The Metals Report: You never really believed that there was anything resembling an economic recovery in the United States, correct?

The Metals Report: You never really believed that there was anything resembling an economic recovery in the United States, correct?

Rick Mills: I don’t believe you can have an economic recovery with the type of jobs that have been created in the last few years. Wages have stagnated. The velocity of money, how many times it turns over in the economy, how many times it’s spent, is at a record low,

TMR: So the decision by the Federal Reserve to hold off on tapering quantitative easing didn’t surprise you?

RM: I’ve gone on record saying there would be no tapering this time around, but that doesn’t mean it isn’t coming—it certainly is. But it will likely be very gradual, and the Fed will start only when they feel the economic data support such a move. I firmly believe, however, that the Fed’s zero interest rate policy is here to stay, and this is very important for gold investors.

TMR: Why?

RM: Because it will result in permanent gold backwardation. That’s when the spot or cash price—gold sold for immediate delivery—is trading above the near active futures contract. Backwardation indicates a physical shortage, it’s very rare for any commodity to go into backwardation, but especially gold. Backwardation tells us that gold is being valued higher right now than fiat currencies. It tells us that people are losing confidence in paper money and they’d prefer to hold gold rather then fiat currency.

With real interest rates (your rate of return minus the rate of inflation) in negative territory, the Fed has unintentionally created a lot of support for gold. Gold doesn’t do well in a high interest rate environment because it’s got no yield. If you could get 6% on your money, why would you buy gold, right? Historically, 2% interest has been the tipping point for gold.

TMR: Some people believe there’s been a divorce between physical gold and exchange traded funds (ETFs). What do you think?

RM: I have never been an ETF fan; if you’re buying gold for insurance against calamity, why would you want it held in Toronto or New York or somewhere else? I want my gold a lot closer than that. We see in the news that investors cannot get their gold back when they try to redeem some of their ETF holdings.

TMR: You’ve warned that with regard to nickel and copper the world is running out of low-hanging fruit. Will this lead to shortages, higher prices or both?

RM: Both. One billion people will enter the global consuming class by 2025. That’s 83 million (83M) people per year. Demand is not going to go down. China will have to increase its average urban per-capita copper stock by seven or eight times just to achieve the same level of services we in the West enjoy.

While this is happening, copper mining has become an especially capital-intensive industry. In 2000, the average cost was between $4,000 and $5,000 to build the capacity to produce a tonne of copper. Today, this figure is north of $10,000 per tonne on average and has been reported as high as $18,000 for one particular project.

TMR: Why are costs escalating so rapidly?

RM: Two reasons. First, declining copper-ore grades mean much larger scales are required for mining and milling operations. Second, a growing proportion of mining projects are in remote areas of developing economies where there’s little to no existing infrastructure.

TMR: You’ve predicted significantly higher copper production from Chile is not likely. Why not?

RM: Chile has a shortage of electrical power, a problem exacerbated by “green” groups delaying or stopping new power projects. Chile also has a serious shortage of fresh water needed for mining. Many companies are starting to pipe it in from the ocean and desalinate it.

TMR: Do we see the same higher demand/higher costs scenario with nickel?

RM: Yes, it’s the exact same trend except a few degrees worse. Capital intensity for new nickel mininghas gone through the roof. And the discrepancy between the initial per-pound capital cost of nickel projects and the ultimate construction costs is over 50%. And larger-scale projects have not demonstrated lower per-unit capital costs. Sometimes large projects have even higher capital intensity.

In the future, global nickel supply will come increasingly from laterite nickel deposits, which require high-pressure acid leach (H-Pal) plants. We are now looking at north of $35 per pound ($35/lb) capital intensity as we move into these multibillion-dollar ferronickel and H-Pal projects.

TMR: Your search for cost-effective new sources for industrial metals has led you to Greenland, the world’s largest island. What advantages does this Danish colony have over northern Canada?

RM: Approximately 80% of Greenland is covered by ice with the exposed area forming a fringe around the edge. Geologically, these ice-free coasts are an extension of the Canadian Shield. Both Canada and Greenland are stable politically. The balance starts to tip in Greenland’s favor when we talk about regulation. All permitting in Greenland is done through one agency, the Bureau of Minerals and Petroleum. This is pretty much one-stop shopping—very efficient compared to the regulatory duplication common in Canada.

TMR: How about infrastructure?

RM: Greenland’s easy access to seaborne freight gives it a tremendous cost advantage over northern Canada. If you are in the interior of the Canadian north, you need to truck your product, usually across vast distances, to get it to a railhead or port, sometimes utilizing both a railway and ocean freighter to get it to a smelter. In Greenland, transport distances from project site to open water are usually only tens of kilometers, versus hundreds of kilometers in Canada’s north.

Access to the sea puts the world’s smelters, end users, middlemen, etc., at your fingertips. It lowers your upfront development costs and capital expenditures/operating expenditures (capex/opex) when it comes time to build and run your mine. The southwest coastal region of Greenland has a relatively mild climate with deep-sea shipping possible year round. And climate change leading to the disappearance of sea ice seems to be making the Northwest Passage a viable route.

TMR: Canada’s native peoples are often highly suspicious of—and sometimes outright hostile to—mining activity. This is not the case in Greenland?

RM: No, they seem to welcome the increased capital. Mining brings an awful lot of money into the local and national economies. It provides jobs and taxes. Greenland is dependent on Denmark for much of its funding but wants to become self sufficient. Greenlanders are very protective of their environment. They’ve got rules in place, but they’re not onerous. You can get your work done.

TMR: What specific Greenland nickel-copper play do you like?

RM: North American Nickel Inc. (NAN:TSX.V). The company has the Maniitsoq nickel, copper, cobalt and PGM project in southwest Greenland. This project contains the 70-km Greenland Norite Belt (GNB).

TMR: This is not a laterite deposit, right?

RM: Correct. It is a nickel-sulphide deposit. Something to understand about nickel sulphides is that although they can occur as individual bodies, groups of deposits may occur in belts up to hundreds of kilometers long. Such deposits are known as districts. Two giant nickel-copper districts stand out above all the rest in the world: Sudbury, Ontario and Noril’sk-Talnakh, Russia.

What I want to get across to our readers is that Maniitsoq is thought to be a meteor-impact event like Sudbury. Unlike Sudbury, however, Maniitsoq’s outcrop exposures of nickel-copper sulphide mineralization and its massive sulphide drill intercepts are at surface or very close to surface. Sudbury had glacial movement, whereas this isn’t so in Greenland. I ask myself, what would Sudbury look like if you scraped away the top few hundred meters. It might look like Maniitsoq.

TMR: What is the exploration situation at Maniitsoq?

RM: The company has, so far, over 100 targets. In 2012, 1,550 meters (1,550m) were drilled in nine holes targeting geophysical anomalies. In November 2012, the company announced significant assay results for nickel, copper and cobalt in near solid to solid sulphide mineralization within the GNB from its Imiak Hill target. In December 2012, it announced the discovery of a second zone of significant nickel, copper, platinum, palladium and gold mineralization from drilling at Spotty Hill, which is 1.5 kilometers (1.5km) from Imiak.

In September of this year, North American Nickel announced a second discovery and a third zone of mineralization. Drill hole MQ-13-026 intersected 18.6m of sulphide mineralization averaging an amazing 40–45% total sulphides, with numerous sections containing 65–85%. This third discovery, at Imiak North, is in close proximity to Imiak Hill and Spotty Hill. The company is starting to get some significant intersections and is building tonnage. And the mineralized zones discovered to date are all open at depth.

But with only 27 holes in the ground and over 5,106 square kilometers of area to cover, I think it’s safe to say that North American Nickel is just getting started.

TMR: Could you comment on its cash position and management?

RM: The management is very, very good. It’s the same group as VMS Ventures Inc. (VMS:TSX.V). They are fully backed by the Sentient Group, a very large resource fund, and they raised $7.5M earlier this year, so the company is fully funded. VMS owns 27% of North American Nickel.

TMR: You’re quite excited about anorthosite. What is this, and why does it excite you?

RM: It’s calcium feldspar, which is basically sand containing aluminum, calcium and low levels of soda and iron. Anorthosite could serve as an alternative material in many industrial applications. For example, it could be a new source of filler material. Fillers are a significant component of the plastic, paints and paper industry. It could also replace kaolin, which is a major component of glass fiber manufacturing. And we’re not talking about the pink fiberglass that insulates your house; we’re talking about the fiberglass that piping and a lot of the new materials are being made of.

TMR: What’s the anorthosite situation in Greenland?

RM: Hudson Resources Inc. (HUD:TSX.V) is a fascinating opportunity for investors to get in early and watch the company grow into production. Hudson has the White Mountain anorthosite project in thesouthwest coastal region of Greenland. Hudson has already proved it can reduce its anorthosite’s iron content by running it through an onsite magnetic separator. So now both the soda and iron are below the levels needed to create a ready replacement for kaolin. It’s a fairly easy thing, and we’re talking about an immense deposit.

In addition, Hudson has produced alumina, which is aluminum oxide, from initial bench-scale testing on its anorthosite. James Tuer, the company’s president, believes Hudson is well on its way to producing a marketable smelter-grade alumina. Interestingly enough, Alcoa Inc. (AA:NYSE) is building an aluminum smelter in Maniitsoq, just 80km away from the White Mountain project

TMR: What other Greenland asset does Hudson hold?

RM: It has one of the world’s largest carbonatite complexes, Sarfartoq, which is also in southwest Greenland. What is important about it is neodymium, which is the key to making rare earth permanent magnets. These are the superior, high-strength permanent magnets used for many energy-related applications. For instance, the most efficient wind turbines require 1,000 kilograms of neodymium for each megawatt of electricity.

These magnets are also used in hybrid automobiles, the result of the shift away from electromagnetic systems toward permanent magnetic-based direct drive systems.

Sarfartoq has one of the industry’s highest ratios of neodymium to total rare earth oxide. Right now, Hudson’s working on a flow sheet for the metallurgy, and I expect some news on that fairly soon.

TMR: Tell us about VMS Ventures’ Manitoba joint venture (JV) with HudBay Minerals Inc. (HBM:TSX; HBM:NYSE).

RM: That’s the Reed Copper project in Manitoba. VMS signed a JV agreement with HudBay in 2010. HudBay holds 70%, and VMS holds 30%. VMS is carried through production, so its portion of the mine construction costs will be financed by HudBay, and its 30% share of capital expenditures will be paid back out of the proceeds of production.

TMR: When does production begin?

RM: It’s expected to begin later this year, with full production reached in Q2/2014. The current life of mine (LOM) is estimated to be approximately six years, although deposits in this camp have a habit of growing. Once you get underground, you start drilling to explore for additional mineralization. In the meantime, VMS and HudBay are exploring the prospective areas around the Reed project for new deposits.

TMR: How lucrative is this deal for VMS?

RM: When full production is reached, approximately 1,300 tonnes per day from a probable reserve of 2.16 million tons (Mt), and after recoveries are factored in, the rock is going to be worth $270/tonne. That’s at spot prices of $3.25/lb copper, $1,363 per ounce ($1,363/oz) gold, and $23.60/oz silver.

That’s $354,000 worth of production per day over the current LOM of six years. So, remembering that VMS is carried by HudBay at 30% of production, that’s $118,000 gross per day coming VMS’s way after the payback of production costs. That is an extraordinary amount of money for a junior resource company to have coming in every day. It’s an extraordinary accomplishment.

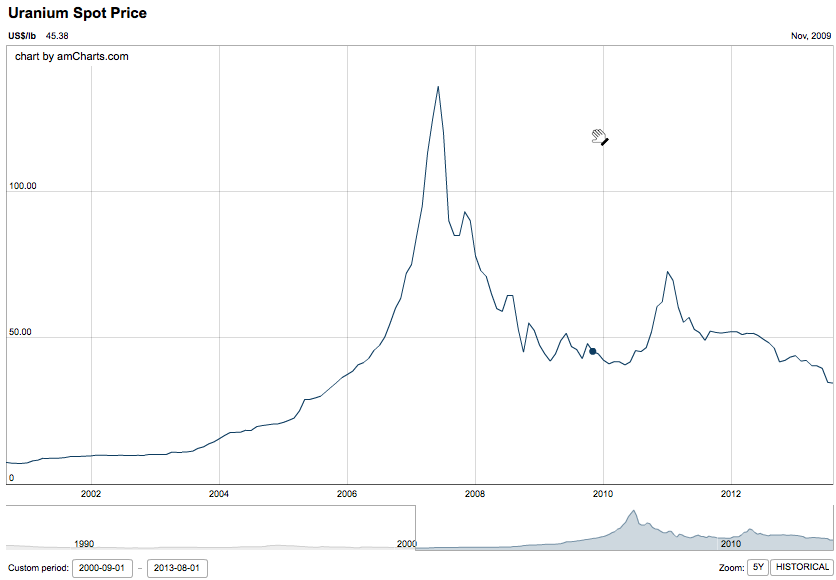

TMR: You’re bullish on uranium. Why so?

RM: First off, let’s remember one of the golden rules of investing—buy something when it’s out of favor, buy what the herd shuns and hold it ’till they want it. The United States produces 5 million pounds (5 Mlb) of U308 per year, yet they use over 50 Mlb. The Russian enrichment program with the U.S. is coming to an end at the end of this year. That’s going to reduce American supply significantly.

TMR: Is there a near-term U.S. uranium play you like?

RM: Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.MKT) is in Wyoming and the company will be going into production soon. It’s a no brainer, as far as I’m concerned. You’ve got a well-run company that will be producing uranium in the States. Uranerz significant offtake agreements and Cameco Corp. (CCO:TSX; CCJ:NYSE) are going to be processing the resin for the company.

TMR: You’ve written about Barrick Gold Corp.’s (ABX:TSX; ABX:NYSE) considerable investments in Nevada in general and in the Spring Valley in particular. Which juniors stand to benefit from joint venture and net smelter royalty agreements there?

RM: Midway Gold Corp. (MDW:TSX.V; MDW:NYSE.MKT) is Barrick’s joint-venture partner. The company has carried to production by Barrick. Two years ago, the published resource was 4.1 million ounces (4.1 Moz), but since then the JV has drilled some of the best holes to ever come out of the deposit. We should get a new resource fairly soon, and I expect it to grow significantly. Midway is a cashed-up junior with other irons in the fire.

Another company that would stand to benefit from Barrick putting Spring Valley into production is Terraco Gold Corp. (TEN:TSX.V), which has a royalty on the Spring Valley deposit. Once the project goes into production, the cash flow to Terraco will be tremendous, and Terraco can also use pieces of the royalty as an ATM, as it were, if they want to do a non-dilutive financing.

TMR: What about Terraco’s other assets?

RM: It has a project called Moonlight, which is attached to the north end of the Spring Valley project. It certainly looks like the Spring Valley mineralization heads north to Moonlight. Also, most people don’t know that there could be a very good opportunity for silver there. That’s why it’s called Moonlight. The old-timers used to talk about seeing the moonlight glint off the silver at night.

The other thing Terraco has got going for it is almost 1 Moz gold in its Almaden project in Idaho. With heap leach, it looks like it would be very cheap to put into production. All told, Terraco is an interesting play.

TMR: What other silver miners do you like?

RM: I’ve been following Great Panther Silver Ltd. (GPR:TSX; GPL:NYSE.MKT) for many years. I’ve watched it grow to be a significant producer. I like it for its exposure to rising silver and gold prices as a producer.

TMR: Do you think we’re going to see prices rise?

RM: Absolutely. You’re looking at a zero interest rate policy in the U.S., that’s negative real rates forever and permanent gold backwardation. You’re looking at a currency war where each country has to keep its currency lower than its export competitors in order to get other countries’ citizens to buy its products rather than everyone else’s. Countries keep their currency weak by printing. The money that has been created so far hasn’t gotten out into the general economy. The monetary base has exploded, but the actual money supply hasn’t gone up appreciably. The banks have been hoarding the money. They haven’t been lending, but bank stocks are rising in anticipation of a lending restart. It’s happening with commercial and real estate loans and some consumer loans, and banks are going to do very well with the interest rate differential. It’s all pointing toward a perfect storm.

TMR: Would you expect major upward movements in the prices of gold and silver before the end of the year?

RM: No. I think all of this is going to take time to work out. The banks have to start lending again; the velocity of money has to increase; and we have to get over this wage stagnation. But it will come. Gold and silver need to find a base for a while, and then we’ll start to see a climb in prices.

TMR: Rick, thank you for your time and your insights.

Rick Mills is the owner and host of www.Aheadoftheherd.com and invests in the junior resource sector. His articles have been published on over 400 websites.

Want to read more Metals Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Metals Report homepage.

Related Articles

- Anorthosite: What It Is and Why You Should Care

- An Investing Opportunity of a Lifetime: Lessons from the Sprott Precious Metals Roundtable

- Look Beyond Gold for Compelling Risk/Reward Ratios: Michael Curran

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Metals Report and provides services to The Metals Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Metals Report: Uranerz Energy Corp., Great Panther Silver Ltd. and Terraco Gold Corp. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Rick Mills: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: Hudson Resources Inc., North American Nickel Inc., VMS Ventures Inc. and Great Panther Silver Ltd. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

An economic recovery that isn’t one. A civil war that isn’t one. Cheap oil that is no more. According to Bob Moriarty, resources remain one of the few absolutes in the world. In this

An economic recovery that isn’t one. A civil war that isn’t one. Cheap oil that is no more. According to Bob Moriarty, resources remain one of the few absolutes in the world. In this

JM: The improvements in horizontal drilling and hydraulic fracking is the most recent innovation that has changed the landscape of the oil and gas industry, making it possible to develop oil and gas deposits in shales and other tight formations. But this is old news at this point. Currently, most oil and gas companies utilizing this technology are trying to improve these operations in their specific development areas by finding the optimal frack design. The ultimate goal is usually to optimize returns by improving recoveries, increasing production rates and lowering costs. Some investors may find a discussion boring about the optimal number of frack stages or whether to use ceramic or sand-based proppant, but that’s where we are at now.

JM: The improvements in horizontal drilling and hydraulic fracking is the most recent innovation that has changed the landscape of the oil and gas industry, making it possible to develop oil and gas deposits in shales and other tight formations. But this is old news at this point. Currently, most oil and gas companies utilizing this technology are trying to improve these operations in their specific development areas by finding the optimal frack design. The ultimate goal is usually to optimize returns by improving recoveries, increasing production rates and lowering costs. Some investors may find a discussion boring about the optimal number of frack stages or whether to use ceramic or sand-based proppant, but that’s where we are at now.