Gold & Precious Metals

WE SAW EXPECTED DOWNSIDE FOLLOW-THROUGH ON MONDAY, BUT VOLUME DECLINED AND TODAY IS A POTENTIAL ‘TURNAROUND TUESDAY’. CAUTION FLAGS ARE STILL RAISED THAT A MORE SERIOUS SETBACK COULD BE UNFOLDING. AFTERALL, THE LAST TIME I LOOKED AT THE CALENDAR IT WAS STILL SEPTEMBER AND OCTOBER LOOMS AROUND THE CORNER. BUT, BEARS HAVE TO BE WATCHFUL THAT THE WHITE KNIGHT (BERNANKE) WILL COME TO THE BULLS RESCUE. THE BIG ISSUE IS WITH THE BANKS – THE REASON I BELIEVE TAPERING WAS NOT INSTITUTED LAST WEEK, I.E., THE BANKS ARE IN TROUBLE AND THE FACT THE FED HAS LOST CONTROL OF LONG INTEREST RATES. DON’T BE SURPRISED TO SEE TAPERING INCREASE FROM $85 BILLION TO $100 BILLION OR MORE TO KEEP EQUITY MARKETS FROM DECLINING AND TO KEEP LONG BOND PRICES FROM DECLINING FURTHER.

———————————————

The S&P 500 was down 8.07 at 1701.84 touching 1697.10 intraday. It traded at a new bull market high of 1729.86 on Thursday. Risk is down to the 50 day moving average at 1678.00. A bigger sell-off would find support at 1627, 1610 and then 1550. When and if we clear 1729.86, look for 1757.00 and even possibly 1807.00.

——————————————–

The TSX was down 120.31 at 12806.47. Resistance is at the 12889.26 peak from back on May 22. Above there we could theoretically see 13370.00. Should we break below 11759.04 (the June 24 low) look for 11,400.

——————————————–

The TSX Venture was down 6.78 at 946.10. Next resistance is 971.96 then 1017.59. A double-bottom formed comparing the 859.31 low from June 27 to the July 9 low of 873.05. Under those lows, look for support at 830.00 and 780.00 on the way down

METALS – AS I WARNED, LAST WEDNESDAY’S BIG UPSIDE ‘KEY REVERSAL’ COULD HAVE BEEN NOTHING MORE THAN JUST ANOTHER ‘DEAD CAT’ BOUNCE. IF, HOWEVER, IF WE CAN CLEAR THURSDAY’S HIGHS, E.G., 1374.77, WE COULD BE ‘COOKING WITH GAS’. WE JUST HAVE TO WAIT AND SEE. THE SAME APPLIES FOR THE MINING SHARES. THE NEXT BIG UPSIDE BARRIER ARE THE AUGUST 27 HIGHS. IF, HOWEVER, WE BREAK UNDER WEDNESDAY’S LOWS, E.G., 1295 IN SPOT GOLD, WATCH OUT BELOW, WE COULD BE HEADED TO 1000 -NOT THE DESIRE RESULT, UNLESS, OF COURSE, YOU ARE SHORT. AT THE MOMENT, THAT APPEARS TO BE THE MORE VIABLE STRATEGY. FOR THE MIINERS, WATHC THE PHLX XAU INDEX UNDER 88.29 OR 82.28.

———————————————

Spot Gold was down 1.76 at 1319.27. Gold touched 1295.15 intraday last Wednesday forming a ‘key reversal’ day to the upside, but ran into a stone wall at Thursday’s high of 1374.77. The recent high is 1432.38 from August 28. To date, the big, big low (as compared to the record high of 1922 from September, 2011) was formed on June 28 at 1186.40.

———————————————

Spot Silver was up .17 at 21.69. Last Wednesday’s low at 21.23 is still being tested with 20.61 and 18.31 next support. Downside risk is to 13.00 if these levels are violated. We need to clear 23.90 and 25.07 to begin talking about the resumption of the uptrend.

The 2013 Annual Forecast Model is now on-line. SUBSCRIBE NOW! It is a premium report.

If you call my office by Thursday of this week and leave your name and number, you will be entitled to receive a 50% discount on this valuable report. If you wish to order from the internet and pay full price, here is the link:

https://www.vrtrader.com/subscribe/index.asp

The Annual Forecast Model (The VR Forecaster Report) is published each and every year in early February and comprises Mark Leibovit’s proprietary cyclical forecast for the Dow Industrials and Gold. Don’t miss the opportunity to see this Report that projects market direction and/or important cyclical change points months in advance. We have called it our ‘Blueprint to the Future’. Unique to Mark Leibovit it has been published since the mid 1980s. Access to the report is provided via the website using the username and password provided to you.

About Mark Leibovit

Mark Leibovit is Chief Market Strategist and Publisher for the VRTrader.com -“Tools for the High Performance Trader”, the Leibovit VR Gold Letter and the author of ‘The Trader’s Book of Volume’ which was published in 2011 by McGraw-Hill. You may have recognized Mark as one of the ten “Elves” on Louis Rukeyser’s Wall Street Week television program where he served as a weekly consultant for 7 years and also as a regular Market Monitor guest for the past 30 years on PBS’ The Nightly Business Report. He is a popular speaker at investment conferences both in the U.S. and Canada and is often seen on PBS, BNN and FOX Business News. TIMER DIGEST Magazine has named him the #1 Gold Timer for the twelve-month period from 8/26/10 to 8/26/11 and the #2 for 2011 He was also named the #1 Intermediate Market Timer for the 10-year period ending in 2007. Mr. Leibovit was a member of the Chicago Board Options Exchange where he became a market maker in several stocks including Newmont Mining. Through the late 1980s he was Technical Research Director for Rodman & Renshaw and subsequently began publishing several financial newsletters. He holds a CIMA and AIF designation and is a member of the Market Technicians Association (MTA) and the CFA Institute.

——————————————–

What is a Leibovit Volume Reversal (VR)?

A Leibovit Volume Reversal ™ is a change from a Rally day to a Reaction day accompanied by a increase of volume or a change from a Reaction day to Rally day accompanied by an increase in volume.

Leibovit Volume Reversals ™ coming off intermediate lows or highs have greater significance in helping to define those lows or highs and important pivot points in the marketplace. MEANWHILE, THEY ARE GENERALLY TRADEABLE FOR UP TO TWO DAY MOVES IN THE DIRECTION OF THE VOLUME REVERSAL.

Use the following link to sign up:

http://www.metastock.com/products/thirdparty/?3PC-ADD-VRIS

Mark Leibovit – Metastock Webinar – April 30, 2012. Here’s your chance to learn more about the proprietary Leibovit Volume Reversal indicator and strategy.

Link below:

The Volume Reversal ™ is a registered trademark and can only be used or quoted after receiving express written permission from VRTrader.com and Mark Leibovit.

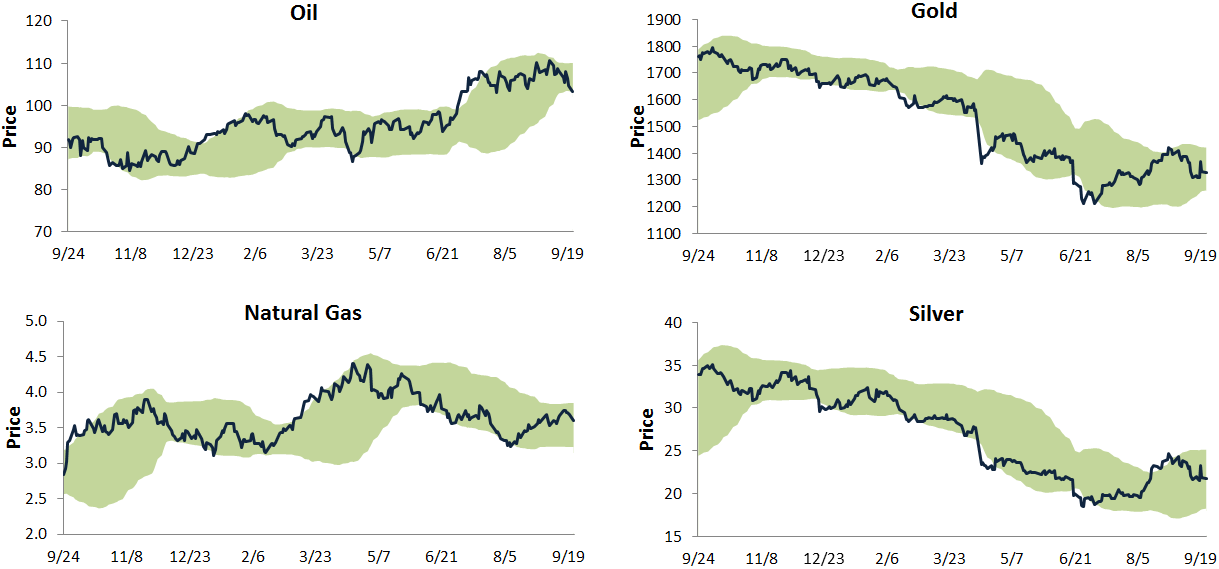

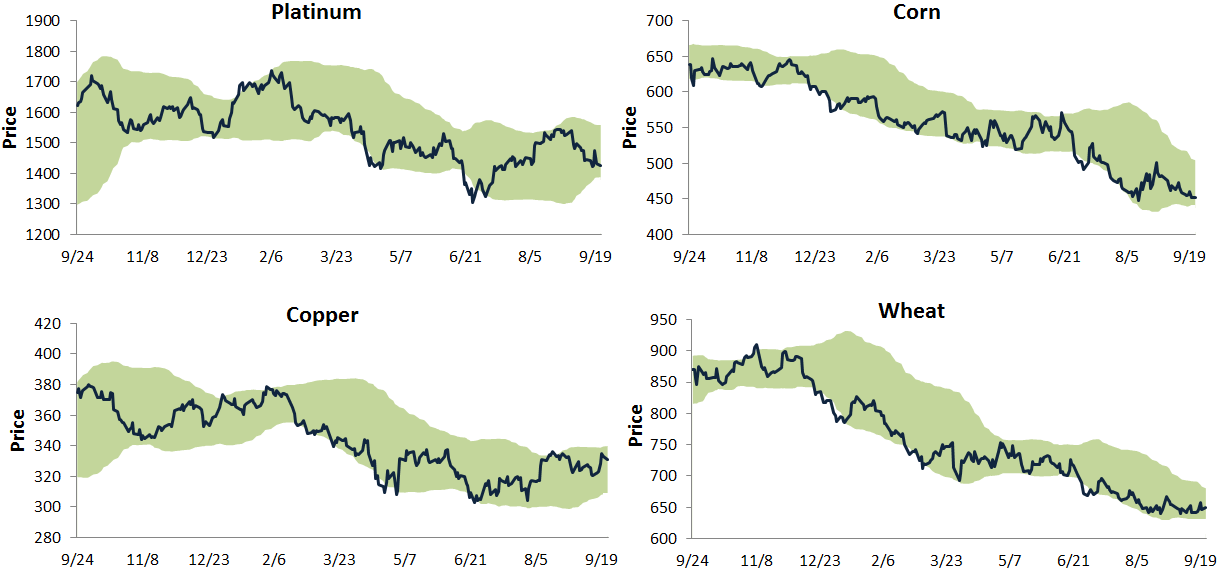

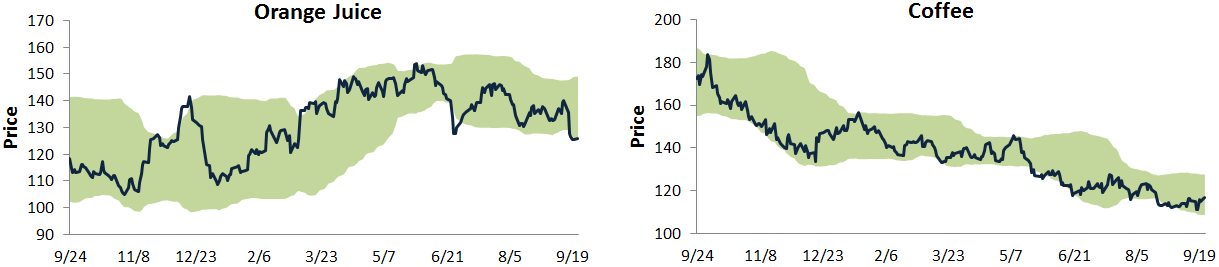

Below is an updated look at our trading range charts for ten major commodities. In each chart, the green shading represents between two standard deviations above and below the commodity’s 50-day moving average. Moves above or below the green zone are considered overbought or oversold.

Nine of the ten commodities shown have been in downtrends for quite awhile now, and oil — which had been in an uptrend — looks like it could join them soon with its most recent break down. The metals looked like they might be able to break out of their downtrends a couple of weeks ago, but they have pulled back recently. Corn, orange juice, wheat and coffee are all at the bottom of their trading ranges with not much upside in sight. It has been a rough year for the commodities asset class. Until these downtrends get convincingly broken, it’s going to be hard for portfolio managers to increase their allocations.

S&P 500 Percentage of Stocks Above 50-Day Moving Averages

The S&P 500 has pulled back about 1.5% from its all-time closing high last Wednesday. Below is a chart showing the daily percentage of stocks in the index trading above their 50-day moving averages over the last year. As shown, the reading is currently at 66%, but what’s telling is the fact that we’ve seen lower highs in the reading each successive time it has peaked so far this year. This means that participation by individual stocks has been dwindling as new market highs have been made. You’ve probably heard that this has become more and more of a “stock picker’s market,” and this chart bears this out.

….read & view more HERE

About Bespoke Investment Group

James Dines is one of the godfathers a technical analysis, the original gold bug, author of one of the real bibles of investment called “Mass Psychology”, and he is a specialist in Super-Major Bull Markets. This is a word for word transcript of the interview Michael did with James that can be listened to HERE if you prefer

James Dines is one of the godfathers a technical analysis, the original gold bug, author of one of the real bibles of investment called “Mass Psychology”, and he is a specialist in Super-Major Bull Markets. This is a word for word transcript of the interview Michael did with James that can be listened to HERE if you prefer

Michael Campbell: I’m talking with James Dines who is also the author of the book Gold Bug, a great book if you want to understand the gold market and the relationship with things like the central bank’s printing of money. James also wrote Mass Psychology, a book I recommended it to my children, if they wanted to understand the market. They all have, I might add, bought copies and read that book.

Jim, let me just fire some questions at you as I want to make best use of this opportunity. Let’s start with the positive market reaction to the extension of QE3 on Wednesday into Thursday. Then Friday it gave up most to the gains. What do you think are the consequences of the Federal Reserve’s decision for the stock market short term and longer term?

James Dines: Listen, the central policy of the world’s Fed’s is to overspend, get deeper in debt and print money like mad with no relationship to work except printing it. Then they expect prosperity. In the last six years alone debt has nearly doubled in america from 9 trillion to 17 trillion dollars with no plan to pay it back because there is no hope of paying it back. So they hide behind these codes like QE1, QE2, QE3 & Taper. Its double-talk, all it means is getting deeper into debt that cannot be repaid and won’t be.

This can’t be a valid Road to to a long-term recovery. QE1 and QE2 didn’t work, why should QE3 work any better? We are in a six-year recession and I think its the coming Great Depression that I have been warning about that is papered over by money. This can’t be a valid road. I’ve never met anyone who’s who’s gotten rich guessing what the Fed is going to do. To the contrary, when the Fed surprised everybody on Wednesday and people jumped in I was selling into it, doing the opposite.

To continue this thought, try to realize that this whole thing about the Fed is a mistake. They should not be printing they should be paying off some of this debt. How can you be optimistic that they’re postponing printing when the reason for it is that the economy is not doing well. Shouldn’t the market go down if the economy is still not recovering after six years.

Campbell: You wrote in early September in your Interim Warning Bulletin that you thought that gold and silver were going to pull back, which they did. Then we get the extension of QE3 announcement on Wednesday and Gold and Silver have a quick sharp move up followed by a pull back on Friday. What do you see for gold and silver at this point?

Dines: The long-term view of gold and silver is that the more money they print the more pieces of paper will be chasing it. Therefore there is no question that Gold and Silver prices are going up over the long term. I have been saying this since Gold was 35 Dollars and Silver was 92.5 Cents. They have to go up. Gold almost got up to $2,000 recently so you have to keep the long-term framework in mind.

Second of all, Gold and Silver a very emotional investments. They tend to attract mass psychological swings and trying to look at day to day movements is a mistake. We recently got off our sell signal on Gold and now we are bullish on it. I think you’re going to see a rise starting as soon as this October. I think that if you just hold some Gold coins and hold some good Gold stocks that you’ll wind up profiting in the end. I remember we recommended this Silver stock that sold for a dollar a share, Industrias Penoles. It got up to $50.00 recently. All you have to do is just hold it.

Campbell: There certainly has been a disconnect between gold bullion and gold stocks in that Gold had a a decline but the stocks did far worse. Is it time to accumulate quality gold stocks, or are you waiting until October? =

Dines: On a short term basis I think they are going to come down a bit more. But they should be hitting bottom sometime within coming weeks and I’m looking to flash and interim warning bulletin. There is a difference between gold bullion and gold stocks and the difference is this: Gold is already above the ground, you’re buying it, you’re getting it and that’s where it is. It won’t move as quickly as a stocks or as much in percentage terms because stocks are more leveraged. Stocks have other factors. Governments can raise taxes on them, or steal them. They call that nationalizing. Or they can run out or ore. All kinds of things can happen to a Gold mine and because of that level of uncertainty they don’t do as well.

There’s an even deeper motive, look I remember when they said that are you couldn’t mine gold unless it had at least one percent Gold. That was the limit, under one percent they said the mine would close. Now it’s down to one gram. In other words you move a ton of earth to get a paperclips worth of gold for which you’ve got to use chemicals , labor, fuel, pay taxes and everything else to recover. At some point we are going to run out of mineable gold. What’s the limit, a half a gram, a quarter, a tenth a gram,? We are actually facing the limit of gold mining and we’ll see it in our lifetimes. This planet has been scoured for gold since humanity began and at some point you run out, there is just not an infinite amount of gold.

The age of Gold mining is ending and that’s when Gold prices will go to my long-term targets of $3000 to $5000 an ounce. I have been saying that since Gold was $35. and let me tell you something, it’s going to happen.

Campbell: Turning to China, avert being bullish on China since 1979 wo years ago you turned bearish on China. Great call on being bearish on China, but I sense that maybe again you’re now seeing some more positive signs. Can you to comment on that?

Dines: Well we specialize in what I call Super Major Bull markets, that’s where serious money is being made and that’s the important way, I think, instead of day trading to make money. To get in early into a new bull market and make money, and China was one of them.

With China you’re right, the minute Mao died I flew over to China to see for myself and I came out wide-eyed. I said this is going to be the biggest thing I’ve ever seen and I actually predicted that China would dominate the financial world in the 21st century. People got apoplectic when I said that but I had the guts to stand my ground. It was what I call a screaming bull market and these China’s stocks were absolutely the place to be. Two years ago everybody began to agree with me and everybody assumed it was going to grow and grow. That’s the mass psychology you have to avoid, you need to go opposite to the crowd to make money. It’s not easy to do because we are programmed to listen to the people around us, or influenced by it. Indeed the Chinese market had a serious crash, a lot of stocks went down. Recently I’ve been recommending China stocks and they’ve been doing fantastically well. though you have to be in the right ones.

Let me go back to the other super major bull market. In 1994, including on your show Mike, I talked about the coming boom in a new area call the Internet. Most people didn’t even know what it was then and in the next five years we made absolute killings in those things. We got out of them in 2000 fortunately. Now we’re getting into a new phase of the Internet. This phase is going to be anything involved with restructuring industries. The Chinese are doing it, but we’re doing it here also and this is a red-hot bull market going on right now. ddTake for example Twitter, or Linkden that is redefining the method of employment, or Amazon that is redefining bookstores out of existence with the Kindle. Whole industries are being restructured.

To me the next big one, and it’s both in the US and China, is something that is transnational. I’m not sure how many you have in the Canadian market, but in the year 1994 I said would be the biggest invention since the 15th Century Gutenberg Printing Press. I’m announcing this on your show as a new aspect of the internet and I’m calling myself the original restructuring bug, redefining every business. Yelp for example made the Yellowpages obsolete. Twitter, Google or Facebook we’ve been focusing on which one would, believe it or not, restructure manufacturing.

Its going to be 3D Printing. You can imagine needing to buy a scissors or a screwdriver but instead of going shopping you press a button on your desktop 3D Printer and it appears the next morning in the exact color, shape or sharpness you want. Imagine printing many things as well as what bringing manufacturing into your into our homes will mean to the world. Plus the plunge in manufacturing jobs that’s going to follow.

This is not a dream for the future you know, right now you can buy a 3D printer on Amazon and a guitar has been made from it. Somebody actually printed a gun that fired a bullet, Boeing is already making plane and they’ve even tested a rocket fuel injection nozzle.

I see another industrial revolution bigger than the Internet. It’s going to transform manufacturing from factories to the residence. If you if you have a a vehicle with the discontinued part you can just have it printed on your own layer by layer, atom by atom overnight. It can be done with plastic but also with metals. It’s going to redefine medicine, dentistry by printing orthodontists tooth braces, hearing aids are already being fitted precisely to the shape of the inner ear. Body parts like a prosthetic limbs. Somebody gets a jaw shot off in wartime they can just build a new jaw and then they can even spray cells onto it to become skin.

This is the biggest thing I’ve seen, much bigger than China and and I’m very excited about it because as I said you get a machine from Amazon for $1,300 and that is going to come down over time. Now it’s plastic but later going to be bronze, carbon fiber, ceramic cellulose, even food.

Campbell: Its interesting when you say this is restructuring. I think everyone’s familiar with Amazon and how it’s redefined the book business and how iTunes did the same for the music business. Now you say there is more coming with Linkedin etcetera. How do we take advantage of those? Its not easy as you could have bought a lot of bad internet stocks. What is the key thing you say to keep in mind if I want to invest in the restructuring trend?

Dines: I would say that the single most important factor in picking these stocks is people, the management. Many are called but few are chosen, and with all due respect Lincoln was wrong. We are not all created equal. There are some like Jeff Bezos who created Amazon despite being scorned by Barron’s and everybody else. Or the genius who founded Tesla.

Campbell: You mentioned you might tell us about a stock.

Dines: I’ve never mentioned a stock on your show before in all the years I’ve been on it. It is easy for anyone to find this stock, it is the blue chip of the group. There are four on our list now and they range in price from $50.00 to $5:00 dollars and the blue-chip is the one that I’m going to mention. The name of the Stock is 3D Systems and this is going to be the one they’ll eventually be focusing on when people come storming into this group looking for stuff to buy.

I am going to be focusing on this group very intensely and actually have been for some time. We’ve even got our own average of 3D stocks and nobody else that I know about has one.

Campbell: Before I let you go we’ve talked about China and some of these changes longer-term. Just in general what is your view on the commodity complex right now? Is the is a commodity bull market over, it certainly is taking a breather here and it’s been in corrective mode.

Dines: China I knew would be building its infrastructure so I was very bullish on commodities. They are the world’s largest consumer of commodities and we made a great deal of money in 2009 -10. In the last two years, 2011-12, we’ve had a crash in the whole commodities markets. Everything came down, even rare earths and Gold. I think thats ending, I think china is going to be recovering here. They still have a real estate crash ahead of them coming, but basically I’m looking for recovery in the entire market. In fact in next week’s letter you’ll see our charts of some of the commodity stocks that have already begun to turn up. Very slowly, very quietly the number of new lows made in the Canadian markets in mining stocks is diminishing and I think you’re going to see a very surprising jump in this group.

Campbell: Let me just finish with this question. You also were on top of that uranium market when it was eight dollars a pound. It then went up to a hundred and forty six dollars, and has since retreated. We now have Japan talking about eliminating all Nuclear Power, what’s your outlook for uranium?

Dines: Uranium is a very emotional metal. The truth is that we’ve got global warming and this is the only really clean and largely available energy source on the planet. There is a problem with waste disposal but that’ll have to be solved.

A lot of countries are are saying they will not use it such as Germany and Japan, but they’re already beginning to try to replace it with wind power wind which is not enough. They’re also trying to replace it with buying oil in the open market which they can’t afford. The Japanese are already groaning about the much higher electricity bills I and my prediction since Fukushima was that they would go back to nuclear power. Don’t forget Fukushima occurred not because of the plant, it occurred because they were too stingy to put a high enough wall up in front of it to prevent against a tsunami. That’s what caused the trouble.

You know location is everything and you must you must take Nuclear Power seriously. It’s as dangerous as fire and electricity and we had to learn the hard way with those also. We need to avoid earthquake zones, you need to be protected from natural disasters, and then you have a great source of energy. It must be done intelligently and taken seriously and not be done by stingy people who are trying to save some money on a wall. Look what that has cost them.

Campbell: Great stuff Jim, I am so appreciative you of finding time for us on this show and our audience across the country. For all the years, I very much enjoyed today. Thank you.

Dines: Anytime for you Mike. You are a great reporter and Canada is very lucky to have you.

You can reach the Dines Letter at http://www.dinesletter.com

The call for this week: As expected, Bernanke did not taper last week. As not expected, most of the major market indices I monitor made new all-time highs, rendering another Dow Theory “buy signal.” However, last Wednesday’s upside explosion looked conspicuously like a short-covering, upside, exhaustion rally. That view was reinforced by the relatively quick “giveback” of Thursday/Friday. As stated, typically after a huge momentum move, like Wednesday’s “no taper” rally, the equity markets will trade sideways for a few days. That just didn’t happen as the S&P 500 pulled right back to its previous intraday high of 1709.67 (August 2, 2013). Historically, there is evidence that when you get a momentum move like last Wednesday’s, which is followed by a closing price below a previous high, it has resulted in more of a pullback. Therefore, it will be interesting to see how the SPX reacts off of the August 2nd pivot point of 1709.67 this week.

Brent Woyat, Portfolio Manager, CIM, CMT

brent.woyat@raymondjames.ca

www.ofip.ca

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair