Timing & trends

Billionaire George Soros’ family office hedge fund, Soros Fund Management, filed its 13F quarterly report with the Securities and Exchange Commission yesterday.

As Marketwatch reporter Barbara Kollmeyer points out, one interesting highlight from Soros’ filing is that he bought a bunch of puts on the SPDR S&P 500 ETF in Q2.

It’s his biggest holding in the filing.

During the second quarter ended June 30, Soros held 26,157 shares of SPDR S&P 500 and call options on 143,600 shares and put options on 7,802,400 shares in the ETF.”

….you can read more on the 13F filing HERE including what he held last quarter.

Ed Note: Keep in mind two things when analysing these figures. Soros also disclosed that he bought 66,800 Apple shares @ $499.23, further that 13F filings do not require the disclosure of short positions, fund managers only have to disclose their long positions.

Treasury yields are on the rise as I have noted on numerous occasions recently.

The action has prompted the world’s largest hedge-fund manager, to throw in the towel on treasuries and inflation-linked TIPS.

Ed Note: Canadian Bonds Plunge with U.S. Treasurys After Strong Data

Ed Note: Canadian Bonds Plunge with U.S. Treasurys After Strong Data

Canadian Bonds Plunge with U.S. Treasurys After Strong Data

Please consider Dalio Patched All Weather’s Rate Risk as U.S. Bonds Fell

As the bond market plunged in late June, Ray Dalio convened the clients of Bridgewater Associates LP, the world’s largest hedge-fund manager, to tell them that a fund designed to withstand a broad range of market scenarios was too vulnerable to changes in interest rates.

Bridgewater, citing months of study, said it had underestimated the interest-rate sensitivity of various assets in its All Weather fund and was taking steps to mitigate the risk, according to clients who listened to or read a transcript of the June 24 call. By the end of the month, the Westport, Connecticut-based firm had sold off enough Treasuries and inflation-linked bonds to help reduce the fund’s most rate-sensitive assets by $37 billion, according to fund documents and data provided by investors.

The move, disclosed to investors five days after the Federal Reserve said it’s prepared to phase out its unprecedented bond purchases, was unusual for the fund. As its name suggests, All Weather is designed to produce returns in most economic environments and avoid altering asset allocations when the outlook changes. All Weather incurred a second-quarter loss of 8.4 percent that was primarily tied to its $56 billion portfolio of inflation-linked debt, said the clients, who asked not to be named because the fund is private. ‘A Foretaste’

The decline at All Weather and similar funds, including those run by Cliff Asness’s AQR Capital Management LLC and Invesco Ltd. (IVZ), shows Bridgewater’s pioneering strategy for allocating assets between stocks and bonds, known as risk parity, can leave investors overexposed to rising interest rates. The losses were amplified for some funds by a selloff in inflation-linked securities that also caught Bill Gross’s $262 billion Pimco Total Return Fund (PTTRX) off guard.

“This is just a foretaste of what is going to happen,” said Ramin Nakisa, a global asset-allocation strategist at UBS Investment Bank who co-wrote a March research report titled “When Risk Parity Goes Wrong.” Nakisa called June’s selloff in Treasuries and inflation-linked bonds “a dress rehearsal” for the volatility awaiting when the U.S. Federal Reserve actually begins to taper its bond-buying program, known as quantitative easing.

All Weather trimmed its use of leverage to about 144 percent of net assets at the end of June, according to the clients who requested anonymity. Gross exposures to different asset classes declined to about $116 billion from $138 billion in the quarter, while net assets stayed at $80 billion.

Reflections on Leverage

Lovely. All Weather now has a mere 144 percent leverage? What happens if stocks, bonds, and commodities all take a dive?

Here’s the deal: This selloff in treasuries may be over. Or it may not be. Anyone who thinks they know is fooling themselves.

What I do know is leverage works both ways. I also know that the Fed has so distorted the economic horizon that it is next to impossible to predict what’s coming down the pike.

Stocks, bonds, and commodities other than gold all rose in union over the past few years. My bet is on an unwinding of that trade.

I see no value in treasuries, no value in corporate bonds, no value in equities, and no value in municipal bonds.

I do see value in gold, so that is where I am. Without leverage. Patiently waiting.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

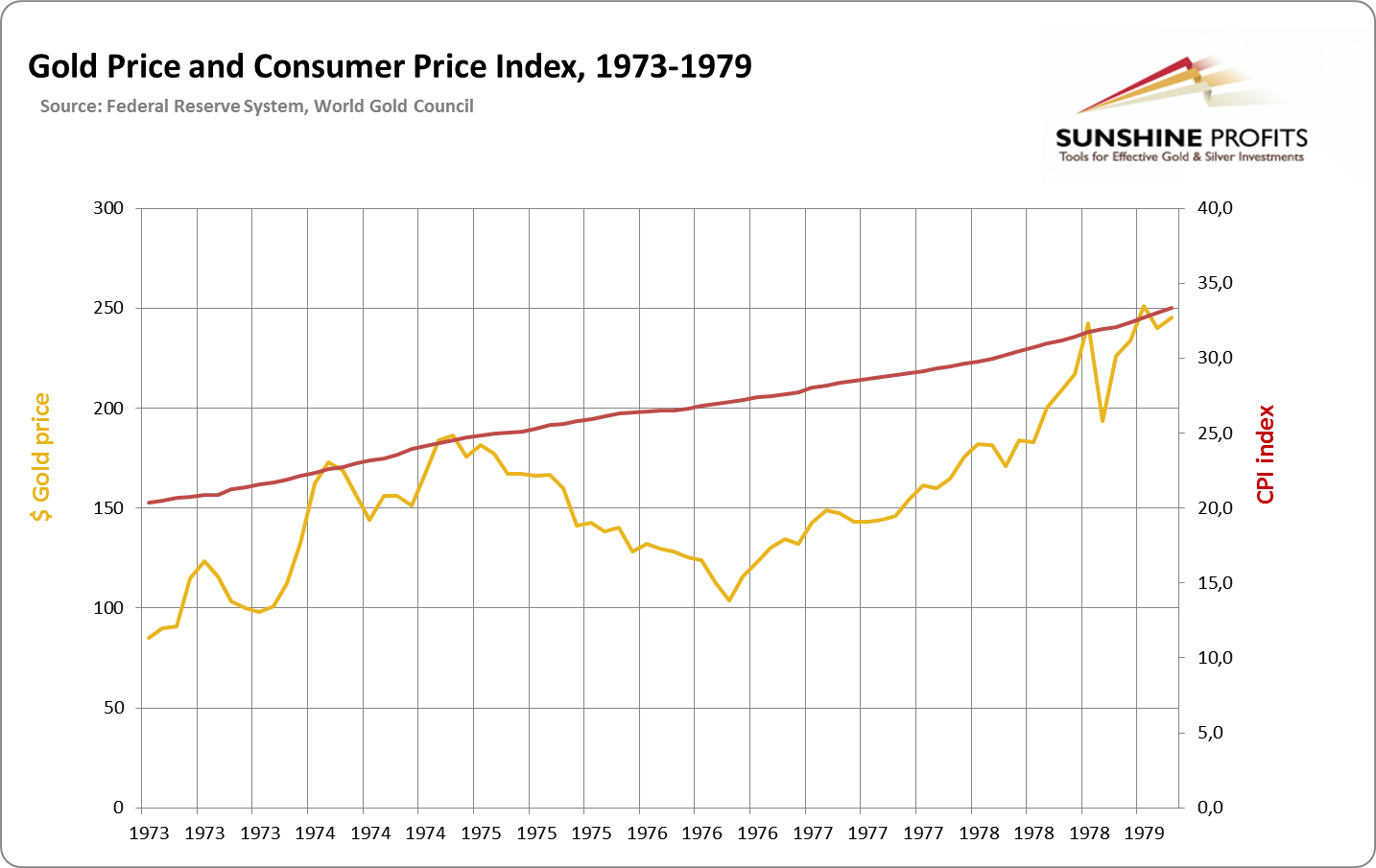

Last week we focused on the idea that gold is not an inflation hedge. Today, we will develop this notion even further. If we’re talking about gold as a hedge, it is rather a system-hedge than an inflation-hedge. Since 1973, when the dollar was allowed to float, gold has confirmed this view.

When it is wanted as a dollar alternative, the price of gold goes up. This takes place when the trust in the dollar plummets, or actually when the trust in the dollar-dominated-system plummets. Gold rose during the end of the 1970s because of expressively high inflation. But it was not only inflation that was decisive. This high inflation led to distrust in the dollar, therefore, gold became the alternative. The general trend of gold looks a lot like increasing CPI:

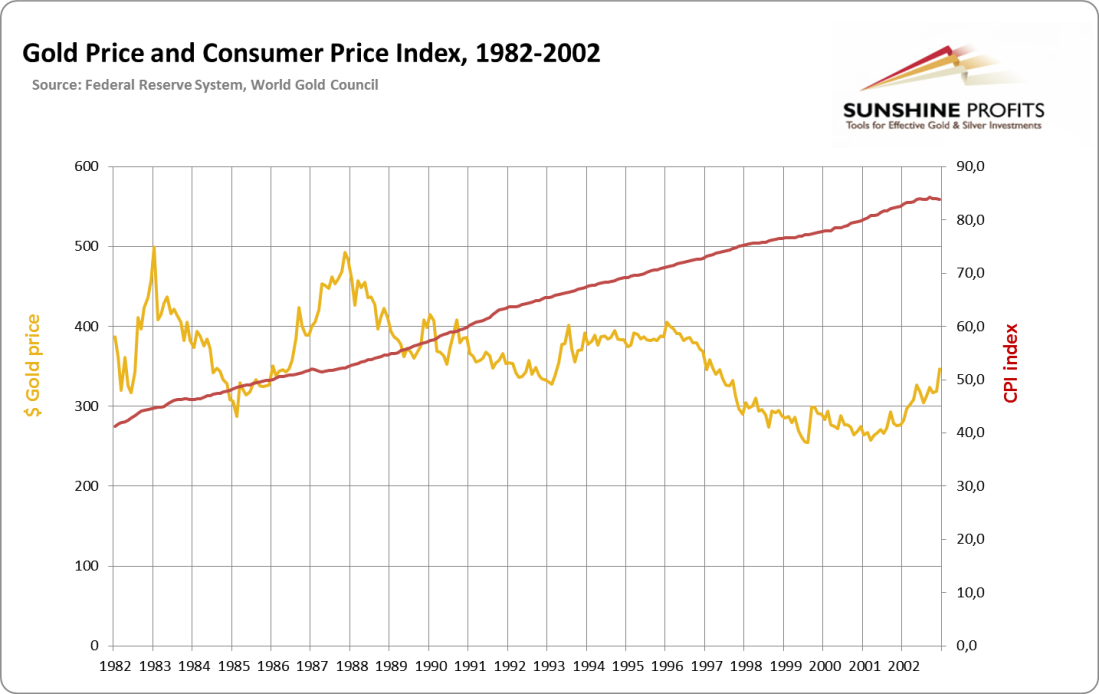

After the 1980s recession and end of the short-lived gold bubble Volcker tamed the dollar, which renew trust in it. The next 20 years were times of a noticeably strong dollar and stronger faith in this paper money. The conditions also paved the way for enormous increases in debt of the economy, which transformed the United States into the greatest debtor in the history of human civilization. During that time despite positive inflation gold was dropped as a “currency alternative”, therefore lost its value. The dollar was drained by mild inflationary forces; gold did not keep the pace and went down:

With oversupply of US dollars, the credit situation was reversed in the 21st century. Over indebtedness in the American economy has shaken the trust in the dollar-dominated system (especially due to agency debt and private debt). As Paul Samuelson called it, the “run on dollar” was triggered from 2001. This was visible in the decline of the dollar against other currencies, and also gold became a reliable alternative. The pace of inflation was overall no more impressive than it was for the previous 20 years. Yet suddenly the relation between gold and dollar had shifted, and the price of gold grew at a much higher pace than the dollar was losing value. Why? Because of the system dynamics and lowered trust in the dollar.

In any case gold is not really an inflation-hedge. It is a special investment vehicle that requires careful focus and analysis separate from only inflationary forces. Those forces no doubt affect the gold market. But not in a way many people often suggest, and in a way which may lead to misplaced investments.

The above is a small excerpt from our latest Market Overview report. The full version includes much more in-depth analysis of this and other fundamental factors that are likely to affect the gold market in the near future. You can sign up for these reports here.

Thank you.

Matt Machaj, PhD

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Matt Machaj, PhD and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Matt Machaj, PhD and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Matt Machaj, PhD is not a Registered Securities Advisor. By reading Matt Machaj’s, PhD reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Matt Machaj, PhD, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

…..most investors never learn.

From Louis James, Chief Metals & Mining Investment Strategist, Casey Research:

I’ve always wondered why we tend to glorify pirates and treasure hunters: the Indiana Joneses, the Jack Sparrows, the Long John Silvers. I think it’s because most people, while it may not be reflected in their daily lives, are adventurers at heart.

Don’t we all dream of digging a hole because we just know there’s something there, and hearing that telltale clunk of our spade striking the lid of a treasure chest filled with gold doubloons?

Fact is, the precious metals mining sector — although by many derided, as Doug Casey says, as a “choo-choo” industry — is one of the last bastions where wannabe daredevils can still dream big…

Most of the companies my subscribers and I invest in are explorers looking for gold, silver, and other metals.

Of course today there’s a lot of science involved in finding those modern treasure troves.That includes the latest technologies, like XRF guns, to assay rock samples right in the field.

And some geologists just have that spot-on intuition about how mineralization twists, turns, plunges, thickens, pinches out, breaks off, and reappears.

However, we can’t — and shouldn’t — underestimate the role of luck in every discovery.

Mother Nature likes to hide her treasures well, plant false clues, and bury them deep. That’s what makes the treasure hunt so exciting, difficult, and ultimately (when successful) profitable.

Here’s a secret that most mainstream investors don’t know: There are literally thousands of mineral exploration companies, and…

More on gold stocks:

Where resource master Rick Rule is finding great value now

Incredible chart may have called the exact bottom in gold stocks

This could be “the most undervalued sector” in the entire stock market today

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair