Energy & Commodities

The stubborn spot price of uranium has frustrated market watchers for the past year. But that’s not the whole story. As most long-term contracts have been made at higher prices, astute investors have been slowly moving into the stocks of uranium producers and explorers in anticipation of the delayed commodity price move expected in 2014. In this interview with The Energy Report, Cantor Fitzgerald Canada Metals and Mining Analyst Rob Chang explains what lies ahead and how the turnaround in the uranium market will benefit the companies he thinks investors should focus on for maximum profits.

The stubborn spot price of uranium has frustrated market watchers for the past year. But that’s not the whole story. As most long-term contracts have been made at higher prices, astute investors have been slowly moving into the stocks of uranium producers and explorers in anticipation of the delayed commodity price move expected in 2014. In this interview with The Energy Report, Cantor Fitzgerald Canada Metals and Mining Analyst Rob Chang explains what lies ahead and how the turnaround in the uranium market will benefit the companies he thinks investors should focus on for maximum profits.

The Energy Report: During your last interview in January, you, along with many analysts, were expecting that 2013 was going to be the turnaround year for the uranium market. With the current price hovering around $35 per pound ($35/lb), what’s it going to take to get this market moving?

Rob Chang: The uranium spot price has not moved as quickly as we were forecasting. However, uranium equities have shown some strength over the past year or so, as investors started buying ahead of the uranium spot price moving. Spot prices depend more on utilities and their short-term requirements, which translates into their activity in the spot market. However the spot market accounts for a small portion of the total market. Most transactions occur in the long-term prices, and the long-term contract price is at a healthier level in the $50/lb range. We believe the uranium spot price is currently below the marginal cost of production and therefore unsustainable, as half the producers around the world are losing money.

What’s really going to drive the price higher is utility demand. Most utilities will go back into the market at some point to buy more material. We expect that will happen later this year or early next year. For this year, we’re forecasting roughly flat to slightly higher prices if buying activity does heat up, and a much higher price next year, starting in Q1/14 or Q2/14, depending on how quickly utilities move. We are very bullish and forecasting an average 2014 uranium spot price of $49.50/lb. Investors primarily focus on spot prices, but they really should be looking at the long-term price instead.

TER: On August 21, the Russians made their final shipment of LEU (low enriched uranium) under the Megatons to Megawatts HEU Agreement. This was one of the milestones many were looking for as a positive market catalyst. Is this going to help the market?

RC: This eventuality has been baked in for four or five years now, but the generalist investors who don’t focus on resources may see this as an important milestone and start looking at uranium.

TER: What other market developments have you seen since we last spoke that give you hope for salvaging 2013 as a turnaround year for uranium? Or are we now looking forward to 2014?

RC: 2014 is really when we’ll start seeing some meaningful developments that would move the market, barring an earlier-than-expected announcement from the Japanese government. Since we last chatted, the Japanese government’s Nuclear Regulatory Agency (NRA) has been established and is evaluating applications for 10–12 reactors to be turned on, or at least being approved by this year. We would be surprised to see any this year and at most we think up to three might be turned on this year. We think the majority of the restarts are really going to happen next year. Our forecast is that of the 50 reactors in Japan, about two thirds, will be turned back on at some point over the next two or three years. That’s certainly going to be a positive catalyst.

I don’t see any other major catalysts on the horizon between now and then. The equity markets generally lead the fundamental supply and demand numbers, and we’ve seen some opportunistic investors start to pick away and show some interest in the space. So in the last few months of this year, we do expect the equities to start leading the way prior to the uranium spot price actually moving.

TER: How about the situation in China?

RC: China has the largest nuclear buildup program in progress right now. Russia also has very extensive plans to build more reactors. The United Arab Emirates (UAE) has plans for building nuclear reactors, which sends an important signal to the market. As one of the most oil-rich countries in the world, it could probably power itself with oil, yet is looking to diversify into nuclear. I think that’s a fantastic sign. So we certainly are looking forward to seeing developments.

TER: What do you see going on with specific companies that might create some activity in the stocks?

RC: Starting off at the top with the largest publicly traded company, Cameco Corp. (CCO:TSX; CCJ:NYSE)is putting Cigar Lake into production. Several years ago we were wondering whether Cigar Lake would even start, and now it’s in the early stages of going. Cigar Lake has a major impact on future supply. With the HEU Agreement coming off, one of the new projects that was supposed to make up the difference is Cigar Lake. How well Cameco can ramp up production will be a very key topic for us, but we are still very bullish on the company. We do cover the stock with a Buy recommendation and we use a conservative 14x forward cash flow multiple to arrive at our $26.50 target price. Historically, Cameco has traded at 15x cash flow. Once there is interest returning to the uranium space, we believe Cameco will probably trade at its historical multiple, pricing it closer to the $30 range.

Another investment that we are bullish on is Uranium Participation Corp. (U:TSX), which is more of an investment portfolio that holds physical U3O8 and UF6. This gives investors full exposure to the commodity without any of the possible operational or geopolitical risks associated with miners. So we are very positive on that and do note that it’s currently trading around par to its net asset value. Historically, it has traded at a slight premium, given that investors tend to buy the portfolio in advance of expected increases in the spot price.

Moving to the explorers, outside of Cameco and AREVA (AREVA:EPA), the next impressive land package in the Athabasca is held by Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT). Its high grade Phoenix discovery at its Wheeler River project is arguably the highest grade uranium project in the world, and has every indication of becoming a world class project. On top of that, it also either owns entirely, or has significant pieces of assets surrounding Rio Tinto Plc’s (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK)Roughrider project, for which it acquired Hathor Exploration Ltd. in a battle with Cameco.

If Rio Tinto is going to make a go of it in the Athabasca Basin, it probably needs to expand its footprint there because Roughrider’s 70+ million pounds (7+ Mlb) is not large enough to move the needle for a company of its size. Including the mineralization and resources surrounding Hathor, you’re probably in the 100–130 Mlb range with growth potential. If Rio Tinto is to be aggressive in this space, it would probably have to buy Denison to consolidate its position in the basin. It also has valuable mill access. Cameco is already the juggernaut in the region and could opt to consolidate its land position in the Athabasca and, if it wanted to make a strategic move, push Rio Tinto out. If Roughrider is not large enough to be economic, and if Cameco ties up everything around it, Rio Tinto could decide to pack up and leave.

TER: What about some of the smaller players?

RC: Ur-Energy Inc. (URE:TSX; URG:NYSE.MKT) is a company that just started production. We visited its Lost Creek mine and were very impressed with what we saw. It has a management team from large world-class producers, bringing the best of all worlds into one project. Reaching producer status should provide a valuation bump, especially since it’s a low cost, in situ recovery (ISR) operation in the U.S. Given that the U.S. requires about 50 Mlb of uranium and only produces 5 Mlb domestically, any incremental production in the U.S. should be valued at a premium in light of domestic security-of-supply considerations. Ur Energy is a very attractive company.

Another U.S. producer we’re following is Uranium Energy Corp. (UEC:NYSE.MKT). Although we do not cover it, we do note that it is a low-cost ISR producer in Texas and believe that it should deserve a premium pricing for the same reasons as Ur-Energy.

We also cover Energy Fuels Inc. (EFR:TSX; EFRFF:OTCQX), which is the second largest producer of uranium in the U.S. and probably has the best story leveraged to the uranium price. It currently produces only about 1 Mlb/year, by design, with several mines that can be turned on relatively quickly. We estimate that it could quickly turn on anywhere between 2–5 Mlb more in annual production once prices get to attractive levels. On top of that, it also has the White Mesa mill that it acquired from Denison, located in Blanding, Utah, which is the only conventional mill in the U.S. Having mill access is extremely important because you effectively cannot produce your final product without it. Energy Fuels has a monopoly position with a conventional mill and it can even make money by processing material on a toll basis for other producers. We believe that this is a very attractive company for those who believe that the uranium price will head higher.

Moving further down the chain, we like the 50/50 Fission Uranium Corp. (FCU:TSX.V) and Alpha Minerals Inc. (AMW:TSX.V) joint venture of Patterson Lake South in the southwest corner of the Athabasca Basin. This is probably the most exciting story in the uranium space right now, in terms of news flow and stock price movements. Even though it doesn’t have a resource yet and it’s less than a year old because the initial discovery was in November, the drill results that have been produced to date point to a potentially world-class project. There are currently four zones identified. Based on drilling results and our analysis of the assays to date, our back-of-the-envelope calculation estimates about 50 Mlb at that project already, with significant upside potential. So we’re very excited about seeing the development of this likely world-class project.

Recently, Fission Uranium and Alpha Minerals announced an LOI by which Fission will acquire Alpha for 5.725 shares of Fission for 1 share of Alpha ($7.67 per share of Alpha). We believe this is an excellent outcome for shareholders of both companies as it unlocks the potential for the acquisition of Patterson Lake South by either Cameco or Denison now that the ownership structure has been cleaned up. In addition, shareholders of each company will receive shares in spincos for the respective companies. This will unlock the value of the portfolio of assets Fission and Alpha are currently holding, which the market is assigning zero value to currently.

TER: What else are you looking at and liking?

RC: We like Kivalliq Energy Corp. (KIV:TSX.V), located in Nunavut. It has the highest grade deposit outside the Athabasca Basin and an impressive land package with several highly prospective conductors. We’ve visited the property twice now and have been impressed with the area potential, although Nunavut does present some infrastructure challenges. It will probably need a large resource to be economic; however, we do believe that it does have that potential. The management team has been very cost-effective in identifying resources, which is very impressive. We believe Kivalliq is a very good value play for someone looking a little longer term.

Another notable company is U3O8 Corp. (UWE:TSX; UWEFF:OTCQX), a consolidator of South American uranium assets. It has some interesting developments in Argentina and seems to be getting things in place with the potential for a low-cost, low-grade, open pit operation. Its flagship Berlin project is located in Colombia and has the potential to be of decent size with decent grades as well. Its other asset is in Guyana, giving it three decent assets that all have the potential of being developed, once prices get better. We continue to monitor the progress of U3O8 Corp.

Circling back to Patterson Lake South, one company that catches our attention, although it’s a little too early to say much about it other than we do like where it sits, is NexGen Energy Ltd. (NXE:TSX.V). NexGen sits northeast of the Fission/Alpha Patterson Lake South project, and we believe that it probably has the best prospects for hosting similar, if not the same mineralization, that Fission and Alpha are currently drilling.

Of all the plays in that area, we’re particularly interested in NexGen’s property as well Azincourt Uranium Inc. (AAZ:TSX.V), which is a little to the north of the Patterson Lake South project, as it may host a parallel structure. So both of those seem interesting to us, though a little more speculative.

TER: What strategy do you think investors should be using at this point to try to get maximum return in the uranium space?

RC: The first movers will always be the larger companies, so investments in Cameco, Uranium Participation Corp. and Denison will probably be the most obvious and first to move. Those who are looking for a little more upside torque with a little more volatility would certainly be interested in seeing the Fission/Alpha story given that it has excellent drill results. Those looking for something in between could look to Ur-Energy or Energy Fuels, given that they’re both producers. They have slightly higher costs and should see a meaningful increase in their share prices once uranium prices go higher.

TER: We appreciate your time and thoughts today, Rob.

RC: Thanks again.

Cantor Fitzgerald Canada Metals and Mining Analyst Rob Chang has covered the metals and mining space for over eight years for the sell-side and the buy-side. Prior to Cantor, Chang served on the equity research teams at Versant Partners, Octagon Capital and BMO Capital Markets. His buy-side experience includes managing $3 billion in assets as a director of research/portfolio manager at Middlefield Capital, where his primary resource portfolio outperformed its direct peer and benchmark by over 28% and 18%, respectively. He was also on a five-person multi-strategy hedge fund team, where he specialized in equity and derivative investments. He completed his Master of Business Administration from the University of Toronto’s Rotman School of Management.

Emerging economies including China and India, which are growing several times faster than the U.S., have nevertheless disappointed investors this year. The S&P 500 Index of the U.S. has rallied 22 percent, compared with the benchmark MXEF, MSCI Emerging Markets Index’s 1.46 percent loss.

U.S. stock markets clearly aren’t forward-looking. They’re blind. They’re no longer following fundamentals. They’re bedazzled by only one thing: How much money the Federal Reserve and other central banks will print.Nothing else matters.

Does that mean it’s time for investors seeking long-term value to look outside the U.S.?

With the U.S. economy expected to grow 2 percent a year and the U.K. at 1.5 percent, compared with China expanding at 7.5 percent and India at 5 percent, it may be time to look elsewhere.

Consider this: Other than the U.S. and Germany, all Western markets are lower than they were in 1999. In real-inflation-adjusted terms, even the U.S. and Germany are down about 30 percent.

So far this year, investors have disregarded emerging markets’ economic advantages in favor of focusing on the risks, namely Fed policies that suck capital out of their financial systems like a giant vacuum cleaner and into speculative U.S. assets.

So far this year, investors have disregarded emerging markets’ economic advantages in favor of focusing on the risks, namely Fed policies that suck capital out of their financial systems like a giant vacuum cleaner and into speculative U.S. assets.

However, investors who are focused only on American investments run the risk of missing out over the long run. That’s because the fundamental advantages of emerging markets, particularly in Asia, remain solidly in place, including:

- A strong banking system supported by high personal savings rates. Banks have avoided foolish lending practices and are in a much stronger position to finance economic growth than peers in the developed world.

- Ample foreign-currency reserves with flexible exchange-rate policies.

- Companies with healthy balance sheets.

- Strong growth fundamentals — fast-growing, increasingly richer, middle classes; continuing strong investment in infrastructure that promotes economic growth; generally business-friendly government economic policies.

With forward-looking price-to-earnings ratios for emerging markets now below 10 (compared with almost double that in the U.S.), shares of companies in the emerging world have rarely been so cheap.

As the iconic investor Warren Buffett says: “Price is what you pay, value is what you get.”

Along that line, that’s why I believe the emerging markets have fallen back toward levels that represent good value. While they could continue to lag in the short run, especially if their currencies weaken, it’s my view that patient investors who maintain a balanced portfolio will be well-rewarded.

See Money and Markets‘ Facebook page to get my investment recommendation for emerging markets.

Best wishes,

Bill

“…The East and South China Seas are the scene of escalating territorial disputes between China and its neighbors, including Japan, Vietnam, and the Philippines. The tensions, shaped by China’s growing assertiveness, have fueled concerns over armed conflict and raised questions about Washington’s security commitments in its strategic rebalance toward the Asia-Pacific region.”

“…The East and South China Seas are the scene of escalating territorial disputes between China and its neighbors, including Japan, Vietnam, and the Philippines. The tensions, shaped by China’s growing assertiveness, have fueled concerns over armed conflict and raised questions about Washington’s security commitments in its strategic rebalance toward the Asia-Pacific region.”

Please click HERE to view the excellent summary of this important issue – Regards Jack & JR

Most people are risk averse because it’s been bred in them from early childhood. Protective parents caution their children “Don’t climb that tree, you might fall.” “Be careful of that dog, it might bite you.” That caution carries over into early adulthood and then into the workplace, where “don’t rock the boat” makes the most sense. Is it any wonder that when it comes to investing people are subjected to two conflicting ideals? One is to make as much money as possible, and the other is to take as little risk as possible to achieve this. How can this be done? Well, it can’t. Many people resort to professional money management in their desire to achieve these diverse aims.

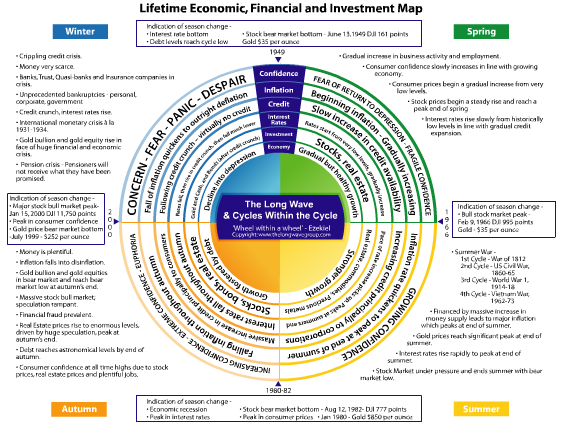

Even the best money manager will fail if the investment cycle is not with him or her. A major benefit of understanding the Kondratieff cycle is that it allows us to make lower risk investments in each of the four Kondratieff seasons. In each of the seasons there are appropriate and inappropriate investment mediums. For example, in the Kondratieff autumn, stocks, bonds and real estate make the best investments, whereas investing in gold and gold stocks are high risk. The opposite is true for the Kondratieff winter. The trick is recognizing where we are in the cycle. Fortunately there are events that provide us with that information. For example, we know when the great bull markets in stocks, bonds and real estate are about to commence in sync with the onset of the Kondratieff autumn. Four events precede this: the peak in interest rates, the peak in prices, a bear market in stocks, and a recession. These events occurred between 1980 and 1982 and similarly between 1920 and 1921. Following those events one could have invested in real estate, bonds and, in particular, stocks, with the confidence that these three investments were about to begin the biggest bull market of a lifetime.

Important: Click HERE or on image for functioning Chart below

……read more HERE

Markets that see volume of transactions evaporate on up days and surge on down days have traditionally offered a warning sign to invested capital. The price action on Friday for the Canadian TSX 60 (here captured in the XIU) is just one of several red flags to anyone who is paying attention to downside risk. Red bars at bottom of this chart (in red oval) denote selling pressure and should be compared with the grey bars of buying pressure shown here on the other trading days year to date.

Source: Cory Venable, CMT, Venable Park Investment Counsel Inc.

Ed Note: More from Danielle Park

How the economic machine works

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair