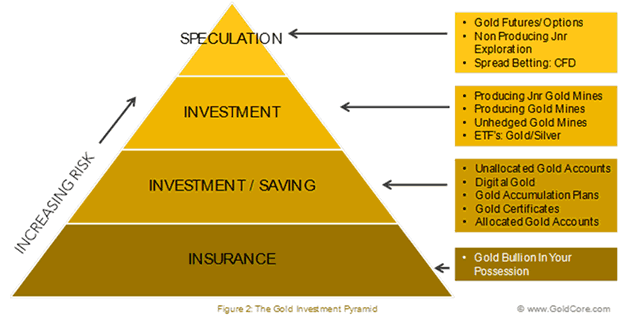

Asset protection

Special Guest: Mark O’Byrne feels that holding a Degree in Greek and Roman Civilization with a focus on their economic and monetary history, gives O’Byrne insights into the cyclical nature of societies that few other writers have. It is these insights that Mark shares in this 42 minute video. Bank Bail-Ins are only a modern day indicator of financially collapsing societies. “Unfortunately, we don’t learn the lessons of history to our own downfall!”

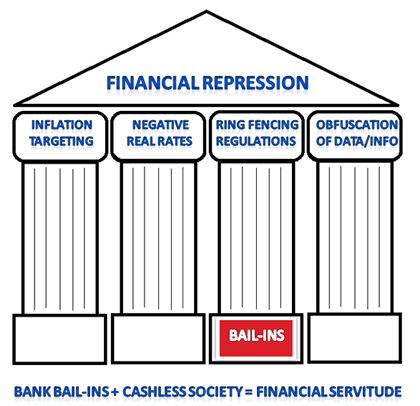

Financial Repression

“Given the large amount of debt in the world today we are seeing almost ‘anti-free market philosophies’ whereby the governments don’t like price signals and the pricing mechanism, so they are trying to repress this to repress interest rates.”

“Given the large amount of debt in the world today we are seeing almost ‘anti-free market philosophies’ whereby the governments don’t like price signals and the pricing mechanism, so they are trying to repress this to repress interest rates.”

“By artificially suppressing the pricing mechanism, similar to forcing an inflated beach ball under the water, it will shoot up in another direction and can go in the opposite direction to what is initially intended!”

Bank Bail-Ins

“We are told Bail-Ins are to protect the taxpayer from the government having to bail-out the banks. But the depositors are the tax payers? Bail-Ins are just to protect the Senior Secured Debt holders!”

This is wrongful deception as people belief their money is safe in the bank It is intended to protect the assets of the Senior Secured Creditors within the banks capital structure. Private individuals and depositors are not holders of Senior Secured Credit to the banks which is strictly the relm of select international banks

Confiscating Depositor Funds Means Deflation

“If you confiscate depositors funds (in a Bail-In) you will cause deflation like you would not believe!”

If you follow Mark O’Byrne’s analysis you quickly realize that Bail-Ins are both economically very dangerous and basically nothing more than regulations to protect elements of the bank financial structure. The question may be: are regulations today to protect tax payers from the banks or to protect the banks from taxpayers (depositors)?

“Maybe today we need to come to the obvious realization that the government is no longer regulating the banks, but rather the banks are regulating the government!” Gordon T Long

International Diversification is The Answer – While the Doors are Still Partially Open

….and much, much more in this fact filled 43 minute Video.

Mark O’Byrne, Founder & Research Director, Goldcore. Mark O’Byrne founded GoldCore more than 10 years ago and today it has clients in over 45 countries. Mark contributes to media internationally and takes part in the Reuters, CNBC and Bloomberg gold and precious metal surveys.

Mark O’Byrne, Founder & Research Director, Goldcore. Mark O’Byrne founded GoldCore more than 10 years ago and today it has clients in over 45 countries. Mark contributes to media internationally and takes part in the Reuters, CNBC and Bloomberg gold and precious metal surveys.

The Greek default is merely the opening act of the worst sovereign-debt crisis in history. By the time it comes to its conclusion, roughly five years from now, the crisis will have enveloped — and destroyed — the Western world governments of Europe, Japan and the United States.

Government (sovereign) bond markets will be destroyed. So much so that in the June issue of my Real Wealth Report, I told my subscribers that …

Over the next few years I expect government bonds to easily lose as much as 50 percent of their value, and possibly much more. No amount of yield they could possibly offer will save you. Not even if you live to 200 years old.

Owning any sovereign debt of Europe, Japan, or the United States, I said, would be akin to creating a cemetery for your wealth.

From Greece, the crisis will spread to the other heavily indebted countries of Europe and the European Union.

Take Italy, for instance, which owes 32 percent more than its economy produces in a year. Portugal, 30 percent more. Cyprus, 8 percent more. France, indebted to the tune of 98 percent of its GDP. Ireland, 110 percent.

And those figures don’t even include “unofficial” debts and IOUs, which are multiples higher.

As Europe starts to go down the drain, the crisis will then spread to Japan, where government debt is a whopping 230 percent of the country’s GDP.

And once it becomes obvious that Japan too will eventually default, Washington will no longer be spared.

The most indebted government in the history of civilization, Washington, is in debt to the tune of more than $200 TRILLION — more than ELEVEN times the entire output of our economy.

Let me give you a little more insight on the sovereign debt crisis that’s now starting. Also from my June Real Wealth Report, the big question I pose — and answer — is this …

Where Will the Massive Capital That Flees Government Bonds Go?

The frightened trillions that will stampede out of government bond markets has to go somewhere. So let’s trace it out logically. Will the capital that flees government bonds in Europe, Japan and the United States go to …

A. Cash under the mattress? Some of it, yes. But certainly not the bulk. Savvy investors always want to put their money to work somewhere for some yield and potential gains — even in the worst of times.

B. The stock market? Yes, a major portion of it will be invested in the U.S. stock market. We’ve already seen it impact the stock market. It’s the chief reason the major indices are so firm.

B. The stock market? Yes, a major portion of it will be invested in the U.S. stock market. We’ve already seen it impact the stock market. It’s the chief reason the major indices are so firm.

It does not preclude a selloff in stocks, which I still fully expect. Especially as jitters over a looming Fed rate hike continues.

But in the longer run, the implosion of government bond markets is going to be extremely bullish for the U.S. stock market.

The U.S. stock markets are the last bastion of capitalism, and the deepest liquid market on the planet.

C. Real estate? Absolutely. Don’t fall for any claims that rising interest rates — as a result of falling bond prices — will kill the real estate market again. It won’t. It will largely have the opposite impact, driving real estate prices higher!

How so? It’s simple: As the cost of mortgage money begins to rise, pent up demand for property will come pouring out of the woodwork. After all, if rates are going to rise, then you’re far better off buying now rather than later.

Naturally, different locations in the U.S. and around the world will fare differently. And you want to buy real estate based on location.

But to think that real estate will implode as interest rates start to rise and the sovereign bond markets implode is simply dead wrong. Real estate, as a tangible asset, is going to do just fine, opening up all kinds of new opportunities for you.

D. Foreign stock markets? Over the next few years you will see Asia’s markets double and even triple, offering incredible opportunities, largely due to a wholesale exodus of capital out of Western government bond markets.

E. Natural resources? Although deflation still has the upper hand on a macroeconomic basis, and will for some time, mark my words …

In the not-too-distant future, capital will become so frightened over the collapse of the Western world’s government bond markets — and the inevitable bankruptcy of Europe, Japan and the U.S. — that …

Natural resources, gold, silver, oil, coal, copper, nickel, food, timber, water, platinum, palladium, and more … will once again, explode higher.

Not because of inflation. But because the world’s largest governments will be going down the tubes.

It’s coming, and it’s not far off.

Best wishes, stay safe, and stay tuned …

Larry

Larry Edelson, one of the world’s foremost experts on gold and precious metals, is the editor of Real Wealth Report, Power Portfolio and Gold and Silver Trader.

Larry has called the ups and downs in the gold market time and again. As a result, he is often called upon by the media for his investing views. Larry has been featured on Bloomberg, Reuters and CNBC as well as The New York Times and New York Sun.

James Turk: “The inevitable finally happened.” “The Greek financial system is collapsing. We can’t say yet that it has “collapsed” because we are not there yet. The collapse is just beginning. At this time, we do not know where all the pieces will fall…”.

James Turk: “The inevitable finally happened.” “The Greek financial system is collapsing. We can’t say yet that it has “collapsed” because we are not there yet. The collapse is just beginning. At this time, we do not know where all the pieces will fall…”.

Greece has chosen the path to default!

Specifically, Greek officials called for a nationwide referendum on July 5 over the European bailout program rather than reach a direct agreement with creditors over the weekend.

Next, Greece itself said it will skip a 1.7 billion euro debt payment due tomorrow to the International Monetary Fund (IMF). That, in turn, is a default in everything but technical name only. It also means Greece’s current bailout program will expire with nothing to replace it.

The European Central Bank (ECB) responded to the referendum news by refusing to hike its emergency aid to the Greek banking system, currently around 89 billion euros after several recent increases. Since those funds were the only thing keeping Greek banks alive, the Greek government was forced to shut down all the nation’s banks through at least July 6.

Greek citizens can still take money out of an ATM, but only 60 euros per day. The Greek stock market was also shut.

Those moves temporarily halt the worst of the financial bleeding in Greece. But they also open up a whole host of other questions.

The most pressing one for depositors: What the heck will they get back the next time a teller window is open to them? Euros? New drachmas? IOUs? And the bigger question for investors around the world is: “Does this mean Greece is going to get kicked out of the euro currency union?

The most pressing one for depositors: What the heck will they get back the next time a teller window is open to them? Euros? New drachmas? IOUs? And the bigger question for investors around the world is: “Does this mean Greece is going to get kicked out of the euro currency union?

If Greek citizens vote “No” to Europe’s last and best offer on the table this coming Sunday, I believe Greece will get kicked out. If they vote “Yes,” there’s always a possibility the country hangs on by its fingernails for a while.

But without permanent debt relief that acknowledges it can never pay back all its bonds at face value, Greece might be forced to abandon the euro and introduce its own currency anyway. It sure seems like Germany, France, and other European nations – which hold all the financial cards here — are fed up and ready to cut the country loose.

Greek Prime Minister Alexis Tsipras tried to put a brave face on the situation. He tried to rally his political base behind a “No” vote, couching it in terms like this: “The dignity of the Greek people in the face of blackmail and injustice will send a message of hope and pride to all of Europe.”

But the initial reaction in global markets was swift and severe. Asian markets tanked, while stock markets around Europe plunged as much as 5%.

Bonds issued by peripheral European countries fell in value, while the euro currency dropped below 1.10 against the dollar, before bouncing a bit. Anyone unlucky or unwise enough to own the handful of direct Greek investments that trade here in the U.S., such as the Global X FTSE Greece 20 ETF (GREK) or National Bank of Greece (NBG), lost even more of their money. NBG plunged 24%, while GREK lost 20%.

Now, we’ll see where the rubber meets the road. I laid out my three possible scenarios for what would happen in Greece, and how that would impact investors like you, two weeks ago.

We clearly did not get Scenario #2 (a last-minute can kick deal). That leaves Scenario #1 (a quick and painful, but ultimately healthy move) and Scenario #3 (a long, drawn-out disaster scenario).

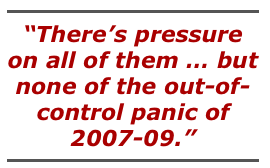

I suggested #1 was the most likely all along. But the truth is, the markets are going to determine the ultimate answer. My three “tells” to see which is getting the upper hand? The euro currency, the European bond market, and U.S. financial stocks.

If the euro tanks and other peripheral European bond markets start following Greece’s into the abyss, that would be a huge red flag. And if U.S. financial stocks start plunging, that would be a sign that contagion fears were spreading beyond Greece’s (and Europe’s) borders.

If the euro tanks and other peripheral European bond markets start following Greece’s into the abyss, that would be a huge red flag. And if U.S. financial stocks start plunging, that would be a sign that contagion fears were spreading beyond Greece’s (and Europe’s) borders.

So far, there’s pressure on all of them — with the Dow dropping by around 350 points today … but none of the out-of-control panic we saw during the credit crisis days back in 2007-09. That could easily change, though, and you can bet I’m watching closely. So stay tuned for more recommendations and commentaries about what to do next – right here at Money and Markets and in your other subscription services.

This is an “Amber Alert” day in the markets.

This is an “Amber Alert” day in the markets.

“Greeks Line Up at Banks; ATMs Run Dry” was the headline over at the Drudge Report. Versions of it ran throughout the financial media.

Greece is the canary in the coal mine for what could one day happen to your savings.

You’ll recall our prediction: In a crisis, banks will move fast to block access to your money.

First, they will limit withdrawals. Then they will either close their doors or run out of cash.

Capital Controls Have Arrived…

That’s what’s happening in Greece right now…

The showdown going on there for months is reaching a climax.

The Greek government has announced it will put creditor demands to a popular vote.

“Hey, how do you feel about paying our national debt?” they’re going to ask the hoi polloi.

And how do you think the hoi polloi are going to respond?

The best guess is they’re going to say: Let’s not.

Which will leave the banks cut off from new funds… and short of old ones.

Smart depositors figured this out long ago. They took their money out of Greek banks. But the rest of the people are now wising up. In effect, they’re voting with their money – getting it out while they still can.

Naturally, the banks tried to protect the money that isn’t theirs. Piraeus Bank and Alpha Bank limited the amount you could take out. All you could get from a Piraeus ATM, for example, was €600 ($667).

This made people more eager than ever to get their hands on their money. Lines formed at ATMs on Saturday. One banker estimated that €110 million ($122 million) left the banks by 11:30 a.m.

Not all banks are open on Saturday. But even those that were normally open stayed shut.

And now Greek prime minister Alexis Tsipras says Greek banks will be shut, and that capital controls will be imposed, until July 7.

Greeks will only be allowed to take out a maximum of €60 ($67) a day. And they’re banned from moving their savings to accounts outside of Greece.

How Not to Manage a Bubble

The sense of panic and impending doom over the weekend was heightened, as the Chinese government took action to halt a stock market plunge.

In the last two weeks, the Shanghai Composite Index has lost 20% of its value. That’s the equivalent of the Dow losing 3,600 points. It’s the kind of thing that makes investors nervous. Or desperate.

If that happens in the U.S. – which it surely will – you can bet your bippy that the feds will intervene. The Chinese are doing the same. They’ve just cut the central bank lending rate to the lowest level ever.

Will that do the trick?

From John Rubino at DollarCollapse.com:

China, meanwhile, has spent the past couple of decades directing an infrastructure build-out that in retrospect was maybe twice as big as it should have been.

Now it’s fiddling with all kinds of imperfectly understood fiscal and monetary levers, trying to maintain a 7% growth rate that is looking more and more fictitious.

Here again, the best way to deal with a bubble is to not let it happen in the first place. The second best way is to let it pop and allow the market to clean up the mess.

The absolute wrong way to manage a bubble is to intervene from the top to keep it going. Look where that has gotten Japan and the U.S.

Stay tuned for more exciting developments…

Regards,

Bill

Dublin, Ireland

Further Reading: The freezing of accounts in Greece is only a taste of what’s to come… As Bill has been warning, right now in America, the highest levels of government and the banking system are locked in a desperate last stand against a disturbing monetary shock… one that will make what’s happening in Greece seem mild by comparison.

And it could disrupt your life in ways you never thought possible… You will suddenly be locked out of your bank account… unable to withdraw cash or deposit a check… your stocks will swing wildly out of control… your Social Security payments will pile up unopened on your kitchen table… no one will cash them…

To find out what has Bill so worried, go here now.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair