Timing & trends

Surging Crude a Worry for Broader Economy, Boon for Service Stocks in Our Coverage Universe

For the most part, stocks have proven bears wrong so far in 2012 – for now. Strength has been more pronounced in the U.S. where a five-month rally has been built on a string of improving economic data that suggests U.S. corporate profit growth will remain intact near term at least.

The Standard & Poor’s 500 is up for eight of the last nine weeks. This week, the Dow closed above the 13,000 mark for the first time since May 2008 and the S&P 500 twice closed above 1,370, up 9% in 2012 alone. The NASDAQ, at one point, crossed the 3,000 level this week and is trading at its highest since 2000.

While Toronto’s main index closed lower on the day, driven down by slumping resource issues as oil prices fell 2.3% a day after hitting a 10-month high above US$110 on supply concerns in the Middle East. Lower gold prices also affected the resource weighted index, but year to date, the S&P/TSX Composite index is up 5.76%.

Look close enough and you can find both strident bears and bulls at present with relatively reasoned arguments on each side. In the near term, the markets may be due for a pull-back – this can be a natural conclusion. But in the end, we tend to care little about the near-term noise.

The fact is, there are some really expensive stocks out there and some really cheap ones when we look 1-3 years out. It is our job to find them.

OIL RAISES A RED FLAG AND AN OPPORTUNITY – One we have been positioned for over a year to take advantage of.

Investors are focusing more on economic data lately, with a bailout package for Greece in the works and U.S. earnings news winding down. But rising oil prices create some anxiety for the broader economy as crude is often considered a tax on doing business. As it rises, growth can slow. Concern about supply disruptions from Middle Eastern oil producers has kept crude oil above US$120 a barrel.

While the strength in crude could become a drag on the rather tepid recovery, it has already been a boon for oil service stocks as both energy producers and explorers continue to drill and utilize their strong current cash flow to expand. Year-end and quarterly numbers from the oil service stocks in our coverage universe started to come in at the end of this week and the growth has been very strong (as expected).

Forecasts for Q1 continue to be strong and we expect a relatively solid 2012. We will be updating these oil service stocks over the coming weeks for our clients with fully updated BUY/SELL/HOLD ratings.

Our first report will be on Strad Energy (SDY:TSX) which reported recorded record numbers and instituted a dividend policy late today. We are happy to report the stock reacted very favourably this week.

KeyStone’s Latest Reports Section

- Extrusion & Automotive Manufacturer Posts Strong Q1 2012, Pays Strong Dividend (3.1%), Looks for Growth in 2012 – Reiterate BUY (Flash Update)

- Micro-Cap Oil Sands Service Company Trades at 4 Times Earnings and with Big Growth Opportunities in 2012 (New Buy Report)

- Technology – Software Company Reports Record 2011 Results, Q4 EPS Significantly Beats Street Estimates (Flash Update)

- Oil & Gas Equipment Manufacturer Announces Tripling of Quarterly Dividend (Yield Now 4%) (Flash Update)

- Contract Drilling Company, Low Valuations (5.5 times EPS), Strong Growth, Strong Rig Growth – Initiating Coverage with SPEC BUY (Focus BUY) (New Buy Report)

The US dollar has been rallying strongly for several months. That’s what we call a “gift horse.” And just as the saying goes, “Don’t look a gift horse in the mouth.” Instead, look for ways to exchange your strong dollars for other currencies and investable assets that don’t fly out of Federal Reserve Chairman Ben Bernanke’s printing press.

For many Americans, foreign investments are more of an accident than an objective. They might own a few foreign stocks through a global mutual fund. Or they might have some exposure to foreign economies and currencies through the shares of an American multinational corporation like Johnson & Johnson or GE.

But American stocks and bonds remain the steak and potatoes of traditional American investment portfolios. Foreign stocks and bonds are merely the spices and sauces. This provincialism — epitomized by the spectacular success of Warren Buffett’s Berkshire Hathaway — has served American investors very well for several decades. But a reassessment may be in order.

Simply stated, the America of the future may not reward investors as handsomely as the America of the past. For example, despite doubling from its lows of March 2009, the S&P 500 index has produced a negative total return during the last five years… and only a miniscule return during the last 10 years.

The US dollar’s role as the ultimate “safe haven” currency is also due for a reassessment. While the dollar may be safer than the euro, for example, the dollar is hardly safe in any absolute sense. The dollar is safer than the euro… just as a rabid squirrel is safer than a rabid wolf. But you don’t really want to cuddle up at night with either one.

America’s federal debt has exploded to more than 100% of GDP — an astonishingly large Greek-like debt load. Yet none of America’s political or financial leaders seem to have any plan for reducing the nation’s debt… except maybe to add a graveyard shift to the dollar-printing production line at the Philadelphia Mint.

Our advice: Spend your strong dollars while you can. Reallocate them into other currencies and asset classes.

Throughout the eurozone crisis of the last few months, the US dollar has been attracting widespread “flight to safety” demand. But the dollar is not merely rallying against the euro; it is rallying against almost every investable asset on the planet. For example, a dollar buys 36% more silver today than it did six months ago. A dollar also buys 20% more wheat, 13% more corn… and even 2% more “American house.”

If we broaden out our analysis to include stocks and currencies, the results are similar. A dollar buys 32% more French stocks today than it did six months ago… as well as 34% more Indian stocks and 18% more Japanese stocks. Among world currencies, a dollar buys 11% more Norwegian kroner today than six months ago… as well as 15% more Swiss francs and 8% more Canadian dollars.

It is that last financial asset — the Canadian dollar — that we find particularly compelling as an alternative to holding US dollars. The Canadian dollar, known affectionately as the “loonie,” possesses many virtues.

In no particular order:

- Canadian government finances are fairly solid; US government finances are spiraling out of control. Canada stands out as being one of the few countries that is not only rated AAA by the major credit agencies, but actually possesses a AAA balance sheet… or at least something close to AAA.

- Canada’s GDP growth is outpacing US GDP growth.

Canadian employment growth is booming; U.S employment growth is moribund. The Canadian economy has created nearly 800,000 jobs during the last five years, while the US economy has lost more than 5 million! In other words, the Canadian labor force has expanded by 4%, while the US labor force has contracted by 4%!

As a result of these trends, Canada is becoming an increasingly attractive investment destination, relative to the US The Canadian dollar, in particular, is increasingly attractive. The Canadian dollar’s appeal is hardly a new story, but it remains a very relevant story.

As the nearby chart illustrates, the Canadian dollar has been trending higher against the US dollar for several years. We expect this trend to continue — more or less — over the next several years. But investors should expect some bumps along the way. Currencies can sometimes bounce around even more than stocks. The Canadian dollar plummeted more than 25% during the depths of the 2008 credit crisis, for example, as terrified investors piled into the US dollar. Once the crisis eased, the Canadian dollar recovered. But the lesson is clear: Currencies can be volatile.

If you have a mind to Fed Reserve-proof a strong dollar, we like the Canadian dollar.

Regards,

Addison Wiggin

for The Daily Reckoning

Joel’s Note: It’s hard to put one’s finger on the exact date it began, but harder still to deny that the American Empire is in gradual, inexorable decline. It’s nothing personal. All things come to an end…even world dominance.

Some say the beginning of the end ticked over in 1913, with the passing of the Federal Reserve Act and the introduction of the Income Tax. Others argue all was well until Richard “Tricky Dick” Nixon cut the dollar’s last, tenuous ties with gold in 1971. Or maybe it was when the military industrial complex found the excuse it needed to kick into overdrive at the beginning of this millennium. Who knows?

In any case, the writing has been on the wall for some time. What we do know is that, as the managed economy attracts more and more meddlesome parasites, each with a nosier fix than the last, the boom-bust cycle increases in both frequency and magnitude. This general trend has led Addison to forecast the “Mother of All Bubbles.”

Find out what he’s talking about…and discover the safe haven investments you can employ to help protect yourself, right here.

“The Bank of Japan and The Bank of England are also flooding their markets with newly printed cash. And this week, in comments before Congress, Federal Reserve Chairman Ben Bernanke also signaled he has no intention of stemming the flood of easy money coming from his central bank.” – Money and Markets

US Stock Market Update

by Peter Grandich

Despite numerous bearish long-term fundamentals, I’ve stated the market’s least resistance is up. While not a card-carrying member of the “Don’t Worry, Be Happy” crowd, I’ve managed to avoid taking any bearish strategies and thus not becoming part of the perma-bear carnage that has grown since the bottom in March 2009.

Having said that, I do think it’s time to start preparing for the top in this massive countertrend rally in a secular bear market that began back in late 2007. Somewhere between here and the marginal new, all-time high I suggested the DJIA could reach, I feel selling non-metals related shares seems wise. I would like to be mostly in cash (except for mining shares) before years-end.

I know the question many now have – what about resource stocks? Selling in May and going away may just be wise this year but for now, all systems remain go.

I do believe on the first news of a large-scale military conflict with Israel and Iran, we shall likely expedite any selling still left to do.

Stay tuned!

ABOUT PETER GRANDICH

Though he never finished high school, Peter Grandich entered Wall Street in the mid-1980s with no formal education or training and within three years was appointed Vice President of Investment Strategy for a leading New York Stock Exchange member firm. He would go on to hold positions as a Market Strategist, portfolio manager for four hedgefunds and a mutual fund that bared his name.

His abilities has resulted in hundreds of media interviews including GMA, Neil Cavuto’s Your World on Fox News, The Kudlow Report on CNBC, Wall Street Journal, Barron’s, Financial Post, Globe and Mail, US News & World Report, New York Times, Business Week, MarketWatch, Business News Network and dozens more. He’s spoken at investment conferences around the globe, edited numerous investment newsletters, and is one of the more sought after commentators.

Grandich is the founder of Grandich.com and Grandich Publications, LLC, and is editor of The Grandich Letter which was first published in 1984. On his internationally-followed blog, he comments daily about the world’s economies and financial markets and posts his views on social and political topics. He also blogs about a variety of timely subjects of general interest and interweaves his unique brand of humor and every-man “Grandichism” expressions with his experience gained from more than 25 years in and around Wall Street. The result is an insightful and intuitive look at business, finances and the world, set in a vernacular that just about anyone can understand. In his first year, Grandich’s wildly-popular blog had more than one million views. Grandich also provides a variety of services to publicly-held corporations on a compensation basis.

Peter Grandich “This an opportunity for those not yet fully invested in gold and silver. Last call! Train to pull out of the station on the way to new highs by summertime”……….. Mark Leibovit – “The bottom line here is we will still see a big move to the upside because we have a tight physical market and that’s going to cause the price to explode higher.”

GOLD – ACTION ALERT – BUY – Written 3/01/2012 by Mark Leibovit

Perhaps I had a sixth sense that something may be ‘rotten in Denmark’ when I wrote yesterday morning: “Though I am on a BUY signal, remember, chasing any market is not a wise financial practice. If you have been slowly accumulating positions all along (at all levels), there is less stress in trying to ‘catch up’ and chase prices when they are rising. The ‘boys’ have the power to pull the plug at any time. We learned that last year. I suspect the ‘big’ players (hedge funds) are also part and parcel to the current upside action. When they change their mind, watch out. I suppose NOT seeing gold and silver into new record highs this year might act as such a catalyst on their part.”

Gold prices were selling off Wednesday after Federal Reserve Chairman Ben Bernanke indicated that an additional round of quantitative easing was becoming increasingly unlikely. We experienced a ‘flash-crash’ type scenario yesterday. Short-term, a ‘Key Reversal’ and Negative Leibovit Volume Reversal patterns on some daily and weekly charts. At the worst levels, spot gold declined $106.00 measuring from Tuesday’s 1792.40 high to yesterday’s 1686.40 low. Silver declined from the morning high of 37.62 to 33.88 or $3.74.

Central planners can’t announce they are going to have constant and massive QE or everything would go to the moon. So the idea is floated around that QE3 is off the table. If gold and silver are going to head a lot higher from here, this is what you would expect the manipulators to do ahead of that move to make sure as few people as possible are on the long side. The bottom line here is we will still see a big move to the upside because we have a tight physical market and that’s going to cause the price to explode higher.

Seasonals warn of a top at the end of February for Gold and an equivalent top by mid May, so much of this may be just a cyclical phenomenon regardless of Bernanke. That said, technicals rule and until we clear highs from earlier today and/or Positive Leibovit Volume Reversals are formed, some caution needs to be exercised if you’re trading. I am in the camp that any washout (including this one) is a buying opportunity, so I remain on my BUY signal. That said, picking the exact bottom of such events is more of an art than a science – so I cannot provide you a precise downside target for this correction. Indeed, we could have seen the lows yesterday. If you believe as I do that silver is headed into triple digits (maybe high triple digits) and gold could see $11,000 an ounce in the current decade, any washout is an opportunity to do some buying.

For details the Leibovit VR Gold Letter (www.vrgoldletter.com) and the VR Forecaster (Annual Forecast Model) report which is now available at: https://www.vrtrader.com/subscribe/index.asp

After Gold’s No-QE3 Plunge, Market Clear For Another Rally

posted @ 3/01/2012 @ 4:37PM by Forbes

“What caused such a violent drop? Evidence points to Fed Chairman Ben Bernanke’s omissions regarding further easing, and QE3 specifically, in Wednesday’s Congressional testimony. Dennis Gartman and UBS’ Edel Tully agree on that, and so does the price chart. “

…read full article HERE

Opportunity Knocking

I see gold close near $1700 and silver under $35. I am travelling back from vacation in Florida and consider this an opportunity for those not yet fully invested in gold and silver. Last call! Train to pull out of the station on the way to new highs by summertime. Peter Grandich Written 02/29/12 Grandich.com

Fractal Gold Report: Flash Crash

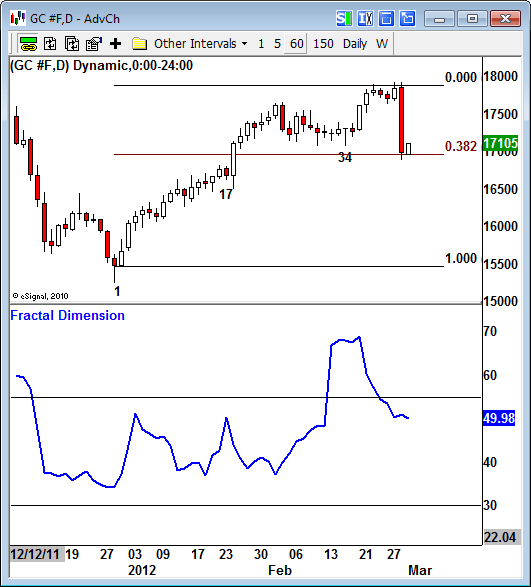

One of the really interesting things about Wednesday was how the carnage was for the most part limited to gold and silver. Other markets saw an uptick in volatility, and some scattered selling, but really nothing close to gold. Even oil came down for a 38.2% retracement and bounced right back up, and stocks didn’t really do all that much.

So what the heck happened?

It seems hard to believe, but gold did a 38.2% retracement of the entire move off the bottom in just one trading day, and almost right to the tick. Such a super-intense retracement can still be part of a bullish pattern — in fact, if the market survives such a test, this sort of hard retracement can become the impetus for a giant rebound, and a trending move that extends for weeks.

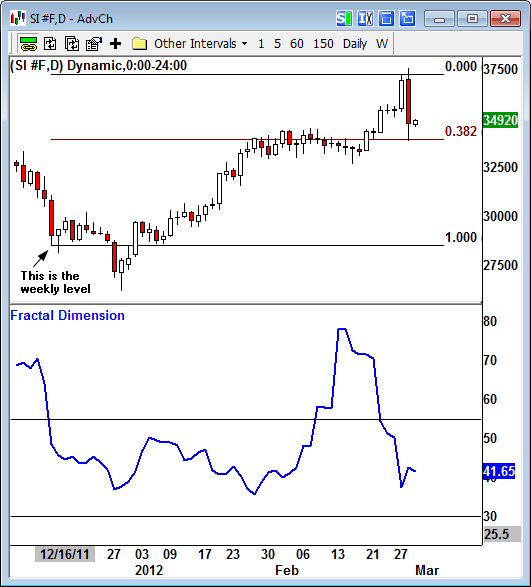

Silver also completed a to-the-tick 38.2% retracement of its full move off the bottom.

So even though it didn’t remotely resemble anything bullish, this type of sell-off can still be considered part of an ongoing bullish pattern, in both gold and silver. The problem is the size and scope of the moves in precious metals right now, as these patterns are not exactly unfolding on a “user-friendly” scale. It’s crazy out there, and that’s not likely to change anytime soon.

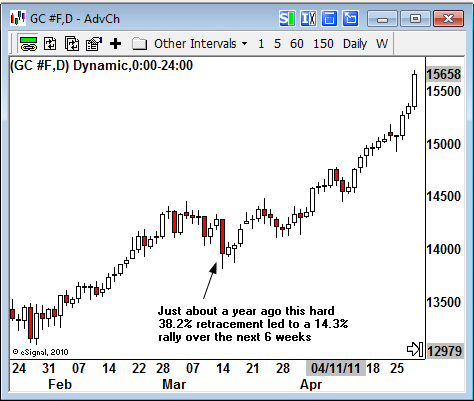

In fact, this set-up reminds me of another Bernanke-inspired sell-off about a year ago that was the direct precursor to 14% rally over the ensuing 6 weeks.

An equivalent rally from here will take gold back to the all-time highs around $1,920. But I think this could actually be the set-up for a bigger rally up to the $2,100 target area. A very hard 38.2% retracement typically triggers an even bigger response in the direction of the trend. And I can’t recall ever seeing a harder 38.2% retracement.

So it’s alarming to see gold plunge like this, but it’s definitely not over yet for this emerging pattern. However, the bullish case will suffer a major set-back, at least in the short-term, if gold sinks below $1,690 and can’t get right back over.

But if gold holds here, and especially it if quickly rebounds over $1,733, then the bullish pattern should be stronger than ever. In fact, this could be a perfect set-up for options, futures, and leveraged positions, as a market that survives and rebounds after a hard retracement will often see relentless upside pressure for weeks.

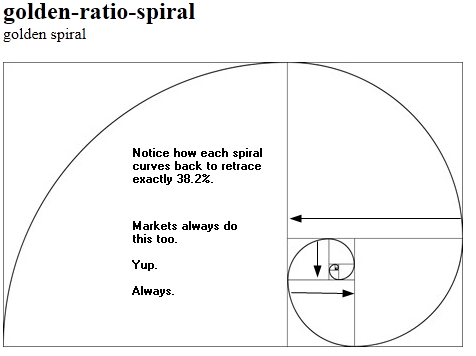

Fractal Editor’s Note: 38.2% retracements are the building blocks of every single trending move in markets, and the closest thing to a “market law” that will ever be characterized. This is because the 38.2% retracement is a component of the golden logarithmic spiral, which is based on the golden ratio and the Fibonacci series. The golden spiral is a foundational pattern for financial markets, as it is a universal shape that is infinitely scalable in both directions, both outwards and inward, which is a necessary characteristic for fractal systems like markets.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair