Asset protection

“When interest rates tick up, as they did just recently, this is an indication that the market is showing a nascent preference for cash, rather than bonds.

“When interest rates tick up, as they did just recently, this is an indication that the market is showing a nascent preference for cash, rather than bonds.

This incipient increase in interest rates is warning that we may see, at some point, a widespread desire to dump bonds for cash; that would mean a jump in interest rates which would lower the prices of bonds, and the fall would cause losses to holders of bonds and other credit instruments which form the debt cloud. Hasty sales of bonds would aggravate the fall in values and reinforce the rise in interest rates. As in all cases of panic, those who panic first have the greater chance of avoiding losses.

There is a further problem:”

More Stimulus And More QE Coming As The World Economy Falls Off A Cliff

More Stimulus And More QE Coming As The World Economy Falls Off A Cliff

“For quite a while the Fed has led the market to believe that there would have been a rate increase at their meeting this week. But of course that did not happen. So now the guidance is that there will be rate increases at the next two meetings, with the first one in September. But, Eric, soon the data-dependent Fed will realize that there will be no room for rate increases. Instead, there will be more stimulus and more QE, as the U.S., the EU and the rest of the world economy falls off a cliff.”

….continue reading Egon von Greyerz’s interview with King World News HERE

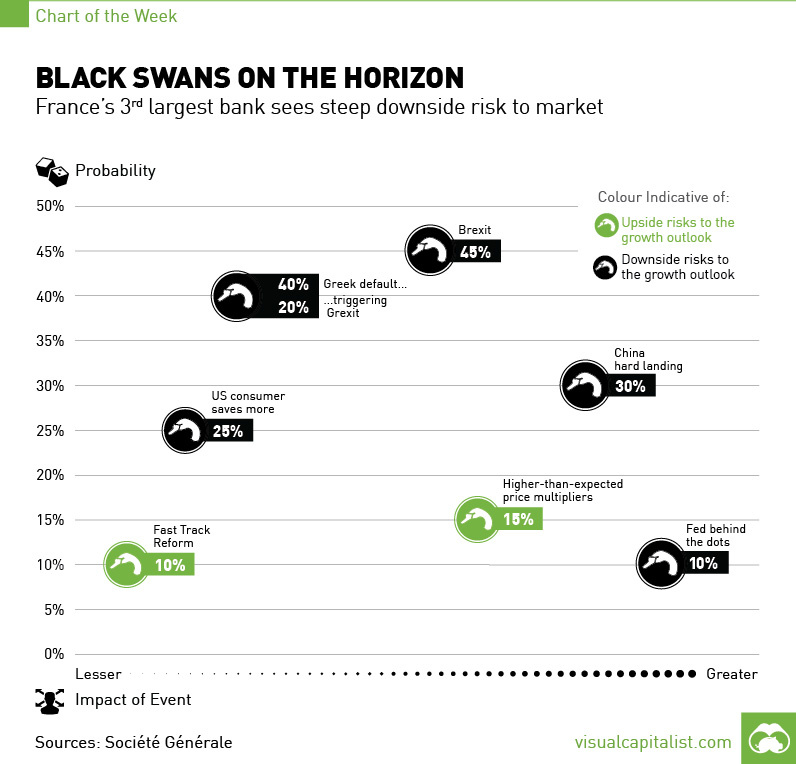

Frances 3rd largest bank sees steep downside risk to the market.

The folks at Société Générale, France’s third largest bank, are avid birdwatchers.

When they are not busy getting hawked by regulators for scandals, they are trying to spot the next black swan on the horizon that could have a profound negative or positive impact on the markets.

By definition, black swans are not seen by everyone. Nassim Taleb, the developer of the Black Swan Theory, uses the “turkey analogy” to describe this: although it is a surprise to the turkey that it is eaten for Thanksgiving dinner after days of positive data (being fed), it is not a surprise to the farmer nor the butcher.

In other words, don’t be the turkey.

That’s why every analyst, including SocGen, tries their best to predict which black swans are on the horizon. The most recent quarterly report sees eight potential black swans: six with potential downside, and two with potential upside:

Downside risks and their probability:

- 45% – Great Britain leaves the EU

- 40% – Greece defaults on debt and then (20%) Greece leaves the EU

- 30% – China hard lands (growth of <5%)

- 25% – US consumer saves more

- 10% – Fed behind the dots

Upside risks and their probability:

- 15% – Higher-than-expected price multipliers

- 10% – Fast track reform, particularly in Euro Area

The ratio of negative to positive black swans remains the same as their report from the previous quarter, but the probabilities have increased significantly: The chance of a Brexit has gone from 10% to 45%, while a Greek default goes from not existing on chart to a 40% probability.

Today, the most important “known unknown” in all of finance – something so powerful it could change the character of the entire global economy.

Today, the most important “known unknown” in all of finance – something so powerful it could change the character of the entire global economy.

But first, a short trip to Paris…

On the walls of the chapel at the French military school are rich paintings… including a couple of 18th-century masterpieces by French painter Louis-Michel van Loo.

The one behind the altar is of Saint Louis, dying from dysentery in the 13th century. There he is in his splendid blue robe… with the fleur-de-lis on it… receiving extreme unction from a priest.

Saint Louis (aka King Louis IX) died in Tunis, North Africa, on the Eighth Crusade; what he was doing there is not clear. But at least he went in person. And he died in the campaign.

Everything has a price tag. The previous crusade – which he had undertaken 20 years earlier – had been a disaster, too.

He took his army to Egypt to do battle with the Hafsid Muslim dynasty.

There, in the heat of the Nile River Valley, his soldiers must have made quite a picture – with an English contingent, led by William of Salisbury, and the Knights Templar with their banners and tunics.

Everything seemed to be going so well… until…

We’ll come back to that.

God’s Fool

We were sitting in the chapel, attending mass on Sunday. The priest offered his sermon.

We couldn’t tell if it was dull or just pointless. But our eyes wandered to the paintings on the wall… and our mind wandered to thoughts of war.

This – the chapel at the École Militaire – was the sacred heart of France’s military tradition.

This week marks the 200th anniversary of the Battle of Waterloo, a French defeat.

Since then, French military successes have been few. But before Wellington and Blücher hammered Napoleon at Waterloo, the French had won far more battles than Americans have ever fought.

French history is littered with bodies – cut, pierced, blown to bits.

The French, like the British and the Americans, celebrate their fallen heroes and pretend that their wars served a worthy purpose.

And who knows… Wars may look foolish – in retrospect. But man is God’s fool. And all His works demand our solemn curiosity.

And so, with a mixture of respect, shame, and embarrassment, this week, we turn to Mars – the god of war.

When Bonds Turn, So Will the World

But first, let us take up our usual post – where we keep an eye on markets and economies, in the hopes of seeing what mischief is afoot.

Friday, the Dow fell 140 points – or about 0.8%. Given the 108% rise over the last six years, that’s hardly significant.

But the bond market may be a different story… It’s looking more vulnerable. After 33 years of trending down, yields may have finally switched directions.

For example, the yield on the 10-year French sovereign bond quadrupled in the last two months. At 1.2%, it’s still microscopic. And neither the significance nor the permanence of this move is known. But it’s still worth taking note.

By the way, the direction of travel of bond yields – which reflects expectations of where interest rates are headed – is probably the most important “known unknown” in the financial world. Central banks influence, but cannot control, interest rates.

Knowing what Fed chief Janet Yellen wants to happen is not the same as knowing what will happen.

People are not usually prepared to lend money for nothing. Sooner or later, we expect they will want a decent return on their investment.

When they do, the world will change. Asset prices have floated higher and higher on the flood of credit over the last 33 years. When the tide ebbs, assets will fall. And the character of the economy will change.

And that change could be shockingly quick and staggeringly large. The bond market is huge. But just a few players – today, mainly central banks – dominate it.

Read more > One of the early warning signs will be a “run” on paper dollars

For example, government-sponsored agencies Fannie Mae and Freddie Mac backed 60% of U.S. mortgages between 2008 and 2013. And large chunks of U.S. debt are held by just a few players – such as the Fed, China, and Japan.

The feds have convened a meeting of major banks and bond investors this Wednesday. They are worried about what would happen in a crisis.

There could be many bonds on offer, for example, but no bidders. Bond prices would crash – provoking an even more sensational disaster.

The Battle of Al Mansurah

But now let’s return to the poor Christians… sweating in the hot Egyptian sun… seven and a half centuries ago.

They were there to sort out the Middle East and wrest control of the area from the locals – much like U.S. troops in Iraq and elsewhere.

At first, the crusaders’ campaign went well. The Muslims fled, leaving a crucial bridge over the Nile intact.

The crusaders crossed the river, led by Saint Louis and Robert of Artois. Then the town of Al Mansurah was open to them.

Thinking the defenders had run off, the Christians entered the gate. They soon discovered that they had been led into a trap. From all sides, the Muslims attacked. Robert of Artois was killed. So was William of Salisbury. The Knights Templar were almost wiped out. Only five escaped alive.

The Christians retreated as best they could. They dug a ditch to protect their camp. The sun beat down. Supplies of food and water ran short, as the Muslims blocked the crusaders’ ships from reinforcing their compatriots. Famine and disease settled into the camp like swamp gas.

Finally, a deal was struck. Louis was taken into captivity by Muslim forces, along with about 12,000 of his troops. They were freed when France paid a ransom. The price tag: a sum equal to about a third of France’s annual tax revenues.

Louis agreed not to go crusading again. But he learned nothing from the adventure. Twenty years later, he was once again sunning himself in North Africa, waiting to die.

Regards,

Bill

Paris, France

Further Reading: More than 286,000 people have already checked out Bill’s newest video presentation. Click here now to watch it, so you won’t be caught off guard when the violent monetary shock hits.

…also The Week Ahead: FOMC, Currency Wars, Greece and More

…also The Week Ahead: FOMC, Currency Wars, Greece and More

The lack of faith in central bank trustworthiness is spreading. First Germany, then Holland, and Austria, and now – as we noted was possible previously – Texas has enacted a Bill to repatriate $1 billion of gold from The NY Fed’s vaults to a newly established state gold bullion depository…”People have this image of Texas as big and powerful … so for a lot of people, this is exactly where they would want to go with their gold,” and the Bill includes a section to prevent forced seizure from the Federal Government.

….read more HERE

….more from ZeroHedge:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair