Economic Outlook

While Greece is now dominating the debt default stage, the real tragedy is playing out much closer to home, with the downward spiral of Puerto Rico. As in Greece, the Puerto Rican economy has been destroyed by its participation in an unrealistic monetary system that it does not control and the failure of domestic politicians to confront their own insolvency. But the damage done to the Puerto Rican economy by the United States has been far more debilitating than whatever damage the European Union has inflicted on Greece. In fact, the lessons we should be learning in Puerto Rico, most notably how socialistic labor and tax policies can devastate an economy, should serve as a wake up call to those advocating prescribing the same for the mainland.

While Greece is now dominating the debt default stage, the real tragedy is playing out much closer to home, with the downward spiral of Puerto Rico. As in Greece, the Puerto Rican economy has been destroyed by its participation in an unrealistic monetary system that it does not control and the failure of domestic politicians to confront their own insolvency. But the damage done to the Puerto Rican economy by the United States has been far more debilitating than whatever damage the European Union has inflicted on Greece. In fact, the lessons we should be learning in Puerto Rico, most notably how socialistic labor and tax policies can devastate an economy, should serve as a wake up call to those advocating prescribing the same for the mainland.

The U.S. has bombed the territory of Puerto Rico with five supposedly well-meaning, but economically devastating policies. It has:

1. Exempted the Island’s government debt from all U.S. taxes in the Jones-Shaforth Act.

2. Eliminated U.S. tax breaks for private sector investment with the expiration of section 936 of the U.S. Internal Revenue Code.

3. Required the nation to abide by a restrictive trade arrangement.

4. Made the Island subject to the U.S. minimum wage.

5. Enabled Puerto Rico to offer generous welfare benefits relative to income.

While passage of such politically popular laws seems benign on the surface (and have allowed politicians to claim that their efforts have helped the poorest Puerto Ricans), in reality they have deepened the poverty of the very people the laws were supposedly designed to help. The lessons here are so obvious that only the most ardent supporters of government economic control can fail to comprehend them

Tax-Free Debt

By exempting U.S. citizens from taxes on interest paid on Puerto Rican sovereign debt, Washington sought to help the Puerto Rican economy by making it easier and cheaper for the Island’s government to borrow from the mainland. As a result, Puerto Rican government bonds became a staple holding of many U.S. municipal bond funds. As with Fannie Mae and Freddie Mac bonds a decade ago, many investors believed that these Puerto Rican bonds had an implied U.S. government guarantee. This meant that the Puerto Rican government could borrow for far less than it could have without such a belief. However, this subsidy did not grow the Puerto Rican economy, but simply the size of the government, which had the perverse effect of stifling private sector growth.

In contrast to the tax-free income earned by Americans who buy Puerto Rican government bonds, those with the bad sense to lend to Puerto Rican businesses were taxed on the interest payments that they received. Businesses could have used the funds for actual capital investment (that could have increased the Island’s productivity), but instead the money flowed to the Government which used it to buy votes with generous public sector benefits that did nothing to grow the Island’s economy or put it in a better position to repay. That problem was left for future taxpayers who no politician seeking votes in the present cared about.

This dynamic is almost identical to what happened in Greece, where low borrowing costs, made possible by the strong euro currency and the implied backstop of the European Central Bank and the more solvent northern European nations, permitted the Greek government to borrow at far lower rates than its strained finances would have otherwise allowed.

Taxing Private Investment

Perversely, as the U.S. government made it easier for the Puerto Rican government to borrow, it made it harder for the private sector to do so. In 2006 the government ended a tax break that exempted corporate profits earned on private sector investment in Puerto Rico from U.S. taxes. As a result, U.S. businesses that had been making investments and hiring workers on the Island pulled up stakes and moved to more tax-friendly jurisdictions. The result was an erosion of the Island’s local tax base, just as more borrowing (made possible by triple tax-free government debt) obligated the remaining Puerto Rican taxpayers to greater future liabilities.

The Jones Act

The Jones Act, a 1920 law designed to protect the U.S. merchant marine from foreign competition, has had a devastating effect on Puerto Rico, and should be used as a cautionary tale to illustrate the dangers of trade barriers. Under the terms of this horrible law, foreign-flagged ships are prevented from carrying cargo between two U.S. ports. According to the law, Puerto Rico counts as a U.S. port. So a container ship bringing goods from China to the U.S. mainland is prevented from stopping in Puerto Rico on the way. Instead, the cargo must be dropped off at a mainland port, then reloaded onto an expensive U.S.-flagged ship, and transported back to Puerto Rico. As a result, shipping costs to and from Puerto Rico are the highest in the Caribbean. This reduces trade between Puerto Rico and the rest of the world. Since a large percentage of the finished goods used by Puerto Ricans are imported, the result is much higher consumer prices and fewer private sector jobs. Even though median incomes in Puerto Rico are only 63% of the poorest U.S. state, thanks to the Jones Act, the cost of living is actually higher than the average state.

The Federal Minimum Wage

In 1938 the Fair Labor Standards Act subjected Puerto Rico to a federal minimum wage, but it was not until 1983 that a 1974 act, which required that the Island match the mainland’s minimum wage, was fully phased in. The current Federal minimum wage of $7.25 per hour is 77% of Puerto Rico’s current median wage of $9.42. In contrast, the Federal minimum is only 43% of the U.S. median wage of almost $17 per hour (Bureau of Labor Statistics (BLS), May 2014). The U.S. minimum wage would have to be more than $13 per hour to match that Puerto Rico proportion. The disparity is greater when comparing minimum wage income to per capita income.

The imposition of an insupportably high minimum wage has meant that entry level jobs simply don’t exist in Puerto Rico. Unemployment is over 12% (BLS), and the labor force participation rate is about 43% (as opposed to 63% on the mainland) (The World Bank). A “success” by the Obama administration in raising the Federal minimum to $10 per hour would mean that the minimum wage in Puerto Rico would be higher than the current medium wage. Such a move would result in layoffs on the Island and another step down into the economic pit. I predict that it could bring on a crisis similar to the one created in the last decade in American Somoa when that island’s economy was devastated by an unsustainable increase in the minimum wage.

It will be interesting to see if our progressive politicians will have enough forethought and mercy to exempt Puerto Rico from minimum wage increases. But to do so would force them to acknowledge the destructive nature of the law, an admission that they would take great pains to avoid.

Welfare

In 2013 median income in Puerto Rico was just over half that of the poorest state in the union (Mississippi) but welfare benefits are very similar. This means that the incentive to forgo public assistance in favor of a job is greatly reduced in Puerto Rico, as a larger percentage of those on public assistance would do better financially by turning down a low paying job. Because of these perverse incentives not to work, fewer than half of working age males are employed and 45% of the Island’s population lived below the federal poverty line (U.S. Census Bureau, American Community Survey Briefs issued Sep. 2014). According to a 2012 report by the New York Federal Reserve Bank, 40% of Island income consists of transfer payments, and 35% of the Island’s residents receive food stamps (Fox News Latino, 3/11/14).

In other words, Puerto Rico’s problems are strikingly similar to those of Greece. Its government spends chronically more than it raises in taxes, its economy is trapped in a regulatory morass, and its economic destiny is largely in the hands of others.

The solutions to Puerto Rico’s problems are simple, but politically toxic for mainland politicians to acknowledge. Puerto Rico must be allowed to declare bankruptcy, the Federal incentive for the Puerto Rican government to borrow money must be eliminated, Puerto Rico must be exempted from both the Jones Act and the Federal Minimum wage, and Federal welfare requirements must be reduced. Puerto Rico already has the huge advantages of being exempt from both the Federal Income Tax and Obamacare, so with a fresh start, free from oppressive debt and federal regulations, capitalism could quickly restore the prosperity socialism destroyed. With the current incentives provided by Acts 20 and 22 (which basically exempt Puerto Rico-sourced income for new arrivals from local as well as federal income tax – see my report on America’s Tax Free Zone) and with some additional local free market labor reforms, in a generation it’s possible that Puerto Ricans could enjoy higher per capita incomes than citizens of any U.S. state.

If Washington really wanted to accelerate the process, it should exempt mainland residents from all income taxes, including the AMT, on Puerto Rico-sourced investment income, including dividends, capital gains, and interest related to capital investment.

Read the original article at Euro Pacific Capital.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube

“People are said the markets went down because of Greece. I don’t believe that for a minute. I believe markets went down because it’s becoming evident that the Chinese economy is not growing anymore.”

Also from Marc on July 11th

Marc Faber Warning : Global Economy Going in Recession By The End of 2015

The Federal Reserve may embark on more quantitative easing if the S&P 500 falls by 20 percent, according to Faber. In the link just above he also discusses China and Greece with Manus Cranny on Bloomberg Television’s “The Pulse.”

Dr. Marc Faber was born in Zurich, Switzerland and obtained a PhD in Economics at the University of Zurich. Between 1970 and 1978, Dr. Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In 1990, he set up his own business, Marc Faber Limited which acts as an investment advisor and fund manager. Dr. Faber publishes a widely read monthly investment newsletter, “The Gloom Boom & Doom Report,” which highlights unusual investment opportunities, and is the author of several books including Tomorrow’s Gold: Asia’s age of discoverywhich was a best seller on Amazon. Dr. Faber is known for his “contrarian” investment approach and charismatic personality. He became infamous after calling the 1987 crash in US equities.

ATHENS, Greece – “It’s finished. The euro finished. Greece finished.”

ATHENS, Greece – “It’s finished. The euro finished. Greece finished.”

With this apocalyptic shorthand, our taxi driver described the situation in Athens.

The banks here have been closed for two weeks. To try to prop up the crumbling banking system, the government has banned Greek citizens – but not tourists – from withdrawing more than €60 ($67) a day from the ATMs.

The breaking news this morning is that the government and its creditors have cobbled together a deal to keep Greece in the euro zone.

Prime minister Alexis Tsipras has caved in to creditors’ demands on economic reforms. Trouble is his countrymen voted to reject almost the same deal in last weekend’s referendum.

And Tsipras still has to push the reforms through the Greek parliament on Wednesday.

We Hopped on a Plane to Athens…

Like a storm chaser, on Saturday we hopped on a plane from London to Athens to study the tornado moving through downtown Athens.

It would be fun to see so many vanities and pretensions fly high, we thought. At the very least, it would be instructive – useful training for the storms coming elsewhere.

But nothing happened: No twister. No train wreck. No panic in the streets.

From our explorations in the historical Pláka neighborhood – on the slopes of the Acropolis – we found only tourists. And they seem to have no idea that there is a financial crisis going on.

Last night, we went over to the Syntagma Square – the city’s central square – to look for mayhem and chaos. All we found was a squad of police dozing in an armored bus.

ATMs were working; no lines in front of them. Restaurants were about half full.

Nor did we see signs of extravagant spending or reckless investment. In Athens there is no equivalent of the Arc de Triomphe. No Eiffel Tour. No Louvre. No fancy apartments. No gleaming offices.

At least, none that we saw…

Its main achievements were completed more than 2,000 years ago. You wonder how Ancient Greeks did it. The Parthenon – a temple on the Acropolis dedicated to the goddess Athena – required huge investment and meticulous organization.

It is breathtaking… an architectural masterpiece. There is no sign of such capability here today. Instead, Athens is a washed-out, slightly trashy Mediterranean burg.

“Hey, can I help you?”

A seedy-looking man approached. We didn’t know what he was offering, but we didn’t want any.

“No… thanks.”

We turned to walk in the other direction. He followed.

“Hey… what are you looking for? I can help you find it.”

“Well, I’m looking for signs of financial breakdown.”

“Oh, I can help you find drugs… women… gambling. But I don’t know anything about financial breakdowns.”

We gave the man another “thank you” and went off.

Makers and Takers

As you know, Greece is just another front in the Great Zombie War.

The real issue here is the same as all the other fronts: how to keep the credit flowing.

Honest people make. Zombies take.

They take what they can from earnings and savings. But it is not enough. It is credit that keeps them alive.

Zombie businesses borrow more and more to keep the lights on. They pay out big bonuses, and their stock goes up!

Cheap credit keeps the feds in business, too. Practically every government in the world is operating in the red. Take away the red, and zombie programs would have to be curtailed.

Cheap credit funds the layabouts, the chiselers, the lobbyists and lawyers, foolish wars and foolish investments, and all the many millions of people who live at the expense of others.

Want to know if you’re a zombie?

In theory, the test is simple: If no one were forced to support you, would you still have the same income?

If this answer is no, you have been zombified.

But in practice, it can be hard to tell a zombie from an honest living, breathing human being.

Often they don’t even know themselves. Some honest professions, for example, have been almost entirely zombified. So have entire countries.

Greece, for example, has been able to live beyond its means – on credit provided by Northern Europeans.

Many of its people – especially those who work for the government – have gotten used to earning more than they’re worth. (For more on this, scroll down to today’s Market Insight.)

There were few zombies in the world of Pericles, Aristotle, and Euclid. The economy could not support many parasites.

Now, the world is full of them.

Regards,

Bill

original article HERE

The Greek drama, ot Greek Tragedy, continues with a rumored agreement to continue the stimulus in return for promised reforms only to have Greek Prime Minister Alexis Tsipras announce a surprise referendum on July 5: after June 30 which puts the IMF payment into default. Late last week EurAsia Group’s Ian Bremmer remained confident that the Greek Parliament will approve the agreement at the last minute. Meanwhile Greek politicians demonstrate their commitment to election promises of anti-austerity while the Troika talks tough on reforms to appease their own electorate. Monday is the Eurozone Summit while Tuesday the Greek IMF payment will go into default. Next week promises to be a volatile week in the markets with the arrays showing a turning point in many markets on Wednesday.

The Greek drama, ot Greek Tragedy, continues with a rumored agreement to continue the stimulus in return for promised reforms only to have Greek Prime Minister Alexis Tsipras announce a surprise referendum on July 5: after June 30 which puts the IMF payment into default. Late last week EurAsia Group’s Ian Bremmer remained confident that the Greek Parliament will approve the agreement at the last minute. Meanwhile Greek politicians demonstrate their commitment to election promises of anti-austerity while the Troika talks tough on reforms to appease their own electorate. Monday is the Eurozone Summit while Tuesday the Greek IMF payment will go into default. Next week promises to be a volatile week in the markets with the arrays showing a turning point in many markets on Wednesday.

…continue reading this extensive article including market forecasts HERE

If you believe in the legitimacy of Government account , this May men began sitting on fat wallets and women’s purses were stuffed with cash. Auto sales led with the Toyota Camry the leading passenger cars sold and Ford F-150 the top selling vehicle overall in Canada. Japanese cars held the top 6 positions in passenger car sales.

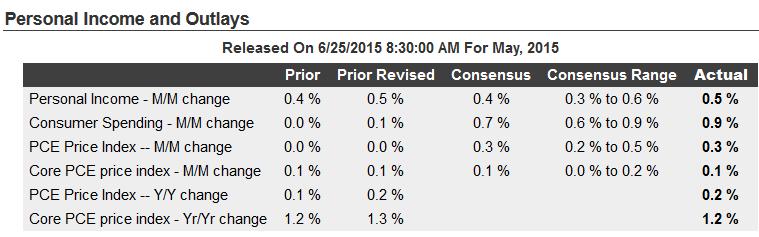

“The consumer came to life in May, boosted by a 0.5 percent rise in personal income and helping to support a 0.9 percent surge in personal outlays that reflects heavy spending on autos and retail goods. And gains are not inflationary, at least yet, based on the very closely watched core PCE price index which edged only 0.1 tenth higher in May and is at a very benign 1.2 percent year-on-year rate which is actually down a tenth from an upward revised April.

Components on the income side are very solid with wages & salaries up 0.5 percent in the month. Both proprietors’ income and rental income show especially strong gains. Spending components show special strength for durables, again tied especially to autos, and also strong gains for non-durables, here tied to higher pump prices. Spending on services once again shows an incremental gain.

Turning back to PCE prices, the overall price index looks a little hot in May at plus 0.3 percent but the year-on-year rate is unchanged at only 0.1 percent. That’s right, that’s the year-on-year rate at only the most incremental level of inflation. And the 1.2 percent year-on-year core appears to be moving in reverse, down 1 tenth in each of the last two reports and further away from the Fed’s 2 percent target.

Consumers, in an expression of their confidence, dipped into their savings to spend, with the savings rate down 3 tenths to 5.1 percent. This is a good report for the bulls, showing a strong non-inflationary bounce for the second quarter. This report won’t be keeping the doves up at night and does not move forward the Fed’s coming rate hike.”

The actual report can be read on the US Department of Commerce’s Bureau of Economic Analysis website: Personal Income and Outlays for May 2015.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair