Energy & Commodities

Loyal subscribers know I often opine that world markets are in the midst of a secular bull market for commodities, or “stuff”, as my recently passed friend Clyde Harrison was so fond of saying. Despite his traitorous penchant for Coors Light (instead of the classic St. Louis-brewed lagers), Clyde was one of those fellow Missourians who always had to be shown, and we all miss his wry wit, sense of humor, and insight into the speculative commodities markets.

You may also be aware of my many writings and interviews on the supply-demand fundamentals of copper, the metal with a “Ph.D. in Economics”. Copper is the one commodity that most directly reflects the near- and mid-term health of the world’s economy.

The modern copper industry started in the early 1900s with advent of large, mechanized open pit mines that could mine lower grades thru economies of scale. Development of these mines was coincident with the demand for and delivery of electricity to the industrialized world. Copper cable and wire is necessary for efficient transmission of electrical power and remains the main use of the metal.

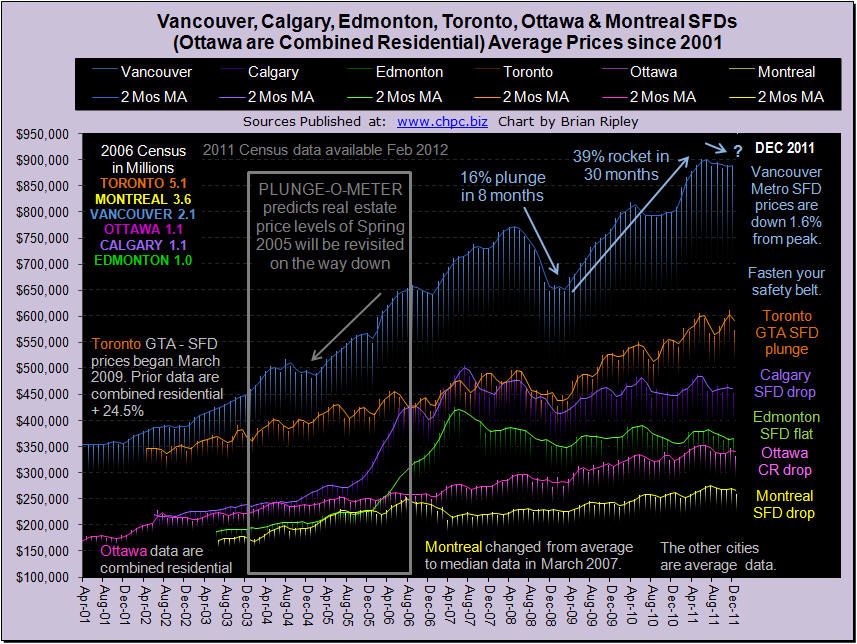

The chart above shows the detached housing prices for Vancouver, Calgary, Edmonton, Toronto, Ottawa* and Montréal (*Ottawa are combined residential). In December 2011 Canadian real estate prices resumed the trend down (Click HERE or on the image for Larger Chart) especially in Toronto, Ottawa and Calgary with M/M drops of 6%, 4.4% and 3.6%. Year end sales dropped off (Scorecard) and we will have to wait for January-February figures to get a glimpse of buyer appetite which certainly is not being held back by the cost of money (Yield Chart). Borrowing costs are low and asset prices are high. Should you be a buyer or a seller… start with figuring out your ROI here.

Powers Energy Investor Editor Bill Powers doesn’t shy away from microcaps; he embraces them. In this exclusive interview with The Energy Report, he explains why triple-digit oil is here to stay and how the best-positioned companies will be sitting pretty when natural gas prices rise—as will investors who time the rebound right.

COMPANIES MENTIONED: ADVANTAGE OIL AND GAS LTD. – ARSENAL ENERGY INC. – CHESAPEAKE ENERGY CORP. – CONNACHER OIL & GAS – DENBURY RESOURCES INC. – ENERGY XXI – EVOLUTION PETROLEUM CORPORATION – FAIRBORNE ENERGY LTD. – PETROBAKKEN ENERGY LTD. – PETROBANK ENERGY & RESOURCES LTD. – PETROMINERALES LTD. – QUICKSILVER RESOURCES INC – SM ENERGY CO. – SOUTHWESTERN ENERGY CO. – TOTAL ENERGY SERVICES – ULTRA PETROLEUM CORP.

The Energy Report: Is it fair to say that you are a value investor?

Bill Powers: Absolutely. I’m very much a value investor focused on fundamentals and finding companies that can grow reserves, production and cash flow without taking on too much debt and/or diluting shares. Those are the companies that can have very strong long-term outperformance. That is my theme, and I think it is really powerful right now. The companies I’ve identified do not currently reflect future prices that their stocks will be receiving.

TER: Clean balance sheets, steady cash flow and a depressed market price: would that sum it up?

BP: Yes. The Canadian junior market has changed in the last 10 years markedly. It’s matured greatly. Many companies have proven management teams and very good cash flow but are trading below their net asset value.

TER: Do you try to stay away from micro-cap stocks?

BP: Absolutely not; I very much embrace micro-cap stocks. As a newsletter writer, my commentary is largely directed at investors who want information on companies that are below Wall Street or Bay Street’s radar screen. I try to find the company that I feel is best positioned in a certain play and that have the chance for the best share price appreciation. Usually, it’s not the large-cap producers who have acreage in the play.

TER: How do you define a micro-cap?

BP: I consider a micro-cap as $250 million (M) on down.

TER: You recently wrote in the Powers Energy Investor that foreign investors are paying too much for joint venture (JV) agreements with large North American companies. If foreign companies are overpaying, why is that depressing the price of gas?

BP: I’ll give an example: Chesapeake Energy Corp. (CHK:NYSE) made a deal with Total Energy Services (TOT:TSX) to farm out its Utica shale acreage in Ohio. To put this into perspective, there have only been a handful of wells drilled in Ohio into the Utica shale, primarily within one county. This is a speculative play and I am very skeptical of how productive the Utica shale could really be.

That being said, the way these deals are structured is that Total, the foreign company in this case, pays $600M up front to Chesapeake, which will be drilling wells funded completely by Total. So between now and the end of 2014, it will be spending $1.5B on drilling. There are other companies that have done similar deals totaling maybe $20B from largely foreign companies farming into U.S. acreage. This is important because the foreign company will fund drilling for usually two years irrespective of gas price, and when companies drill with somebody else’s money, they are not sensitive to the fact that gas right now is under $2.50/thousand cubic feet (Mcf). It’s a good deal for the American companies, but it’s usually a very, very poor deal for the foreign firms.

TER: Classic economic theory says that if you keep producing like this and prices get very low, people will quit producing. Then, eventually, prices will go back up. When does that happen?

BP: I think it’s going to be happening fairly soon. Right now we have a glut of gas. Part of this is due to Haynesville and Marcellus operators’ drilling acreage to keep leases from expiring. The rig count is really starting to fall, especially in the Haynesville, which is producing 6 billion cubic feet (Bcf)/day right now and is the largest-producing field in the U.S. But that rate has already flattened out, and production will probably start to fall as rigs continue to get dropped. These are very high-decline wells. Texas production is beginning to decrease because the Eagle Ford is not offsetting production declines elsewhere in Texas. Gulf of Mexico production continues to go down. Basically, with gas under $3/Mcf, virtually every field in North America is uneconomic, and we will see a big slowdown in drilling. Very few companies have attractive hedges in place because we’ve had low gas prices for a couple of years. We will see a rebound in gas prices, and it will be quite violent. The challenge is finding the right timing of it. It is not so much a function of when the economics make sense as it is about when other people’s money runs out. We’re seeing that happen right now.

TER: Have we reached the point of maximum pessimism yet?

BP: That’s hard to say. I do think there is a lot of pessimism, but that doesn’t mean a reversal is imminent. I do think that at some time in 2012 we will see that reverse itself, and when that happens we will see gas prices increase substantially.

TER: It sounds like you are playing a very bullish scenario for natural gas. One of the first things I noted in your model portfolio from your Powers Energy Investor is that you have significant personal exposure to natural gas.

BP: Yes, absolutely. From an investor’s standpoint, being a contrarian is easy when your stocks are going up or when your ideas are being recognized by other market participants. What I’m doing in my newsletter is finding gas producers that have been beaten bloody by the marketplace but are low-cost producers that will make it to the other side to see the rebound in gas prices. I’ve identified about five companies that are leaders in certain plays or that have very good leverage to what I think are some of the best North American unconventional resource plays. Those are all places that will continue to produce into the future because they have the better acreage that will become economic once gas prices go back to $4/Mcf. Right now, you’re getting a lot of upside for free because the marketplace doesn’t believe that gas prices will eventually rebound.

TER: Could you talk about those companies you just referenced?

BP: Sure. One of the companies is Ultra Petroleum Corp. (UPL:NYSE), which is a slightly bigger company than I usually cover. It is very active in Wyoming on the Pinedale Anticline, and it’s also very active in the Marcellus. It is a very low-cost producer. This company was a penny stock about a decade ago.

Another I really like, a smaller company, is Advantage Oil and Gas Ltd. (AAV:NYSE; AAV:TSX). It has a great project in the Montney in Canada. It is an extremely well-run company that I think is doing very good work up there.

There are other companies that offer a lot of value and have seen their share prices decline, such asFairborne Energy Ltd. (FEL:TSX) in the Willrich. It’s a very exciting play in Alberta’s Deep Basin.

This is just a preview of companies that I think have good acreage and that are very leveraged to rising gas prices.

TER: Those were three of your five favored gas companies. What were the other two?

BP: One is Quicksilver Resources Inc. (KWK:NYSE). It’s a U.S.-based company that has a fair amount of debt on its balance sheet. However, for a small-cap company, it has fantastic acreage in the Horn River Basin, where it is very early stage, but this may turn out to be the best shale gas play in North America. Time will tell. This company has been around for more than 50 years, and it has a very good management team. It has been a leader in a number of shale plays. It had the Antrim shale in Michigan and the Barnett shale in Texas. It was one of the early players in those plays.

The other one I like is a bigger company that continues to produce very good results, and that isSouthwestern Energy Co. (SWN:NYSE) in the Fayetteville shale as well as in the Marcellus. The company has a dominant acreage position in the Fayetteville and has really been able to grow its production quickly in the Marcellus. It is a very well-run company by Steve Mueller.

So those are just some companies that I try to find. Each is unique. Each of them has different catalysts that will help its share prices more than double once gas prices start to move up. I think these stocks could go up three- or four-fold from here without any problem.

TER: Ok, you love natural gas. What about oil?

BP: I’m very bullish on oil. I think there are some very good factors that will keep the price of oil over $100/barrel (bbl) almost irrespective of how the economy does. With the natural declines from the Gulf of Mexico and the North Sea as well as Venezuela and Mexico, a lot of countries are struggling to keep up production. I think the U.S. has been able to increase its production materially over the last five or six years due to breakthroughs in technology, but that does not change the long-term trajectory of oil production in the U.S. We will see declines from California and the Gulf of Mexico, and we will see further production declines in Alaska, which will largely offset some of the very exciting production growth in unconventional plays, such as the Bakken in North Dakota or the Permian Basin in Texas. I do think triple-digit oil prices are here to stay, and I think we could see $150/bbl before too long, especially if there is a disruption in the Middle East. I think the leverage available to investors with small-cap companies is really mindboggling when you look at what oil prices mean to these companies.

TER: What oil-based companies are we looking at?

BP: Arsenal Energy Inc. (AEI:TSX), a very exciting play in the Bakken. It also has acreage in the Willrich and a very good management team. It is growing its production, and it just did an acquisition that grew its production to around 4 thousand barrels (Mbbl)/day. It has a very strong future as far as production growth that’s high net back, high cash flow and reasonable balance sheets. That’s one company that I am very high on. It has a market cap of only about $109M. It is one of my favorites.

As far as other companies that have great leverage that will go up, I’m becoming very keen on oil sands companies. I think companies like Connacher Oil & Gas (CLL:TSX) are going to rebound and continue to rebound. PetroBakken Energy Ltd. (PBN:TSX), Petrobank Energy & Resources Ltd. (PBG:TSX) and Petrominerales Ltd. (PMG:TSE) are all very oil-weighted companies that will be able to really ramp up cash flow in 2012 as oil prices maintain the $100-level.

Then we do see some U.S.-based companies like SM Energy Co. (SM:NYSE) in the Eagle Ford. This is along my theme of trying to find companies with the best leverage to a certain play. I think SM Energy has the best acreage in the Eagle Ford.

A couple of companies are involved in secondary oil recovery are Evolution Petroleum Corporation (EPM:NYSE) and Denbury Resources Inc. (DNR:NYSE). I think both of those companies are very well-leveraged to oil prices.

So those are some ideas that I think will provide shareholders great returns in the next two years.

TER: Speaking of oil sands, the Obama Administration nixed, at least temporarily, the Keystone XL Pipeline from Canada down to the Gulf Coast. Are the concerns valid? Aside from the developer TransCanada Corp. (TRP:TSX), who does this hurt?

BP: I think this really hurts American consumers. I don’t believe the concerns over the environmental aspects of the XL Pipeline were valid whatsoever. I think this was almost entirely a political maneuver. Right now, the U.S. still imports a substantial amount of production from overseas, and I don’t think some of these overseas suppliers are nearly as reliable as Canada. We import a lot from countries such as Venezuela and Mexico, which are struggling to maintain their production levels and are increasing internal consumption. So I think it is unlikely we will see material imports from either of those countries 10 years from now. Given the growth profiles of many Canadian oil sands producers such as Imperial Oil (IMO:TSX; IMO:NYSE.A) and Cenovus Energy Inc. (CVE:TSX; CVE:NYSE), I think we will see material growth in the Canadian oil sands from about 1.2 million barrels (MMbbl)/day to maybe 4 MMbbl by 2022, obviously depending on permitting issues and the price of oil. I think the Keystone would have been a very good supply. Eventually, I think the Canadians will get fed up and build a pipeline to Port Rupert and send the oil sands production to Asia if the U.S. cannot find some solution to get the XL Pipeline moving forward.

TER: The differential in price for what Asians are paying could pay for shipping that oil to Asia.

BP: Yes, absolutely. And one of the things we’re seeing in Asia is that some of the biggest producers such as Indonesia are seeing flat to declining production. And China has really struggled to keep its production flat. There have been some very good offshore finds in Malaysia and Vietnam that will replace some of the declines from places like Indonesia, but on an overall basis, those are not keeping up with the growing regional demand. Numerous Asian countries, especially China, would love to tap into the Canadian oil sands. A pipeline will get built. It’s just a matter of whether it leads to the U.S. or to the west coast of Canada.

TER: You have reviewed Energy XXI (EXXI:NASDAQ) recently.

BP: It’s not in my model portfolio right now, but I was very impressed that it has been able to grow production and that the company has a material oil weighting. It has a very good mix of exploration prospects as well as development prospects. Right now, the market has really turned its back on the Gulf of Mexico producers such as Energy XXI, and it is trading at lower valuations than its onshore peers, but it is able to generate material cash flow. In the case of Energy XXI’s balance sheet, I think some investors were a little scared off by its debt levels, which I see as very manageable given the cash flows it will be receiving over the next two years and its significant material reserves that it can borrow against. I think Energy XXI has a pretty bright future. I’m going to continue to monitor the company and see how it continues to execute over the next six months or so. It has a very good mix of high-impact exploration and lower-risk development.

TER: Bill, you are writing a book now?

BP: I’m currently working on a book that looks at shale gas and what I consider to be the myth of a 100-year supply. While there is a significant amount of shale gas that will be recovered in the next decade, it is nowhere close to a 100-year supply. Shale gas is not the game changer that a lot of people think it is.

TER: What thought would you leave us with?

BP: I think the perceived risks in energy investing have been somewhat overblown given where oil prices are. The space is very volatile, but for investors who can take a longer-term approach and who can identify companies that are well-run and that have legitimate projects, there are fantastic returns available. The energy sector has been out of favor, but the fundamentals are very strong. I think investors who can position themselves in gas-weighted firms ahead of the coming rebound will be richly rewarded, but there are also fantastic returns in oil-weighted companies that will benefit mightily from triple-digit oil prices.

TER: Bill, I’ve enjoyed speaking with you.

BP: Thank you for having me.

Bill Powers is the editor of Powers Energy Investor and previously the editor of the Canadian Energy Viewpoint and US Energy Investor. He is a former money manager and has been an active investor for over 25 years. Powers has devoted the last 15 years to studying and analyzing the energy sector, driven by his desire to uncover unrecognized trends in the industry and identify outstanding opportunities for retail and institutional investors.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

While the first reaction is for gold to rally and the pundits to come screaming out of the weeks yealling it’s inflationary, the harsh reality of this statement is….

U.S. stock markets just keep going higher and higher! How much higher will they go? I am forecasting another 25% higher for U.S. stocks! The ‘bullish trend’ from the breakout continues, as expected. Breadth has become strong, once again, including a new all-time high on the SPX Advance/Decline line to match the new all-time high for the SPX. My breath thrust index reissued another buy for the SPX on May 31st, 2017. Once the markets wake up and realize that there will be no U.S. tradewars, they will then begin their assent.

THE BIG PICTURE

The Fourth Industrial Revolution, which will be referred to as ‘Tech Hypergrowth’, will be the enabling attribute of technology’s new central role within the global economy. Through technological innovation and investment, in developing infrastructures, companies are heading into an all new frontier.

Harnessing technology so as to realize undeveloped opportunities is a hallmark of ‘tech hypergrowth’. This approach leads to the now quite familiar phenomenon of innovation. Tech Hypergrowth Companies are employing both existing and recently developed infrastructures for growth. These new opportunities lie in ongoing and recent technology shifts, industry transformations and demographic and societal changes. Research indicates that ‘tech hypergrowth’ companies are highly data-driven and that data is enabled to adjust the fit between the technology, the business and its’ customers.

‘Emergency Stimulus’ Is Now Permanent

Last Friday, June 2nd, 2017’s Jobs Report supported the number of new jobs that are now expected. If the economy continues to contract, the Fed, in alliance with the Trump Administration, will increase their money printing which will, in turn, push gold higher.

This explains why gold prices rallied in response to the disappointing jobs report. There is no market crash on the horizon. In last weeks’ article, May 26th, 2017, I wrote (that) “When short-term sentiment becomes pessimistic, it creates a new entry signal to re-enter the SPX long. This is exactly what occurred on May 25th, 2017”.

We still remain extremely bullish with a stop/loss at 2400. There is major support at the 2400 level. This level used to be strong resistance, then became major support in the May 2017 breakout.

Historically, the best sectors were dominated by staples, utilities and health care which had shown consistent positive returns.

Understanding correlations in complex financial systems is crucial in the face of turbulence, such as the continuing ongoing ‘financial crisis’. The strong breath and new highs support the advance of the SPX as it continues on its’ gains.

The New Bear Market Of Interest Rates

In recent decades, this has led to a further decline in interest rates, almost every time, along with a rally in the more defensive sectors of the stock market.

Over the past 36 years, the ten-year Treasury Note Yield has preceded a new downtrend in interest rates, virtually every time,when they have reached major support. Yields dropped an average of a 11% over the following year and declined 9 out of 11 times.

As interest rates continue to decline, it is great for bond funds, but not good for banks. The SPDR S&P Bank (NYSE:KBE) is near its 2017 low as depicted in the chart below.

The U.S. dollar index closed last week at a new low for the move at 96.67, down 47 basis points on Friday, June 2nd, 2017 (0.48%). The dollar’s trouble came when the government jobs report announced only 138,000 new jobs were created last month. This fell short of economists’ expectations and lower than that of April of 2017. Dropping yields are a driver of currency exchange rates and forecast future lower interest rates.

The U.S. dollar clearly took a hit from the May jobs report with expectations of the Fed raising U.S. interest rates beyond June. From a technical standpoint, the Dollar Index is bearish on the daily charts. With the lack of confidence that the Fed will not take any action beyond June, the dollar has been pushed further into a new bear market territory but price is nearing critical support and I do feel a short term bounce in dollar is near.

The Decoupling Of Correlated Asset Classes

In financial systems, correlations are not constant, all the time, but rather, vary over time. Reliable estimates of correlations are necessary to protect a portfolio. I find that the result that the correlation among different ‘asset classes’ scales ‘linearly decouple’ with market stress.

Consequently, the diversification effect, which should protect, melts away in our current financial times. My empirical analysis is consistent with the interesting possibility that one could anticipate diversification breakdowns.

In our very leveraged financial markets, the ‘leverage effect’ can decouple the traditional relationships correlation between the asset classes.

It is crucial to understand the fundamentals of the capital processes that are currently in play. President Trump is preparing for a major shake-up at the Fed. There are three vacancies coming up at the Fed’s Board of Governors. President Trump is preparing for a series of new appointments to the Fed. He is considering a former Federal Reserve Economist, who advocates the implementation of negative interest rates. The administration has been saying that it plans to deregulate the old rules that were imposed on Wall Street in the aftermath of “The Great Financial Crash of 2007”.

In January 2018, the term of Fed Chairwoman Janet Yellen will expire. The president is undecided whether he will reappoint her or seek a new appointee for this position.

In my opinion, President Trump wants a weaker dollar which in return will boost profits in U.S. corporation.

TRADES IN MAY:

Amicus Therapeutics Inc (NASDAQ:FOLD), up 18% in 6 Weeks

Direxion Daily Small Cap Bull 3X Shares (NYSE:TNA), up 5.9% in 11 Days

Direxion Daily Energy Bear 3X Shares (NYSE:ERY), up 4.75% in 2 Days

iShares Silver (NYSE:SLV), up 3.2% in 5 Days

Mobileiron (NASDAQ:MOBL), up 15% in 7 Days

FOLD, up 9.5% in 40 Days

Direxion Daily Gold Miners Bull 3X Shares (NYSE:NUGT), up 81% in 27 Days

VelocityShares 3x Long Natural Gas linked to S&P GSCI Natural Gas Excess Return (NYSE:UGAZ), up 74% in 14 Days

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair