After a very good month for U.S. stocks (in which is normally not a great month seasonally), it would be prudent to begin questioning the validity of the advance over the past year.

It would be very difficult to argue that Quantitative Easing (aka money-printing, QE) has not had a major impact. The question is: How much of the cyclical rally is the result of QE? Answer: Maybe all of it.

In the end, there is only one thing that drives a rational decision to buy stocks: Net earnings. This is what produces the cash flow needed to pay dividends. Even if a stock does not pay a current dividend, the growth implied by its current price is assumed to fund an eventual dividend of some sort. There simply is no other reason to hold a stock. We can’t eat it. We can’t drive it. And now that it is extremely difficult to acquire a physical stock certificate, we can’t even look at it anymore. It is only good for producing current or future expected dividends, or to sell it, hopefully realizing a capital gain, to somebody who believes in its dividend potential.

The one issue with all of this is that net earnings for major US publically-listed companies over the last 12 months have been flat. Despite gains well in excess of 20% across all the major U.S. equity indices, the bottom-line fundamentals of companies in those indices have not improved over that time period.

If fundamentals are not driving stock prices, then it is hope that is driving them. One might counter that prices are justified if earnings are expected to grow rapidly. However, as we have approached the last couple of earnings seasons, analysts have lowered earnings expectations significantly and there is nothing to suggest that this trend will change when we approach the earnings reporting season for the 4th quarter of 2013.

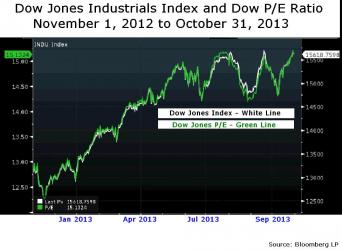

The top chart above illustrates the lack of fundamentals behind current stock prices. It shows the Dow Industrials Index over the last year as well as the average Price to Earnings Ratio for the companies in the Index. The two lines almost line up perfectly. If earnings had grown over the period, this would not be the case.

The bottom chart above shows that we have started to hit a bit of a ceiling (despite the gusher of printed money). Eventually, fundamentals like earnings have a gravitational pull on stock prices. If earnings have not increased, then that gravitation pull will be in the downward direction.

Now, it must be stated that U.S. equities prices are not at crazy valuations. However, they are currently higher than the historical average. That, in itself, does not portend a sell-off. But, it does increase the amount of general risk to levels that we have not seen in five years.

As a result, we have no intention to add to our weighting in U.S. equities at the current time. We are going to have to see a bit of a selloff or a significant improvement in earnings before we do so.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.