Charts courtesy of Bloomberg.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

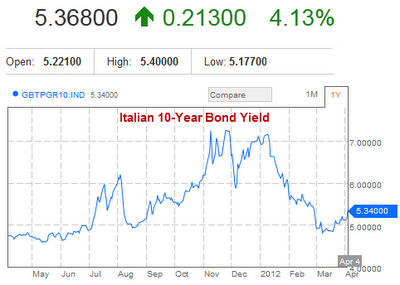

Sovereign Bond Yields Sharply Higher in Spain, Italy, Portugal Curve Watcher’s Anonymous has an eye on European sovereign bond yields. In the absence of another huge LTRO program from the ECB, and perhaps even with another LTRO program, yields in Spain, Portugal and Italy should head North. The LTRO is not going to trump long-term fundamentals which are downright horrible.

Here are a few charts to consider.

Spain 10-Year Yield

Italy 10-Year Yield

Portugal 10-Year Yield

The Hera Research Newsletter is pleased to present a fascinating interview with Martin A. Armstrong, founder and former Head of Princeton Economics, Ltd. In the 1980s, Princeton Economics became the leading multinational corporate advisor with offices in Paris, London, Tokyo, Hong Kong and Sydney and in 1983 Armstrong was named by the Wall Street Journal as the highest paid advisor in the world.

As a top currency analyst and frequent contributor to academic journals, Armstrong’s views on financial markets remain in high demand. Armstrong was requested by the Presidential Task Force (Brady Commission) investigating the 1987 U.S. stock market crash and, in 1997, Armstrong was invited to advise the People’s Bank of China during the Asian Currency Crisis.

Based on a study of historical gold prices and financial panics, Armstrong developed a cyclical theory of commodity prices, which lead to the pi-cycle economic confidence model (ECM), used to make long term forecasts. Using the ECM, Armstrong predicted both the high-water mark of the Nikkei in 1989, months ahead of time, and the July 20, 1998 high in the U.S. equities market, as well as a major top in financial markets on February 27, 2007. The ECM was called “The Secret Cycle” by the New Yorker Magazine and Justin Fox wrote in Time Magazine that Armstrong’s model “made several eerily on-the-mark calls using a formula based on the mathematical constant pi.” (Pg 30; Nov. 30, 2009).

…..read the whole interview HERE (scroll down a bit)

The Key Points:

“The crucial question over the next decade is not “where will my returns be highest?” but “where will I lose the least money?. The inevitable crash, or “rebooting the computer,” will simply have to be endured. He advises how investors should play this situation:

Equity-like corporate bonds – 25% of a portfolio. Another 25% made up of stocks, especially in emerging markets, with a further 25% in precious metals (which tend to be severely underweighted in a typical pension fund). Real estate in certain areas (such as Asia) for the remainder. He added that US house prices are looking decidedly cheap and that an investment in remote farmland could pay off, as growing social tensions could make urban life intolerable.

Marc Faber: Continuing Financial Crisis Must Be Endured – (The Entire Article)

Marc Faber, editor of “The Gloom, Boom and Doom Report,” kicked off the CFA Institute Middle East Investment Conference by quoting Ernest Hemingway who said, “The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring permanent ruin.” On this downcast note, Faber attacked short-term Keynesian spending and reviewed the implications for investors of the accelerating shift of world economic and political power from the developed countries to the developing world.

Central bank action to cut interest rates, whilst intended to boost consumption and hence economic growth, has had unintended and severely negative consequences. Faber argued that “dollar bills dumped by helicopters” all over the US have not been channelled into housing, as hoped, but into other more speculative asset classes, particularly commodities such as precious metals and oil. He added that expansionist monetary policies have contributed to higher financial and economic volatility, in addition to inflation. Since greater money supply does not flow evenly across sectors, this gives rise to asset bubbles, which are not easy to identify.

For Faber, at the start of any bubble, “promoters have the vision, and investors have the money.” But the reverse occurs as the bubble bursts: the promoters end up with the money, while most people lose out. Current negative real interest rates, which make cash a safe, but poorly-returning investment, penalize savers, and encourage them to speculate. But Faber asked, “Is deflation such a bad thing?” During deflationary periods in the nineteenth century, real per capita income apparently increased faster than it does now.

Faber also noted that excessive debt always contributes to risk. For example highly leveraged US developers became insolvent when the housing bubble burst, in contrast to their more conservative Hong Kong counterparts who managed to remain solvent. Borrowing has increased just to maintain a standard of living. In 1980, US debt/GDP stood at 140%. Now it is approaching 400%, if unfunded liabilities such as social security and Medicare are taken into account. As a result, adjusted US government debt now exceeds $15 trillion, and continues to rise. US spending is up, but taxes are down. Faber contended that the vast majority of tax revenue goes to mandatory expenditures such as medical care, social security and interest expense rather than to capital formation. Given these imbalances Faber is unsurprised that the quality of US government bonds has been called into question.

By slashing interest rates, governments have also contributed to higher commodity prices, especially oil prices, according to Faber. Any intended boost to consumption is undone by higher energy prices which act as an additional tax on the consumer.

Adding that the G7’s exports continue to decline, Faber contrasted this with climbing developing world exports, resulting in rapidly growing reserves among emerging economies. These reserves will be spent on scarce resources such as precious metals and other commodities. Faber believes that oil demand among the emerging economies now exceeds that of the developed world. China is increasingly absorbing the world’s resources to feed its growth. It is positioning itself carefully as a global economic and political power, assiduously dominating shipping lanes, forging alliances with neighboring states, and investing heavily, so much so that Faber argues China has now got its own domestic credit bubble. Faber sees parallel scenarios being played out in India, Southeast Asia and Latin America. The growing economic power of these nations will inevitably lead to further geopolitical tensions where the MENA region is a potential powder keg.

So how should investors play this situation? Faber states that diversification is key alongside low leverage. His recommendations are as follows: cash and bonds are not hugely attractive, given negative real interest rates, but equity-like corporate bonds could form 25% of a portfolio. Another 25% could be made up of stocks, especially in emerging markets, with a further 25% in precious metals (which tend to be severely underweighted in a typical pension fund). Real estate in certain areas (such as Asia) could make up the remainder. He added that US house prices are looking decidedly cheap.

Faber closed his speech by emphasizing that the crucial question over the next decade is not “where will my returns be highest?” but “where will I lose the least money?” In fact, he believes that losses of 50% should be considered as a relative success. He advised that an investment in remote farmland could pay off, as growing social tensions could make urban life intolerable. In his view the welfare state has evolved from the many helping the few to the few helping the many and that the inevitable crash, or “rebooting the computer,” will simply have to be endured. Whether this crisis occurs soon, as further credit expansion is voluntarily abandoned, or occurs later, as the currency system meets final and total catastrophe, Faber cannot predict.

Due to an overwhelming number of inquiries over the past few days I am sending out this brief market update, which I know is a few weeks overdue for sure.

The Spring market for purchase and sale has been extremely busy, as has the refinance side of things, as such finding the time to put something detailed together has been a challenge. My apologies.

Every Spring for the past three years we seem to have the same situation, it is starting to feel like that Bill Murray Movie ‘Groundhog Day’.

A few Big Banks get their economists on the news telling folks that rates are moving up and they had better lock in, get out of the ‘risky’ (non-profitable) variable and into a nice ‘safe’ (profitable) fixed rate product.

Then each year we see rates trickle back down to the same or lower levels as they were at before. Lately all of the media attention has been on a 4 year fixed rate product that has in fact been around for months, and on a very limited ‘no-frills’ 5 year special – which ironically enough was available in November 2011 through the broker channel but received no fanfare.

This Spring feels no different than the last three because bond markets, stock markets, and the world economy is not what is being talked about as the impetuous for a rate increase, instead it is the Banks ending a 4 year fixed rate special…

There is still a 3 year 2.79, the 5 year rate remains at or near 3.19 with most lenders.

You can watch the long version at this link and gain a better understanding as to just what is going on.

Or the short version;

Prime is going nowhere, enjoy the variable. Fixed rates will move around a little bit, however have a strong likelihood of staying very close to where they are.

Kind Regards

Dustan

“The (Trade) data has proven my point. Just as the prosperity of the ’90s and ’00s blinded us to the coming crisis in ’08, the current talk of recovery is distracting investors, commentators, and even academics from rapidly degrading fundamentals. This course can only lead to a greater crisis, that I have dubbed in my latest book “The Real Crash.”

This article was revised on March 23, 2012.

Earlier this month, the Department of Labor reported that 227,000 new jobs were added to the economy in February, marking the third consecutive month of positive jobs growth. Many observers have taken the news as evidence that the recovery is underway in earnest, helping send the S&P 500 index to the highest level in nearly five years. However, the very same day, the Commerce Department reported that after surging for much of the last year, the U.S. trade deficit increased to $52.6 billion for January – the largest monthly trade gap since October 2008. This second data point should dampen enthusiasm for the first.

From 2005 through mid-2008, those monthly figures almost always topped $50 or $60 billion, setting a monthly record of $67.3 billion in August 2006. But when the housing and credit markets imploded, attention was focused elsewhere. At that time, I was one of the few economists to raise a red flag about the dangers of growing trade deficits. In any event, the faltering economy took a huge bite out of imports, pushing the trade deficit down 45% in 2009. Even those people who were still paying attention to trade assumed that the problem was solving itself.

However, after reaching a monthly low of $35.7 billion in May of 2009, the trade deficit began to grow again, expanding 31% in 2010 and 12% in 2011. While the $52.6 billion deficit in January is still about 10% below the monthly average seen in 2006-2008, if GDP continues to nominally expand, as many assume it will, we may soon find ourselves in the exact same place in terms of trade that we were before the financial crisis began. That’s not a good place to be.

If the jobs that we have created over the last few years had been productive, our trade deficit would now be shrinking, not growing. But the opposite is happening. These jobs are being created by the expenditure of borrowed money, and are not helping to forge a newer, more competitive economy. In the years before the real estate crash, our economy created millions of jobs in construction, mortgage finance, and real estate sales. But as soon as the bubble burst, those jobs disappeared. Today’s jobs are similarly being built as a consequence of another bubble, this time in government debt. And, likewise, when this bubble bursts they too will vanish.

Throughout much of the last decade, I had continuously warned that the growing trade deficit was an unmistakable sign that the U.S. was on an unsustainable path. To me, monthly gaps of $60 billion simply meant that Americans were going deeper into debt (to the tune of $2,400 per year, per citizen) in order to buy products that we were no longer productive enough to make ourselves. I pointed out that America had become an economic juggernaut in the 19th and 20th centuries on the back of our enormous trade surpluses, which allowed for growing wealth, a stronger currency, and greater economic power abroad. This is exactly what China is doing today. Deficits reverse these benefits. (To learn how China is spending its surplus, see my latest newsletter.)

My critics almost universally dismissed these concerns, typically saying that our trade deficits resulted from our economic strength and that they were a natural consequence of our status at the top of the global food chain. I pointed out that even highly developed, technologically advanced economies still need to pay for their imports with exports of equal value. Instead, all that we have been exporting is debt and inflation.

The financial crisis initiated a painful, but needed, process whereby Americans spent less on imported products while manufacturing more products to send abroad. But the countless government fiscal and monetary stimuli stopped this healing process dead in its tracks. Government borrowing and spending redirected capital back into the unproductive portions of our economy. Health care, education, government, and retail have all expanded in the last few years. But manufacturing has not grown at the pace needed to solve the trade problem. In short, these jobs are creating more consumers and less producers, they are making us poorer rather than richer.

Job creation at home has been like vegetation sprouting along the banks of rivers of stimulus. These artificial channels may help temporarily, but they prevent trees from taking root where they are needed most. Our economy has yet to restructure itself in a healthy manner. The recession should have forced us to address the problem of persistent and enormous trade deficits. We have utterly failed to do this. So while the job numbers look good for now, the pattern is ultimately unsustainable.

The last time the monthly trade deficit was north of $50 billion, the official unemployment rate was under 6% and our labor force was considerably larger. Should this artificial recovery actually return millions of unemployed workers to service-sector employment, our monthly trade deficits could go much higher – perhaps eclipsing the previous records of 2006. It is possible that the annual deficits could top the $1 trillion mark, thereby joining the federal budget deficit in 13-digit territory.

Also, last week, we got news that our fourth quarter current account deficit widened 15% to just over $124 billion. The $500 billion of annual red ink is actually reduced by a $50 billion surplus in investment income (resulting primarily from foreign holdings of low-yielding US Treasuries and mortgage-backed securities – however, when interest rates eventually rise, this surplus will quickly turn into a huge deficit). At anything close to a historic average in employment and interest rates, today’s structural imbalances could produce annual current account deficits well north of $1 trillion. As higher interest rates would also swell the federal budget deficit, it is worth asking ourselves how long the world will be willing to finance our multi-trillion dollar deficits?

Back in the late 1980s, when annual trade and budget deficits were but a small fraction of today’s levels, the markets were rightly concerned about America’s ability to sustain its twin deficits. This anxiety helped lead to the stock market crash of 1987. But with the boom of the ’90s, all talk of trade deficits was dropped. Though I spoke out about the danger of having consumption chronically outstripping our productivity, the general feeling of prosperity meant my warnings fell on deaf ears – even as the deficit figures hit all-time record highs. This was a major factor in the economic implosion of 2008. However, even when the imbalance had reared its head, mainstream economics predicted that the economic contraction would slow consumption sufficiently to significantly close the gap. Once again, I took to the airwaves warning that if the government tried to solve the crisis by encouraging consumption instead of production, the trade gap would only get worse – causing a greater crisis in the near future.

The data has proven my point. Just as the prosperity of the ’90s and ’00s blinded us to the coming crisis in ’08, the current talk of recovery is distracting investors, commentators, and even academics from rapidly degrading fundamentals. This course can only lead to a greater crisis, that I have dubbed in my latest book “The Real Crash.”

To save 35% on Peter Schiff’s new book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, pre-order your copy today.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

A sane voice in a scrambled investment world.

~ Ed R.

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair