Personal Finance

Vancouver the second least affordable city in the World. But perhaps the biggest sign of a Canadian housing bubble is debt. The average debt burden of Canadian families stands at a remarkable 153 percent of disposable income—and growing. If the bubble bursts millions of Canadians will be left paying a fixed mortgage on a rapidly depreciating asset that will destroy their financial lives.

Canada’s Housing Bubble Is Stretched to the Limit

Do the math: If you earned a salary of $50,000 per year, and bought an average house, it would cost almost $300,000 (in Regina a 900sq ft house built on a small lot in the 1930’s goes for more than $200,000). In Canada, this salary puts you in the 20 percent tax bracket. That means you really only bring home $40,000 per year, or $3,300 per month.

Now look at your mortgage costs. A 4.5 percent, fixed-rate, 30-year mortgage has a monthly payment of $1,520 per month. Almost half your total income goes to paying just the mortgage. That’s why the mortgage industry started providing zero-down 40-year loans, before the federal government banned them for being too risky for consumers.

If you are like many people, and don’t have a 20 percent down payment, you will need to buy mortgage insurance. Estimate another $250 per month if you have close to 20 percent. If you only put down 5 percent, you will need to cough up closer to $700 per month.

Then there are property taxes: Add at least another $500 per month. Property insurance: Another 250 per month.

You haven’t even begun to consider upkeep costs, or home owner’s association fees, and you are already paying $2,520 per month. If you only put 5 percent down, you would be paying $2,970 per month. That would leave you a miniscule $330 per month, all of which would probably be needed to pay utilities.

….read it all HERE

The following is part of Pivotal Events that was

published for our subscribers February 2, 2012.

SIGNS OF THE TIMES:

“Take Federal bailout money, watch your company’s stock fall 90%, become a Co-Chair of Davos”

– Bloomberg, January 20

The headline was referring to Citigroup CEO Vikram Pandit.

“Junk-bond trading volumes are rebounding to the highest levels in 11 months – optimism.”

– Bloomberg, January 27

“Societe General SA and Credit Agricole SA were among French banks to have their credit grades cut by Standard & Poors.”

– Bloomberg, January 24

“The IMF cut its forecast for the global economy as Europe slips into recession.”

– Bloomberg, January 24

* * * * *

STOCK MARKETS

The best January for the stock markets in years has restored their popularity. Bullish comments include low P/Es and attractive dividend yields as well as favourable comparisons to bond yields. Not to overlook outstanding earnings gains.

In our dispassionate approach this is considerably different to conditions in early October. Choppy action, but rising until around January was possible and couple of weeks ago we thought it could continue into February.

The February 24th ChartWorks “Complacency Abounds Oh-Oh!” outlined the probability of a top within the next four weeks.

The surge out of mid-December has been exciting enough to register some cautionary alerts and last week we were looking for some “key” technical excesses. The S&P has since reached 73.3 on the daily RSI and this compares to 70 reached with the high of 1370 at the end of April. That was on the speculative surge that out proprietary Forecaster expected to complete in that fateful April.

Stock markets are poised to roll over. If so, the latest rally is a test of the April high which we considered the cyclical best of the first bull market out of the crash.

Credit Markets

The demand for risk continues with favourable action in corporate and municipal bond markets. Yields for the Italian ten-year keep going lower and after registering scary headlines last week even the Portuguese bonds are declining in yield.

Sub-prime mortgage bonds have rallied in price from 38 in October to 51.6 – that’s up a little more than half a point from last week.

Money market stuff such as the Ted-Spread started to narrow at the end of December.

To Ross’s “Complacency Abounds” in stock market volatility we would add that it is abounding in the credit markets as well.

Fortunately, we may have an exit indicator.

The action in municipals (MUB) has been good enough to register an Upside Exhaustion. The price could roll over within a couple of weeks and the change could be part of a general reversal in risk products. This will likely show up in the reversal in the stock market VIX.

Long-dated treasuries are working on a big top. Within this the final rally has been likely to occur as the excitement in stocks and commodities fades.

This has taken the bond future from the 140 level to the 145 level. The high was 146 in December.

Currencies

Ross targeted the decline in the US dollar index to around 78.8 and so far it has bounced off this level a number of times. With this, the Canadian made it up to 103 (briefly). It is now vulnerable to a decline in commodities.

Link to February 3, 2012 ‘Bob and Phil Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2012/02/jobs-boom-stocks-pop/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net“>bhoye.institutionaladvisors@telus.net

Negative real interest rates and growing global money supply power the Fear Trade for the precious metals

After prices fell 10 percent in December, many investors wondered if the bull market in gold was running out of steam. That was before Federal Reserve Chairman Ben Bernanke swooped in with a “red cape” and fired the bulls back up. Since the Fed reassured the world that interest rates will remain at “exceptionally low levels” for another two years, gold has jumped more than three percent.

….read more HERE

Also Peter Grandich recommends: AN ABSOLUTE MUST WATCH VIDEO TO THE END!!!

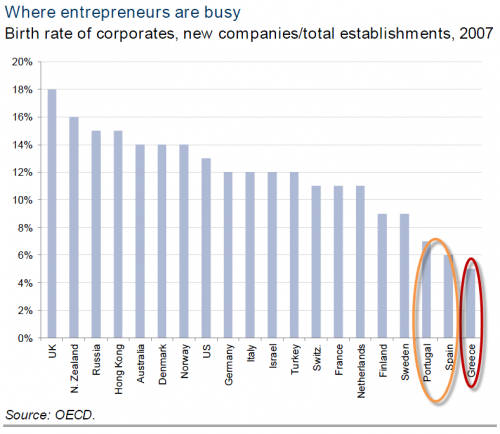

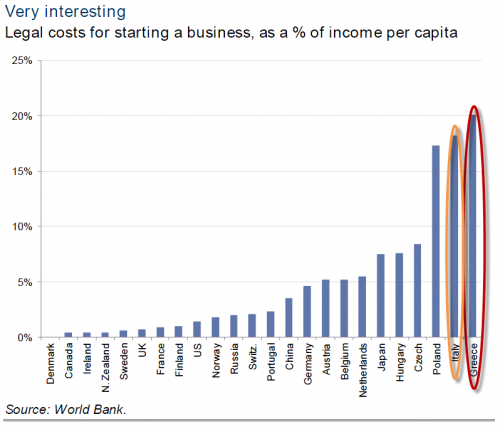

Perhaps after today’s budget miss in the Hellenic Republic it is time that the focus shift from the reality of a pending #fail for the voluntary PSI (for all the reasons we have at length discussed no matter how many headlines the markets tries to rally on) to a post-restructuring real economy reality in Greece. Whether self-imposed by devaluation or Teutonia-imposed by Troika, austerity is in the cards but there is a much more deep-seated problem at the heart of Greece – a total and utter lack of innovation and entrepreneurship. As Goldman’s Hugo Scott-Gall focuses on in his fortnightly report this week “the competitive advantage of innovation is one that developed markets need to keep” and in the case of European nations that desperately need to find a way to grow somehow, it is critical. Unfortunately, Greece, center of the universe for a post-restructuring phoenix-like recovery expectation, scores 0 for 3 on the innovation front. Lowest overall patent grant rate, lowest corporate birth rate, and highest cost of starting a new business hardly endear them to direct investment or an entrepreneurial dynamism that could ‘slow’ capital flight. Perhaps it is this reality, one of a Greek people perpetually circling the drain of dis-innovation and un-growth, that Merkel is starting to feel comfortable ‘letting go of’. Maybe some navel-gazing after seeing these three doom-ridden charts will force a political class to open the economy a little more, cut the red tape (after a drastic restructuring of course) and shift focus from Ouzo, Olive Oil, and The Olympics. We also suggest the rest of the PIIGS not be too quick to comment ‘we are not Greece’ when they see where they rank for innovation.

As if these were not bad enough, via Wikipedia, we also note the following three fun facts about the glorious Mediterranean nation:

Greece has the EU’s second worst Corruption Perceptions Indexafter Bulgaria, ranking 80th in the world, and lowest Index of Economic Freedom and Global Competitiveness Index, ranking 88th and 90th respectively.

Quite impressive…and no wonder 5Y CDS held their high cost of protection even when immediate credit event triggers were doubted…sooner rather than later they will default again unless something drastic changes and our admittedly premature discussion of more violence is becoming more and more likely every day as social unrest seems the only catalyst for change in a surreal world of central bankers, banks, and politicians.

I think by most conventional measures, used by most professional investors, European Central Bank Chief Mario Draghi has been a success. He has bolstered the returns for equity funds considerably since his decision to utilize a three-year term, instead of one year, in the ECB recent liquidity injection to European banks.

The fact is I missed the trees for the forest on this, and it has hurt. Failing to understand this lending-which reduced stigma associated with 1-year terms and better matched the funding needs of banks, led to more participation than expected. This in turn created a classic self-reinforcing positive feedback loop for asset prices:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair