Daily Updates

THE DOLLAR INDEX… In Monthly Terms… and We Stand By Our Watershed Comment: We turned bullish of dollars… primarily against the EUR… several weeks ago when we issued our “WATERSHED” shift in sentiment. Thus far that has proven wise. A close for the EUR below 1.4250 would “secure” our thesis and secure our position. – Dennis Gartman

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website

China Puts The Brakes On!

by Chuck Butler – EverBank World Markets

Good day… And a Wonderful Wednesday to you! As I understand it, we are in for some Monsoon like rain today and the next couple of days… Living in a little river town, and having a creek at the back of my property, lends itself to cause me to worry when I hear things like Monsoon like rains expected… But… It’s mother nature, I can’t do a thing to stop it, so, I carry on… But worrying while I carry on!

The rain is falling on the currencies too… The dollar has rebounded very quickly the past few days, and there are no roadblocks right now(Ed. Emphasis mine) The risk takers in the markets are running for safety again, sent running by China’s decision to curb lending and attempt to slow growth before their economy overheats…

You see, China was the linchpin for risk taking… For, with China growing, commodities were in need, and commodity countries were very happily sending those commodities to China… The Commodity Countries would then be flush with cash, rising job creation, and be confident about their future… Interest rates would rise to combat inflation in the Commodity Countries, and the Karma would be flowing for each respective currency…

But, China said… Whoa there partner! (say that like John Wayne would!) And… I don’t blame them… They seemed to be the only major country that was experiencing economic growth, I mean China’s most recent quarter will probably show GDP at 10%! Hey! It takes two to tango! And in China’s case, it takes more than two to tango… So… They decided to throw some cold water on the heating economy, and see what they have when the smoke clears…

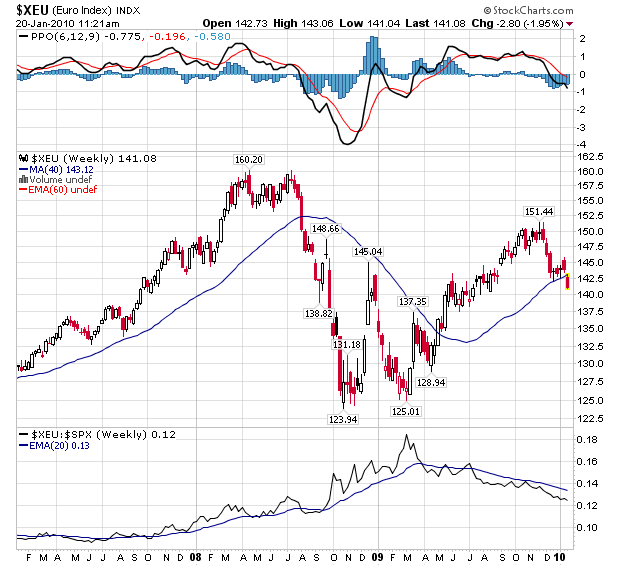

So… As we start today, the euro has fallen to below the 1.42 handle, after spending most of yesterday gaining back lost ground to the dollar. The Aussie dollar, which just 10 days or so ago, was heading toward 94-cents, has fallen below 92-cents, and so on… Shoot Rudy, even the darling of recent times, the Canadian dollar / loonie, has dropped back a bit… Risk taking is off the table…

The question is… For how long? In the past year, whenever risk aversion set in, it really didn’t last too long, and all it did was provide cheaper levels for investors to buy! So… The question du jour is how long will the Risk Aversion last before investors get tired of the paltry yields available in places like the U.S., and Japan… The two countries that seem to be favorites of the Risk Aversion campers…

Yesterday I told you about the rising prices in things that I got from Larry Edelson’s newsletter… today, I’ll tell you about a few story headlines that I came across last night on the Bloomie…

1. U.S. Hog Prices `Rampage’ Higher, Pork Demand `Caught Fire,’

2. Florida Freeze Kills Estimated 70% of Southwest Tomatoes, Other Vegetables

3. Sugar Rises in N.Y. on Speculation Supply Deficit to Widen;

So… the “deflationists that don’t believe inflation is creeping all around us and ready to take our economy under, should pay attention here… Pork prices “rampage higher”… Florida freeze kills 70% of tomatoes, Sugar rises…

AS I’ve said before… this is just great… NOT! Soon we’ll not only have a dollar that’s robbing us of our purchasing power, but what dollars we have left will be getting eaten away by inflation… Where do I sign up for that?!

Also… I want to talk about something that I wrote yesterday regarding why the euro was seeing a slide down the slippery slope… I said it was the “German Investor Confidence falling again… but the more I thought about it, and then a reader asked me about it, I knew that the Massachusetts election was playing with fire in the currency markets too… The currency traders were looking the possibility of a Republican victory, which would not be a good thing for the health care bill, and therefore the dollar wouldn’t have to worry about an additional $1.5 Trillion in deficit spending if the health care failed…

But as I told the boys and girls here on the desk… That still leaves $2 Trillion in deficits for this year that have to be financed… and I’ll let you in on a little secret that’s just the Robinson’s affair… that last year’s Treasury buying was propped up by U.S. financial firms that sold their toxic waste bonds to the Fed, and then took the funds and invested them in Treasuries… That plan that came together to work all that out? It is supposed to end in March of this year… So… without those financial firms buying The Debt, who will be there to pick up the tab? I’m very serious here folks… This is HUGE… Foreigners only bought about 1/3rd of our Treasuries last year…

Remember when I kept talking about the TIC’s data, and wondering why the dollar wasn’t getting punished? Because on the other side of the cocktail napkin, the Treasury was selling to financial firms, and the Fed, as I documented in the past… And all that comes to an end in March… Hmmm….

OK… I’ve been doing a lot of thinking about the Greece thing… and I know that I’ve ranted about how it shouldn’t be on the minds of investors over the problems in California, New York, Illinois, Michigan, etc. but… it is… and so I think we need to deal with this, talk about it…

Now, you know my stance on the bailouts here in the U.S. and that hasn’t changed, but it happened, and that’s now water under the bridge.. the river may be swelling to take away that bridge, but it’s water under the bridge today…

Well… It now looks like Germany is going to have to step in and bailout Greece… yes, I know that some European Central Bank (ECB) members have talked tough on Greece… I also don’t believe that they would jeopardize the European Union and the euro by ignoring Greece… So… I now feel as though Germany will have to step in… If they don’t… it could have a domino affect and cause some major harm to the euro… So, that’s something to watch for…

The major harm might be short-lived… sort of like the slowest buffalo theory… where the slowest buffalo gets killed, but makes the herd faster… Greece would be the slowest buffalo here… OR… it could send things spinning out of control in the Eurozone… So… in this case, we will have to go with Germany stepping in…

So… Last week, I carried on about the Fed making $52 Billion last year, and wondered why this wasn’t as big a deal as Exxon/ Mobil’s huge bonanza a couple of years ago… I mean, at least when Exxon/ Mobil made Billions, there were stock holders that benefitted… Normal people, moms and pops, etc. When the Fed had the bonanza it handed it over to the Treasury, which some would think would go back to the taxpayers… Yeah, right…

But, I got to thinking this past weekend about the bonds the Fed is holding… No wonder they don’t want to see interest rates rise! For, if interest rates rise, their holdings would take on water, and… The Fed has stated that they intend to sell these bonds back to the markets some day… Well, try doing that when interest rates have risen on your bond holdings!

And… What happens if interest rates rise so high that the Fed starts taking on water, with negative interest rates spreads on the their holdings? Talk about cries to audit them then!

OK… Let’s go on to something else… This Fed / Treasury stuff gets me so riled up, and I start pounding on the keys! I’ve had to have my keyboard replaced about a dozen times in the past 10 years, but mostly in the past 5 years… Besides pounding on the keys when I’m typing something that ticks me off, there are times I just pick the keyboard up and slam it down on my desk! Now… Those of you who have ever met me at shows, etc. would think, not Chuck! He’s so mild mannered, and easy going! It’s my evil twin that does these things, folks…

Gold had a mini-rally of $5 during yesterday’s trading, but overnight has sold off $9…

I want to make something perfectly clear, that I’ve talked about before regarding Gold… When I talk about Gold, I’m also talking about Silver… I just don’t want to have to type Gold and Silver every time I’m talking about the precious metals… Silver is another store of wealth… In the December Currency Capitalist, I talked about giving the gift of Gold, and teaching whomever you gift it to, the lessons of wealth building… When my older kids were youngsters, I bought them Silver coins, for I could not afford anything else then… Those Silver coins have proved the point of providing a store of wealth, as they have never gone to zero, and have gained in value over the years!

OH! And the Bank of Canada left rates unchanged and kept their statement pretty much the same at their meeting yesterday. So… There was nothing there for the Canadian dollar / loonie…

And… It looks as though I was barking up the wrong tree yesterday with my call that New Zealand’s inflation would be higher than expected, thus moving the Reserve Bank of New Zealand (RBNZ) to hike rates sooner than expected… New Zealand inflation actually fell in the 4th QTR .2% putting the annual inflation rate smack dab on the RBNZ’s ceiling target of 2%… Now.. Having inflation at your ceiling target rate isn’t anything to ignore… But this is going to push back my call for higher interest rates by 75 BPS by summer… It will probably only be 25 BPS and maybe 50 BPS by summer…

Across the Tasman in Australia… Australian Consumer Confidence rose in January by the most in 6 months! Here’s another data piece that goes in the “pro” column for a rate hike in February by the Reserve Bank of Australia! (RBA) Job creation is strong as witnessed by last weeks jobs report, and now we have Consumer Confidence rising 5.6% last month! I would have to think that this pretty much nails it down for the RBA, and rates will me hiked at the Feb. meeting… Which, would put Australia rates a full 3.5% ahead of U.S. rates…

And then finally… I know I’ve gone on and on today… But finally… There was this… Our Foreign Bond Trader, Don Ries, came over to show me a bond issue that he found yesterday… Now… I must say that bonds are done in our brokerage, EverTrade Direct Brokerage, and are not FDIC insured deposits of EverBank… OK, now that I have that out of the way… OH! And this is NOT A SOLICITATION TO SELL THIS BOND! It’s simply information to make you aware of things… The bond was a 7-month bond, issued by a supra-national bank, the IADB (Inter-American Development Bank) that’s denominated in Brazilian real, that yields 7%!!!!

So… The reason I’m telling you this, is simply to show you one of the reasons the Brazilian real was posting a 35% return VS the dollar last year, and why the Brazilian Gov’t was doing whatever it could to slow down the real’s appreciation, which by the way, they have done! When you have bonds denominated in your currency yielding more than 300 BPS higher than the rest of the world, you’re going to see a ton of interest in your currency to buy the bonds…

I’m still of the belief that the Brazilian Gov’t’s plans to stem the currency’s rise will run out of steam… To me… It’s just a question of when…

Oh! And one more thing this morning… I don’t know if you track this or not, but the Hong Kong dollar has been slipping in value VS the dollar recently… I find this to be a strange thing, in that the honker is supposed to be pegged to the dollar…

A couple of years ago, I made a call about honkers saying that China would allow the honker to float first, since it was the more mature currency, and see how that worked out, before doing so with their renminbi… Could this be the beginning of that? Too soon to tell… But to see honkers losing value VS the dollar is strange… Strange indeed!

Well… The people of Massachusetts voted yesterday, and I think it says a lot when a state like Massachusetts doesn’t elect a Democrat… Maybe, just maybe, the Gov’t will get the message that deficit spending is not an approved thing by voters any longer!

To recap… The dollar is much stronger today, as Risk Aversion has settled back in the currencies, on the back of China attempting to cool down their economy. And then I carried on about all kinds of things!

Currencies today 1/20/10: American Style: A$ .9135, kiwi .7210, C$ .9635, euro 1.4165, sterling 1.6270, Swiss .96, European Style: rand 7.50, krone 5.7490, SEK 7.1550, forint 189.75, zloty 2.8375, koruna 18.2575, RUB 29.64, yen 90.80, sing 1.3980, HKD 7.7660, INR 45.92, China 6.8270, pesos 12.71, BRL 1.78, dollar index 78.06, Oil $77.90, 10-year 3.67%, Silver $18.54, and Gold… $1,129.50

That’s it for today… Whew! My fingers are tired! Well… I sure had a lot to say today… It was good to see my brothers and sisters (minus one in Houston) last Saturday night. There were 7 of us… We lost my oldest sister to cancer, but remaining 6, have gone our separate ways, and seldom all get together… I just saw that an after-shock had hit Haiti… That country can’t catch a break… There are heart warming stories though, like the German dog team that pointed out people caught beneath the rubble, and were rescued… Well… The Butler boys will be “batching it” for next 4 days, starting tomorrow morning, as my beautiful bride goes skiing with her “sorority sisters”… That means I’ll be writing from home, and we all know how much I enjoy doing that! NOT! My little buddy, Alex, and I will be eating healthy in Kathy’s absence… Yeah right! OK… Time to go… I thought I was early, but now it’s late… UGH! I hope you have a Wonderful Wednesday…

Chuck Butler

President

EverBank World Markets

1-800-926-4922

1-314-647-3837

Market analysts including Howard Ruff, long-time financial advisor and founder of the 35 year-old investing newsletter The Ruff Times, are becoming quite bullish on uranium mining stocks. In a recent interview with The Gold Report, Ruff acknowledged his enthusiasm for uranium mining plays.

“Uranium mining interests me because there’s going to be demand,” he explained. “There are enough nuclear plants either under construction or on the drawing boards and there’s only half enough uranium above ground to service their needs.”

For those who like to play it safe, big producers and development companies with identified resources in the ground offer the best investment prospects for this sector, advises Ruff. Of course, investing in uranium explorers can be quite profitable, but should be left to those not adverse to risky endeavors.

Cameco to Make a Play for Paladin?

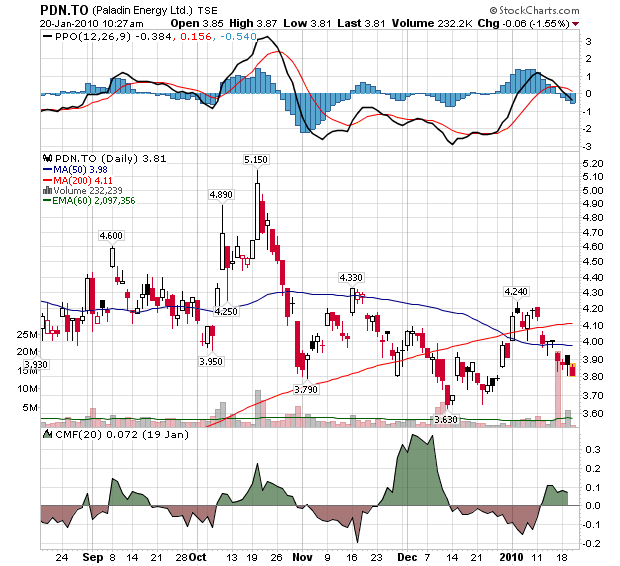

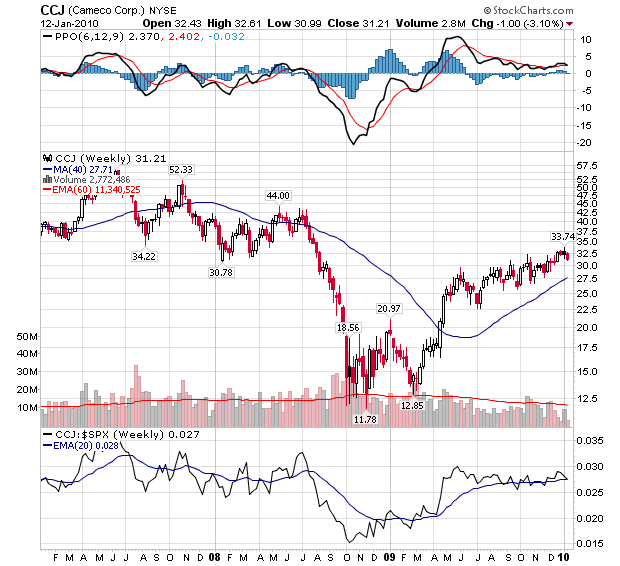

There’s a lot of speculation swirling in the marketplace about the prospect of Canada’s mining giant Cameco making a bid for Australia’s Paladin Energy.

Cameco, the world’s second largest uranium producer, is looking to double its annual uranium output from its current holdings by 2018. Adding some additional producing mines to its largesse would go a long way toward securing its already prominent foothold in the uranium supply market.

Back in November 2009, Cameco CEO Jerry Grandey said the miner was seriously considering acquisitions and mentioned Paladin as an attractive target. The main drawback, however, is the cost. “We’ve always been challenged by the valuation,” Grandey said.

RBS analysts Lyndon Fagan says Cameco would most likely need to fork over a premium of more than 30 per cent Paladin’s current share price. The Australian Financial Review says the takeover could cost $3.7 billion.

A 15 per cent retreat in the Australian miner’s share price over the last three months may have Cameco salivating. “I think Cameco would certainly be looking at Paladin,” said Fagan. “Paladin’s share price has been underperforming recently because of failing to deliver on production targets, and the recent weakness could provide an opportunity for the likes of Cameco.”

On Tuesday, shares in Cameco [TSX: CCO] were trading at $31.62. Shares in Paladin [ASX: PDN] were trading at $4.06.

Khan Resources Update

Last week, Khan Resources [TSX: KRI] announced the mining licence on its joint venture project on the Dornod deposit in Mongolia has been reinstated after a temporary suspension in July of last year.

The licence suspension came about as a result of the Mongolian government’s enactment of a new Nuclear Energy Law, which allows the government to take ownership without payment of at least 51 per cent of any uranium project with resources that were determined through exploration with state funding. The law even gives the government the right to take at least 34 per cent of projects developed even without the use of state funds.

Khan’s involvement in the Dornod project is as a partner in the Central Asian Uranium Company (CAUC). The miner has a 58 per cent interest in the property. The Mongolian government (21 per cent) and Russia’s state-owned Atomredmetzoloto JSC (21 per cent) are also partners.

Khan has received notice that the government may decide to increase its holdings to 51 per cent under the new legislation. “We view this notice as part of the process of implementing the new Nuclear Energy Law”, said Khan CEO Martin Quick.

Khan’s shareholders have until January 31 to come up with a “favourable resolution” or the mining licence could be revoked once again.

“We have been working cooperatively with representatives of the Mongolian government in an effort to reach a mutually satisfactory arrangement that will provide the framework which allows the government of Mongolia to achieve its goals while also protecting Khan’s investment in the project and enabling us as the operator to proceed with the development of the mine,” said Quick.

Khan is also facing a hostile takeover bid from their other CAUS partner, Russia’s ARMZ. Late last year, ARMZ issued a bid for all of Khan’s shares, which Khan’s management has urged shareholders to reject on the basis that it smells of opportunistic greed and is highly inadequate.

Are the Mongolian government’s actions towards Khan a part of ARMZ’s strategy to muscle Khan out of its stake in a key resource deposit? One wonders.

For more Uranium News go to Uranium Investing News

Let’s look at what the euro has done against the US dollar compared to what the Chinese currency has done since the last dollar bear market began. Below is a percent change chart with the starting date June 1, 2002. As you can see, the euro (purple) has gained 54% since that time; while the juggernaut of global growth from China-the yuan-has moved about 0% since that time. Thus, the euro has appreciated about 54% against the Chinese currency too.

Quotable

“The UK recovery is likely to be sub-par, but it would be unwise to write off the prospects for a stronger recovery. However, assuming a sub-par recovery, monetary policy tightening is unlikely before the end of 2010. What happens to monetary policy will also be substantially affected by what happens to the fiscal outlook (with the election a major complicating factor). On fiscal policy, we continue to think that more needs to be done than on the existing government’s plans. Debt issuance will remain enormous in 2010-11, and without Bank of England buying there will be a shift in the balance of supply and demand. However, we think that demand worries are overdone and that worries about UK solvency remain significantly overdone. However, the (albeit weak) economic recovery will ultimately ensure higherbond yields. The prospect of higher bond yields is the main reason why we remain cautious on UK equities.” – Morgan Stanley Economic Forum

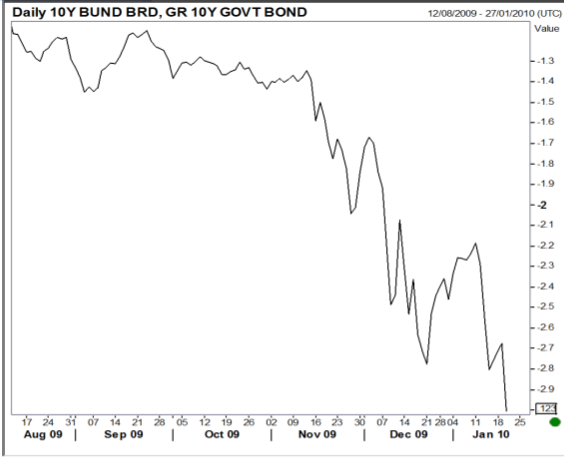

- Greek government bonds tumbled, led by two-year notes, after European Commission President Jose Barroso said the region’s economy is at a “delicate moment.” (Bloomberg)

Note: Below is a Greek vs. German Bund 10-yr bond spread chart we showed you in Monday’s Curency Currents; we were expecting the euro to follow…it has and is being punished this morning.

- The China Banking Regulatory Commission said it hasn’t “specifically” told banks to suspend lending in January, but a report that it had asked several banks to stop issuing loans helped to send equity markets tumbling. (WSJ)

…..read more HERE

The reality is that bullish sentiment on gold right now is infinitely higher than it is for silver; and keep in mind that while gold is the most malleable metal of all (the only metal that will look the same 1,000 years from now as it does today), silver pieces going all the way back to pre-biblical times were the primary medium-of-exchange (fiat paper currency, in the overall scheme of things, is a relatively new phenomenon and a convenient one for politically sensitive central banks). How well known is that up until 1968, silver certificates were redeemable for an equivalent amount of silver?

….read David Rosenberg’s whole comment “Silver Linings” (scroll down to the title) HERE

As many of you already know, I am very bearish onthe dollar.

And in just the past four weeks of trading — starting right before the holidays and continuing into the new year — the benchmark U.S. Dollar Index (DXY) has lost nearly 9% of its value against the world’s major foreign currencies.

In other words, on an international basis, the dollar now purchases 9% less than it did just four weeks ago!

My reasons for remaining so bearish on the dollar have not changed …

A. There’s simply no way the world will recover from the financial crisis without a weaker dollar.

It is the only way Washington will ever get out from under the $134 trillion and growing debt mountain it’s created. By defaulting on those debts, on the sly, via devaluing the dollar.

Fed Chief Ben Bernanke knows this. So no matter what he says in public about supporting a strong dollar, take it with a grain of salt. The truth is he wants the dollar to decline in value. Period.

B. We are the world’s biggest debtor, with the world’s worst budget deficit to boot. That may sound similar to the problem above, but we need to put it in context.

Reason: Way too many analysts compare today’s U.S. economy to the 1930s, claiming we’re on the precipice of a great recession, at best, and a great depression, at worst.

There’s no disputing those last two points. But understand this: In the 1930s ….

- The U.S. was a creditor nation.

- Washington had a balanced budget.

- The dollar was backed by gold.

Exactly the opposite core fiscal conditions that we have today. A great recession now? Absolutely. A great depression? Entirely possible, and I would even argue that we’re already in one.

But whatever your view is of our economy today, how the economy can slide into a severe deflationary environment is illogical when the fiscal conditions underpinning our economy today are the polar opposite of what they were in the early 1930s.

Think it through and the only valid, logical conclusion is that we’re headed into the opposite of what we experienced in the 30s: A hyperinflationary depression.

It’s like fire and ice. An economy can destroy itself through severe deflation (ice), or severe inflation (fire). Both extremes end up in the same place.

It’s a matter of how you get there. In the 30s, the economy took the deflationary path to ruin.

Now, in the early 21st century, because the core fiscal conditions — not to mention monetary policy — are exactly the opposite of the 1930s — the economy will take the hyperinflationary path to ruin.

t’s simply a matter of time, not if, but when.

C. Because the U.S. is the world’s largest-ever debtor … because Washington has the world’s largest budget deficit … because there’s no gold standard … and because Bernanke will stop at nothing to devalue the dollar and inflate away debts …

There is simply NO WAY the dollar

can be a safe haven in this crisis.

That’s why it irks me when I see so many analysts and investors running toward the dollar when there’s some bad economic news elsewhere in the world.

They’re simply jumping away from a fire — but plunging headlong into the frying pan.

In other words, the theory that the dollar is one of the world’s safest havens in this financial crisis is dead wrong for today’s economic environment. For all the reasons I cite above.

Sure, there will be short-term rallies in the greenback, like the one we just experienced. But each and every one of them remains destined to fail, and the dollar set for much lower levels in the months and years ahead, wiping out the savings of most investors.

Except those that understand how the process works, and who take defensive action.

One of the ways you can do that is by owning a good chunk of the only true international currency: Gold.

So, be sure your gold holdings are up to snuff.

Another way to make sure your portfolio has some money invested in other contra-dollar investments is with the PowerShares DB U.S. Dollar Bearish Fund (UDN) — an ETF designed to appreciate in value as the dollar falls in value in international markets.

And still another way is natural resource stocks, companies whose main products are the bread-and-butter commodities and resources the world needs on a daily basis; tangible assets denominated in dollars and whose value goes up as the dollar goes down.

There are oodles of natural resource stocks out there that are going gangbusters, with gains of as much as 48% in just the last four weeks.

For more details, your best bet is to stay abreast with my Real Wealth Report — a publication devoted to protecting your money, making sure it’s always real wealth, and headed for real profits.

Yet a fourth way is to invest in select companies in foreign markets that are performing well. Case in point: China, whose economy is still rocketing higher. Check out the latest stats from China …

- For the 11 months ended November 2009 (latest data), bank lending in China doubled to $1.35 trillion.

- For all of 2009, automobile sales in China soared 46.2% over 2008, to 13.6 million units, officially making China the world’s largest car market.

- Fourth-quarter GDP in China likely exceeded 11% growth. For all of 2009, GDP likely hit at least 8.9%.

- In December, China’s exports surged 17.7%, while …

- China’s December imports exploded 55.9% higher, proving that China’s 1.3 billion people haven’t skipped a beat when it comes to improving their lifestyles.

- Other Asian economies — India, and most southeast Asian countries — are also firing away on eight-cylinders, decoupling from their dependence on the U.S. economy.

- It’s also why over the last 10 months, many of my suggestions in this column are paying off for investors in spades …

- The iShares FTSE/Xinhua China 25 (FXI), up 55.5% since I alerted you to it in my March 16, 2009, column …

- The U.S. Global Investors China Region Fund (USCOX), up 47.0% since I suggested it in my April 6, 2009, column.

And two other recommendations in Asian economies and markets show open gains of as much as 57.6%.

Bottom line: Make sure you’re protecting the value of your dollars and are set to reap profits this year from the dollar’s ongoing demise — with gold, natural resources and tangible assets, and Asian stock market investments.

Best wishes,

Larry

In the mid-1980s, Mr. Edelson was one of the largest gold traders in the world, responsible for as much as $1.4 billion in daily gold trading volume on the Comex in New York, in today’s dollars. Mr. Edelson also managed several multi-million-dollar natural resource and commodity-based private investment funds.

Widely respected throughout the financial industry for his forecasts, Mr. Edelson has successfully called nearly all the major turning points in the world’s macro-economic trends, including …

The Stock Market Crash of 1987 and its subsequent rally to new highs by 1990.

The 21-year bear market in precious metals.

Major turning points in the currency markets, including the now multi-year-long decline in the dollar.

The peak of the stock market bubble in 2000.

The new bull market in natural resources that began in 2001.

One of the only analysts in the world to correctly identify in 2004 the start of the major bull markets in Asian economies and stocks.

This investment news is brought to you by Uncommon Wisdom. Uncommon Wisdom is a free daily investment newsletter from Weiss Research analysts offering the latest investing news and financial insights for the stock market, precious metals, natural resources, Asian and South American markets. From time to time, the authors of Uncommon Wisdom also cover other topics they feel can contribute to making you healthy, wealthy and wise. To view archives or subscribe, visit http://www.uncommonwisdomdaily.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair