Nuclear fusion is rather different from nuclear fission. Fission, is the reaction currently used in nuclear power plants, and produces dangerously radioactive elements; fusion is the currently being researched by various laboratories around the world, and produces no radioactive waste and far more energy.

Nuclear fusion is rather different from nuclear fission. Fission, is the reaction currently used in nuclear power plants, and produces dangerously radioactive elements; fusion is the currently being researched by various laboratories around the world, and produces no radioactive waste and far more energy.

TER: How does the domination of the Middle East by a handful of countries and corporations affect the movement of energy prices?

CM: While big energy companies may be behind wars of acquisition so that they can gain control of oil-rich regions, once they are in and established they generally want stability so that they can get on and pump the oil without interruption to maximize their profits. While price spikes caused by the threats of unrest and war may produce a welcome boost to profits, actual wars that cause destruction of their facilities and disruption of production are not beneficial.

The control of large areas by the majors results in stability, the sort that we have seen in Saudi Arabia for many decades, for example. But the danger with these mega corporations controlling countries and regions, often in bi-lateral arrangements with local governments, is that giant cartels are created that result in price fixing. So we can say that the advantage of the Middle East being in effect controlled by a handful of western mega corporations is price stability and a tendency to political stability, while the disadvantage is the potential for these stable prices to be on the high side, which is of benefit to the junior companies as well. The junior companies might find it hard to get a foothold in such areas, however, because of the dominance of the majors, and are probably better off exploring elsewhere, the exception perhaps being newly opened-up areas like Iraq.

TER: What has been the effect this year of large investment firms covering shorts in the energy markets? Do you have any picks of junior energy firms that might be rebounding?

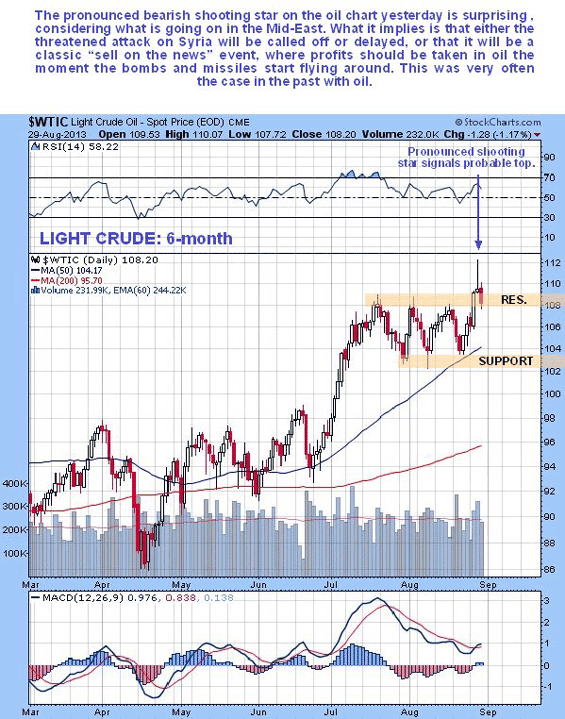

CM: This has caused a sizeable spike in the price of oil relative to other commodities, and there can be no doubt that Syria had an important role to play in this. However, with Syria apparently cooling, this has opened up downside risk for the sector, because a lot of these large investment firms are now all on one side of the boat. On the other side are the commercials, which are now heavily shorting crude—and they are not renowned for being on the wrong side of the trade. The latest Commitments of Traders (COT) charts for natural gas, on the other hand, look bullish.

There are a few junior energy stocks that look attractive to me at this time, based on their technical picture. The charts indicate that there’s something going on in Anderson Energy Ltd. (AXL:TSX). This stock has been pulverized, dropping from a high at about CA$9 eight years ago to the current very low price of CA$0.15. Aggressive buying caused the price to spike in the middle of the month, but it has since drifted right back again almost to where the spike started. A large bull hammer appeared on September 27, suggesting that it will now start up again. The number of shares in issue is rather large but this is well-factored into the price.

Arcan Resources Ltd. (ARN:TSX.V) staged a powerful, high-volume breakout earlier this month but has since drifted back on declining volume to an attractive entry point, although it could drift a few cents more before turning up. It will need to get above its 200-day moving average before an uptrend can get established, but this could happen quite quickly now. Arcan was trading at more than CA$13/share less than eight years ago, so it’s picking up from a very low level now. The number of shares in issue is an acceptable 97 million (97M).

There’s strong upside volume in Artek Exploration Ltd. (RTK:TSX), which appears to have been consolidating for the past year to date. This strong upside volume has already driven volume indicators sharply to new highs, suggesting that an upside breakout is approaching, which will lead to another significant upleg. Shares in issue are a relatively modest 62M.

Cequence Energy Ltd. (CQE:TSX) appears to be bubbling under before making a move higher. We saw aggressive and persistent buying of the stock during the first half of September on high volume, which drove volume indicators sharply higher, but it has since obligingly drifted back to a very good entry point at the support level on much lighter volume. It has been pretty much downhill all the way for Cequence since it started life back in 2007 at the lofty price of CA$14, but the latest technicals show that it is firing up for a significant rally. The number of shares is on the high side at 210M, but again this is already built into the price

TORC Oil & Gas Ltd. (TOG:TSX) is at a good price here, especially as the volume pattern and volume indicators suggest that it is likely to start an uptrend before much longer. The price has been depressed for several years after falling back from a high over CA$56 in 2008, but recent heavy volume, most of which is upside volume, is a sign that interest is building in this stock. It looks like there is good value here, and the number of shares in issue is an acceptable 91M.

TER: How is the short-term life span of fracked wells affecting stock prices? What is the overall situation for supply and demand in energy markets, worldwide?

CM: We would expect the short-term life span of fracked wells to create a more rapid boom and bust cycle in junior energy stocks, unless a more or less continuous stream of producing wells can be maintained.

The overall supply and demand situation for oil and gas appears to be pretty much in balance, which is why the oil price has been in a trading range for the past two years. We have seen peak oil and the depletion of existing oilfields, but, necessity being the mother of invention as they say, we have also seen ingenious responses to the situation in new ways of looking for oil—for example, a massive field has been found in the Gulf of Mexico using special deep drilling techniques, and we have the polar ice cap melting at the perfect time for exploration to expand there in a big way, although this is not such good news for polar bears, of course.

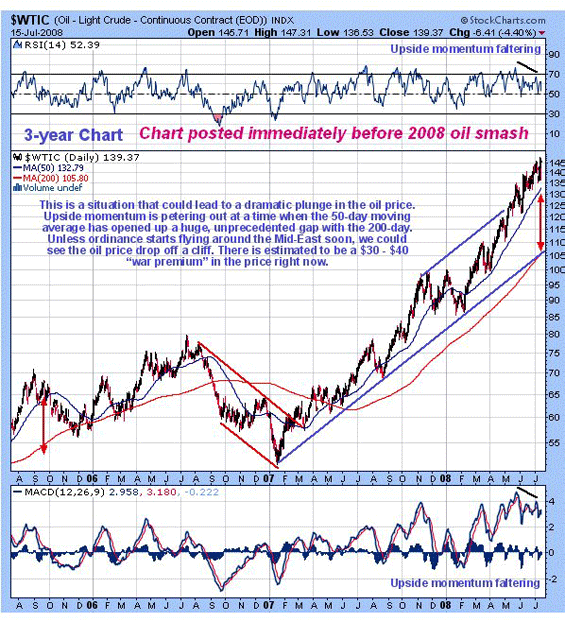

Oil found in more difficult-to-access places is more expensive, and this is what has encouraged the search for cheaper supplies, resulting in massive discoveries in the U.S. These new supplies look set to take the U.S. toward energy self-sufficiency, which would have been unthinkable just a few short years ago. However, this may also lead to a supply shock that drives prices lower. This is another reason that the bearish-looking oil COT charts are thought to presage a lower price trend, and it is thought that the oil price was given a reprieve in recent months by the Syria crisis. Over a shorter time horizon, traders need to watch out for a slump engendered by rapid economic contraction due to rising interest rates. As we saw in 2008, sometimes macro factors render the fundamentals of the oil industry irrelevant. This might be what the COTs are warning of.

TER: Are energy ETFs a good bet? If so, what kinds?

CM: Energy ETFs are an excellent way to play the energy market. They have three great advantages. One is that the ordinary investor can avoid the possibly cumbersome details involved in trading the actual commodity. The second is that you can also avoid the risk inherent in individual stocks, and the third is that you can make money on the downside, too, by using the inverse ETFs available.

Investors have a choice of leverage with these ETFs. There are straight unleveraged ETFs, which move one-to-one with the underlying commodity or index; twice leveraged, which double your gains if you get the move you are expecting (these are the ones we generally go for); and triple leveraged, which have a high decay factor, due to being “juiced” by options, etc., and therefore should generally only be used by professionals, and even then mainly for hedging, or in rare situations where investors are expecting a big move in a short timeframe.

The following (long) ETFs and ETNs provide a broad choice: First Trust Energy AlphaDEX Fund (FXN:NYSE), Vanguard Energy ETF (VDE:NYSE), iShares S&P Global Energy ETF (IXC:NYSE),iShares Dow Jones U.S. Energy ETF (IYE:NYSE), SPDR S&P Oil & Gas ETF (XOP:NYSE) andPowerShares Dynamic Energy ETF (PXI:NYSE).

In addition, we have the First Trust ISE Revere Natural Gas ETF (FCG:NYSE) and iShares Dow Jones US Oil Equipment & Services ETF (IEZ:NYSE).

Short ETFs and ETNs of note include PowerShares DB Crude Oil Short ETN (SZO:NYSE),PowerShares DB Crude Oil Double Short ETN (DTO:NYSE), ProShares Short Oil & Gas (DDG:NYSE),United States Short Oil Fund (DNO:NYSE) and ProShares Ultrashort DJ-AIG Crude Oil (SCO:NYSE).

TER: Is there an optimum entry point for energy stocks in the foreseeable future?

CM: Although technically still in an uptrend, oil stocks as a group have just stalled at resistance and look vulnerable to reversing to the downside soon, especially if the key support for Texas Light at $102 breaks soon, as looks likely. Light crude looks set to drop further back to the high $90-range soon, especially as its latest COT charts look bearish. Military action against Syria looks to have been put on the back burner for now. While there is some support in the 1350 area on the Amex Oil Index, there exists the risk of a deeper reaction back to the 1200–1230 area, where there is significant support, and this reaction could carry considerably further if we see a sharp rise in interest rates. Here we should note that rising rates would likely be accompanied by rising gold and silver prices, as in the late 1970s.

Having said this, many junior energy plays look strong here and set to rise on their own merits, pretty much regardless of what happens to the sector indices and larger oil stocks.

TER: How do currency fluctuations affect oil and gas prices?

CM: Because oil is priced in petrodollars, the key currency to watch in energy pricing is of course the U.S. dollar. Countries that have threatened to cease selling oil and gas in petrodollars, like Iraq and Libya, have paid a heavy price, so we can assume that the U.S. dollar will remain dominant into the foreseeable future, although some countries, like China, are looking for ways to circumvent it. With the Fed maintaining quantitative easing, the dollar is under increasing threat of losing its value, which means that oil and gas prices must move to compensate for a falling dollar.

TER: Thanks you for speaking with us today, Clive.

CM: My pleasure.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts. He lives in southern Chile.

Find out how Maund has used technical analysis to make successful precious metals trades in hisinterview with The Gold Report.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Interviews page.

Related Articles

- Clive Maund: The Mining Sector Resembles the Somme Battlefield

- Don Coxe: China, Japan and Chekhov’s Gun—Where Does Fracking Fit In?

- Bob Moriarty: On the Road to Armageddon, Take Shelter in Resources

DISCLOSURE:

1) The following companies mentioned in the interview are sponsors of The Energy Report: None. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

2) Clive Maund: I or my family own shares of the following companies mentioned in this interview: None. I personally or my family am paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

The Gold Report: Bob, gold prices jumped up on the news that the Federal Reserve would not taper bond buying, then fell days later on news of a possible government shutdown. Did we mark a bottom? Are we in for some more headline-based volatility through the rest of 2013?

The Gold Report: Bob, gold prices jumped up on the news that the Federal Reserve would not taper bond buying, then fell days later on news of a possible government shutdown. Did we mark a bottom? Are we in for some more headline-based volatility through the rest of 2013?