Quotable

“One ought never to turn one’s back on a threatened danger and try to run away from it. If you do that, you will double the danger. But if you meet it promptly and without flinching, you will reduce the danger by half.”

Commentary & Analysis

~ Sir Winston Churchill

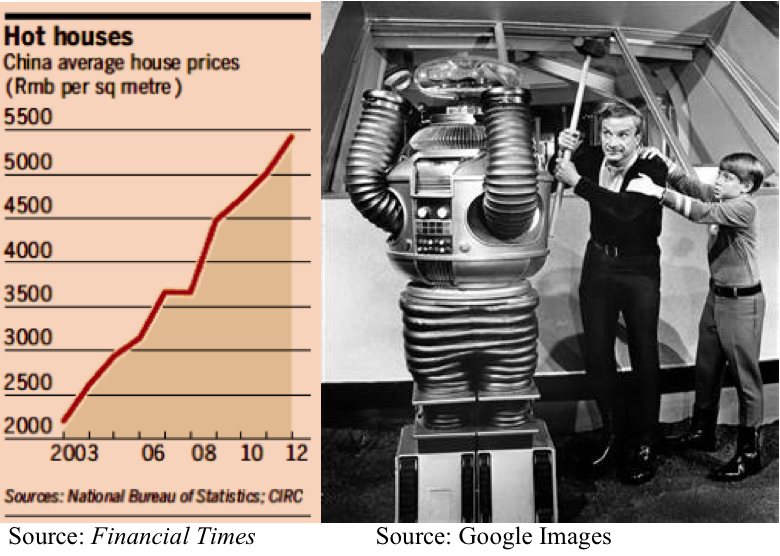

If China Real Estate = Forced Savings…”Danger Will Robinson!”

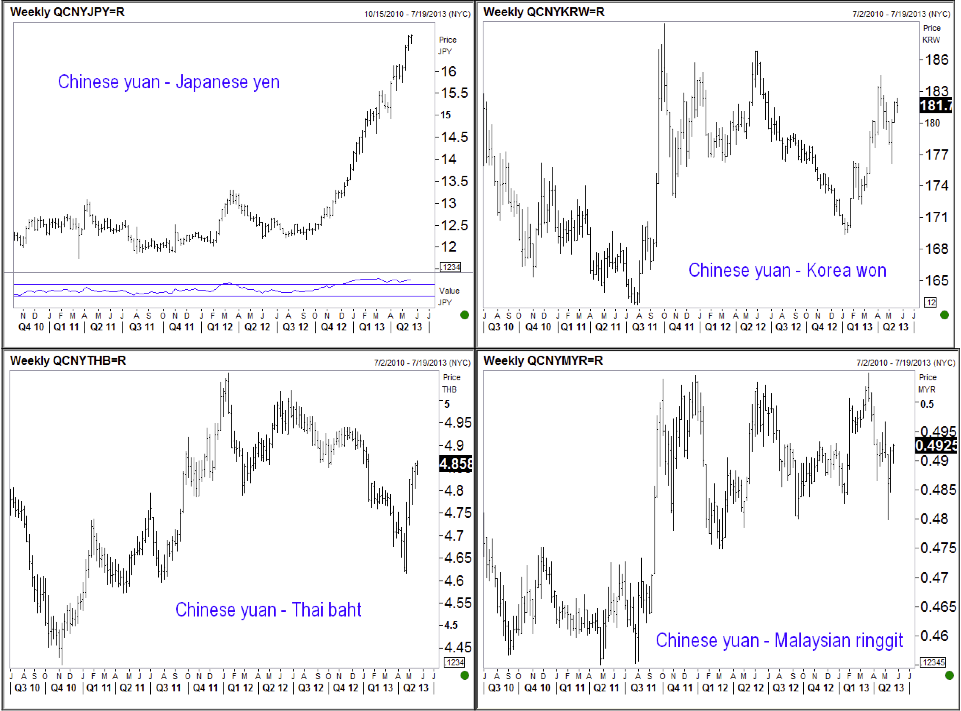

In case you weren’t aware of it, China’s currency, by virtue of its soft “peg” to the US dollar, is very strong relative to the rest of its Asian competitors, as you can see in the various weekly charts below:

The weakness in the Japanese yen is leading the way of course. The question is: Is this a bad thing for China?

If we assume China is still beholden to the export-cum-investment model, this is likely a “bad” thing. But, if we assume China is and must make that transition we and others have talked about for years—to a more balanced economy whereby households gain a greater share of Chinese wealth relative to targeted industries and sectors—then this relative strength in the yuan is a “good” thing. Why?

1. A stronger currency raises China’s relative purchasing power as it relates to imports. And the China demand engine is badly needed in a world of declining aggregate demand.

2. A relative decline in Chinese exports and its current account surplus and forex reserves by definition represents a lower level of “forced savings.” And if the transition to a more balanced economy whereby households gain a greater share of wealth, savings (throughout the economy, i.e. households and businesses alike) will decline.

Here is the tricky part; I pose it in the form of a question: How does the Party hand over the necessary degree of “freedom” to the household sector, allowing them to spend money more freely on a global basis, which would allow for a faster transition and more normalized economy, and at the same time maintain the “viability” of the Party itself in matters economic?

I may be totally off-base here on my global macro flows, but I think “forced savings” upon the Chinese households (financial repression) to fund the export-cum-investment model is one of the primary drivers of Chinese real estate, i.e. where else can the average Chinese put his/her money? We are told there are three generations of Chinese citizens’ savings invested in real estate.

Put another way, if China’s currency continues to appreciate and Chinese households find other opportunities to invest, some outside China, I would imagine other real estate markets and a host of other asset classes would appear to be a much better relative value than Chinese real estate at the moment.

As you can see, no matter how you slice it or dice it, this “necessary transition” for China presents them with opportuinty and danger. It is a process we all need to continue to watch very closely.

Jack Crooks

Black Swan Capital