreted as bullish and European and North American stock markets staged a strong rally. The Euro currency traded sideways for most of the week (Euro peripheral bond yields fell and the index of European bank share prices rose to a 6 month high as the market wants to believe that the European debt problems have been “stabilized”) while the commodity currencies all traded higher. The CAD closed the week at a 3 month high Vs. the USD, while the AUD closed the week at a 15 year high relative to the CAD (I see this as an indicator that bullish enthusiasm is getting overdone.) Gold had rallied $225 from late December to mid-week but seemed to run into resistance around $1750 and dropped $32 on Friday as European debt worries faded and the (apparently) strengthening US economy caused a sharp break in bond prices.

In my short-term trading accounts I took a “one unit” short position in the CAD Vs the USD on Friday’s close on the view that the “run for the roses” in asset prices this week was overdone. This is clearly an opinion-driven counter-trend trade and I won’t keep it if the risk markets continue higher.

The fact that the DJI closed this week above its KEY May 2, 2011 highs (at its highest level in nearly 4 years) may be an early warning sign that we are seeing a sea-change in the entire structure of the markets. If the much broader S+P 500 index trades above last year’s May 2 highs then I will have to re-think some of my “Big Picture” market views….which have been that the rally in stocks and commodities from the March 2009 lows to the May 2011 highs was actually a bear market rally…that the decline into the Oct 4 lows was only the first leg of the resumption of the secular bear trend…that the US Dollar ended a multi-year bear market in July of 2008 and made a KEY “higher low” on May 2, 2011…..and will be trending higher for a number of years….that yields on US Bonds are near a secular low and will be trending higher….and that the $1900 August high in gold was a key high and much lower prices lie ahead.

As a trader I always have “Big Picture” market views….which frequently need to be changed as market conditions change! I often trade against my “Big Picture” views in my short-term trading accounts, as I have with long positions in CAD and the S+P futures over the past several weeks…and these are always cautious positions….but I’m happiest, and more aggressive, when my short-term trading positions are aligned with my “Big Picture” views….and the markets are giving me evidence that I’m right! Bottom line….I’m currently anticipating that asset prices are about to take a significant break…if I see a confirmation of that I will be establishing futures/options positions to profit from falling stocks and commodities….however, if the cash S+P 500 (currently around 1345) trades up through last year’s May 2 highs (1370) I will have to re-think my “Big Picture” views and how I want to trade.

About Victor Adair

Victor is a Senior Vice President and Derivatives Portfolio Manager at Union Securities Ltd., and is also a regular market analyst and frequent host on Canada’s most popular financial radio talk show Money Talks on CKNW980 in Vancouver, BC. He began trading in the financial markets 40 years ago and has held a number of senior positions during his long career as a commodity and stockbroker.

Victor’s trading focus is primarily on the currency, precious metal, interest rate and stock index markets and his clients are high net worth individuals and corporations.

Ed Note: To watch this commentary in video go HERE

Let me say — in no uncertain terms — that if you think all these markets that are rallying are about to shoot to the moon, I think you need to stand back and be very, very careful.

Yes, everything from gold to silver to stocks are rallying — but that does not mean the rallies are the real McCoy — and that they are going to continue to rally. Indeed, ALL of my indicators continue to suggest that big traps are being set, and the next big moves will not be UP, but instead, will be DOWN.

Let’s go right to the charts. Here’s my latest gold chart.

As you can see, gold is now pressing up against the top of a major cyclical trend channel, and it’s going to have a hard time getting through that resistance level.

In addition, I’m seeing signs that gold is overbought … and that demand in Asia, outside of China, is starting to slump. So I am still looking for another move down in gold. Long-term investors should hold their long-term gold positions. Speculators should continue to play the short side.

Now, my latest chart of silver.

Silver has come a lot further than I expected, no doubt about it. But here too silver is coming very close to a confluence of resistance levels on the chart, and it too is showing signs of being overbought.

Plus, it has not hit any major buy signals on my systems. I still expect a major move down in silver, and it will likely come without much notice, so please be very careful in silver.

Meanwhile, the dollar’s recent decline is beginning to stabilize. There’s mid-channel support around the 78.50 level on the Dollar Index, and I expect it to hold and give way to another rally in the dollar.

This is even more likely given the position of the euro, which has already staged a bounce that is near completion. So as the euro likely turns backs down, we will see another leg higher in the dollar.

Now to the Dow Industrials. The Dow is up against a triple-top now, and it would simply be foolish to be buying here. We may see the Dow poke a bit higher, but in my experience with triple-tops, any move up from here is likely to be a trap. Interestingly, the Dow is showing signs of what I’ve been warning all along — that it will eventually become a major new bull market. But that time has not yet arrived. We are far more likely to see a hard decline first, then a fourth attempt back to the horizontal resistance line you see on this chart. The fourth time though will be the charm, indicating a new bull market has arrived in the Dow. But I repeat, we are not there yet and a sharp, surprising sell off in the stock markets could come at any moment.

That’s it for this week. Stay tuned and best wishes, this is Larry.

Downside short term risk in equity markets currently exceeds short term upside potential. More sectors are starting to roll over from overbought levels. Fourth quarter earnings reports, economic news and possible macro events point to the high probability of at least a shallow, short term correction. Short term weakness will provide an opportunity to enter into seasonal plays that traditionally outperform during the spring season (e.g. Energy).

Equity Trends

Editor’s Comment: No question! Response to the U.S. employment report released on Friday was a surprise. Validity of the report is questionable, but the response was real. However, strength on Friday only pushed technical indicators to a greater short term overbought level. Regrettably, Tech Talk missed most of that gain, but the gain does not change the strategy on North America equity markets.

The S&P 500 Index gained 28.58 points (2.17%) last week. Intermediate trend is up. Support is at 1,158.66. Next resistance is at 1,356.48. The Index remains above its 50 and 200 day moving averages. It completed a “Golden Cross” last week. Short term momentum indicators are overbought and showing early signs of rolling over. Strength on Friday on news of the employment report was a surprise, but only caused the chart to become more overbought.

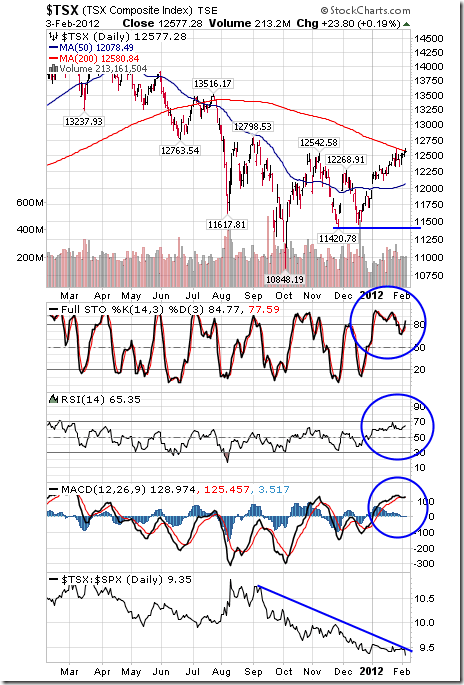

The TSX Composite Index gained110.78 points (0.89%) last week. Intermediate trend is up. Support is at 11,420.78 and next resistance is at 12,789.53. The Index trades above its 50 day moving average and trades at its 200 day moving average. Short term momentum indicators are overbought and showing early signs of peaking. Strength relative to the S&P 500 Index remains negative.

The U.S.Dollar Index was virtually unchanged last week (up 0.02). Intermediate trend is up. Support is at 74.72 and resistance is at 81.78. The Index remains below its 50 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming.

Crude Oil fell $2.07 per barrel (2.07%) last week. Intermediate trend is up. Support is at $92.52 and resistance is at $103.74. Crude fell below its 50 day moving average, but remains above its 200 day moving average. Short term momentum indicators are oversold, but have yet to show signs of bottoming. Seasonal influences turn positive in mid-February.

Gold slipped $3.10 (0.18%) last week. Notice the Leibovit volume reversal on Friday. Short term momentum indicators are overbought. Stochastics recorded a short term sell signal Friday. Strength relative to the S&P 500 was positive until Friday. A correction to its 50 and 200 day moving averages is possible.

….so much more over at Don’t Monday Morning Site HERE

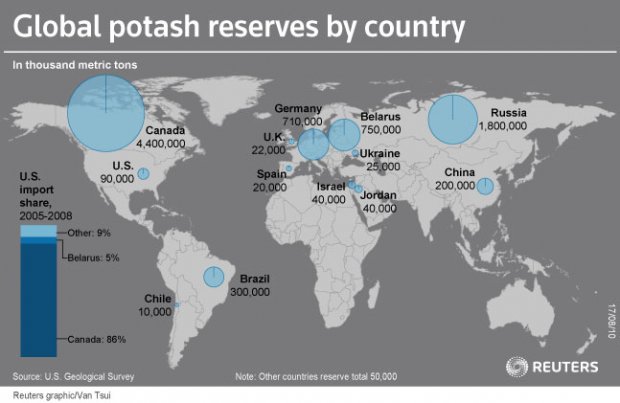

Last year marked the third-largest growth in the potash industry, but hesitancy from India and China may put things on hold in 2012. However, MGI Securities Analyst Corey Dias still expects to see a lot of positive news coming out of the junior potash space. In an exclusive interview with The Energy Report, Dias specifies which companies he’ll be following for progress.

COMPANIES MENTIONED: AGRIUM INC. –ALLANA POTASH CORP. – KARNALYTE RESOURCES INC. – PASSPORT POTASH INC. – POTASH CORP. – RIO TINTO – RIO VERDE MINERALS DEVELOPMENT CORP. – THE MOSAIC COMPANY –VERDE POTASH

The Energy Report: Total potash demand in 2011 was estimated at 56 million tons (Mt), and the market has traditionally grown at a rate of about 3.5%/year. Do you believe we’ll see a similar increase in 2012?

Corey Dias: I think 3.5% could be at the high end of growth for 2012. I would expect slightly lower growth this year given that India is delaying its potash purchases until the end of Q112. China is also determining its exact needs, and there are rumors that it may reduce its imports this year versus 2011. Everything tends to depend on price. Canpotex (the marketing company for Saskatchewan potash producers) and its Belarusian counterpart are holding out for higher prices than India and the China currently seems willing to pay. With those delays, demand will probably be slightly below the historical 3.5% growth rate.

TER: Potash Corp. (POT:TSX; POT:NYSE) of Canada has shut down two mines in that country, andThe Mosaic Company (MOS:NYSE) says potash buying is slow right now as buyers are taking a wait-and-see approach. What do you make of Potash Corp shutting down those two mines?

CD: It is a prudent approach. The company doesn’t want to flood the market with product as it would like to sustain a reasonable potash price that could provide a reasonably profitable return. By shutting down these mines, it’s limiting the output and that should keep the price at a fairly stable level. It’s not a question of shutting down so much capacity that prices are going to spike; it’s simply a way to keep potash prices relatively stable until the moment when a larger buyer comes back into the market, whether it’s India or China.

TER: In 2011, potash had the third-largest price increase among the 32 commodities ranked by the Scotiabank Commodity Index and, over the span of 2011, potash rose about 32%. The leading indicator of potash prices is often the price for corn, which is down significantly after some bumper corn crops in Eastern Europe, Russia, and Australia. What do you believe will be the average price per ton (t) for potash in 2012?

CD: Potash prices seem to be ranging between $450 and $550/t at the moment, depending on the port of delivery. It will probably stabilize around the $500/t level in the short term. I don’t see any reason for a significant spike in the price at this point. Although the corn price has recently seen a dip, it still remains above its historical average. Moreover, given the fact that the U.S. Department of Agriculture said that its stocks-to-use ratio is still well below the historical average, it would take a significant amount of corn production to reach the normal level of 15–20% in terms of that ratio, and reaching that level of production to meet this ratio could be a real challenge, especially when corn demand continues to grow. Therefore, while corn is slightly down, I don’t think there is going to be a downward trend in the corn price, or a complementary downward trend in potash.

TER: You don’t believe that potash will be in the top 10 performing commodities in 2012?

CD: I think it will have a fairly average year. I don’t think it will repeat its price performance in 2012 as it had a relatively low price point from which to start in 2011. It will probably stay somewhere in the middle of the park vis-à-vis other commodities.

TER: In an interview with The Energy Report in May 2011, Dundee Securities’ senior analyst Richard Kelertas predicted that we would see $750/t potash at some point before May 2013. What’s your perspective?

CD: As you said, that was in May 2011. The market looks a little different now than it did then. The fact that India is pushing back on pricing and delaying its purchases and China is reassessing are going to mitigate the potential upside of the potash pricing. Probably $600–650 is a reasonable price going to 2013, but there are a number of different factors that come into play in addition to India and China, whether it is production capacity being added to the market via brownfield or greenfield projects, whether or not there is a recovery in the European market, or whether or not the U.S. recovery continues. The fact that farmers seem to have a lot of money coming out of 2011 could, at worst, bode well for holding a pricing floor on potash at current levels and could potentially even support a higher price. I think that $600–650/t is reasonable.

TER: Tell us about your coverage universe and the types of companies you cover.

CD: I’m now ramping up coverage in the potash space. My first report was about Passport Potash Inc. (PPI:TSX.V; PPRTF:OTCQX), a name that I’ve followed since early 2011 when I was working in an institutional equity sales capacity at MGI. I really like this story and the fact that it’s in a safe, mining-friendly jurisdiction. An opportunity to build a mine in a potash-rich region—the Holbrook Basin—with only two competitors in the Basin could provide an opportunity for consolidation. It is a story with a great deal of appeal.

Generally, I’m looking at small-cap developers and am not restricted to North America. There are developers in Africa and South America that could be appealing in the same way. It will be up to clients to decide whether or not they have the risk tolerance for assets outside North America.

TER: Is that typically the type of company that MGI covers even in the other sectors?

CD: We tend to cover smaller-cap names. Large-cap names would be a bit more difficult for us to champion in a lot of ways because we wouldn’t necessarily get the mind space from clients for large-cap ideas because clients are well covered by banks and bulge bracket firms that are looking at the Potash Corps of the world, companies like Agrium Inc. (AGU:NYSE; AGU:TSX) and Mosaic.

TER: Passport Potash’s share price took a beating in 2011. It’s currently developing the Holbrook Basin potash project in Nevada. Why do you believe that junior is going to rebound this year?

CD: Part of Passport’s problem this past year was based on the market itself being quite volatile, especially toward the end of the year. In general, small-cap names tend to suffer the most in those circumstances. But management made a few promises to the market that it was unable to keep and probably didn’t realize the extent to which it would be punished by the market by having missed deadlines. However, I believe that the company is starting to right itself. It is in the process of putting together an NI 43-101-compliant resource estimate, which we expect to be released by the end of Q112. Following that, we should see a preliminary economic assessment or scoping study and, further, a prefeasibility study from Passport in order to show the economic viability of its project. In addition, there was an announcement on January 18th that Passport has brought on a new chairman who has significant operational experience gained during his time with Rio Tinto (RIO:NYSE; RIO:ASX). It also has added Ali Rahimtula, who has experience in India, which is key in this type of business because there is the potential for an offtake agreement with an Indian partner. Passport has acknowledged the fact that it needs more relevant experience on the board, and has clearly begun to address this shortfall.

Like most of the names in the junior developer space, there tends to be a rerating—in terms of valuation—of these types of businesses once milestones are met along the road to production. As Passport meets its milestones, the market will likely provide the company with a more positive valuation via a re-rating of its stock. The company’s stock price hit bottom at $0.17 toward the end of last year. Since then, it has been able to at least project to the market that it does have some deadlines, which it intends to meet. Passport has engaged the engineering firm ERCOSPLAN to complete its NI 43-101. ERCOSPLAN has a really good reputation in the marketplace and has done a lot of work for developers in the potash space worldwide. The market now understands that the company is working very hard to meet its current deadline and, once met, Passport will have a potash resource estimate to put to the market. The market at that point will respond favorably, in my opinion.

TER: A competitor operating in the same basin that Passport is operating in, the Holbrook Basin, already has an NI 43-101 resource of 125 Mt potassium chloride (KCl). How large do you expect Passport’s resource to be once it’s published?

CD: The competitor has about 94,000 acres of land, while Passport has about 81,000 acres. If we were to use a ratio of acres to contained tons of KCl for the competitor and apply it to what Passport has, Passport would probably come in somewhere about 100–101Mt of contained KCl. Remember, this is in no way a forecast that I am making as to the size of Passport’s resource. Even if Passport has something like 80% of that number, I think it’s still a decent-sized resource. In my report, I am forecasting that Passport will produce about 1Mt/year over 40 years. That implies about 40Mt of in situ KCl. If we’re talking somewhere between 80–100Mt of contained KCl, there is significant opportunity for Passport to increase the size of production on an annual basis, or it gives a bit more leeway in terms of what the potential resource size could be, on a contained-ton basis.

TER: You have a Speculative Buy on that particular equity. What is your 12-month target?

CD: My 12-month target for Passport is $0.75.

TER: Another junior in that space, Allana Potash Corp. (AAA:TSX; ALLRF:OTCQX), jumped out of the gate in 2011 and slipped above $2 in June 2011 before spending the rest of the year retreating from that benchmark. It now sits well below $1. Will that junior rebound this year? If so, what are the catalysts that are going to make that happen?

CD: I think so. Allana probably jumped up based on speculation more than anything else, but as the actual resource-related numbers come in, then it tends to start trading at some kind of multiple based on its enterprise value (EV), whether it’s EV:resource or EV:ton KCl, et cetera. When the market sees that it’s getting closer and closer to production, that’s when the valuation will start to improve. I think that is something that could happen this year. When one has an asset that doesn’t have any economic information tied to it, it’s very easy to speculate as to what you think the value should be. Obviously, the closer one gets to production, then there are hard and fast numbers that one can start applying some kind of multiple to in order to value a company like Allana Potash. That’s probably why it’s now down below $1. It’s probably more reasonably priced here and as more news comes out that’s favorable to the company, then you should start seeing the stock move back up.

TER: What are your thoughts on the Danakil potash project in Ethiopia?

CD: The Danakil project is interesting because it’s a near-surface project, which means the capex should be low. I think that it will have a fast track to production, which is another positive. And the fact that it’s probably selling to India, and perhaps China, is another positive because there is a quicker trade route to those countries when compared to North American or South American potash producers.

That said, there is no domestic demand for the product in Ethiopia. The companies that I believe have an advantage are those that have domestic demand or significant domestic demand, whether it’s a place like the U.S., which imports most of its potash needs, or South America—Brazil in particular—where 90% of its potash needs are imported. Ethiopia is also landlocked, that is, it has to go through another country in order to reach the port. Moreover, there is a greater possibility of political risk in Africa than in the U.S. or in Brazil. However, if everything remains stable, I think there could be a big opportunity for Allana, especially given its low operational cost base.

TER: What are some other small-cap potash plays that you expect will outperform in 2012?

CD: Verde Potash (NPK:TSX.V) is planning to produce a unique product called Thermopotash. Thermopotash, derived from the combination of glauconite and limestone, is a slow-release potash product with no chloride, which is great for crops like tobacco, coffee and oranges. In addition, the company is exploring the use of a new technology—the Cambridge process—which could potentially convert Verde’s potassium-rich rock to regular KCl. This would be a massive opportunity in Brazil. In terms of available infrastructure, Brazil falls behind North America but is certainly ahead of Africa.

Rio Verde Minerals Development Corp. (RVD:TSX) is another small company operating in Brazil that recently confirmed that it has potash on its property. The stock has moved up a little bit on the back of that news. Once an NI 43-101 resource estimate is released for Rio Verde Potash’s potash asset, we should see another re-rating of the stock.

Karnalyte Resources Inc. (KRN:TSX) is another one. Once again, I tend to favor the junior potash developers that have a bit of a unique element or bring something a little bit different to the table. Karnalyte is focusing on extracting potash from the potash-bearing carnallite layer, which is unusual for Saskatchewan because other producers and developers target the sylvinite layer that is usually closest to the surface. Karnalyte’s deposit is based on an anomaly where there is a significant carnallite layer that is relatively near-surface vis-à-vis the sylvinite layer. The technology that it is planning to use also could provide a magnesium byproduct and sodium chloride byproduct, both of which the Company could potentially market and sell in the future. Karnalyte has a number of things going for it; I think management is very strong. The fact that it has four patents pending for its technology could mean that what it ends up with is going to be very unique. It has a massive land holding and has only conducted advanced exploration on 20% of it. Fnially, it plans to expand its plant by using cash flow generated from its initial buildout.

TER: It has done a nice job of managing its share flow, too, with only about 21M shares outstanding vs. something far greater for a company like Allana.

CD: Yes.

TER: Or do you prefer a larger share count, such as Allana, with its 193M shares verus 20M for Karnalyte?

CD: When you’re in the small-cap space—and especially if your float is small—it becomes a bit riskier for clients to hold when the markets are a bit more volatile. It’s one thing to get into a stock, but when the market is volatile and a client is looking to exit a position, it’s very difficult to do if the trade volumes aren’t there. That’s the risk with Karnalyte. The average trade volume is 34,000 shares a day. So if you have a position that’s 100,000 shares, it’s going to take you roughly three days to get out of that position, and that assumes that you can be 100% of the trading volume over those days. And you could end up driving its price down significantly while you’re trying to exit your position. Having a more liquid position in a stock like Allana that you can get in and out of a lot more easily would likely appeal to portfolio managers.

TER: Could you give our readers an outline of what to look for in the small-cap potash space over the next year or so?

CD: You’ll see a number of companies starting to reach the prefeasibility and feasibility stages. At that point, these companies will start to look for strategic partners, whether it’s to fund the buildout of the products or secure an offtake agreement for the product that’s going to be produced a few years out. At that point, we’ll start to see which projects are going to be viewed as more viable. There probably won’t be enough demand to drive a need for every single junior potash developer that is currently out there to actually move into production. That said, there is also the possibility that some of these companies will be absorbed by larger entities that are looking to enter the potash space given the future, positive fundamentals for potash or those that are currently in the market and are looking to increase potential capacity moving forward. I expect to see a lot of positive news coming out of the junior potash space, especially as a few of these companies meet milestones in order to get a little bit closer to production and production becomes more of a reality.

Corey Dias has worked in the capital markets industry since 2003 and has spent eight years in institutional equity research and institutional equity sales. In addition, he has worked for a U.S. hedge fund, where he shared responsibility for the running of a $400M portfolio and sought out assets for private equity investment on behalf of the fund. Mr. Dias holds a Master of Business Administration from the Richard Ivey School of Business at the University of Western Ontario.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair