Michael Platt, CEO and founder of BlueCrest Capital, a $30 billion hedge fund, states the case in an interview on Bloomberg for being totally on the sidelines in short-term US Treasuries and German Bonds.

{youtube}lvuZ7CQIkJo{/youtube}

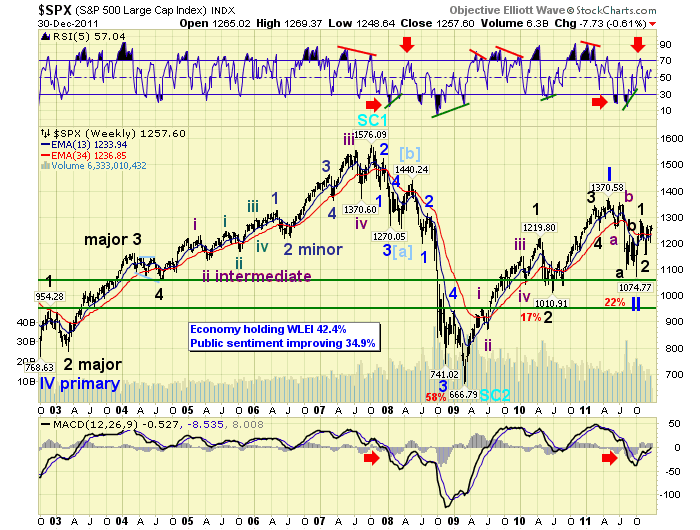

LONG TERM: inflection point

After completing a 26 month, (Mar09-May11), Primary wave I high at SPX 1371 the market declined in five waves to 1075 by Oct11. We initially interpreted this decline as five waves down completing Major wave A. Then we expected a Major wave B rally, lasting about two months, retracing about 61.8% of the entire decline: around SPX 1258. The market then surprised most with an impulsive looking uptrend to SPX 1293 in only 18 trading days. We then considered the five waves down might have been an extended flat. Similar to the extended flat that ended the 1987 crash. This opened options to both a bull and bear market scenario. After the late-October SPX 1293 high, the market corrected in an abc pattern into a late-November low at SPX 1159. This corrective downtrend, essentially, kept both bull and bear scenarios alive: a resumption of the bull market, or a Major wave B still underway.

(click on the chart or HERE for larger view and the whole article)

“Once again I beseech (beg) my subscribers to be OUT of stocks. The outlook for the markets, all of it, is now very bearish. We are watching the greatest debt bubble in history about to deflate, and it won’t be a pretty sight”

also:

“Signs of inflation are now appearing. Super Bowl ads for this year have already sold out at the price of 4 million per 30 seconds a piece. Starbucks has just raised its prices. The prices of oil, silver and gold have surged higher today — all signs of inflation. Almost all commodities closed higher as well.

Amid all the good news, investors took the the bit in their teeth today and pushed the Dow substantially higher. Tomorrow I’ll see how the internals of the market were affected by today’s Dow action.”

My bet — Obama will be will be a one-term president after the next election. The economy, the stock and bond markets — and stubborn unemployment will defeat him.

Posted January 3rd at 2pm PST in Richard Russell’s Dow Theory Letters daily comment .

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

In 1989 Russell took over Julian Snyder’s well-known advisory service, “International Moneyline”, a service which Mr. Synder ran from Switzerland. Then, in 1998 Russell took over the Zweig Forecast from famed market analyst, Martin Zweig. Russell has written articles and been quoted in such publications as Bloomberg magazine, Barron’s, Time, Newsweek, Money Magazine, the Wall Street Journal, the New York Times, Reuters, and others. Subscribers to Dow Theory Letters number over 12,000, hailing from all 50 states and dozens of overseas counties.

A native New Yorker (born in 1924) Russell has lived through depressions and booms, through good times and bad, through war and peace. He was educated at Rutgers and received his BA at NYU. Russell flew as a combat bombardier on B-25 Mitchell Bombers with the 12th Air Force during World War II.

One of the favorite features of the Letter is Russell’s daily Primary Trend Index (PTI), which is a proprietary index which has been included in the Letters since 1971. The PTI has been an amazingly accurate and useful guide to the trend of the market, and it often actually differs with Russell’s opinions. But Russell always defers to his PTI. Says Russell, “The PTI is a lot smarter than I am. It’s a great ego-deflator, as far as I’m concerned, and I’ve learned never to fight it.”

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

IMPORTANT: As an added plus for subscribers, the latest Primary Trend Index (PTI) figure for the day will be posted on our web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

“Those of us who look into a crystal ball end up eating lots of broken glass.”

The finest gentleman I ever met in nearly three decades of being in and around the financial services industry, Mr. Kennedy Gammage, often said the above when asked for his outlook. At best, some of us can make an educated guess. At worst, one would have been better off with darts. In 2011, yours truly fell somewhere in between.

In a world where “what have you done for me lately” is paramount, I begin 2012 with a mixed bag of thoughts and a sense it shall end up better being a live chicken versus a dead duck. Because I derive a living and much of my personal investing dollars are geared towards an industry where failure is the norm, the junior resource market, I believe I’ve become more realistic of my chances and have borrowed an old slogan of “bet with your head, not over it.” Unfortunately, too many people don’t treat it as gambling and are not prepared financially and mentally to lose part or all their capital – a feat all too common in the junior resource market.

Instead of having a very small amount of high-risk capital allotted to the junior resource segment with a true understanding that failure is the norm and losing part or all of one’s capital is very real, they instead plow a large percentage of their monies and then look to blame anybody but themselves when the odds stacked against them play out. The fact that most of the pundits in this arena never note the dark side doesn’t help.

So first and foremost, to any and all readers of my blog I say that when it comes to the junior resource market, failure is the norm and I will have my fair share of it. Don’t fool yourself into thinking a business where 9 out of 10 companies eventually failed to go the whole nine yards is a place where you should place any capital that you’re not fully financially and mentally prepared to lose.

Keeping in mind that while I comment on various markets, this blog’s main purpose is to feature companies I’m compensated by, I shall endeavor to make “guesses” on what may unfold in the following markets:

U.S. Stock Market – Perhaps the best thing I did in 2011 was not to short this market despite lots of suggestions to, and I ended up making my only trade from the long side. While something unforeseen can take it down hard, it continues to look like for the early part of 2012 that the least resistance is to the upside. I think the “Don’t Worry, Be Happy” crowd will make the argument that the market held up despite an onslaught of so-called bad news like the European debt crisis and, with the U.S. economy grudgingly improving, can push share prices higher.

The key question is, can the November presidential election create another “hope” win for either party and therefore postpone until after 2012 the inevitable horrific fiscal crisis that is coming here at home… no ifs, ands or buts? I don’t know the answer, but I do know it’s not a question of if it gets real bad here, but when.

U.S. Bonds – Personally, I think it’s insane to lend anyone (let alone broke Uncle Sam) money for 10 – 30 years for interest rates of 2-4%. You would have to believe in Santa Claus and the Tooth Fairy and think that Elvis and Jimmy Hoffa are alive on an island somewhere to believe inflation is/will be less than these interest rates over the next 10 -30 years. In the end, I think bonds end up the worst bet for the next 10 years.

U.S. Dollar – Its main competition, the Euro, is in horrific shape at the moment and giving some wind behind the dollar’s sail. The problem with that is the Europeans have at least come face to face with the debt problem. Americans by and large still have their heads buried in the sand and have made an already bad problem worse. I don’t know the date or time, but the ability to kick the can down the road is nearing an end. The price to be paid will be enormous and shall eventually kill the U.S. Dollar.

I continue to believe the Canadian Loonie (dollar) is the only currency to own. I love Canada (I’m working on the Canucks part).

Gold – Whatever lows we make in this current correction (worse case is the low $1400s, best case is low being put in very near term), I suspect it shall be well within the 1st quarter and by the time 2013 arrives, we shall be at new highs. The mother of all gold bull markets remains, IMHO.

Base Metals – After a couple years of seriously underweighting with base metals, I think many of them are at or near their lows. I especially like zinc and continue to favor copper.

Oil and Natural Gas – Believing a crisis or a series of crises in the Middle East is inevitable, it’s hard to envision oil much lower and can spike to new highs if and when one or more crises raise their ugly heads.

Much more abundant supply of natural gas has taken the air out of a budding new bull market. However, with natural gas at $3 and oil at $100, a long gas/short oil play for the one in one million speculators/gamblers out there who meet the financial and mental toughness to engage such a play is worth considering.

Please note – None of these stocks hit price and suggestion has now ended.

My theme for quite some time now is to make tomorrow the first day of the rest of your life. This song helps me focus on that. (Ed Note: What a great version of this song!)

This entry was posted on January 2, 2012 at 7:13 PM. You can follow any responses to this entry through the RSS 2.0 feed. Responses are currently closed, but you can trackback from your own site.

Ed Note: In keeping with Legendary Investor Jim Rogers assertion in an article posted here yesterday that there is little reason for optimism in anything but agriculture, this article delves into Potash, a resource used to gain higher crop yields.

People have to eat. That seemed to be the consensus of the markets in 2011, which saw potash gaining traction as a new kind of safe haven. A resource that promises higher crop yields in a time of exploding global population growth, potash is ripe with potential profits for investors who choose carefully. The Energy Report dug deeper into this sector in 2011, interviewing analysts and industry experts who shared how to gain exposure to this growing market.

Investing in agriculture can take many forms. Bob Moriarty, 321energy.com founder, shared his insights in a March article titled “Food Is Fuel.” He said: “Potash is used to make fertilizer. As food gets more valuable, potash gets more valuable. It’s not necessarily that you’re more efficient in the production of food. If the price of wheat doubles, farmers can afford twice as much potash. It’s not necessarily more efficient; it’s just cheaper in relative terms. The price of food is going to go higher and higher. Potash is around $600/ton now, but it could be $1,500/ton based on the cost of food today.”

The trend will not continue forever, Moriarty cautioned. “Most companies are going to fail. You have to be counter-cyclical. Potash was way too cheap. Companies couldn’t afford to mine it profitably, and now it will overshoot in the other direction. I hope there is a bubble. That will be a tremendous opportunity to get out at a giant profit. We’re not at the top for potash, but everything goes up and everything goes down.”

Moriarty elaborated in a December article titled “Profit from Peak Oil“, making the point that energy and food are directly related. “Potash is a form of energy. Food is a form of energy. To make more food, you need more energy and you need more potash. There are enormous potash deposits, basins of sedimentary deposits—basically a variation of salt—that date back tens of millions of years. We know where they are. They’re easy to drill. A lot of people are going to make a lot of money in potash.

“You can bet on some things in the short term and others in the long term. I don’t think anyone would conclude the cost of energy is going to go down over the long term, because there are no cheap energy sources. There is no magic bullet. So the cost of food is going to go up. I think any potash company would be a good investment right now. Real safe investments for 5, 10 or 15 years would be food, potash, water, oil and natural gas. Good shorter-term investments would be anything real—gold, silver, platinum and anything that you can actually hold in your hand.”

Moriarty is not alone in his assessment of the agriculture industry. In a May story titled “Potash Prices Heading to $750,” Richard Kelertas said:

“We believe the upward price pressure started after the economic crisis in 2009, and it could remain a substantial bull market until stocks:use ratios (carryover:total use) in most major food stocks—grains, corn, soy beans—can be brought back up to 10-year averages. Currently, the ratios are well below those averages. There doesn’t seem to be any reprieve in sight, unless we have two to three years of bumper harvests in all grains around the world.

“In retrospect, 2009 was a tough year for a lot of fertilizer producers. Farmers had to delay applications, even though they started to see crop shortages followed by slowly rising crop prices. We didn’t really see fertilizer-price recovery until 2010. Around March/April, or mid-2010, we started to see a pickup in fertilizer stock prices. It was slow at first and, in some cases, it has been muted; but at the beginning of 2011, it started to surge dramatically. Now it’s come off again on the expectation that all commodity prices, including that of oil, will come off as the global economy slows down (especially in China). But our view is that this is just temporary, and that these stock prices don’t really reflect anywhere near the fertilizer prices we are looking at in 18–24 months. So, these current stock prices are only reflecting mid-cycle, but nothing near peak prices.

“We won’t see $1,000/ton. I don’t expect the type of hoarding experienced back in 2007 and 2008 will happen again to the same degree. We certainly will get speculation; but, typically, the amount of cash that’s available, the lending requirements and margin calls are more stringent than they were three years ago. You will probably see one-half of the speculative run-up in potash that we saw back in 2007. This time it is coming from actual supply/demand dynamics, not speculative investors gobbling up contracts. So, $1,000/ton?—I’ll never say never, but I think the next peak we’ll see is probably more in the $700–750/ton range. . .in the next 24 months.”

For investors looking to get closer to the farm, Kevin Bambrough, founder of Sprott Resource Corp., suggested two private equity deals in a February article entitled “Fiat Currencies Are Worthless“.

“We have two entities that are the hardest to value but potentially the most exciting assets. Right now, very little value is being given to them in the Resource Corp. share price but, eventually, their value could be very large. These are the One Earth companies—One Earth Oil & Gas Inc. and One Earth Farms Corp., both of which are private. One Earth Farms is something we started working on in 2007. It’s taken a few years to get there, but we’re very pleased that it’ll be the largest farm in Canada and one of the largest farms in North America in 2011. It’s also positioned to be one of the largest farms in the world in the coming years.

“One Earth Farms has synergistic cattle and grain operations. Its real goal is to change the typical farming model, wherein the average farmer buys retail and sells wholesale. By that, I mean he buys his equipment, fertilizer, etc., from a local dealer or store, and then sells his crop as a commodity at harvest time based on wholesale prices. With the size and scale we’ve already attained, we’ve established that we can buy wholesale. And now we’re working on the model that can allow us to capture some of the retail margin by partnering with food processors or retail outlets. It’s almost impossible to find good investments in the Ag sector, and there are very few corporate farms in which to invest around the world. We’re building one that, hopefully, will provide inflation protection, as well as food security for potential investors and partners.

“By the way, One Earth Farms is, in our minds, the only way you can invest in Canadian farming in a large way. That’s because it is in partnership with the First Nations groups of Canada, which are federally regulated and permitted to allow public companies and foreigners to lease land. Typically, non-First Nations lands in Manitoba and Saskatchewan are restricted under provincial law from public company ownership or leasing or foreign participation.

“I think that One Earth Farms is a company that ultimately will be highly valued and coveted by three different types of investors. First, large pension funds might find it very desirable for the inflation protection it could provide pension fund holders. Also, I think that the sovereign wealth funds and the Ag ministries of the world that are trying to get food security for their nations would find this to be very strategic. Lastly, we feel it would be valued by ordinary institutional and retail investors if it were publicly listed.”

As more analysts and investors lose confidence in the dollar, marketproof alternatives are even more in demand. As Bambrough said at the end of his interview, “I think that we’re going to come up with different monetary instruments that are reflective of precious metal or other holdings. Sooner or later, I envision we’ll have a currency that may be reflective of a basket of commodities that we may trade in units tied to something tangible. Ultimately I think we could have an energy-based currency.”

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

A sane voice in a scrambled investment world.

~ Ed R.

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair