Daily Updates

We’ve danced around some delicate topics through theyears; subjects that many didn’t want to hear, much less accept.

We flagged Fannie Mae (FNM) and Freddie Mac (FRE) in 2005 before most folks blinked an eye.

We mused in 2006 that seeds were being sown for something “entirely more depressing than a recession” as the markets climbed a slippery slope.

When we offered that Wall Street was technically insolvent in 2007 — as financial stocks were near all-time highs — we didn’t make many friends.

We argued that an invisible hand was responsible for the unnatural bid to the tape and people thought we fell out of our tree.

When we poohed crude in the midst of the 2008 mania — prior to the 75% oil slick — and shared the variant view that lower energy prices would be equity negative, you could almost see conventional wisdom wince.

Indeed, we’ve made a lot of prescient observations — along with our fair share of mistakes — as we navigated the twists and turns of this wild world.

Class Houses

One of our mainstay observations the last few years has been the percolating societal acrimony and an emerging class war between the “have’s” and “have not’s.”

As I wrote in my 2008 Themes:

“The middle class steadily eroded between the lifestyles of the rich and a struggle to exist. Structurally, my sense is that this dynamic continues. The wealthy will endure on a relative basis as the “other side” gets squeezed. What will change, in my view, is the perception of wealth. Black cards, fast cars and private jets will be frowned upon while philanthropy and other acts of selflessness will be embraced.

Channeling Kevin Depew, I continued, “If the 90s were about wealth, accumulation and consumption, 2008 will continue the mean reversion toward something altogether more austere, if not more sensible. Debt reduction and the rejection of (and guilt projection toward) materialism will continue what began in 2006 and 2007 as meditations on not just doing more with less, but doing less… period.”

I continued that thread of thought in this year’s themes when I shared:

“The age of austerity has officially arrived and we’ll see a steady stream of social strife as the rejection of wealth increases in size and scope. While societal acrimony began to percolate last year, this dynamic will manifest through social unrest and geopolitical conflict as we edge ahead.”

Now, please understand I’m an optimistic person at heart. The mission of Minyanville is to effect positive change through financial understanding, not beat a steady drum of dire predictions.

It’s not always fun — and not always right — but as I told a producer in September 2008 when she whispered in my ear to be “more optimistic,” immediately preceding the financial meltdown, my opinion isn’t for sale.

What’s my point? Glad you asked; I sometimes have a tendency to go on tangents.

We’re not in Kansas anymore. What was once a craft — trading was an art, not a science — has turned into a polarizing profession predicated on predicting unforeseen actions of government entities and the corporatocracies they protect.

This isn’t sour grapes or a random rant; it’s simply what is, whether we like it or not.

Of Mice and Markets

Free market capitalism; the mere mention invokes deep-rooted responses.

For some, it’s a longing for simpler times when an assimilation of primary trading metrics allowed for honest pay after a long day. For others, it’s an opportunity to unleash vitriolic criticism on anyone and anything associated with Wall Street. Pick a side or stand aside, people, the nation is dividing as we speak.

I believe history books may one day look back at Shock & Awe — or perhaps, 9/11 — as the beginning of WW3 when it was broadcast on CNN.

I’m not talking about a nuclear winter; I’m simply saying the entire global dynamic seismically shifted in that short stretch of time and the needle is now pointing towards an entirely unfortunate direction.

Societal acrimony to social unrest to geopolitical conflict; it’s a trifecta that won’t pay off for anyone.

I share these thoughts with genuine intentions. When I read stories about Goldman Sachs (GS) employees arming themselves with pistols so they’re equipped to defend against a populist uprising, I take notice.

When I see Ahmadinejad thumb his nose at the US and Russia — and call out Israel, which already has an itchy trigger finger — I take notice.

When benevolent gestures and philanthropic efforts are immediately met with suspicion and distrust, I take notice.

I view the world through a somewhat binary lens. On one side, there’s painful yet inevitable debt destruction that will eventually lead to a prosperous outside-in globalization. That scenario requires lower asset classes, a higher dollar and a lot of patience. The US likely won’t lead the world higher but that’s all right; a little humility will go a mighty long way.

On the other side, there is more credit creation, more stress on the system and cumulative imbalances that are destined to manifest in a meaningful way. I’m not smart enough to know how or when, but the “why” is self-evident. When the next phase of crisis arrives, it will be one of confidence that could shake our socioeconomic construct to the core.

Harsh? Yeah, it is. Imminent? It doesn’t feel that way, and corporate credit markets suggest it’s not. Looming and ever-present? You betcha, and I’ll again use the magic word: cumulative. As social mood and risk appetites shape financial markets, we would be wise to watch for the next progression of problems, be it sovereign defaults, state bankruptcies or commercial real estate.

There are, as always, two sides to every trade and the bullish bent is akin to a relay race; the government-sponsored euphoria handed the baton to corporate America (which rolled mountains of debt and issued tons of equity) and the transfer of risk will land in the lap of an unsuspecting public. Yes, the best-case scenario doesn’t cure the underlying disease; it simply masks the systems and pushes risk further out on the time continuum, perhaps all the way to our children.

Know this; it’s of no benefit to me or my business to communicate this view but I’ll always give it to you straight; sometimes right, sometimes wrong, and always honest. I offer these thoughts not only to open some eyes, but also to ask for help. As we’re apt to say, if you’re not a part of the solution, you’re part of the problem and society is simply a sum of those parts.

Now, more than ever, we need proactive problem solvers as we edge ahead through this uncertain world.

R.P.

For more on how to play what’s going on in the world take a FREE trial to our Grail ETF & Equity Investor newsletter. This morning’s edition contained 4 international plays using ETFs.

Todd Harrison, founder and CEO of Minyanville, has 18 years of experience on Wall Street.

After graduating from Syracuse University with honors (1991), he spent seven years on the worldwide equity derivative desk at Morgan Stanley (vice president). In 1997, he became a managing director of derivatives at The Galleon Group. Three years later, he joined $400 million hedge fund Cramer, Berkowitz as partner (head of trading) and was President from January 2001 until January 2003.

Minyanville Media, Inc. (MMI) is an Emmy Award winning content and community platform. MMI creates branded business content that informs, entertains and educates all generations about the worlds of business and finance. Minyanville is a place where people who seek useful, unbiased information come to learn, laugh and connect. MMI strives to raise the level of financial understanding by connecting with a highly desirable audience through insightful commentary laced with humor and humanity. This distinguishes MMI by creating a true intersection of Wall Street and Main Street.

Some thoughts on the gold market today Posted by Peter Grandich at 8:57 AM on Wednesday, December 9th, 2009.

It is an excellent and detailed posting…..go HERE to read and view the charts.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar. For a trial Subscription of The VR Silver Newsletter CLICK HERE

STOCKS – ACTION ALERT –

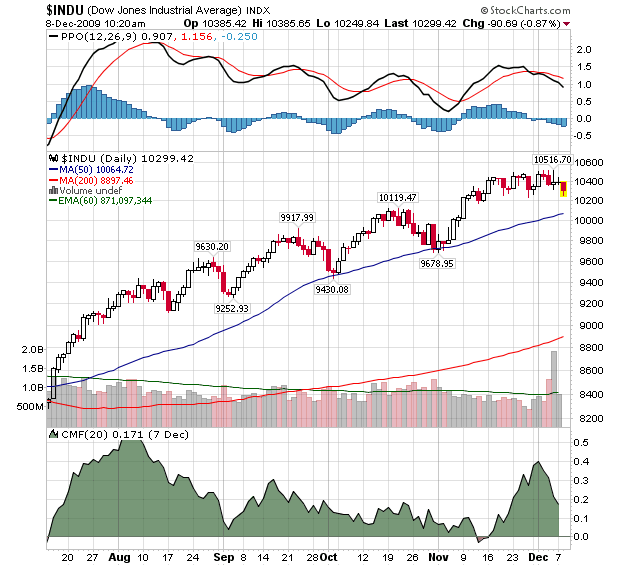

It was ‘Turnaround Tuesday’ and the market showed lived up to its reputation for volatility. Today is ‘Weird Wally Wednesday’, the Wednesday of the week prior to options expiration (third Friday of the month) which also usually hosts some volatility. The ‘usual’ pattern would be to witness a retracement part of this week to be followed by a strong recovery into next week’s options expiration.

Meanwhile, the sell-off was attributed to disappointing news from Dow components McDonald’s and 3M, another decline in the Dubai stock market, a downgrade of Greece’s debt, and credit concerns about the U.S. and U.K trade deficits, sent the risk averse fleeing from equities and commodities and towards the dollar and US Treasuries. (See all the stories in the news section.) For the session, the Dow was off 104.14 at 10285.97, the S&P 500 was off 11.92 at 1091.93, and the Nasdaq Composite was off 16.62 at 2172.99. Volume increased over Monday and breadth was weak.

The S&P 500 broke but managed to hold support at the 1080 level. Negative Volume Reversals ™ have been formed and the market certainly looks heavy. Cyclically, however, my work had a ‘cycle change point’ due on or about December 9 (today) and with all the ‘bad news’ yesterday we could very well see the market recover.

Gold, too, continued lower, but I saw the current sell-off coming and advised clients ahead of time (actually a few days early) in our VR Gold Letter.

For the most part, I am sitting on the sidelines with some modest positions for Platinum subscribers with one short recommendation in Gold via an inverse ETF which I’m inclined to sell and look to take profits here or on any further short-term weakness.

The culprit is the U.S. Dollar which has suddenly become the bastion of safety for unsafe economic world whose strength has now put pressure on stocks and Gold. Do I believe it will last? No. Do I believe we’ll see new Dollar lows? Yes. The rally in the Dollar is a mirage. The trend in Gold is unmistakenly higher (except for this current correction). The trend of the stock market is still overall higher if you look at weekly and especially monthly charts of the major indices, but we cannot dismiss the risk of a correction and following my Volume Reversals ™ you have to be cautious here until positive volume appears and/or we manage to break out to new highs. As I mentioned yesterday, recent strength in the leading Dow Transportation Average cannot be ignored.

We have many year-end cross currents at work from tax loss selling to investment managers seeking to ‘ring the register’ and get paid awaiting the New Year to implement investment strategies.

At the same time I am not Pollyanna. I realize that the market could have really topped or is about to and a more serious correction lies ahead – perhaps a couple thosand points to the downside in the Dow Industrials. There are just some times (like now) when keeping a low profile makes sense. You don’t have to be invested in them market all the time and this may be one of those moments.

I am looking to have a restful and quiet holiday season and not looking to take on any unnecessary stress. Until my 2010 Annual Forecast Model is completed, I hope to do as I’ve just said – be patient!

Energy (XLE -1.7%) and materials (XLB -1.6%) were among the worst performers on the day as commodities got hit by the rising Dollar. Each declined on an increase in volume.

All nine market sectors are down, though Utilities (XLU) held up the best, yet again, falling just 0.4%.

The gold miners ETF (GDX -4.04%) continued its ugly slide on solid volume as gold (GLD -1.91%) and silver (SLV -2.92%) continue to correct.

This push lower in equities may be short lived, however, as money flowed into high yield bonds (HYG +0.12%) and semiconductors as the PHLX Semiconductor Index gained 0.07% in the face of obvious negativity yesterday.

These bright spots may or may not be enough to hold up the broader market, however. Watch the November 27 low on many of the charts. That is the line in the sand. If that gives way, a larger correction is unfolding.

Looking at the S&P 500’s MACD and RSI, it is establishing yet more negative technical divergences. As long as the market sets higher highs and higher lows, which it has continued to do, these divergences can be ignored. But they are early warning systems and could signal bad things ahead if support is broken. Look for support at the recent lows just above 1080, 50 day moving average of 1080, and at the bigger lows of 1020 and 1030.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

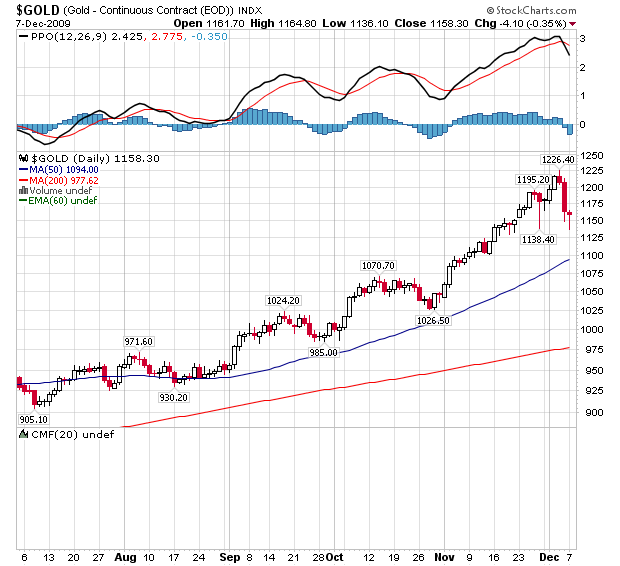

On Thursday of last week, gold hit an all-time high of $1,227 an ounce. Since then, gold’s price is down to $1,145 per ounce for a quick loss of nearly 7 percent.

Strong U.S. employment data were cited as the reason behind this move and other fireworks in the financial markets.

After the data release stock prices shot up, but finally closed way below the day’s high. That’s a rather disappointing outcome for bulls expecting a year-end rally to begin soon.

The dollar also caught a bid and rose two cents against the Euro — not giving back this gain later on.

Lastly, Treasury bonds got hit hard, down more than a full point, extending a losing streak which cut 30-year bond prices by four points in as many days, another very sharp move.

The technical pictures of all of these markets were already weak and point to an overdue correction. The release of better-than-expected employment data seemed to be a welcome trigger — but nothing more.

For some clarity, let’s take a closer look at the dollar versus the euro …

A Normal Short-Term Euro Correction

After rising from below 1.30 to slightly above 1.50, or 15 percent in seven months, some kind of a correction should be accepted as normal.

First, technical support comes in at 1.45. If the Euro declines to this level, it’ll mean that nothing spectacular happened, just a normal flow of the tides. Hence, it’s not yet time to make much out of this short-term reversal.

After a month-long rise, a larger correction is not a surprise.

Then There’s the Amex Gold Bugs Index …

As you can see on the chart, just a few days ago this gold mining index was back to its all-time high of early 2008. It’s the first index having achieved that feat. This extraordinary absolute and relative technical strength is containing a very bullish medium- and long-term message for this sector. I fully expect an outbreak to new highs and more spectacular gains to follow relatively soon.

But a short-term correction beginning at this distinctive point definitely wouldn’t hurt. It’s a typical resistance area. To take a deep breather here could be just what the doctor ordered to get in the right shape to stage the next huge rally phase.

After returning to the all-time high of 2008 some kind of a correction is but a healthy and refreshing move.

Bottom Line: Gold’s Medium-Term Uptrend Is Still Healthy

Finally, let’s look at gold’s price chart. After the breakout of this huge consolidation formation at approximately $1,000 an ounce, a fast uptrend followed, lifting gold’s price by about 20 percent.

This very healthy trend does not exhibit any signs of weakening. There are no negative divergences or even short-term trend breaks. This medium-term uptrend is fully intact.

At this stage of the bull market I expect no more than a short-term correction lasting just a few weeks. And I see no change to the fundamental picture, either.

I expect the current correction to turn out as nothing more than a short-term hiccup, akin to the correction of November 2007. It may last a few weeks and bring prices down a bit more. But in the end it will turn out to be just another buying opportunity.

Best wishes,

Claus

Claus Vogt is the editor of Sicheres Geld, the first and largest-circulation contrarian investment letter in Europe. Although the publication is based on Martin Weiss’ Safe Money, Mr. Vogt has provided new, independent insights and amazingly accurate forecasts that, in turn, have contributed great value to Safe Money itself.

Mr. Vogt is the co-author of the German bestseller, Das Greenspan Dossier, where he predicted, well ahead of time, the sequence of events that have unfolded since, including the U.S. housing bust, the U.S. recession, the demise of Fannie Mae and Freddie Mac, as well as the financial system crisis.

He is also the editor of the German edition of Weiss Research’s International ETF Trader, which has delivered overall gains (including losers) in the high double digits even while the U.S. stock market suffered its worst year since 1932.

His analysis and insights will be appearing regularly in Money and Markets.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

4:25 PM on Monday, December 7th, 2009

It’s been quite hectic on both work fronts for me and I’m only catching up as I type. I do want to thank Stan Bharti of Forbes & Manhattan for an incredible time while in Toronto. Not only was I very impressed by the depth and knowledge of many of his staff but also his down-to-earth manner went a long way with me and Joe Klecko. I didn’t think there was another Hunter-Dickinson type out, there but ND and Forbes & Manhattan clearly have some similar qualities.

U.S. Stock Market – If not for the fact that we’re in the midst of one of the most favorable seasonal periods for equities, I do believe I would’ve already pulled the trigger of putting my bear suit back on. The lower end of my 10,500 – 11,000 DJIA has been hit but I’m holding off in hopes of not being the Grinch (Grandich) that stole Christmas. Stay tuned.

Gold – I’ve said it for over six years now and from just above $300: gold is in its greatest secular bull market ever and there are no real signs of a major top. I’ve also stated all the way up that it’s hated by most in the financial services industry and the financial media and to never expect it to be viewed favorably by most.

As noted in my update the morning of December 1st, I placed most gold-related holdings on hold because my 2009 price objective of $1,200 was reached. The inevitable correction soon followed and with any good fortune, it will last long enough to get gold off the front page again and allow the gold perma-bears a chance to come out from underneath their desks and pound what’s left of their chests.

One note on the perma-bears. I mentioned two by name a couple of months ago. One of them was since fried in the press for his overall poor performance and the other, well, he doesn’t need any help in showing what he really is and isn’t. He is the Andy Smith of the 21st century and when gold gets to $1,500+ in the next 12 – 24 months, he, too will be like Smith when people ask, “whatever happen to….?”

Gold has held the low around $1,130 again and even if it breaks below, I believe the area where India bought its gold on either side of $1,050 is the total risk to the downside. Again, as I’ve said for years, the surprises should mostly be to the upside.

I welcome this correction/consolidation and hope it can last for much of the remainder of 2009. But to those who have high hopes of a gold price with three digits again, I truly believe that can only occur by an event I just can’t fathom at this time. As a forty year NY Jets fan, I’ve learn to fathom the unfathomable-lol.

U.S. Dollar – Despite all sorts of media reports and 24-hour vigils by the gold perma-bears for a dollar rally, the terminally ill Uncle Sam representative still can’t get above 76.50 on the U.S. Dollar Index. It needs to have two consecutive closes above that level before any legitimacy to a bear market rally can take hold. Because we’re going to see conditions get thinner as we draw closer to month and year-end, moves in this and other markets could be exaggerated so we must be careful not to get too caught up until after the New Year.

I believe the sharp decline in oil shows the rise in oil was as I suspected–dollar driven versus improving fundamentals. Natural gas remains uninteresting from either side.

The Model Portfolio has been updated.

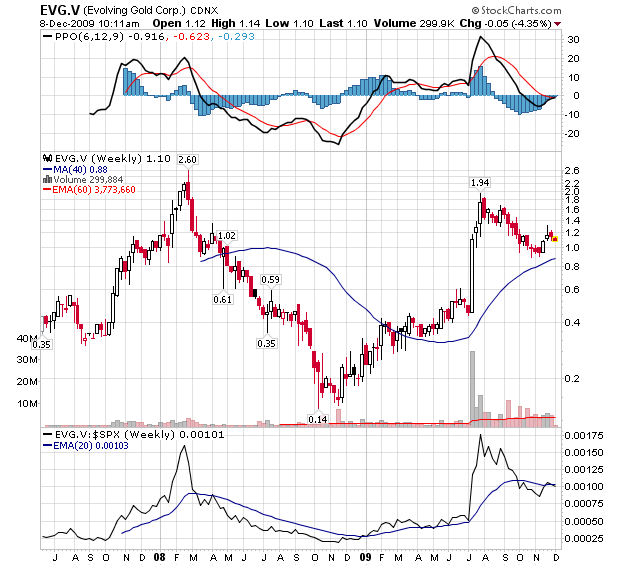

Evolving Gold (EVG-TSX-V $1.13) has engaged my services. I’m very optimistic for 2010 and beyond. The stock will remain in my model portfolio because it was a recommendation before becoming a client. I prefer not to give buy and sell on clients but since many people had already bought EVG per my model portfolio, they’re deserving of a continuing opinion.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair