The reasons why the technology has so much potential are as follows:

The reasons why the technology has so much potential are as follows:

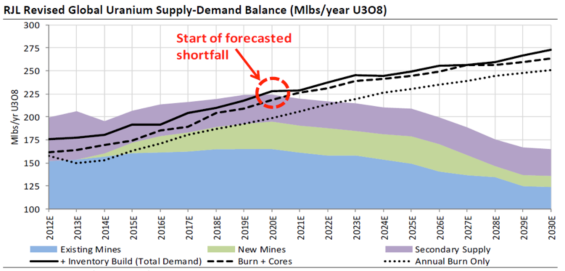

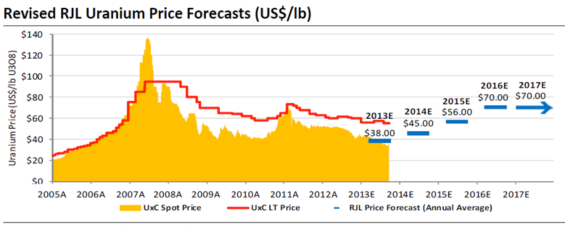

source: Raymond James Ltd., UxC

TMR: Given all these conflicting trends, how are mining companies responding?

DS: The mining companies have suffered. Spot uranium prices are at eight-year lows and are not reflecting the longer-term fundamentals. For companies that have meaningful exposure to current market prices, that is to say those that don’t benefit from long-term fixed-price contracts, their realized prices are on a downward trend. That is definitely factoring into equity valuations as well. We’ve got producers averaging well below historic levels. We typically see producers averaging well over 1.5-times price-to-net asset value, for example, and right now they’re trading at fractions of that. The juniors are even more battered with reduced prospects of securing equity financing and greater challenges in quickly getting their projects into positive cash flow. But the uranium price must inevitably go higher and we see a lot of opportunity on the equity side because of that. We think there’s going to be a continued trend toward mergers and acquisitions with logical consolidation in key jurisdictions such as the Western United States. Also, many larger entities are well capitalized, while potential acquisition targets are trading at bargain valuations.

As far as how uranium companies have coped, over the last 12–24 months we’ve seen Cameco shelve its Double U project, BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) shelved its Olympic Dam expansion plans. Trekkopje, Imouraren, Bakouma, Stage 4 at Langer Heinrich, Ranger Heap Leach—these are just some of the projects that have been pushed back or canceled, now removed from the project pipeline. Existing production has been cut back as well. Energy Fuels Inc. (EFR:TSX; EFRFF:OTCQX) has halted mining at three small mines in Colorado and Uranium One is throttling back on well field development at its Willow Creek mine in Wyoming, which should result in declining output rates there. Further supply cutbacks like those could be one of the catalysts that spark the uranium price over the next 12–24 months. We highlight Uranium One’s Honeymoon mine in Australia, Paladin’s Kayelekera in Malawi, Rio Tinto’s Rössing in Namibia and further growth in Kazakhstan as potentially being the next victims of this low price environment.

TMR: You recently attended this year’s World Nuclear Association Symposium. What were the takeaways?

DS: The symposium is the largest demand-side event in the industry. Normally we see an uptick in market activity following the conference as market participants from around the globe sit down in London and hammer out supply deals. That didn’t really happen this year. I think what became apparent at the WNA was the demand side of the industry feels satisfied with the amount of uranium available to meet its uncovered needs over the next couple of years. That in part has led to a complete collapse of the long-term contracting market. We’re just not seeing any long-term contracting right now. Year-to-date there’s only been about 14 million pounds (14 Mlb) of yellowcake that has changed hands in the long-term market. That compares to about 140 Mlb/year average over the last decade. There’s some thinking that at some point utilities have to resume contracting. That’s really going to be what gets the uranium price moving upward in our view—that concern among utilities that they’re not covered on the supply side, coupled with an increasingly apparent future supply shortfall, leading to more buying. As I’ve mentioned, Japanese reactor restarts and further supply cutbacks could be critical in the timing of this.

TMR: You have 10 uranium companies under coverage. What are your choice picks and why?

DS: Two of our top picks are Cameco Corp. (CCO:TSX; CCJ:NYSE) and Ur-Energy Inc. (URE:TSX; URG:NYSE.MKT). For Cameco, we’ve got a $25/share target and an outperform rating. This company is the industry’s go-to, the blue chip uranium company. It’s organically growing very low-cost operations, which are for the most part in very safe jurisdictions. It has a lower-risk approach to contracts, with a targeted pricing mix of about 40% fixed-pricing and 60% market-related pricing in the contract book. The company’s got a solid balance sheet. We think it’s going to end Q3/13 with about $800M in working capital and another $2 billion ($2B) in undrawn lines of credit. It’s also diversified across the nuclear fuel chain, with exposure not only to its core uranium mining business but also with nuclear fuel services, like conversion and fuel fabrication. It’s got a stake in the Bruce nuclear power plant as well as a newly bolted-on uranium trading business, so it’s quite diversified. On top of that, Cameco pays a 2% dividend. We think it offers a very attractive risk/reward proposition at these levels.

On Ur-Energy, our other top pick, we’ve got a strong buy rating and $1.80 target. Ur-Energy is the world’s newest uranium producer, having just started operations at its flagship, wholly owned Lost Creek in-situ leach mine in Wyoming, a very favorable geopolitical jurisdiction for mining. Lost Creek has lowest-quartile cash costs. We’re modeling it at about $22/lb life-of-mine average production cost there. Ur-Energy just put out a strong production update in September. We think that the ramp-up curve on production is highly derisked now. The company also boasts an operationally experienced management team that has done a great job hedging themselves. About 33–50% of design production rates are going to be delivered into fixed-price contracts through 2019. Those contracts are priced well above current market levels, providing significant near-term cash flow. Having just secured its long-sought-after low interest bond loan from the state of Wyoming, $34 million at 5.75% interest, we model Lost Creek as fully funded, and the company’s balance sheet as carrying much lower risk. Furthermore, trading at only 0.6 times price-to-NAV, a 40% discount to the group average, we think the current share price offers a very attractive entry point at the moment.

TMR: Speaking of Cameco, in September you bumped your target for Cameco up $1 to $25, but the stock fell 14%. What was the thinking behind that?

DS: That change was more of a housekeeping revision. With that research note, as we always do around that time of the year, we rolled forward the discount periods on our discounted cash flow models from 2013 to 2014. We also rolled forward the valuation period on our price to cash flow to 2015. Both of those changes, in this case, had a slightly positive impact on our valuation and that’s what resulted in the upward tick to a $25 six- to twelve-month target price.

TMR: How will the opening of Canadian uranium mine investment to European companies affect your uranium companies?

DS: It’s certainly good news. Elimination of the non-resident ownership policy (NROP) will permit European Union-based companies to own a majority stake in an operating uranium mine. That opens the door for companies like Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) and AREVA SA (AREVA:EPA) to push forward with development of existing deposits or to buy more uranium assets in Canada. Accordingly, it increases takeover potential for companies like Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT), UEX Corp. (UEX:TSX) and Kivalliq Energy Corp. (KIV:TSX.V).

Despite Cameco’s apparent support for the rule change, we think it may face increased competition in Canada for personnel, equipment and permitting priority if companies like Rio Tinto and AREVA are allowed to build up production.

TMR: Denison Mines Corp.’s stock is at a four-year low, with its takeover target, Rockgate Capital Corp. (RGT:TSX), having fought Denison’s bid. Your return on Denison has also been poor. Why are you recommending Denison as an outperform?

DS: The board of Rockgate has actually changed its tune and is now recommending shareholders accept the offer from Denison, which we think is a great deal for shareholders on both sides. Denison gets a significant chunk of cash out of Rockgate as well as the Falea project in Mali as a throw in for less than $0.20/lb, while Rockgate shareholders will now get shares of Denison, a company with superior size, liquidity, assets and strategy in exchange for their Rockgate shares. Falea is likely to get spun-out with Denison’s other African assets if the deal closes successfully.

On our recommendation, we view Denison as one of the premier uranium explorations globally with a dominant landholding in the eastern Athabasca Basin. The company has a 60% interest in Wheeler River, the world’s third-highest-grade uranium deposit that continues to grow. It’s got a 22.5% stake in the McClean Lake mill, the most advanced uranium processing facility globally, which is undergoing a doubling of plant capacity at nil cost to Denison and should yield some nice toll milling revenues starting next year. It’s got a 60% stake in Waterbury Lake, the western extension of Rio Tinto’s Roughrider, and then a highly prospective suite of exploration projects elsewhere in the Athabasca as well as in Mongolia and in Zambia.

In addition to outstanding exploration upside at those projects, we recommend Denison on high takeout potential. We believe these growing high-quality assets in low-risk jurisdictions would be a natural fit for many strategic entities, such as Rio Tinto, particularly after the recent revision to the NROP policy, as we discussed, as well as Cameco or even Asian nuclear utilities. Denison is well run. It’s got a solid cash position even without the Rockgate acquisition. Like our other top picks, Denison can weather uranium price weakness in the near term, but it’s poised for that inevitable rebound in uranium prices and industry sentiment. That’s really what drives our valuation on the company.

TMR: Thank you, David. You’ve given us a lot of insight.

DS: You’re welcome.

David Sadowski is a mining equity research analyst at Raymond James Ltd., and has been covering the uranium and junior precious metals spaces for the past six years. Prior to joining the firm, David worked as a geologist in western Canada with multiple Vancouver-based junior exploration companies, focused on base and precious metals. David holds a Bachelor of Science in Geological Sciences from the University of British Columbia.

Want to read more Mining Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit The Mining Report.

Related Articles

- Why Uranium Prices Will Spike in 2013: Raymond James

- 10 Strategies for Success in a Flat Commodity Price Market: John Kaiser

- Look Beyond Gold for Compelling Risk/Reward Ratios: Michael Curran

DISCLOSURE:

1) Tom Armistead conducted this interview for The Mining Report and provides services to The Mining Report as an independent contractor. He or his family owns shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Energy Fuels Inc. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) David Sadowski: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: I was research restricted on Alpha Minerals and Fission Uranium at the time of the interview. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. View complete Raymond James disclosures.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

There are no evidence that the men and women who have the intitiative, passion, work ethic and drive to build small Businesses are appreciated by the media and Politicians. Indeed Michael feels they demonize those who produce, subsidize those who refuse to produce and Canonize those who complain. More below:

There are no evidence that the men and women who have the intitiative, passion, work ethic and drive to build small Businesses are appreciated by the media and Politicians. Indeed Michael feels they demonize those who produce, subsidize those who refuse to produce and Canonize those who complain. More below: