Daily Updates

Ed Note: The above is a small excerpt from Mark Leibovit’s Daily VR Trader. The VR Gold Letter is published WEEKLY. This excerpt from 8/24/09.

GOLD and METALS – ACTION ALERT –

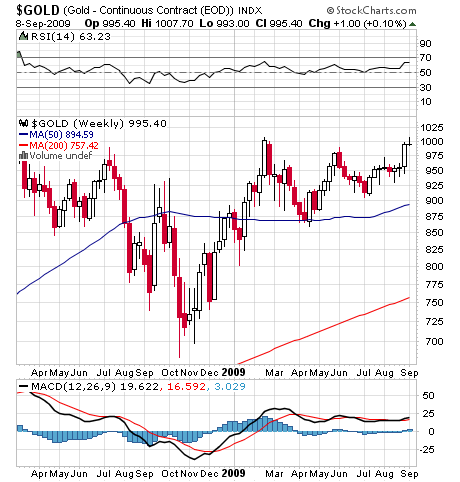

Gold got over the key $1000/oz level as the Dollar fell through support yesterday, but gave up most of its gains by the end of the day. Gold finished the day up 2.20 at 996.70, but well below it morning high of 1008.90. Silver was up 0.24 to 16.46, but was as high as 16.87. Platinum closed up 29 and palladium was up 4.

Gold and silver shares along with the underlying metal are a tad extended following a five to eight day advance, but I’m not ready to run for the hills chasing the bears. From my point of view the party could only be beginning despite the admonishment of what my friend, Peter Grandich, calls the ‘Don’t Worry, Be Happy’ crowd. Nothing has changed my view or the Annual Forecast Model for Gold (seen in the VR Gold Letter weekly), so I’m status quo.

Don’t think for a moment that owning gold is a speculation. Owning gold may not only save your wealth but could save your life. Gold at $5000 to $10000 an ounce is not out of the question between now and the end of the current up cycle which carries into 2020 and it ain’t that far away! (Ed Note: see Charts below)

December copper settled up 0.0895 at 2.9810, getting close its 2.9895 recovery high from August 28.

FOR THIS WEEK ONLY SPECIAL! I’ve slashed prices 50%. I want you to get this information!

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $25 per month and to Silver subscribers for only $35 per month. Email me at mark.vrtrader@gmail.com, but do it this week!

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

Click HERE to view 1982-2009 Point and Figure chart below in full size.

China has issued what amounts to the “Beijing Put” on gold. You can make a lot of money, but you really can’t lose.

I happened to see quite a bit of Cheng Siwei at the Ambrosetti Workshop, a gathering of politicians and global strategists at Lake Como, including a dinner at Villa d’Este last night at which he listened very attentively as a number of American guests tore President Obama’s economic and health policy to shreds.

Mr Cheng was until recently Vice-Chairman of the Communist Party’s Standing Committee, and is now a sort of economic ambassador for China around the world — a charming man, by the way, who left Hong Kong for mainland China in 1950 at the age of 16, as young idealist eager to serve the revolution. Sixty years later, he calls himself simply “a survivior”.

What he said about US monetary policy and gold – this bit on the record – would appear to validate the long-held belief of gold bugs that China has fundamentally lost confidence in the US dollar and is going to shift to a partial gold standard through reserve accumulation.

He played down other metals such as copper, saying that they could not double as a proxy currency or store of wealth.

“Gold is definitely an alternative, but when we buy, the price goes up. We have to do it carefully so as not stimulate the market,” he said.

In other words, China is buying the dips, and will continue to do so as a systematic policy. His comment captures exactly what observation of gold price action suggests is happening. Every time it looks as if the bullion market is going to buckle, some big force steps in from the unknown.

Investors long-suspected that it was China. We later discovered that Beijing had in fact doubled its gold reserves to 1054 tonnes. Fait accompli first. Announcement long after.

Standing back, you can see that the steady rise in gold over the last eight years to $994 an ounce last week – outperforming US equities fourfold, even with reinvested dividends – has roughly tracked the emergence of China as a superpower in foreign reserve holdings (now $2 trillion).

As I have written in today’s paper, Mr Cheng (and Beijing) takes a dim view of Ben Bernanke’s monetary experiments at the Federal Reserve.

“If they keep printing money to buy bonds it will lead to inflation, and after a year or two the dollar will fall hard. Most of our foreign reserves are in US bonds and this is very difficult to change, so we will diversify incremental reserves into euros, yen, and other currencies,” he said.

This line of argument is by now well-known. Less understood is how much trouble the Fed’s QE policies are causing in China itself, where they have vicariously set off a speculative boom on the Shanghai exchange and in property. Mr Cheng said mid-level house prices are now ten times incomes.

“If we raise interest rates, we will be flooded with hot money. We have to wait for them. If they raise, we raise.”

“Credit in China is too loose. We have a bubble in the housing market and in stocks so we have to be very careful, because this could fall down.”

Of course, China cold end this problem by letting the yuan rise to its proper value, but China too is trapped. Wafer-thin profit margins on exports mean that vast chunks of Chinese industry would go bust if the yuan rose enough to close the trade surplus. China’s exports were down 23pc in July from a year before even at the current exchange rate, and exports make up 40pc of GDP. “We have lost 20m jobs in this crisis,” he said.

China’s mercantilist export strategy has led the country into a cul-de-sac. China must continue to run its trade surplus. It must accumulate hundreds of billions more in reserves. Ergo, it must buy a great deal more gold.

Where is the gold going to come from?

Ambrose Evans-Pritchard has covered world politics and economics for 25 years, based in Europe, the US, and Latin America. He joined the Telegraph in 1991, serving as Washington correspondent and later Europe correspondent in Brussels. He is now International Business Editor in London.

Quotable

“Money is not an invention of the state. It is not the product of a legislative act. The

sanction of political authority is not necessary for its existence.” – Carl Menger

FX Trading – Dollar blues…Ugly policies…Hampered markets…gold over $1,000

• Gold through $1,000

• Oil back over $70

• UN wants a new reserve currency

• China alarmed by US money printing

• Obama asks senate to increase debt ceiling

Boy, you know it’s bad when the UN gets into the act and people actually take them seriously.

Is this a crystallized negative sentiment extreme in the dollar? We will only know that with the gift of hindsight of course, but there may be more to go given how nicely government policies seemed aligned to prolong the down turn. Plus, there is another 10% or so left on the downside before the dollar tests its old low made back in March 2008.

The stuff we are seeing and hearing is likely to concern even the most ardent dollar supporter. Maybe we saw a lot of them capitulate yesterday. A friend of mine from Chicago emailed, he said take a look at the volume in the UD dollar index; it’s huge! Does it mean anything?

So to the chart I went. Sure enough, it was huge. You can see it at the bottom of the daily dollar index chart below:

…read pages 2-4 HERE.

Ed Note: Jack Crooks wanted to let readers see an example of his:

8 September 2009 CAD and Euro Charts

Comments: Canadian dollar recommendation Issue #31 & Room for euro to run! You should not yet be filled on this order yet. The G-20 signaled it’s too early to take awaythe punch bowl. All things risk appetite seems to like it. Dollar LIBOR rates feel to a record low in London—adding some weight to the dollar- carry trade idea. Dollar yields now even less than the yen—former carry trade king. Swiss is the only major now lower than the buck.

Sept. 8 (Bloomberg) — Dollar-borrowing costs fell against those for Japan’s currency, widening the interest-rate gap between the currencies to the widest level since March

1993. The London interbank offered rate, or Libor, for three- month dollar loans declined to a record low 0.30875 percent yesterday from 0.31438 percent on Sept. 4, according to the British Bankers’ Association. Libor for yen loans dropped to 0.37938 percent from 0.38125 percent, widening the difference between the rates to 7.1 basis points. Dollar rates became cheaper than those on the yen on Aug. 24, leaving the Swiss franc as the only major currency that is cheaper to borrow than the dollar. Since then, the spread= between the rates has widened for nine-straight days.

There’s talk the ECB and BOC are getting very nervous about the dollar. The background move in gold (back above $1,000 this morning) probably reflects some of that, also sentiment that continued monetary ease will be harder to mop up down the road is again adding weight to the inflation argument—true or not. Oil is up over two bucks, back above $70 this morning. This is all very much consensus stuff and stuff that we do know; but a good backdrop for the Canadian dollar to play catch up to the other commodity currencies (Aussie and New Zealand) already trading in new intermediate-term high territory. We are playing for a breakout in the Canadian dollar above its intermediate term high. Note: Futures traders; the Sep contract goes off the board on September 15th, next Tuesday

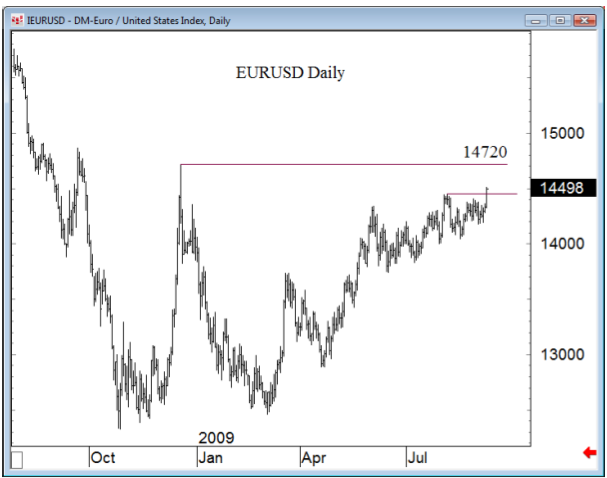

The key level traders were watching in Euro – $ was 1.4450; the euro cleared that resistance today. Next major resistance doesn’t come in till 1.4700-area.

Regards,

Jack & JR

IN THIS ISSUE

• How do we get to peak earnings in the S&P 500, let alone “normalized”?

• Global growth dominated by government initiatives

• Equity market valuation not compelling

• U.S. consumer credit — neither a lender nor a borrower be

• Manpower Inc. employment outlook survey for 4Q not looking good

• Small business optimism

HOW DO WE GET TO PEAK EARNINGS, LET ALONE “NORMALIZED”

Okay, let’s get this straight. We are now being told by the pundits that the reason why Mr. Market is managing to so readily shrug off adverse data is because Mr. Market is discounting “normalized” 2011 earnings of $80. That is behind the latest round of S&P 500 estimates of 1,200. After a momentous 50%+ surge from the lows, anything is certainly possible. But let’s see if it makes sense. First, with household net worth down $14 trillion, employment down 7 million since the start of the recession and consumer credit down $110 billion from last year’s peak, it would seem to us as though there are too many gaping holes to believe we are going to be seeing anything remotely close to “normalized” earnings any time soon. But even if that were the case, it would suggest that the market is trading near a 12x two-year forward multiple. Go back 80 years worth of data, and the mean two-year forward multiple is 7x. Too rich for our liking.

GLOBAL GROWTH DOMINATED BY GOVERNMENT INITIATIVES

We did some digging and found that all of the world economic rebound in 2009 — that is, 100% and then some — is being accounted for by fiscal stimulus. There is still nary a sign that the global recovery is being sustained by organic private sector activity. Oh yes, for 2010, we calculate that 80% of the growth that the consensus is penning in is derived from the public sector. Even FDR would blush over this unprecedented government incursion into the economy. Since the impact from government spending is a second-round effect on corporate profits, it will be interesting to see the extent to which earnings growth come into line with today’s lofty expectations.

VALUATION NOT COMPELLING

With earnings AND revenues down over 20% YoY, it can hardly be said that the fundamentals are very constructive. Current quarter EPS estimates are also down 30% from where they started the year. The technicals and liquidity backdrop are quite positive; however, these give you sharp tradable rallies, but you have to know when to leave the poker table. Valuation metrics are not positive. At the lows in March, the stock market was trading at 13x ten-year trailing earnings. That was the first time since 1991 that the S&P 500 managed to cheapen below the long-run average on so-called “normalized” earnings of 16x (courtesy of Robert Shiller). Fast forward to today — we are back to just around 18x.

….read pages 2-4 HERE.

DUE TO BUSINESS TRAVEL, BREAKFAST WITH DAVE WILL RETURN ON

MONDAY, SEPTEMBER 14

IN THIS ISSUE

• Wage deflation in the U.S.; usage of grocery vouchers, as well as other supplements to the household budget, are on the rise

• Tremendous underemployment; the U.S. economy is actually 9.4 mln jobs short of being at full employment

• Money and money aggregates in the U.S. are now deflating

• Leading job market indicators in the U.S. are not looking good

• A bullish consensus; take a look at page 21 of this week’s edition of Barron’s

• More bank failures in the U.S.; there are now 85 financial institutions that have failed this year

• Another taxpayer-funded bailout? The era of free money is back

WAGE DEFLATION

There are so many headwinds confronting the U.S. consumer it’s not even funny. For a look at the new harsh reality of soaring usage of grocery vouchers, as well as other supplements to the household budget, have a look at the grim article on page 2 of the weekend FT (Families Take Up Food Stamps as Wages Shrink). On the very same page, there is an article on the latest trend in terms of 21st-century breadlines — Middle Classes Turn to Car Park Handouts. To think we still get asked why we aren’t more bullish over the outlook for spending. Truly amazing.

TREMENDOUS UNDEREMPLOYMENT

The U.S. economy is actually 9.4 million jobs short of being anywhere remotely close to being fully employed, which is why any inflation that can somehow be created by the Fed is simply going to be unsustainable noise along a fundamental downtrend in pricing power. After last Friday’s report, we have now lost 6.9 million positions that have been cut during this recession and we have to count in the additional 2.5 million jobs that need to be created — but never were — just to absorb the new entrants into the labour market. The ‘real’ unemployment rate is now 16.8%, so to suggest that this down-cycle was anything but a depression is basically a misrepresentation of the facts. We will certainly take note that (i) the ECRI leading index is soaring to the moon and (ii) the August chain-store sales data came in better than expected. But when you look at the data and the constraints on pricing power, it does suggest that the outlook for profits is far less robust than the markets have discounted — looking at the August retail sales data, it is quite apparent that merchants were very aggressive in their price points and value-oriented chains were the big winners last month. Be that as it may, the year-over-year comps are likely looking better now that we are coming off the detonated figures of late 2008, and on top of that, the lengthening of the back-to-school season could artificially add about a quarter-point to the September chain-store sales numbers.

….continue reading page 2 of 5 HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair