Timing & trends

Martin Armstrong’s perspective fascinated so many at last night’s Emergency Gold Summit, as you can tell from this sent to Martin:

Thank you. Your insight into how everything is connected has saved me a fortune. I cannot tell you how many people showed up tonight simply to hear you. As the moderator said, you have the best track record of anyone. Your insight into the world is amazing. I understand what you said tonight as so many were talking about your speech walking out. It will be the markets that force political change. You have thousands of followers here in Vancouver. You should know that.

Thanks for everything you are doing.

R…S,,,

Martin’s Answer to R…S,,,

Thank you. It is nice to see the understanding of the world economy is growing. I believe to create political change that will preserve our liberty, it requires the public to grasp the world is all connected. If we can accomplish that, we have a chance at leaving our children and their’s a better life rather than a dismal one. I have been speaking in Vancouver for 30 years. It has always been one of my favorite spots in North America.

An example of Martin’s thinking that he posted in this on his blog last night:

Why The Fed Risks are Nonsense

All we have heard is about the hyperinflation is all based on the idea that the Fed has increased the money supply. I have warned that the dollar has become the new world currency. The German elections in September are not looking good. Let’s just step back a second and look at the issue without bias. The real risk of the Fed is perhaps a half-trillion loss that is less than 3% of GDP. We have the Bank of England buying nearly 100% at times of government new debt compared to 60% at the Fed. The Fed has simply a theoretical inflation risk. However, what is the risk at the ECB and Bundesbank? The risk there is the collapse of the Eurozone that ends in the split of the union. The whole issue of the ECB saying that depositors will have to bailout the banks is because they cannot reach agreement of who will pay for what. Germany is not about to pay for a bailout of Spanish banks. So the only solution is that the depositors of the troubled bank will have to suffer the loss. That is the “fair” way of doing this with of course those with more than a €100,000 euro will pay most of the cost.

All we have heard is about the hyperinflation is all based on the idea that the Fed has increased the money supply. I have warned that the dollar has become the new world currency. The German elections in September are not looking good. Let’s just step back a second and look at the issue without bias. The real risk of the Fed is perhaps a half-trillion loss that is less than 3% of GDP. We have the Bank of England buying nearly 100% at times of government new debt compared to 60% at the Fed. The Fed has simply a theoretical inflation risk. However, what is the risk at the ECB and Bundesbank? The risk there is the collapse of the Eurozone that ends in the split of the union. The whole issue of the ECB saying that depositors will have to bailout the banks is because they cannot reach agreement of who will pay for what. Germany is not about to pay for a bailout of Spanish banks. So the only solution is that the depositors of the troubled bank will have to suffer the loss. That is the “fair” way of doing this with of course those with more than a €100,000 euro will pay most of the cost.

In this case the Bundesbank, that sits on €700 billion of peripheral euro (debt) assets of member states. If these assets were shaved by 30%, the currency devaluation for such assets would be about 5% of the German GDP. Clearly, the risks of a catastrophic collapse exists in Europe on a major scale. No such risk exists at the Fed.

The Swiss government holds assets of €350 billion in foreign currency reserves. A 20% franc revaluation to EUR/CHF parity would give them a loss of €70 billion that would amount to 15% of Swiss GDP. The risk for the Swiss is trying to prevent the Swiss from rising against the Euro and that risk in the result of the peg. The Swiss are intentionally buying Euro to keep their currency down. The peg is a loss that could be devastating. They are trying to diversify in turn selling the Euro for other currencies including A$ and C$ along with the US$ of course..

The dollar is the only game in town. If the German elections turn bad, look out come September.

Ed Note: To order the entire Video Presentation of the Emergency Gold Summit including Martin Armstrong’s presentation click below HERE

Mike Campbell: Martin Armstrong has been clear for the last two years that while the market would dictate ultimate price action – the trend remained down. His models warned that gold was not the place to be until late 2015 at the earliest. He has written consistently that the majority of gold analysts don’t understand the factors that move gold. Over the years I have learned to pay attention when Marty speaks.

That’s why personally, I wanted him to answer the questions above and the video includes that Q&A with Marty at the Emergency Gold Summit.

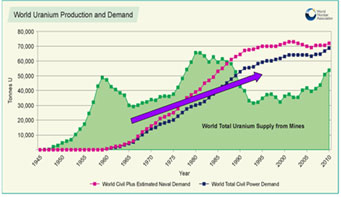

Today there are no fewer than 60 nuclear plants under construction in 14 countries, with another 163 planned and 329 proposed.

Many countries without nuclear power are on the cusp of building their first reactors, including Vietnam, Turkey, Indonesia, Egypt, Kazakhstan, and several among the Gulf emirates. And while many countries with nuclear reactors took a moment to pause and reassess safety standards in light of the Fukushima disaster, almost all have reasserted their support for nuclear power as a major component of their energy strategies.

Uranium is simply the only fuel right now that can reliably produce large amounts of electricity without the release of greenhouse gases and other hydrocarbon pollutants.

Uranium is simply the only fuel right now that can reliably produce large amounts of electricity without the release of greenhouse gases and other hydrocarbon pollutants.

Demand is clearly ramping up, and the world is already short on uranium. In 2011, world industry consumed 165 million pounds of U3O8 but produced only 143 million pounds.

Indeed, the world hasn’t produced enough uranium to meet demand for some two decades.

Secondary supplies have been filling the gap to date. For example, since 1993 the Megatons-to-Megawatts agreement between Russia and the United States has been working toward the goal to recycle 500 tonnes of highly enriched uranium (HEU) from Russian nuclear weapons into the LEU that reactors use to produce electricity. But remember, that deal is set to end next year.

The end of Megatons-to-Megawatts will eliminate 24 million pounds of uranium supply just as demand starts surging. The World Nuclear Association predicted global uranium demand will have increased 33% by 2020, and will then climb almost that much again in the next 10 years.

Those are huge increases. In 2011, the world consumed about 70,000 tonnes of uranium. By 2024, we are expected to need 100,000 tonnes. Can production keep up? Not likely.

If every potential uranium mine on the horizon were approved, built, and commissioned on schedule, supplies might just keep up with demand. But current uranium prices are rendering many potential mines uneconomic, and global economic uncertainty is making it very difficult for uranium companies to obtain the cash they need to build mines. It all adds up to one conclusion: a supply gap is looming.

…..read the entire essay HERE

The persistent decline in gold prices over the past two weeks has produced the first Capitulation Buy Alert since July 1997. The only other signals occurred in September 1988, December 1984 and September 1975. A period of consolidation, with an upside bias, is the most common characteristic in the following weeks.

Three occurrences saw prices rally back to the 50-day moving average within three weeks (currently $1488). The most recent examples saw prices recover to the 150-day average within twelve weeks (now $1619 and declining at $2 per day).

Ed Note: This May 23rd image and comment is from the 1st page of a May 20th 5 page report. This report and 2 follow-up May 23rd reports (a 5 page on silver & a 4 page on Gold) would have been come to you had you been subscribed to Institutional Advisors Free One Month Trial. Be sure not to miss another by subscribing to that FREE ONE MONTH TRIAL of Bob Hoye’s Institutional Advisors. Twitter will announce Publications.

Interest Rates – Greg Weldon Analyses Bernanke & The Fed’s Congressional Testimony as it relates. Go to the 5:37 mark for the beginning of Greg’s presentation. The 7:35 Mark for Greg’s comments on where & when they intend to get short the Bond Market.

Ed Note: With Michael’s Emergency Gold Summit occurring tonight and Precious Metal stocks grinding around the attendee’s and

Ed Note: With metal mining stocks grinding around, names are what you need for investing/speculating. Gregory Weldon’s daily TrendTRAKr is brilliant for isolating Equities & ETF’s in all phases of trending, trend strengthening, trend weakening & end of trend . You can get a 30 Day FREE TRIAL of this $1,200 service HERE, or outright register HERE.

Inquiring minds with extra time on their hands this morning (May 23rd) g are plodding through the Full Transcript of Bernanke’s Testimony To Joint Economic Committee, U.S. Congress looking for the usual collection of half-truths, distortions, and outright lies it usually contains.

Here are some point-by-point statements by Bernanke with my comments immediately following each set of statements.

Bernanke: Conditions in the job market have shown some improvement recently. The unemployment rate, at 7.5 percent in April, has declined more than 1/2 percentage point since last summer. Moreover, gains in total nonfarm payroll employment have averaged more than 200,000 jobs per month over the past six months, compared with average monthly gains of less than 140,000 during the prior six months.

Mish: What Bernanke failed to say is real wages are anemic and the Fed’s low interest rate policy is making it easy for corporations to borrow at excessively low rates and use the money to invest in hardware and software robots to fire workers. Excessively low rates also punish savers and those on fixed income.

Bernanke: Payroll employment has now expanded by about 6 million jobs since its low point, and the unemployment rate has fallen 2-1/2 percentage points since its peak.

Mish: Even if those were all full-time jobs, this was a very anemic recovery by historic standards.

Bernanke: Despite this improvement, the job market remains weak overall: The unemployment rate is still well above its longer-run normal level, rates of long-term unemployment are historically high, and the labor force participation rate has continued to move down. Moreover, nearly 8 million people are working part time even though they would prefer full-time work. High rates of unemployment and underemployment are extraordinarily costly: Not only do they impose hardships on the affected individuals and their families, they also damage the productive potential of the economy as a whole by eroding workers’ skills and–particularly relevant during this commencement season–by preventing many young people from gaining workplace skills and experience in the first place.

Mish: That is a reasonably accurate set of statements but nowhere does the Fed admit its role in creating those conditions with its boom-bust, moral-hazard monetary policies.

Bernanke: The loss of output and earnings associated with high unemployment also reduces government revenues and increases spending on income-support programs, thereby leading to larger budget deficits and higher levels of public debt than would otherwise occur.

Mish: The fiscal deficit is high because of perpetual overspending by Congress on top of the Fed’s boom-bust, moral-hazard monetary policies.

Bernanke: Consumer price inflation has been low. The price index for personal consumption expenditures rose only 1 percent over the 12 months ending in March, down from about 2-1/4 percent during the previous 12 months. This slow rate of inflation partly reflects recent declines in consumer energy prices, but price inflation for other consumer goods and services has also been subdued. Nevertheless, measures of longer-term inflation expectations have remained stable and continue to run in the narrow ranges seen over the past several years. Over the next few years, inflation appears likely to run at or below the 2 percent rate that the Federal Open Market Committee (FOMC) judges to be most consistent with the Federal Reserve’s statutory mandate to foster maximum employment and stable prices.

Mish: The Fed has no idea what inflation is or why because the Fed ignores asset bubbles in stocks, in bonds, and in houses. It uses fatally flawed definitions of inflation, inaccurately measured at that.

Berrnanke: Over the nearly four years since the recovery began, the economy has been held back by a number of headwinds. Some of these headwinds have begun to dissipate recently, in part because of the Federal Reserve’s highly accommodative monetary policy. Notably, the housing market has strengthened over the past year, supported by low mortgage rates and improved sentiment on the part of potential buyers. Increased housing activity is fostering job creation in construction and related industries, such as real estate brokerage and home furnishings, while higher home prices are bolstering household finances, which helps support the growth of private consumption.

Mish: Housing sentiment has indeed improved, but that is of course what happens when central banks artificially suppress rates with the purposeful intention of creating asset bubbles, not to help consumers, but to bail out banks still stuck with housing inventory they need to unload.

Bernanke: Over the past four years, state and local governments have cut civilian government employment by roughly 700,000 jobs, and total government employment has fallen by more than 800,000 jobs over the same period. For comparison, over the four years following the trough of the 2001 recession, total government employment rose by more than 500,000 jobs.

Mish: At best, that’s a start. And it fails to address untenable union wages and benefits and absurd collective bargaining agreements of public workers.

Bernanke: At the same time, though, fiscal policy at the federal level has become significantly more restrictive. In particular, the expiration of the payroll tax cut, the enactment of tax increases, the effects of the budget caps on discretionary spending, the onset of the sequestration, and the declines in defense spending for overseas military operations are expected, collectively, to exert a substantial drag on the economy this year. The Congressional Budget Office (CBO) estimates that the deficit reduction policies in current law will slow the pace of real GDP growth by about 1-1/2 percentage points during 2013, relative to what it would have been otherwise.

Mish: It is preposterous to whine about pissy cuts in spending when the cuts have all been back-end loaded, and there are no real cuts in the first place. Congress did not really cut anything. It decreased the amount of expected budget increases and called that a cut.

Bernanke: In present circumstances, with short-term interest rates already close to zero, monetary policy does not have the capacity to fully offset an economic headwind of this magnitude.

Mish: Headwinds? From non-existent cuts? From a rollback of tax cuts that should never have happened in the first place?

Bernanke: Although near-term fiscal restraint has increased, much less has been done to address the federal government’s longer-term fiscal imbalances. Indeed, the CBO projects that, under current policies, the federal deficit and debt as a percentage of GDP will begin rising again in the latter part of this decade and move sharply upward thereafter, in large part reflecting the aging of our society and projected increases in health-care costs, along with mounting debt service payments. To promote economic growth and stability in the longer term, it will be essential for fiscal policymakers to put the federal budget on a sustainable long-run path.

Mish: Note the blatant hypocrisy of Bernanke whining about non-existent cuts and about tax rollbacks the country could not afford, while warning Congress that something must be done to put the federal budget on a sustainable long-run path.

Bernanke: Importantly, the objectives of effectively addressing longer-term fiscal imbalances and of minimizing the near-term fiscal headwinds facing the economic recovery are not incompatible. To achieve both goals simultaneously, the Congress and the Administration could consider replacing some of the near-term fiscal restraint now in law with policies that reduce the federal deficit more gradually in the near term but more substantially in the longer run.

Mish: Yeah, right. Like what? Of course that’s not his problem. He just begs Congress to kick the can down the road, which of course is all the Fed ever does too, while ignoring every asset boom-bust cycle along the way.

Bernanke: With unemployment well above normal levels and inflation subdued, fostering our congressionally mandated objectives of maximum employment and price stability requires a highly accommodative monetary policy. Normally, the Committee would provide policy accommodation by reducing its target for the federal funds rate, thus putting downward pressure on interest rates generally. However, the federal funds rate and other short-term money market rates have been close to zero since late 2008, so the Committee has had to use other policy tools. The first of these alternative tools is “forward guidance” about the FOMC’s likely future target for the federal funds rate.

Mish: Got that? Forward guidance is supposedly a tool. In reality, the Fed is totally clueless about the economy, about housing, about jobs, and about where interest rates should be (as directly evidenced by repeat bubble-blowing exercises).

Bernanke: The second policy tool now in use is large-scale purchases of longer-term Treasury securities and agency mortgage-backed securities (MBS). These purchases put downward pressure on longer-term interest rates, including mortgage rates. For some months, the FOMC has been buying longer-term Treasury securities at a pace of $45 billion per month and agency MBS at a pace of $40 billion per month. The Committee has said that it will continue its securities purchases until the outlook for the labor market has improved substantially in a context of price stability. The Committee also has stated that in determining the size, pace, and composition of its asset purchases, it will take appropriate account of the likely efficacy and costs of such purchases as well as the extent of progress toward its economic objectives.

Mish: Note the dual mandate nonsense of jobs and inflation. It is impossible for bureaucrats and central planners to target one factor of the economy accurately. Two is insane. Yet, price stability is easy enough to achieve. Simply get rid of the Fed and fractional reserve lending. Here are some links on the absurdity of dual mandates.

Bernanke: At its most recent meeting, the Committee made clear that it is prepared to increase or reduce the pace of its asset purchases to ensure that the stance of monetary policy remains appropriate as the outlook for the labor market or inflation changes.

Mish: That makes sense (in a perverse sort of way). The Fed has no idea what it is doing so it needs to be prepared to do anything. Also note the irony of being prepared to do anything while promoting “forward guidance” as a tool.

Bernanke: In the current economic environment, monetary policy is providing significant benefits. Low real interest rates have helped support spending on durable goods, such as automobiles, and also contributed significantly to the recovery in housing sales, construction, and prices. Higher prices of houses and other assets, in turn, have increased household wealth and consumer confidence, spurring consumer spending and contributing to gains in production and employment. Importantly, accommodative monetary policy has also helped to offset incipient deflationary pressures and kept inflation from falling even further below the Committee’s 2 percent longer-run objective.

Mish: What a bunch of self-serving nonsense. Higher asset prices have primarily benefited the wealthy. For discussion, please see Who Won? the 93% or the 7%? Why?

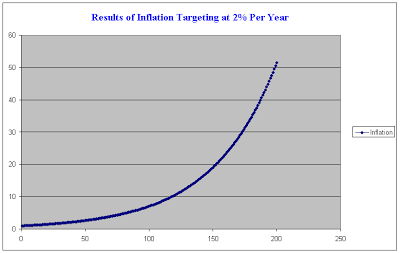

Moreover, Bernanke does not understand the simple math of 2% inflation over time. When wage growth does not keep up, and it hasn’t, huge economic distortions arise along with dependency on food stamps, disability, and other programs. In short, 2% stability, is very destabilizing. I spoke about this at length in Fallacy of Inflation Targeting.

Here is the key chart.

Over time, prices rise, but wages for the masses do not. Worse yet, Bernanke’s cheap money philosophy makes matters worse because it encourages businesses to invest in hardware and software robots that will enable companies to fire more workers.

There are no benefits of artificially low rates, at least to the average worker.

Economist Steve Keen commented on that chart in Exponential Credit Petri Dish; Steve Keen Responds to “World Economic Forum Endorses Fraud” Post

Bernanke: That said, the Committee is aware that a long period of low interest rates has costs and risks. For example, even as low interest rates have helped create jobs and supported the prices of homes and other assets, savers who rely on interest income from savings accounts or government bonds are receiving very low returns. Another cost, one that we take very seriously, is the possibility that very low interest rates, if maintained too long, could undermine financial stability. For example, investors or portfolio managers dissatisfied with low returns may “reach for yield” by taking on more credit risk, duration risk, or leverage.

Mish: The committee would not recognize risk if it jumped up and spit in Bernanke’s face. Low interest rates have already undermined future financial stability by encouraging “reach for yield” excessive credit risk, duration risk, and leverage.

Bernanke: Because only a healthy economy can deliver sustainably high real rates of return to savers and investors, the best way to achieve higher returns in the medium term and beyond is for the Federal Reserve–consistent with its congressional mandate–to provide policy accommodation as needed to foster maximum employment and price stability. Of course, we will do so with due regard for the efficacy and costs of our policy actions and in a way that is responsive to the evolution of the economic outlook.

Mish: Bernanke took one last opportunity to hide behind a ridiculous dual mandate while turning a blind eye to the destabilizing asset bubbles it creates.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

To get Mike’s Daily Economic Analysis go HERE and click on the subscribe by Email button ( top left corner)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair