Daily Updates

Ed Note: Richard Russell also loaded up on bonds in the early 80’s when US Treasuries where yielding 18%+. Some of those bonds haven’t even matured in 2011 as they were 30 year bonds. Rough compound interest would turn $1,000 into $311,367at maturity. (include reinvestment of interest income once annually which Richard does). Wow, no wonder RR say’s compounding is the ROYAL ROAD to RICHES)

Thanks Richard-

I remember when you said, “holding on thru this bull will be the hardest thing you’ve ever done”, and “great wealth lies ahead for those that can hold on.” You were so right, I was determined! I bought the “basket of 6 cheapies.” I gritted my teeth and held.

When you said, “silver is cheaper than dirt”, “sell your house, buy silver, later you’ll buy the block”- well, we didn’t sell the house, but we took a down payment we had saved for investment and bought bags of silver (from Leon) and other assorted coins – that money has now almost quadrupled , and, we are buying a small house next door to us – who knows, maybe we will buy the block later, much of it is for sale at ever decreasing prices.

When gold hit $500 and you said, “you should now own all the gold you want to hold”, I made sure to have a lot. When gold hit the high $800’s you said, “last chance to buy gold under $900, it’s still cheap”, we added a little more. You were oh so right when you told us, “2/3’s physical, 1/3 stock”- (wish I would have listened to that, would have saved me some sleep for sure). We did not listen in the summer of 2008 when you wrote, “sell all your gold stocks now”- if we had, we would have a lot more money right now.

So, where are we now- we have over $***,***invested in metal stocks and physical. Really hoping that will turn into enough to help us retire. We also own 2 businesses, (natural food stores) which we’d like to turn over to our kids if we can. We are holding on tight and hoping that you are right once again, and this may be the start of the 3rd phase- we’ve been waiting for this for 10 years now.

I have been reading you since I was 7- for me, a day without Russell is like a day without sunshine. Thank you. I have learned more about investing and the world from you than anyone except my father- another veteran from WW2, no longer alive. You truly are one of the greatest of the “Greatest Generation”.

G-D bless you – or as my grandmother would have said, “ly levin dein kup” (forgive the spelling).

Russell Comment — Good to hear from you, and great to listen to your success story. Every once in a while I get an e-mail that makes me feel good. They can also make me feel old. I get e-mails from subscribers who tell me, “My dad used to read you, and I got the habit.” So far, l haven’t received an e-mail saying “My grandpa read your stuff back in the 1950s.” As for me, I’ll just keep on truckin’.

Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold. Richard and his subscribers also loaded up on Treasury bond @ 18% in the early 80’s when US Treasuries where yielding 18%+. Some of those bonds haven’t even matured in 2011 as they were 30 year bonds. Rough compound interest would turn $1,000 into $311,367at maturity. (include reinvestment of interest income once annually which Richard does). Wow, no wonder RR say’s compounding is the ROYAL ROAD to RICHES) There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The October jobs report contained much bad news and a few belated treats. Employers shed 190,000 jobs and the adult male and teenage unemployment rates are now at post-Great Depression highs. The unemployment rate jumped sharply, despite more Americans leaving the labor force. Fewer Americans are now participating in the labor market than at any point since 1986. When these Americans try to reenter the job market, the unemployment rate will spike again, and now an 11-percent unemployment rate does not seem very far fetched. Men will likely exceed 11-percent unemployment sometime in the next three months and teenagers will probably hit an unemployment rate of 30 percent plus.

There are some glimmers of hope, such as job losses in the previous two months being revised downward. Another is that the temporary-service industry increased employment by 33,700 jobs. A growth in temporary services often portends a growth in the labor market. This sector will be watched closely in the next few months to see if the increase is real or a one month blip.

Hours of work and overtime have stabilized or are even increasing. After the massive downsizing last winter, companies have been cutting hours instead of employees. If that trend has stopped or reversed, then

it is another sign that hiring could be on the upswing.

While the Obama administration promised that the unemployment rate would fall this quarter due to the stimulus bill, the October report shows that job losses are continuing and the unemployment rate will keep

climbing. It also reveals the hollowness of the administration’s claim to have saved or created 640,000 jobs. While the stimulus may have directed funding to that many jobs, that money was taken from elsewhere

in the economy, and the labor market has weakened considerably since the stimulus became law. Congress and the administration should look to encourage private sector businesses and entrepreneurs to invest and

create wealth and jobs instead of trying to centrally plan a recovery from Washington.

Rea Hederman Jr. is assistant director of the Center for Data Analysis and senior policy analyst

the Heritage Foundation. The Heritage Foundation is committed to building an America where freedom, opportunity, prosperity and civil society flourish.

Dollar drifts lower….

Good day… And good morning to everyone. I wanted to start out this morning’s Pfennig by saying my thoughts and prayers go out to all of the families of the fallen soldiers and civilian at the tragedy down at Ft. Hood. It is tough enough when we here about losses of our soldiers overseas in the ‘combat zones’; but such a large loss of life right here in the US is deeply saddening.

I nailed that FOMC statement… WOW! You might begin to think that I have some inside info on the Fed Heads, the way I’ve been able to basically call every move they’ve made since the beginning of this whole meltdown in August of 2007! But that’s not important here… The important thing is that the Fed said that “economic growth is not enough to hike rates, and therefore they will keep interest rates at near zero for an “extended period”…

Hmmm… Where have I heard that before? Any way, I thought that by continuing to use the words “extended period” that the dollar would get pummeled… And momentarily, it looked as though it might, as the offset currency to the dollar, the Big Dog, euro, raced to trade above 1.49… But a funny thing happened on the way to the forum, and the invisible hand reached down and reversed this move in a NY Minute! The work of the PPT? Probably… The Plunge Protection Team, probably stepped in to keep the dollar from a free-fall… That’s my take on it any way!

Any way… With interest rates remaining at near zero levels here in the U.S. I thought it to be appropriate to pull out this new nickname for Big Ben… “Zimbabwe Ben”… (Thank’s Ty!)

The rate hike decision ball gets thrown over to the “pond” to the Bank of England (BOE) and the European Central Bank (ECB) this morning for their versions of: Leave rates at present levels, but try to sound upbeat… I think you’ll have the “tale of two Central Banks” here this morning. While both will keep rates unchanged, I think you’ll see the BOE opt for more bond purchases in an attempt to shore up Britain’s banking system… The ECB will NOT be making any such announcement.

In fact, I believe we’ll hear ECB President, Trichet, announce that the ECB is moving closer to withdrawing stimulus from the economy! So, those of you who have the ability to go long euros VS sterling, this would seem to me to be the “trade o’ the day”… What do I know, I’m not a short term “cross trader”!

So… With the FOMC finished… And the two European Central Banks on the docket today, somehow the Risk Aversion has crept back into the markets…

I received an email from a reader the other day, asking me why I prefer Australia to New Zealand, as the kiwi had outperformed its kissin cousin across the Tasman from 2002 to 2008…. Well… New Zealand enjoyed a wider yield differential than Australia during that time period, as it posted the highest interest rates in the industrialized world… Now that’s saying something right there, and a good reason kiwi outperformed the A$…

But times have changed… And a very timely talk by Reserve Bank of New Zealand Gov. Bollard yesterday, helps explain why A$’s now over kiwi… Here’s Gov. Bollard…

“Both countries have survived the crisis well, due to a mix of strong institutions and stimulative policies. However, their immediate prospects are different. Australia has avoided negative growth, and its prospects are driven by strong terms of trade, vast mineral deposits, the Chinese market, and rapid population growth.

New Zealand has had a recession, and the pick-up is slower and more vulnerable – a difference financial markets do not appear to appreciate.

Australia is a lucky country, but we could be a lucky neighbor.

Australia is entering a new minerals boom, investing heavily and encouraged by new finds, re-opening markets, bottlenecks and strong prices. Strong investment and export growth would mean big challenges for Australian policy. This all means an economy that looks less like New Zealand.

However, Australia’s potential raised the prospects for New Zealand’s manufacturers and services, which have a bigger share of exports than the same sectors in Australia.”

OK… Back to me… So… Australia is a “lucky country” but New Zealand could be the “lucky neighbor”… Makes sense to me!

The Brazilian real rally took a walk on the wild side yesterday, gaining 2.5% VS the dollar in one day! But, that’s relatively tame for some of the wild moves we’ve seen in recent times with the real… As long as you are not watching the currency like a hawk, and sweating out each pip move, this is no biggie… Keep your eyes on the horizon…

I find it somewhat humorous that the Brazilian Gov’t officials have tried and tried to throw down road blocks for the real, and the investors just keep coming in droves… The 2% tax on Capital inflows did nothing to slow down the real’s move VS the dollar, except for the day it was announced… After that, it was Wayne and Garth playing street hockey once more… “Game On!”

OK… I had a few callers and emails yesterday telling me that I was wrong about the Gold sales to the Reserve Bank of India (RBI), saying that it was done in SDR’s… I think the confusion exits in the fact that the Gold sale kept getting reported as $6.7 Billion worth of Gold… But to put these questions to rest… Here is a report from the Economic Times of India (leading financial newspaper)

http://economictimes.indiatimes.com/markets/bullion/RBI-buys-200-mt-gold-from-IMF-to-pump-up-reserves-value/articleshow/5194492.cms

The purchase was in SDR 4.8 Billion worth.

Today in the U.S. we’ll see the Weekly Initial Jobless Claims data, which will remain above 500,000 per week… And the ICSC Chain Store sales figures, which if consumer spending has gone back to pre Cash for Clunkers levels, would mean these figures would be soft… But I don’t think this data gets much playing time with traders, so we’ll just carry on…

And then there was this… OK… So… Some people chastised me yesterday for saying that the Gov’t can’t prove the 650,000 jobs they claim they “saved”… Well… Here’s a ditty for you! Did you know that the Gov’t is claiming that by giving a person that already has a job, a raise, it constitutes as “saving” that job? Want more funny accounting? Stay tuned, same bat time, same bat channel!

To recap… The FOMC left rates unchanged and said they would remain there for an “extended period of time” this sent the dollar to the woodshed, but reversed on a dime… PPT at work? The BOE and ECB meet this morning to discuss monetary policy. Expect the BOE to announce more bond purchases, and expect the ECB to announce a move to withdraw stimulus.. We learned that New Zealand is not Australia, but lucky to be Australia’s neighbor! And try as they might to keep the real from gaining VS the dollar, the Brazilian Gov’t’s moves have not worked…

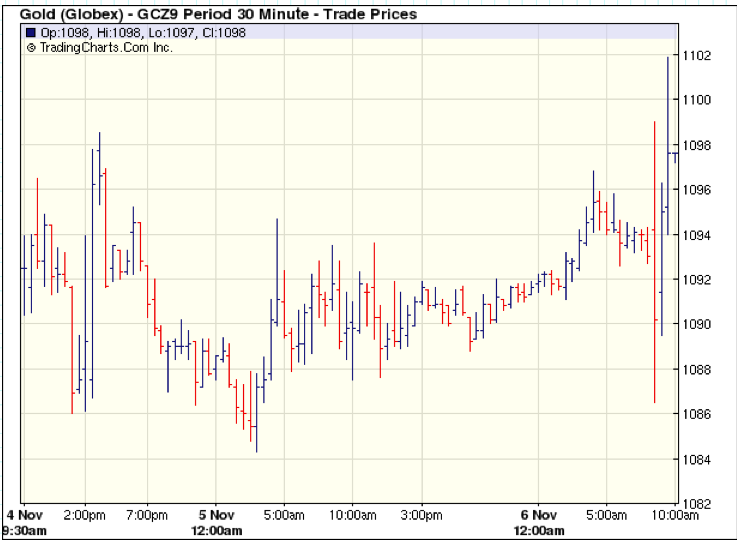

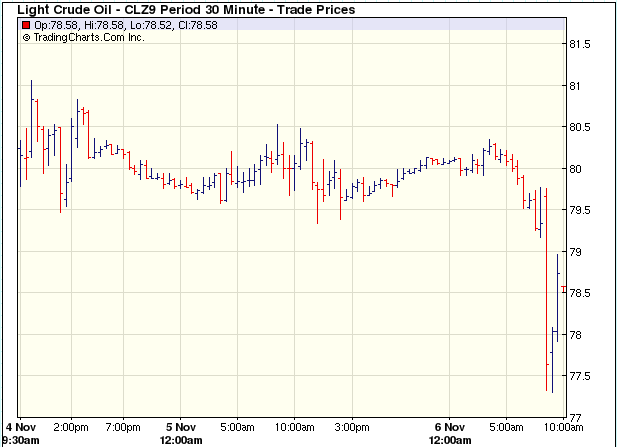

Currencies today 11/5/09: American Style: A$ .9085, kiwi .7190, C$ .94, euro 1.4850, Sterling 1.6530, Swiss .9825, European Style: rand 7.6360, krone 5.6975, SEK 7.0540, forint 186.37, zloty 2.8745, koruna 17.55, RUB 29.15, yen 90.32, sing 1.3955, HKD 7.75, INR 47.02, China 6.8276, pesos 13.28, BRL 1.7255, dollar index 75.81, Oil $79.91, 10-year 3.62%, Silver $17.40, and Gold… $1,088.80

That’s it for today… Writing from home again, as I have yet, another appointment with a doctor this morning. When you have a blood clot, they monitor the thinness of your blood, and it has to be checked every 3 days… So, I have that going for me! I’m taking tomorrow off, so Chris will have the conn on the Pfennig tomorrow… So, as our little Christine would say… This is my Friday! YAY FOR ME! So with that on my mind… Good luck to my beloved Missouri Tigers as they take on Baylor this weekend, and my little Buddy Alex has his last game on Saturday. Congratulations to the Yankees on their World Series Championship… So… I’m off to see the Wizard…

Two decades ago, Chuck Butler embarked on his extensive career in foreign investments as the Director of Operations for the Fixed Income Division of the Mark Twain Bank. He oversaw the clearing and custody of all bond department trades and Mark Twain portfolio transactions.

In 1992, he became the Chief International Bond Trader and Director of Risk Management for the Mark Twain Bank, and was responsible for trading global bonds and currencies, as well and overall risk management. In that same year, Mr. Butler began composing his now decade-old daily currency market commentary, A Pfennig for Your Thoughts-a play on the American aphorism “a penny for your thoughts”(the pfennig is the Germany equivalent of a penny). The Pfennig started as some handwritten market notes and witty anecdotes circulated every morning to help traders stay on top of the economic, currency, and market happenings. Butler’s “Daily Pfennig,” as it is more commonly called today, has become a popular resource for currency investors and traders alike.

In 1999, Mr. Butler joined the team that launched EverBank as the Senior Vice President of EverBank World Markets. He oversees the trading desk and operations for over 12,000 individual and corporate clients, both in the United States and abroad, who look to EverBank for FDIC-insured World Currency Deposit Accounts, and Single Currency and Index CDs . Chuck is also a frequently quoted and respected analyst of the currency market; in 2003 and 2004, he has appeared on, was featured or quoted in, or referenced by: the Wall Street Journal, US News and World Report, CBS Market Watch, USA Today, CNNfn, the Chicago Tribune and many other publications.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair