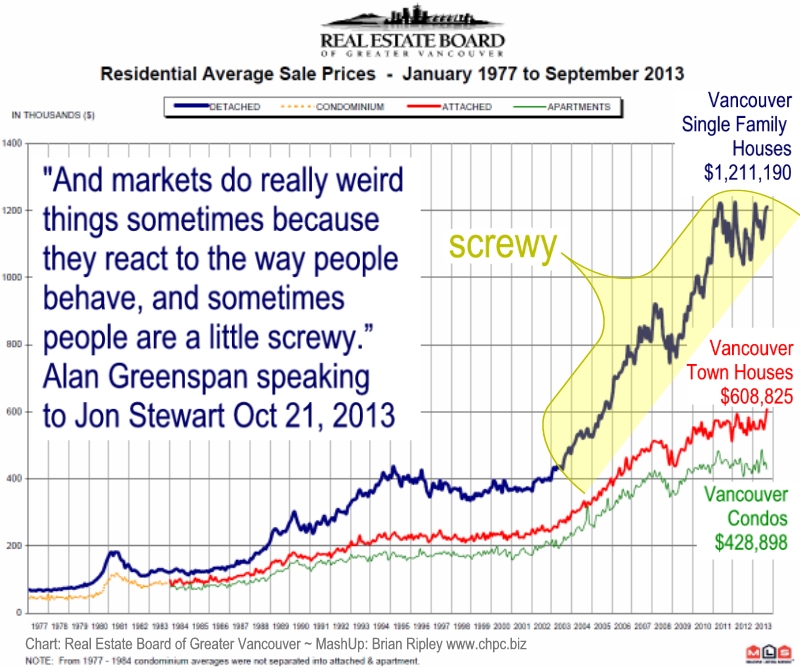

Timing & trends

“We really can’t forecast all that well. We pretend that we can but we can’t.

And markets do really weird things sometimes because they react to the way people behave, and sometimes people are a little screwy.”

Alan Greenspan, speaking to Jon Stewart (at 6.20min) on The Daily Show. More quotes from this interview (paraphrased):

- The banks did not fully understand the risks out there.

- We analysts thought the actors would be rational.

- We couldnt believe their (bank’s) leverage.

- You cannot tell which are the toxic assets.

- Let banks suffer the consequences, don’t let them default.

Alan Greenspan was Chairman of the U.S. Federal Reserve from August 1987 to January 2006. Vancouver has been screwy since the spring of 2005 when commodity markets launched bringing other physical and paper assets along for the ride as private sector investors and government managers abandoned fundamentals.

(Click HERE or Chart to enlarge)

More from Canadian Housing Price Charts:

“Blackstone Group LP (BX), builder of the biggest single-family rental home business in the U.S. is using its experience to replicate the model in Spain where property prices have dropped 40 percent.”

….read Spanish Inquisition

Silver sees largest daily loss in 6 weeks

Silver sees largest daily loss in 6 weeks

- Corn sets 3-year low on expectations of a record harvest

- Coffee hits fresh 4-1/2 year low on increase in supplies

Base and precious metals led commodities lower on Thursday, with silver down 5 percent in its worst daily performance in six weeks, as the dollar gained and investors squared their books ahead of the month’s end.

A sharp rise in the dollar index broadly pressured commodities after data showed business activity in the U.S. Midwest surged past expectations in October, countering recent evidence of soft economic growth. That came after the Federal Reserve on Wednesday dropped a reference to tightening financial conditions in its post-meeting statement, bolstering views that the U.S. central bank could roll back stimulus sooner than many expected.

In recent weeks, investors expected tapering of the stimulus would not start until March 2014. Arabica coffee fell to a 4-1/2 year low on expectations of a bumper harvest in top-grower Brazil and notched its biggest monthly drop since November last year. The oversupplied market has lost ground every month this year except for January and September.

In grains, corn futures prices sank to a three-year low and finished October down 3 percent, while soybean futures also fell, on predictions of further increases to a potentially record-high crop.

Brent crude futures dropped more than $1 a barrel, reversing the previous session’s gains, as traders booked profits and turned their focus to the end of the U.S. refinery maintenance season, which is expected to boost demand for U.S. crude. ]

The Thomson Reuters/Core Commodity CRB index, closed down 0.77 percent, weighed by losses in 15 of the 19 commodities it tracks.

U.S. equities ended the day lower, but posted gains for October. The euro headed for its biggest one-day drop against the dollar in more than six months as a sharp decline in euro-zone inflation and record high unemployment stoked speculation that the European Central Bank may ease further. “We are seeing some liquidation (in precious metals) on the dollar rise and higher Treasury yields. Uncertainty in the equities market is also prompting some gold investors to take profits at the end of the month,” said Tom Power, senior commodity broker at RJO Futures.

METALS DOWN Silver and gold were the weakest performing commodities on Thursday as data showed business activity in the U.S. Midwest surged past expectations in October, countering recent evidence of soft economic growth. For the month, gold ended October just 0.2 percent lower, its decline limited by economic uncertainty over a partial U.S. government shutdown and Washington’s delay in raising the U.S. debt ceiling.

Copper was hit by selling after the Fed’s policy outlook was less dovish than some had expected, while growing supply and weak demand also weighed on the outlook for the metal. Benchmark copper on the London Metal Exchange closed at $7,250 a tonne, down from a close of $7,289 on Wednesday Copper has traded in a $7,000-$7,420 range since early August due to swelling supply and slower demand growth in China and is on track to post its first monthly fall since June.

CORN HITS 3-YEAR LOW U.S. corn futures slumped to their lowest levels in more than three years as the large harvest under way in the United States overshadowed blockbuster export sales. An influx of grain from the advancing harvest was expected to replenish crop inventories that were drained by strong demand following a historic U.S. drought last year. Soybean futures also fell under harvest pressure, with some traders expecting the U.S. Department of Agriculture to increase its crop estimates in a monthly production report on Nov. 8. The corn crop is already estimated to be record-sized and the soy crop the fourth largest in history. “Everybody’s expecting big numbers and they’ll probably get them,” Jack Scoville, president of Price Futures Group, said about USDA production estimates. Chicago Board of Trade December corn futures closed down 2 cents, or 0.5 percent, at $4.28-1/4 a bushel and hit a session low of $4.27, below a three-year low of $4.28-1/4 reached on Tuesday. The contract lost 3 percent during the month.

COFFEE SINKS Arabica coffee on ICE touched a four-and-a-half year low, falling for the 13th straight day on a wave of automatic sell orders as a lack of any new fundamentals kept the over-supplied market’s bearish tone intact. Arabica futures ended October down 7.3 percent, the spot contract’s weakest monthly performance since November 2012 as the market maintained its long-term trend lower on abundant global supplies. The contract has dropped nearly 27 percent in 2013 so far, making it the second-weakest performer, next to corn, in the commodities market. Favorable weather for the vital flowering phase of top grower Brazil’s coffee trees has supported expectations for a third successive large crop. This, combined with the expectation for a record robusta crop from Vietnam’s current harvest and an improved yield in top washed-arabica grower Colombia, is keeping world bean prices under pressure. “We’re generally pretty bearish on coffee, given you’ve got booming supply from Brazil and South America generally,” said Tom Pugh of Capital Economics.

Prices at 6:04 p.m. EDT (2204 GMT) LAST/ NET PCT YTD CLOSE CHG CHG CHG US crude 96.23 -0.15 -0.2% 4.8% Brent crude 108.90 -0.96 -0.9% -2.0% Natural gas 3.581 0.000 0.0% 6.9% US gold 1323.70 -25.60 -1.9% -21.0% Gold 1322.44 -0.75 0.0% -21.0% US Copper 3.30 -0.03 -0.8% -9.6% LME Copper 7249.00 -41.00 -0.6% -8.6% Dollar 80.231 0.454 0.6% 4.5% CRB 277.863 -2.153 -0.8% -5.8% US corn 428.25 -2.00 -0.5% -38.7% US soybeans 1280.25 -7.50 -0.6% -9.8% US wheat 667.50 -7.50 -1.1% -14.2% US Coffee 105.40 -1.45 -1.4% -26.7% US Cocoa 2677.00 17.00 0.6% 19.7% US Sugar 18.32 0.00 0.0% -6.1% US silver 21.867 -27.7% US platinum 1448.40 -31.50 0.0% -5.9% US palladium 736.80 -12.70 -1.7% 4.8%

Produced by McIver Wealth Management Consulting Group

Mark Jasayko, CFA,MBA, Portfolio Manager with McIver Wealth Management of Richardson GMP in Vancouver.

Behind the scenes there has been official disgust with Germany at the highest policy levels for years now because of their seeming explicit exploitation of the credit crunch. While the other big countries did their fair share to provide stimulus-the US, UK, Japan, and China -Germany did their share to make their captive little market called the Eurozone viable enough for German industrialists to get their hooks in deeper to the periphery countries who have seen domestic industry vanish.

Behind the scenes there has been official disgust with Germany at the highest policy levels for years now because of their seeming explicit exploitation of the credit crunch. While the other big countries did their fair share to provide stimulus-the US, UK, Japan, and China -Germany did their share to make their captive little market called the Eurozone viable enough for German industrialists to get their hooks in deeper to the periphery countries who have seen domestic industry vanish.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair