Currency

Quotable

“One ought never to turn one’s back on a threatened danger and try to run away from it. If you do that, you will double the danger. But if you meet it promptly and without flinching, you will reduce the danger by half.”

Commentary & Analysis

~ Sir Winston Churchill

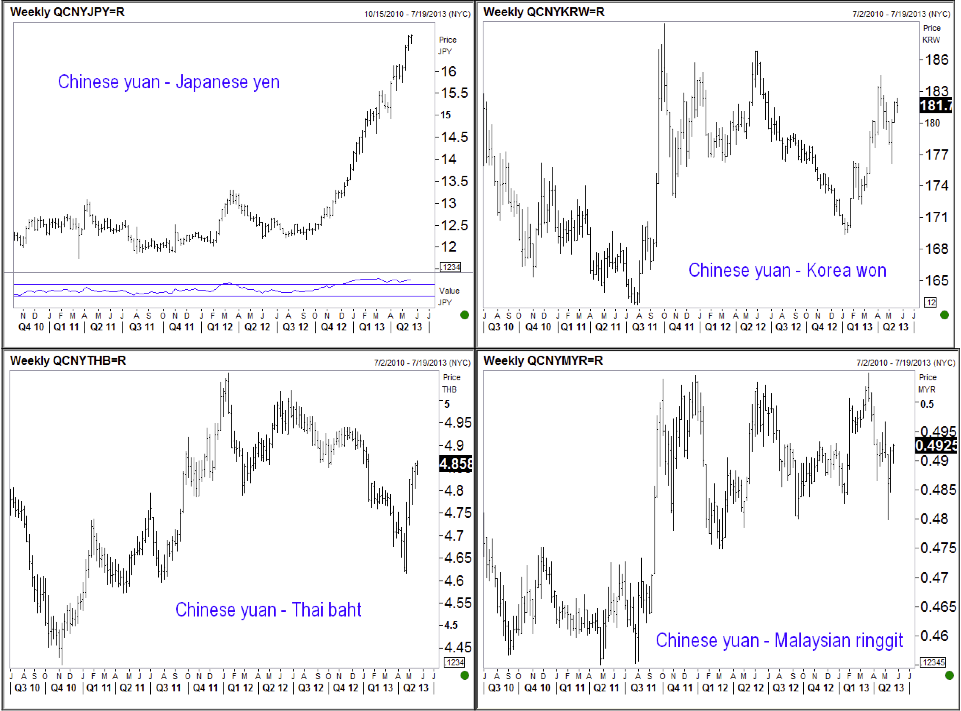

If China Real Estate = Forced Savings…”Danger Will Robinson!”

In case you weren’t aware of it, China’s currency, by virtue of its soft “peg” to the US dollar, is very strong relative to the rest of its Asian competitors, as you can see in the various weekly charts below:

The weakness in the Japanese yen is leading the way of course. The question is: Is this a bad thing for China?

If we assume China is still beholden to the export-cum-investment model, this is likely a “bad” thing. But, if we assume China is and must make that transition we and others have talked about for years—to a more balanced economy whereby households gain a greater share of Chinese wealth relative to targeted industries and sectors—then this relative strength in the yuan is a “good” thing. Why?

1. A stronger currency raises China’s relative purchasing power as it relates to imports. And the China demand engine is badly needed in a world of declining aggregate demand.

2. A relative decline in Chinese exports and its current account surplus and forex reserves by definition represents a lower level of “forced savings.” And if the transition to a more balanced economy whereby households gain a greater share of wealth, savings (throughout the economy, i.e. households and businesses alike) will decline.

Here is the tricky part; I pose it in the form of a question: How does the Party hand over the necessary degree of “freedom” to the household sector, allowing them to spend money more freely on a global basis, which would allow for a faster transition and more normalized economy, and at the same time maintain the “viability” of the Party itself in matters economic?

I may be totally off-base here on my global macro flows, but I think “forced savings” upon the Chinese households (financial repression) to fund the export-cum-investment model is one of the primary drivers of Chinese real estate, i.e. where else can the average Chinese put his/her money? We are told there are three generations of Chinese citizens’ savings invested in real estate.

Put another way, if China’s currency continues to appreciate and Chinese households find other opportunities to invest, some outside China, I would imagine other real estate markets and a host of other asset classes would appear to be a much better relative value than Chinese real estate at the moment.

As you can see, no matter how you slice it or dice it, this “necessary transition” for China presents them with opportuinty and danger. It is a process we all need to continue to watch very closely.

Jack Crooks

Black Swan Capital

Written Summary

Just as the Beatles sent the world into a frenzy in the summer of ‘64, rockstar Prime Minister Shinzo Abe’s latest hit “Abenomics,” is taking Japan by storm. Since announcing his economic jumpstart policies back in November, the Nikkei (^N225) has surged 70%, and now comes fresh evidence that the economy has improved as well, with GDP climbing higher due to strong exports and factory output.

Economists and investors may be praising the sweet tunes of “Abenomics,” however the successes are coming at what some are saying is a steep cost. “[Abenomics] has made the stock market go up quite a lot, it’s been dramatic, but it’s made the currency collapse,” legendary investor Jim Rogers, says in the attached video.

“The [Yen], which is one of the major currencies of the world, has collapsed 27% in no time,” Rogers notes. “It’s a very, very dangerous move.”

Since the Yen blasted through 100 parity level with the U.S. dollar, its slide has continued to a new 4-1/2 year low.

As a general rule, Rogers is skeptical of governments that devalue their currencies. “I know the government is reporting that [the Yen’s] move is good, but I don’t trust governments. I don’t trust our government, their government, or anybody else. Their government is as good at lying as ours is.”

Rogers, who started the legendary Quantum Fund with George Soros, says the Japanese government is being coy about the deleterious effects of the Yen’s slide because Mr. Abe wants to win elections this summer, and it will ultimately be the Japanese citizens who will be left holding the bag.

“One hundred twenty-five million Japanese [stand to lose the most] because of inflation. Everything Japan imports, they import a lot of stuff, is going to go up dramatically in price, everything is going to go up,” says Rogers. “So the Japanese will suffer, but… stockbrokers will do better, currency traders will do better.”

But Rogers isn’t about to shy away from Japanese equities due to his distaste for the Yen’s demise.

“I still own Japanese shares, I sold some last week, not all, but some,” he says. “If [Japanese equities] drop down for some reason conceivably I would buy them back, but I don’t know what would make them go down though because there’s money printing everywhere.”

There are several indications that the currency war is heating up, the gloves are coming off and new players are piling into the barroom brawl. First, Australia unexpectedly cut interest rates, then both the Swedish and New Zealand central bank governors were making their moves. Way down under, New Zealand’s central bank last week acknowledging that it had intervened in foreign exchange markets to try to fight any further appreciation of the country’s currency, known as the kiwi. The New Zealanders are worried about a runaway property market driven by global money rushing into the country

Wait a minute… that’s exactly the same scenario in Israel

This week the Bank of Israel stepped up its efforts to curb the appreciation of the shekel surprising the markets by unexpectedly cutting its interest rate and announcing a program to purchase foreign currency. A weaker currency boosts exports, driven by cheaper prices. The smaller economies are reacting to all the quantitative easing by the world’s large economies.

Israel’s central bank, headed by Stanley Fischer, one of the most accomplished central bankers in the world, cut the key interest rate by a quarter of a percentage point to 1.5% to a three-year low.

Fischer told Bloomberg that the move came “in light of the continued appreciation of the shekel, taking into account the start of natural gas production from the Tamar gas field, interest rate reductions by many central banks – notably the European Central Bank, the quantitative easing in major economies worldwide and the downward revision in global growth forecasts.”

Despite the global financial threats, the Israeli economy is still in the black and healthier than the economies of many European countries. The shekel has risen by nearly 9% over the past six months, making it one of the best-performing currencies in the world, after the Mexican peso. Israel’s central bank also plans to buy around $2.1 billion in foreign currencies.

Israel’s economy is heavily dependent on exports, and a strong shekel weakens the competitiveness of Israel’s products abroad.

It was Japan this year that shot off the latest round in the currency war after announcing monetary stimulus of historic proportions. Recent steps by the world’s third-largest economy have become a central concern. The impact of the country’s aggressive new monetary policy has been making central bankers around the world lose sleep. Is the Bank of Japan trying to influence exchange rates to give its exporters an advantage? Other countries might react in kind, which is exactly what happens in currency wars.

Actually, this is not surprising to us. The global increase in the money supply and lowering of interest rates is not surprising because countries will have to keep doing that in order to keep their exports competitive. It is a currency war and those who inflate first, get the most benefits. They are short-lived because other countries will follow and the ultimate result will eventually be huge inflation on a global scale, but, again, on a short-term basis, the monetary authorities are pressed not to stay behind others. The comments about the lack of currency war are not surprising either. Speaking publicly about it would simply encourage other countries to join it sooner, and those that are already printing more money don’t want that to happen as it means that the above-mentioned advantage that they gained would disappear.

Implications for gold? Bullish in the long run, nonexistent in the short run.

As we can see, the great fundamental outlook for precious metals is intact. Let’s move on to the chart section of today’s essay to see how gold’s current technical situation looks like and therefore how gold can trade in the following weeks. Before we proceed to the yellow metal itself, let us begin with the Euro Index long-term chart (charts courtesy by http://stockcharts.com.)

The index has declined for the past two weeks and it seems now that we should consider the possibility that the head-and-shoulders pattern will be completed here. Such a completion would take the Euro Index much lower.

The size of the projected decline after the breakdown and completion of the pattern is roughly the same size as the height of the head in the pattern. If this decline is attached to where the breakdown occurred, the projected downside target level will be about equal to the 2012 low (in the 121 – 122 area). Such a move would likely contribute to a USD Index rally. All of this could also be bearish for gold in the medium term if it all does indeed materialize.

Let’s move on to gold’s very long-term chart now. (Click HERE or on the chart for larger version)

In this chart, we see a situation quite similar to the declines to 2008, where a sharp pullback was followed by a continuation of the severe decline. The most bearish factor here is the shape of the decline, which is a reverse parabola. This formation results in accelerated declines and makes it difficult to tell how low prices will go. Although the declines will likely end shortly, the increased volatility could result in prices moving very low quickly while still being in tune with the trading pattern. This reverse parabola has been in place since last October.

The very long-term cyclical turning point suggests that a local bottom will be seen soon – within the next month, probably about 2 weeks from now. Keeping both of these factors in mind, we should prepare for even bigger declines.

Let us have a look at the Dow to gold ratio chart, as an important technical development took place there.

Here, we saw an important breakout above the declining long-term resistance line. This has bearish implications for gold. Please note that the breakout above the previous – much less significant – resistance line (the red declining line on the above chart) was followed by major declines in gold.

The next resistance level for this ratio is at 12.5 and with it currently at 11, declines in gold will surely be needed in addition to higher stock prices in order for the ratio to move this much higher (it seems that a move higher in the general stock market will not be enough for the ratio to move that high soon). The implications are, of course, bearish.

Summing up, the situation remains bullish for the USD Index. The recent declines in the Euro Index along with the breakout in the USD Index will likely keep the current bullish outlook in place for the coming weeks. The implications of the bullish situation here, especially for the medium term, are bearish for the precious metals. Gold prices declined last week and pulled back on Thursday but it still does not seem that this period of decline is completely over.

To make sure that you are notified once the new features are implemented, and get immediate access to our free thoughts on the market, including information not available publicly, we urge you to sign up for our free gold newsletter. Sign up today and you’ll also get free, 7-day access to the Premium Sections on our website, including valuable tools and charts dedicated to serious Precious Metals Investors and Traders along with our 14 best gold investment practices. It’s free and you may unsubscribe at any time.

Thank you for reading. Have a great and profitable week!

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Silver Investment & Gold Investment Website – SunshineProfits.com

Bloomberg is reporting on the rising number of hedge funds shorting gold:

Gold Bear Bets Reach Record as Soros Cuts Holdings

Hedge-fund managers are making the biggest ever bet against gold as billionaire George Soros sold holdings last quarter and Goldman Sachs Group Inc. predicted more declines after the longest slump in four years.

The funds and other large speculators held 74,432 so-called short contracts on May 14, U.S. Commodity Futures Trading Commission data show. That’s the highest since the data begins in June 2006 and compares with 67,374 a week earlier. The net-long position dropped 20 percent to 39,216 futures and options, the lowest since July 2007.

Gold prices that surged sixfold in the past 12 years fell 19 percent in 2013, including a seven-session slump through May 17 that was the longest since March 2009. Soros joined funds managed by Northern Trust Corp. and BlackRock Inc. in cutting holdings of exchange-traded products in the first quarter. ETP assets are now at the lowest since July 2011 after some investors lost faith in gold as a store of value amid improving economic growth, low inflation and a rally in equities.

“Gold has faced disappointment after disappointment,” said John Stephenson, a senior vice president and fund manager who helps oversee about C$2.7 billion ($2.65 billion) at First Asset Investment Management Inc. in Toronto. “It’s had a 12-year run, but the whole fear-mongering that the world is going to end is just not working. So, I think that any last vestige of an investment thesis for gold has been stripped.”

Soros Fund Management LLC lowered its investment in the SPDR Gold Trust, the biggest bullion ETP, by 12 percent to 530,900 shares as of March 31, compared with three months earlier, a Securities and Exchange Commission filing showed May 15. The reduction followed a 55 percent cut in the fourth quarter last year. Paulson & Co., the top investor in the SPDR fund, maintained a stake of 21.8 million shares, now valued at $2.86 billion. Global ETP holdings slid 16 percent to 2,207.1 metric tons this year, valued at $96.5 billion.

Goldman Outlook

Gold’s slump “has been faster than we expected,” Goldman analysts led by Jeffrey Currie wrote in a May 14 report. A further drop in ETP holdings would “continue to precipitate this decline,” said the analysts, who forecast prices at $1,390 in 12 months. The metal will get “crushed” and trade at $1,100 in a year and below $1,000 in five years as inflation fails to accelerate, Ric Deverell, the head of commodities research at Credit Suisse Group AG, said in London on May 16.

Physical buying will help to support prices, said Paul Dietrich, the chief executive officer of Middleburg, Virginia-based Fairfax Global Markets, which oversees about $120 million.

India Premiums

Gold premiums in India, the world’s biggest buyer, more than doubled to $40 an ounce May 15 from $17 to $18 a day earlier, according to Bachhraj Bamalwa, a director at the All India Gems & Jewellery Trade Federation. China’s bullion demand jumped to a record 294.3 tons in the first quarter, the World Gold Council said in a report May 16.

Prices surged 54 percent since the end of 2008 as central banks printed money on an unprecedented scale to boost growth. The Federal Reserve is buying $85 billion of assets a month to stimulate the world’s biggest economy, while Japan is making monthly bond purchases of more than 7 trillion yen ($67.8 billion).

“The case for gold is still there,” Dietrich said. “All the central banks are joining in a massive printing of money. Physical demand may be helping provide a floor on prices, and while there’s not a lot of downside risk right now to gold, there is a lot of upside potential.”

……some thoughts on the above from John Rubino of DollarCollapse.com HERE

Based on both recent history and mainstream economic theory the past few years should not have been possible. When you cut interest rates to near-zero, run deficits of 10% of GDP and buy up every government bond in sight with newly created currency, you get a boom, end of story. That’s just the way capitalism works.

But this time was different. After four years of QE and ZIRP and all the other easy-money acronyms, we entered the month of May with Europe in a deepening recession and the US recovery petering out.

The culprit? The one piece of the puzzle that governments can’t control: the velocity of money. This is simply a measure of how quickly holders of currency, i.e., banks, consumers, businesses, hand their currency off to someone else. The faster and more frequent the hand-offs, the more stuff gets bought and the more robustly an economy grows. But after their 2009 near-death experience, the world’s banks have been in no mood to lend. Instead, they’ve been sticking all the new currency their governments have been giving them under the proverbial mattress. This reluctance to lend means record low money velocity and little or no economic growth.

But in just the past month something fundamental has changed. US home sales and prices have accelerated, with prices returning to 2006 levels in some markets and bidding wars, flippers and interest-only mortgages once again becoming common. Stock prices pierced old records and then spiked rather than corrected. Suddenly we’re back in an asset-driven boom.

…..read it all HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair