Timing & trends

The global panic continues as the Nikkei is now down nearly 17 percent in just 7 trading days as gold shines.

By Bill Fleckenstein President Of Fleckenstein Capital

February 11 (King World News) – Once again overnight markets were chaotic, with Japan losing another 2% (as the yen strengthened further), Hong Kong falling 4%, and most of Europe declining 3% to 4%. The SPOOs lost about 2.5% in sympathy preopening and the market opened a couple of percent lower, but from there the dip buyers showed up once again to trim those losses to about 1%, plus or minus. (Early on the Dow was doing a little worse than the Nasdaq. Go figure.) Also overnight, the Swedish Riksbank decided to make rates even more negative there, so bad policy continues to beget more of the same…

The markets have finally cracked and things are about to become a lot more interesting. Today, the price of gold surged more than $60 and silver $0.60 as the markets crumbled. Even though the markets recovered after some TWO-BIT announcement by OPEC stating that they were talking about “Cutting Production” again… I believe the worst is yet to come.

It has been quite some time since the gold priced shot up more than 5% in one day. As I stated in past articles and interviews, we will continue to see a lot more days like today.

The huge spike in the price of gold sparked a surge in demand. According to the Zerohedge article, Lines Around The Block To Buy Gold In London; Banks Placing “Unusually Large Orders For Physical“:

BullionByPost, Britain’s biggest online gold dealer, said it has already taken record-day sales of £5.6m as traders pile into gold following fears the world is on the brink of another financial crisis.

Rob Halliday-Stein, founder and managing director of the Birmingham-based company, said takings today had already surpassed the firm’s previous one-day record of £4.4m in October 2014.

BullionByPost, which takes orders of up to £25,000 on the website but takes higher amounts over the phone, explained it had received a few hundred orders overnight and frantic numbers of phone calls this morning.

“The bullion market has been building with interest since the end of last year but this morning things have gone bananas,” said Mr Halliday-Stein. “Some London banks are placing unusually large orders for physical gold.”

London-based ATS Bullion added it had been inundated with orders for the past week. The firm has sold 4,000 gold bars and coins since February 1, a 40pc rise on the same period a year ago when it sold 1,500.

Again, I believe this is just the beginning of what will become an AVALANCHE of physical gold and silver buying. Right now there is only a hint of fear. Wait until the markets really start to tank as the price of oil heads below $20.

Gold Eagle Sale Surge In February

While demand for gold in Europe has spiked today, Gold Eagle sales surged this week and are already 116% higher than last year February sales:

In the first week of February, the U.S. Mint sold 12,500 oz of Gold Eagles. However, this week they sold another 29,500 oz for a total of 40,000 oz. In less than half a month, the U.S. Mint has sold more than twice as many Gold Eagles as it sold for the entire month last year.

Silver Eagle sales are also quite robust. Total sales of Silver Eagles (Jan-Feb) are now 8 million versus 8.5 million sold last year. However, we must remember, the U.S. Mint has put a weekly allocation of only 1 million per week. So, sales could not be any higher than 8 million.

If the U.S. Mint keeps the weekly allocation the same, while demand remains strong, we can see a total of 10.5+ million oz sold in the first two months of 2016. This would be nearly 25% more than last year.

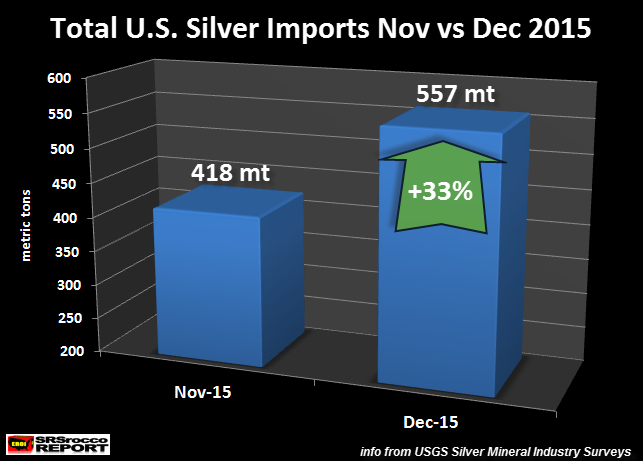

Here We Go Again… U.S. Silver Imports Surged In December

Last year, I kept track of the elevated level of U.S. silver imports. After the spike in silver retail investment demand began to wind down in October and November, U.S. silver imports also declined. However, something changed in December:

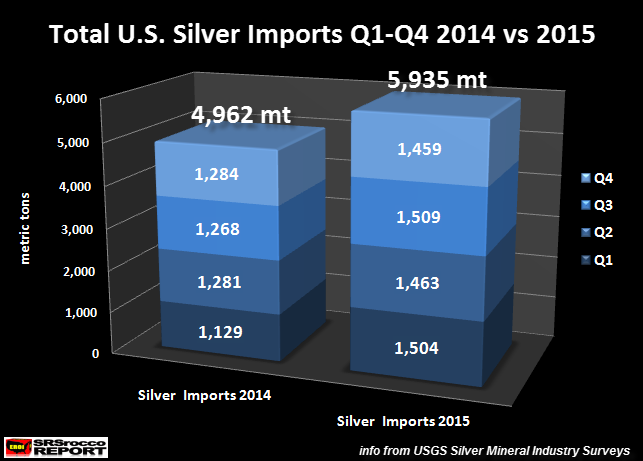

U.S. silver imports jumped by more than 33% in December versus November. Matter-a-fact, the 557 metric tons (mt) of total U.S. silver imports were the second highest monthly in 2015. If we look at the data for the entire year, the U.S. imported nearly 1,000 mt more silver than it did in 2014:

Now, why did silver imports pick up in December if investment demand dropped off as well as industrial demand?? I stated in previous articles that the main driver for the increased silver imports in 2015 had to be investment demand as industrial demand trending lower throughout the year.

I believe there continues to be large entities acquiring silver off the radar. Moreover, the silver didn’t go into the Comex inventories as stocks continued to decline in December.

Something Big Is About To Happen In Gold & Silver

It seems as if the markets finally cracked today. While the clowns and nitwits at the Fed and on the Financial Networks continue to regurgitate that “Everything is okay”, the markets are about to take another huge noise-dive lower.

Fear is starting to enter back into the psyche of the investor. All it would take would be the bankruptcy of a financial institution such as Deutsche Bank to push the whole thing over the cliff. When Deutsche Bank finally goes belly up, we will see an avalanche of physical gold and silver buying. Analyst Jim Willie believes the collapse of Deutsche Bank will be Lehman Brothers TIMES 5.

Already we are see panic buying of gold in Europe and things haven’t really gotten all that bad yet. At some point, the situation in the markets will become so dire… available supply of the precious metals will simply dry up.

So, you wealthy investors out there who still have your net worth tied up into paper assets… you better wake up and start buying physical gold and silver before it’s too late.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter below:

Has the crash begun? The similarities between the current market environment and those seen in the 2008 economic crisis are scary to say the least. Investors are panicking and for good reason – signs that another Lehman-style crisis may be on the horizon.

Deutsche Bank is the one in question. This German banking powerhouse has had its liquidity called into question and is now on the fence, being attacked from all sides as article after article is released pointing to the dangers the bank now finds itself in.

As we reported yesterday, this uncertainty had a dramatic effect on the stock price of the bank, causing it to crash by 10%, dragging it down to levels not seen since the last economic crisis.

The immediate risk that has so many investors on edge is the fact that Deutsche Bank has €350 million in maturing Tier 1 coupons due in April, and even more in the future. The question of whether they will be able to repay this is what has investors so worried.

The attacks have been so fierce and so successful that Deutsche Bank has been forced to issue a press release defending their positions and the fact that they do have the liquidity to meet debt demands in 2016 and going forward in 2017:

Frankfurt am Main, 8 February 2016 – Today Deutsche Bank (XETRA: DBKGn.DE / NYSE: DB) published updated information related to its 2016 and 2017 payment capacity for Additional Tier 1 (AT1) coupons based on preliminary and unaudited figures.

The 2016 payment capacity is estimated to be approximately EUR 1 billion, sufficient to pay AT1 coupons of approximately EUR 0.35 billion on 30 April 2016.

The estimated pro-forma 2017 payment capacity is approximately EUR 4.3 billion before impact from 2016 operating results. This is driven in part by an expected positive impact of approximately EUR 1.6 billion from the completion of the sale of 19.99% stake in Hua Xia Bank and further HGB 340e/g reserves of approximately EUR 1.9 billion available to offset future losses.

The final AT1 payment capacity will depend on 2016 operating results under German GAAP (HGB) and movements in other reserves.

The most worrisome aspect of this press release is the fact that the 2017 projections do not take into account the recent significant losses that the bank experienced in 2016. This means that they are in a much worse position than they were, but whether or not it will affect them in a major way going forward is yet to be seen.

This is just another similarity to the 2008 economic crisis, as that was the last time a major developed market bank was forced to defend itself in such a manner.

Going forward, we can expect the German government to step in and attempt to stave off further collapse of the Deutsche Banks stock price and stem the outflow of liquidity. Banning short selling and jaw boning aplenty are just some of the first steps that we will see.

As in the past, Central Banksters, politicians, and the media will continue to report that all is well, nothing to see here, move along. Yet, there may be no looking back now. This can of worms has been opened and there may be no putting the lid back on – the contagion will spread.

Originally posted at Sprott Money February 10, 2016

Charts Monitor, Rather Than Dismiss Fundamental Data

Charts Monitor, Rather Than Dismiss Fundamental Data

Critics of technical analysis often mistakenly believe that using charts discounts the importance of fundamental data, such as earnings, employment, and economic growth. Charts allow investors to monitor the aggregate investor interpretation of all the fundamental data. Said another way, charts are efficient tools used to monitor vast amounts of fundamental data, which is important since fundamentals ultimately determine which assets classes will perform best. When the economy is healthy, stocks tend to beat bonds. When economic fear dominates, bonds tend to beat stocks. In this article, we will cover the latest signal from the markets that came on February 11, 2016.

Dow Theory Is Based On Economic Common Sense

Dow Theory is based on a series of Wall Street Journal articles written by Charles Dow. The basic tenets of Dow Theory are easy to understand. Charles Dow believed that:

In order for industrial companies to increase their earnings, they had to produce and sell more goods.

In order for industrial companies to increase their earnings, they had to produce and sell more goods.- If industrial companies are selling more goods, then transportation companies must be delivering more goods to retailers and wholesalers.

- Therefore, in a healthy economy, both industrial companies and transportation companies should be experiencing revenue growth.

- If industrial and transportation companies are growing their revenues, then the industrial and transportation stocks should be attractive to investors.

- If industrial and transportation companies are doing well and are attractive to investors, both the Dow Jones Industrial Average and the Dow Jones Transportation Average should be making new highs in unison, serving to confirm a healthy economy.

- From a bearish perspective, signals are generated when the two indexes make important new closing lows, which is indicative of a weakening economy.

Behind The Averages

After reviewing the companies in the industrial and transportation averages, it is easy to see why they represent logical vehicles to monitor the pulse of the U.S. economy. I the present day, our economy is driven by more than just industrial or manufacturing companies. The Dow Jones Industrial Average contains traditional producers, such as IBM (IBM), 3M (MMM), Boeing (BA), Chevron (CVX), and Johnson & Johnson (JNJ). However, the Dow (DIA) also contains Visa (V), Goldman Sachs (GS), and American Express (AXP), since the present day economy relies heavily on the financial sector. The Dow Jones Transportation Average (IYT) still has railroads, such as Union Pacific (UNP) and Norfolk Southern (NSC), but it also contains more modern logistics companies, such as United Parcel Service (UPS), Fed-Ex (FDX), and J.B. Hunt (JBHT).

Just Reconfirmed Primary Bear Market

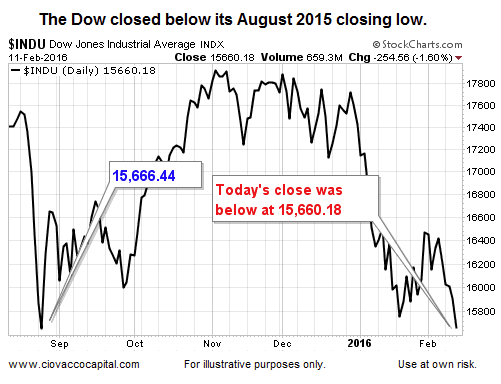

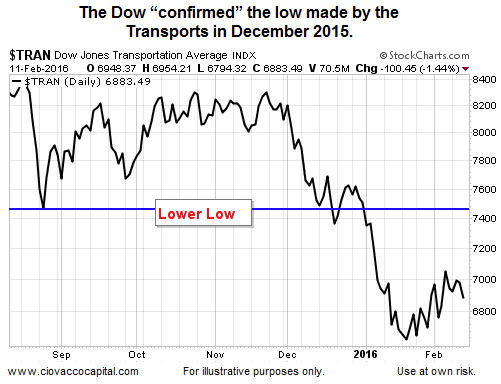

If investors believe industrial and transportation stocks are starting to become less desirable that speaks to their conviction to own these key sectors vs. their conviction to sell. When aggregate bearish conviction starts to outweigh aggregate bullish conviction, stock prices start to fall, which is also a reflection of investors’ perception regarding future economic outcomes. The Dow Jones Industrial Average posted a new closing low on Thursday, February 11, 2016.

Similarly, the Dow Jones Transportation Average also posted a new closing low in December of last year. These lows are the basis for a new Dow Theory primary bear market confirmation signal.

Investment Implications – The Weight Of The Evidence

Our market model does not use Dow Theory, but it does use numerous inputs based on the Dow Jones Industrial Average. As noted in early January, the evidence has been saying “It Is A Good Time To Check Your Bear Market Game Plan”. The Dow Theory signal that occurred on February 11 is another form of evidence saying the same thing. We continue to be concerned about the set-ups described on February 5. Conditions can begin to improve at any time, but until they do our allocations will continue to favor conservative assets (TLT) over growth-oriented assets (SPY).

Sweden’s Central Bank, the Riksbank, rattled markets with a rate cut of .15%, now at -0.50%. Bank shares plunged again. Société Générale is down 13%, Deutsche Bank 7%, and Santander 6%.

Sweden’s Central Bank, the Riksbank, rattled markets with a rate cut of .15%, now at -0.50%. Bank shares plunged again. Société Générale is down 13%, Deutsche Bank 7%, and Santander 6%.

US treasury yields are falling like a rock with gold flying high, up another $40. Oil fell towards $26, and US futures are at the lowest price in two years.

Despite the fact that negative rates cripple bank stocks and rob savers, cutting rates is the only damn thing many of these central banks know how to do.

Please consider Riksbank Cuts Rates Deeper Into Negative Territory.

Sweden’s central bank moved its interest rates deeper into negative territory with an unexpectedly large cut, intensifying fears that global policymakers are being forced to take more extreme action to tackle low inflation.

The Riksbank cut its main repo rate by 15 basis points to minus 0.5 per cent, despite the fact that the country’s economy is booming. The bank said it felt forced to act because of “weakening confidence” in achieving its inflation target of 2 per cent.

The move rattled currency markets, sending the Swedish krona down 1.6 per cent against the euro, while the yen hit a 14-month high of 111.39 against the US dollar.

Bank shares resumed their slide, led by Société Générale, which tumbled as much as 13 per cent. Deutsche Bank dropped 7.1 per cent, Santander lost 6.1 per cent, and UniCredit sank 8 per cent. The pan-European Stoxx 600 fell 3.4 per cent, while US markets were called to open at their lowest in almost two years.

The Swedish cut followed the Bank of Japan’s decision to lower interest rates to minus 0.1 per cent in January, a move which stunned financial markets. At the meeting to approve the cut, some members of the BoJ’s policy committee warned of a global race with other central banks to set the lowest interest rates.

“Today’s action hints at the Riksbank’s willingness to forearm itself also from the ECB’s upcoming action expected in March,” noted Marco Valli, economist at Unicredit.

The ECB lowered its deposit rate to minus 0.3 per cent in December and is expected to make another cut of at least 10 bps at its meeting next month.

Sweden is in the unusual position of having very strong economic growth currently but weak inflation, causing an acute policy dilemma for the Riksbank. It forecasts that economic growth will be 3.5 per cent this year, a little lower than the 3.7 per cent in 2015.

But inflation was just 0.1 per cent in December while core inflation, more closely watched by the Riksbank, was 0.9 per cent.

The Riksbank has been open about its desire to keep the krona weak as part of a global battle to depreciate currencies. The central bank earlier this year delegated authority to its governor and one deputy governor to intervene in the currency markets at any time, a move that has spurred some concern among politicians in Stockholm and dissent from another deputy governor at the Riksbank.

Mind Boggling Stupidity

With economic growth at 3.5%, it would make more sense for the Riksbank to thank deflation than fight it. Spain’s growth is one of the best in the eurozone and Spain too is allegedly mired in deflation.

Next month, the ECB is likely to react with a cut sending its lending rate to -0.40 or -0.50%. Japan will feel forced to act in kind.

Meanwhile, the Yellen Fed still insists the Fed will hike rates this year. I suggest a global recession has begun.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair