Energy & Commodities

Ed Note: Michael Campbell thinks Canada’s Oil Reserves are the Key to Federal Pension / Economic Solvency.

The Benefits of a Bountiful Oil Supply by Joel Bowman

6/20/12 Stavanger, Norway – Mercedes…Mercedes…Volvo…Mercedes…BMW…Mercedes…Volvo…

We were waiting for a taxi outside Oslo’s central train station on the weekend. Not since our dusty stint in Dubai had we seen so many luxury vehicles in a row, all with a meter and a foreign driver, waiting to shuttle the locals around town.

Norway is an expensive place to be. Unless you have the good fortune (literally) of being Norwegian. Tiny, one-bedroom houses on the outskirts of town start at roughly half a million dollars. A round of drinks for four at a pub will eat up most of a $100 note. And oysters down by Oslo’s main pier (admittedly some of the best “Rolls Roysters” we’ve ever tasted) sell for $7 per…um…slurp.

Sitting in the back of the taxi, looking out the window at all the sleek stores and grand old hotels along the famous Karl Johans Gate, we began wondering how a cab driver could afford to live in such a place. Then we arrived at our hotel…barely a five minute drive from the station.

“That’ll be 150 kroner,” said the driver, in perfect English. Our European readers will recognize that amount as about €20. Americans may call it $25. Ah…so that’s how. When it came time to depart the capital, we paid ourself $25 to walk back to the station. Easy money.

Of course, it wasn’t always this way. A little more than half a century has passed since Phillips Petroleum Company (since merged with ConocoPhillips) discovered the Ekofisk oil field in the North Sea. Production began in 1971 and was followed by a slew of other fruitful discoveries, both of oil and natural gas. Since that first well was sunk, Norway’s GDP, adjusted for inflation, has more than quadrupled. Happily for this northern nation, Norway also derives 99% of its domestic energy consumption from hydropower. Nice source…if, again, your geography allows for it.

As of March this year, the total value of Norway’s Sovereign Wealth Fund (SWF) was NOK 3,496 billion ($613 bn) — the world’s largest. Officially The Government Pension Fund of Norway, the fund derives its wealth not from pension contributions, but primarily from oil revenues, including taxes, dividends, sales revenues and licensing fees. Norwegians refer to it simply as Oljefondet, or “The Oil Fund.”

This vast wealth has allowed the Norwegians to indulge in that most costly of economic experiments: Socialism. Proponents of this sadly persistent model of welfare statism like to point to the “Nordic Model” as proof that their tax-and-spend philosophies work. As usual, they confuse cause and effect. Norway’s riches are the result of oil, not socialism. Wealth comes from revenue, savings and capital formation, in other words…not from spending, public works and redistribution. Norway’s oil riches make the case for socialism as well as Abu Dhabi’s riches make the case for oppressive medieval sheikdoms — i.e., poorly to not at all.

Fortunately for Norway — and conveniently for reality-averse advocates of the welfare state — the North Sea’s hydrocarbon bounty is not about to run out overnight. Although production from the North Sea’s largest field, Statfjord, has been in steep decline since the mid ’90s, revenue continues to pour in from smaller, surrounding deposits. Conservative estimates predict the fund may reach $800-900 billion by 2017 — roughly $200,000 for every ridiculously attractive member of the population.

As regular reckoners know, however, the state is always and everywhere working to misdirect capital, to distort markets and to indulge folly. This is true no matter how joyous its people, how scrumptious its seafood, how picturesque its fjords.

Joel Bowman

for The Daily Reckoning

Read more: The Benefits of a Bountiful Oil Supply http://dailyreckoning.com/the-benefits-of-a-bountiful-oil-supply/#ixzz1yPxLUjhQ

OPEC is meeting today (June 14th( in Vienna. And boy, does this group have a lot to talk about.

That’s because the price of U.S.-benchmark West Texas Intermediate crude is down about 25% since hitting a 10-month high of $110.55 a barrel back in March.

That’s a big move in anyone’s book. But I think the price could drop even lower from here.

Part of the reason for that big move down? More supply.

‘A Tremendous Oil Surplus’

According to data from Platts, crude oil production from OPEC rose to 31.75 million barrels per day in May. That’s up 40,000 barrels a day from April; it exceeds OPEC’s own production ceiling by 1.75 million barrels a day, and is the highest level since October 2008.

This occurred even as Iranian supplies were being squeezed by a drop in the number of customers willing to take its oil. Kuwait, Libya and especially Saudi Arabia led production higher.

The Saudis could face pressure from some countries at the Vienna meeting to rein in production. In fact, OPEC president, Abdul-Kareem Luaibi, who also serves as Iraq’s oil minister, told reporters on Monday: “It’s very clear there is a tremendous surplus that has led to this severe decline in prices in a very short timespan. This will not serve anyone.”

So that should put a floor under oil prices, right?

While we could see a bump in the price of crude, the short-term trend for oil prices is actually down. In fact, I wouldn’t be surprised to see crude drop to $70, $65 or even LOWER before the pendulum swings the other way.

Let me give you some reasons why …

#1. Saudi Arabia Could Tell OPEC to Take a Hike.

Recently, Saudi Arabia increased its production to 10 million barrels a day to pick up the slack from sanctions against fellow OPEC member Iran. What’s more, Saudi Oil Minister Ali al-Naimi said the desert kingdom saw increased oil production (and lower prices) as a “stimulus” for the sputtering global economy.

What’s more, Mr. al-Naimi said Saudi Arabia’s analysis “suggests we will need a higher (production) ceiling than currently exists.”

While the Saudis will see how other OPEC members react before formulating a position, Mr. al-Naimi added that his country needs to be allowed to produce more than it currently does. Saudi Arabia says it has spare capacity of another 2.5 million barrels per day.

Is Mr. Luaibi, the oil minister for Iraq, going to tell the Saudis otherwise? Iraq’s oil exports are expected to rise to 2.9 million barrels-per-day next year, from 2.4 million barrels this year. So, Mr. Luaibi might have trouble convincing the Saudis to cut back.

It may all be a wash because Saudi Arabia said it is going into the meeting planning not to ask for OPEC to raise the production level. But that won’t stop it from cheating like a bandit … indeed, any OPEC country that can produce more oil seems to be ready to do so, regardless of quotas.

Also, Saudi Arabia has every incentive to keep prices low enough to discourage a search for alternative fuels and keep demand high for its oil.

Sources say while Iran needs $117 oil to balance its budget, Saudi Arabia is happy with $100 oil. I think the Saudis might be happier with even-lower prices than that, considering that they can pump oil for an estimated cost of $20 per barrel.

Think about it: If the Saudis keep the price of oil low enough, long enough, a lot of expensive deepwater-oil projects will have to be shelved.

Compare their $20-per-barrel cost with North Sea fields that have a marginal cost of about $60 per barrel, while other new deepwater discoveries can cost from $70 to $90 per barrel.

That means more market share for the Saudis, who can ride prices back up again after they put some deepwater competitors out of business.

#2. U.S. Oil Production Soars; Imports Drop.

U.S. oil production has risen 25% since 2008 (an additional 1.6 million barrels per day), and last year, the United States registered the largest increase in oil production of any country outside of OPEC. America’s oil production could increase by 600,000 barrels per day this year.

Hydraulic fracturing has led to a monumental increase in U.S. natural gas and oil production, which will only increase further as the country’s demand for those resources grows.

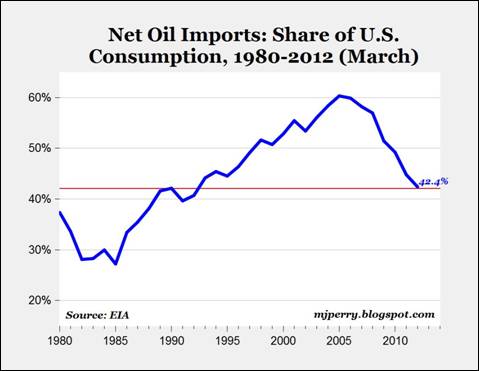

Result: We are becoming more independent of imported oil. Net petroleum imports have fallen from 60% of total consumption in 2005 to 42% today. Here’s a chart I picked up from economics professor Mark J. Perry’s excellent Carpe Diem blog …

What’s more, the composition of our imported oil is changing. The output of Canadian oil sands has tripled since 2000. Not only is Canada a friendly country, but Canada’s production is already hooked into the North American oil grid. So, more production from Canada lowers U.S. oil prices, which already trade at a steep discount to the Brent crude international benchmark.

I’m not saying we’re going to be free of imported oil, or even free of importing oil from countries that hate us. I’m saying that the more independence we get with our energy supply, the better off we are.

Does more oil supply here in the U.S. translate to lower prices at the gas pump? Bet on it! The average price for a gallon of regular gasoline in the United States fell 15.9 cents to $3.624 in the past three weeks.

#3. Global Economic Growth Is Slowing Down.

The debt crisis is just one problem Europe is grappling with. Another is that economies all over Europe are slowing down rapidly, including the engine of Europe, Germany.

This economic slowdown — with a threat of recession — is weighing on oil demand and prices. In fact, Europe’s fuel demand has fallen so fast that nearly a quarter of Europe’s refinery capacity was taken offline in May, as refiners responded to declining demand for gasoline and diesel.

The euro zone accounts for just 12% of global oil demand, or about half as much as the United States. But since oil prices are made on the margins, a euro-zone recession will be a heavy weight on crude.

Meanwhile, in China, imports went up 0.4% in May to a record 6 million barrels, but that’s because China is building up oil stockpiles. In fact, the most bullish news for oil is that China diverted 40 million barrels to its strategic petroleum reserve and could add another 85 to 110 million barrels in the second half of the year.

But China’s economy is hitting the brakes. China’s inflation dipped to a two-year low in May while economic activity remained weak. Steel production fell 2.5% in May compared to April. Iron ore spot import prices fell 8% through most of May. And output of copper fell 1.4% month-on-month, its second-consecutive month of decline.

Here in the U.S., our economy is still growing. But job creation slipped alarmingly in April and May, and manufacturing orders slid lower in the last two months.

I don’t know if we’re going into another recession. In fact, I hope we can avoid it, and one thing that will help us avoid a recession is lower oil prices. But the fear of a recession should be enough to cause traders to make bearish bets on oil prices. And that could send oil prices lower, faster than anyone thinks possible.

OPEC has a poor record of halting such dives. Deutsche Bank data shows that, over the past 20 years, OPEC has slashed production 13 times to try and prop up prices. Three-quarters of the time, the tactic has succeeded within three months. There are three notable exceptions: 1998, 2001 and 2008. In each instance, amid a worldwide economic slump, it took an average of 15 months for the cuts to work.

So oil prices should go lower. Hooray! But don’t get too comfortable …

Why the Drop in Oil Prices Won’t Last Longer-Term

I am expecting oil prices to go down in the short term, but they’ll probably bottom and head higher again by next year at the latest.

For one thing, the election results should clear up the gridlock in Washington one way or another, so we’ll see more economic stimulus. And there will likely be more stimulus in Europe, as well as in China and other countries. That should get the global and U.S. economies firing on all cylinders again.

Another reason — the ramp-up in production from Saudi Arabia is amazing, but advances in technology will only get you so far. You can’t extract an infinite amount of oil from a finite world. So, I expect production in Saudi Arabia to peak either because the Saudis cut to support prices or because aging oil fields simply can’t keep up.

Meanwhile, the marginal cost of oil production, defined as the cost of pumping the last and most expensive barrel required to satisfy demand, is rising as old, cheap oil is pumped and new wells and fields cost much more. If the oil price falls below the marginal cost, there is no incentive to produce more oil. That will remove supply from the global market until prices go higher again.

According to The Wall Street Journal, in 2011, the average marginal cost of oil production was $92.26 a barrel for the 50 largest listed oil and gas companies. And it will reach $100 a barrel next year.

Of course, the best-laid plans of mice and oil men often go awry, so we’ll see what really happens down the road.

4 Ways to Profit from Lower Oil Prices

- For now, you should be hedging bullish positions in oil producers, if you have any. And if you have the stomach for speculation, rallies in oil can be shorted.

- Also, you might want to look at long positions in companies that do very well when oil prices go down — airlines, for example.

- And you know who is helped by falling oil prices? Gold miners! Fuel costs are a big part of the cost-per ounce, so as oil prices go down, profits go up for well-run miners.

- One more thing to consider — when oil prices do bottom, we should see some really attractive opportunities on the long side in the under-loved energy companies.

All the best,

Sean

P.S. What will come out of OPEC’s meeting? As a member of my Red-Hot Global Resources service,you can be among the first to find out how I’m playing the ebb-and-flow of oil prices. Sign up for your risk-free trial membership today!

What the heck is happening with oil prices?

West Texas Intermediate (WTI) oil is selling in the $82 ranger per barrel — way down from recent postings near $110. Overseas, the Brent price for oil is about $97 per barrel — way down from $125 per barrel as recently as early May.

What’s going on? How low can oil prices go? Are we looking at the beginning of a major price slide? Is the oil and oil service investment space under a pricing assault?

I doubt it. Here’s why: 40% of global oil production comes from places where the national governments cannot afford oil prices to go much lower than they are currently.

The nearby chart tells the tale.

This chart, courtesy of Pierre Sigonney, chief economist of the French oil giant Total SA, describes the oil price level that a series of major producers require in order to balance their national budgets.

The red-shaded region at the bottom is the “breakeven cost” for producers (as estimated by Total). That is, the red shading reflects how much it costs to lift barrels of crude oil out of the ground.

As you can see from the chart, many producers lift oil at an overall cost of $10-20 per barrel. Even the major international players (the red bar on the far right) are in the $40 per barrel average for production.

But take a look at that yellow “budget break-even” line. That’s the price at which the major petro-players have to sell oil in order to fund their national spending. Keep in mind that all of the countries on the list — from Qatar to Venezuela — rely on oil sales for the vast majority of their national income.

Specifically, Libya, Saudi Arabia, Algeria, Iraq, Angola, Nigeria, Ecuador, Iran, Russia and Venezuela all require oil prices of at least $80-100 (or more) just to have sufficient income to run their national budgets. Without a strong oil price, these countries will have bread lines and riots. West Texas Intermediate at $82 a barrel and Brent hovering under $100 is the threshold of pain for the world’s largest oil-producing nations.

Now consider that the 10 countries I just named account for about 35 million barrels of global oil output every day — over 40% of total world crude oil output. (Add in natural gas and gas liquids, and it’s even more.) That’s 40% of world crude output coming from places where the national governments cannot tolerate a price drop for long. So no… the oil price shouldn’t go down much from here.

Still, let’s do some devil’s advocacy and think it all through. The European economy is on the ropes. Chinese economic activity is decelerating. Japan is in a bizarre, permanent recession. The US economy appears to be stalling, and is possibly slipping back into Recession II.

So yes… there are problems all over the place. We could see precipitous drops in energy demand from many quarters. But if oil prices fall too far, they probably won’t stay down for long. The world’s largest oil producers cannot afford it, in any sense of the word.

Indeed, an oil price drop will present another re-entry opportunity for investors to pick up more shares of great oil production and/or oil service companies at a relative bargain. Keep in mind that a pullback in share price could also make the dividend yield even more attractive for many oil players.

Between now and the end of the year, I expect to see oil prices firm up gradually, perhaps even violently. We could also see another sharp, upward spike based on all manner of political and technical events.

The consulting firm KPMG recently predicted that oil prices will remain volatile for the rest of the year. There’s a chance we could see over $140 per barrel, according to a wide-ranging poll of energy executives by KPMG. The underlying issues are economic uncertainty, geopolitical risk, rising operational costs and regulatory concerns.

Libya is back online, for example. But according to what I’ve been told, the wartime damage from earlier this year was not properly repaired. Thus Libyan production facilities, pipelines, pumps, etc., are more jury-rigged than not. We could see a sudden drop in Libyan output based on mechanical and engineering issues. And Libya is just one of the ten countries on that chart above.

There is plenty of risk of supply disruptions from the other nine as well.

Buy the dips!

Regards,

Byron King

for The Daily Reckoning

Byron King is the managing editor of Outstanding Investments and Energy & Scarcity Investor. He is a Harvard-trained geologist who has traveled to every U.S. state and territory and six of the seven continents. He has conducted site visits to mineral deposits in 26 countries and deep-water oil fields in five oceans. This provides him with a unique perspective on the myriad of investment opportunities in energy and mineral exploration. He has been interviewed by dozens of major print and broadcast media outlets including The Financial Times, The Guardian, The Washington Post, MSN Money, MarketWatch, Fox Business News, and PBS Newshour.

Special Presentation Shocking gas price prediction released…A former Big Oil executive’s shocking prediction- “Gas prices could soar to “$7 to $8 a gallon.” Smart Americans are getting ready for gas price spike, but they’re setting themselves up to get rich as gas prices rise. Get the full details…

Read more: What’s the Deal With Oil Prices? http://dailyreckoning.com/whats-the-deal-with-oil-prices/#ixzz1xmArIiTx

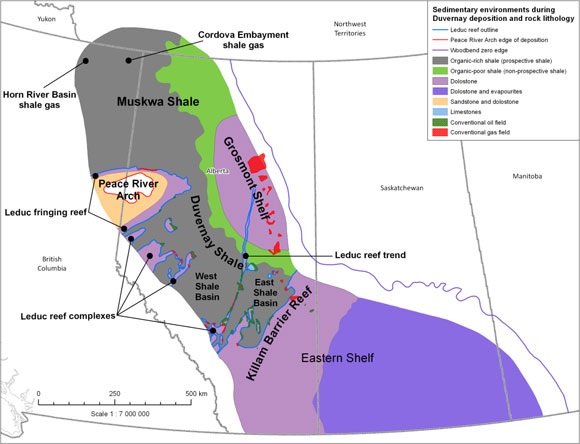

In many ways the oil industry is a fashion industry, and in 2011 the exciting new model on the investment bankers’ catwalk was the Duvernay shale.

Over $2 billion was spent acquiring big land packages, and the rising price per acre kept the play in the news headlines.

Covering over 100,000 km2 along the edges of the foothills of the Canadian Rockies, it’s the source rock for almost all the pools of oil that have created fortunes for Alberta oilmen.

Canada’s second largest brokerage firm, BMO Nesbit Burns, says the highly productive wet gas window in the Duvernay is 7500 km2–that’s 30% larger than the EagleFord wet gas, or liquid rich, area.

It’s huge—no, it’s colossal. It’s over-pressured, and has a high organic content—all the right signs for a great “resource play.”

…..read the entire analysis HERE

Resource developers, especially in the rare earths space, are suffering from the market’s obsession with immediate results, says Byron King, writer and editor for Agora Financial’s Outstanding Investmentsand Energy & Scarcity Investor newsletters and contributor to the Daily Resource Hunter. Nonetheless, he argues, large-scale demand for high-tech metals remains. The question is, which developers can weather the storm?

COMPANIES MENTIONED: ENERGIZER RESOURCES INC. – FLINDERS RESOURCES LTD. – FOCUS GRAPHITE INC. – LYNAS CORP. – MATERION –MEDALLION RESOURCES LTD. – MOLYCORP INC. – NEO MATERIAL TECHNOLOGIES – NORTHERN GRAPHITE CORPORATION – STANS ENERGY CORP.– UCORE RARE METALS INC.

The Critical Metals Report: In the last nine months, poor stock performance has shaken investors’ confidence in the rare earth elements (REEs) sector. What will restore their risk appetites?

Byron King: We need to see successful efforts from developers. Molycorp Inc. (MCP:NYSE) is not the success story it should have been. Molycorp presented itself as an all-American, mine-to-magnets resource, but when it joined forces with Neo Material Technologies (NEM:TSX), its research and development went to Singapore and its manufacturing to China. Its share price is down from a where it was a few months ago, let alone a year ago.

Lynas Corp. (LYC:ASX) was another great hope, but it has had trouble getting its plant in Malaysia up and running. Just as it was nearing the end of construction, local communities raised concerns about radiation in the materials the company is processing and bringing in from Australia. You have to wonder about the source of those problems. Cynics would say, follow the money. What do key Chinese players think about a new, Western player in the sector?

Looking at the smaller developers, their efforts have been slower and more expensive than expected. They prove the rule that nothing is easy in the REE space. It is a hard, technical space to work in. Many management teams are feeling their way through the maze.

Everybody is getting slammed. At the same time, some of the really smart money sees this as the perfect opportunity to buy low.” –Byron King

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair