Daily Updates

“Gold is silently, inexorably, psychologically – morphing to money while the reserve currency dollar slouches toward Bethlehem to be reborn”

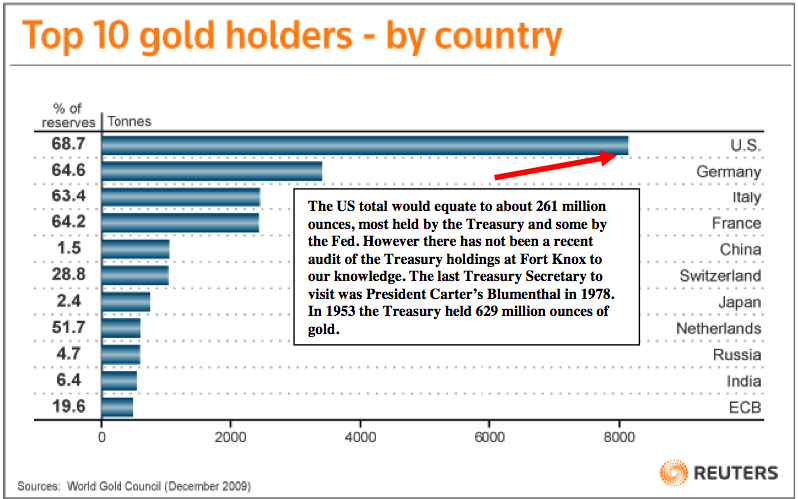

The IMF has decided to sell the remainder of its planned cache of 403.3 tonnes of gold. You will remember that last year (November 3rd) India, then Sri Lanka and finally Mauritius bought 221 tonnes of gold before it even hit the market. India’s November purchase of 8% of world annual production made her a top ten holder of gold at 6.4% of reserves. For India this amounted to a 56% increase in gold held by the Central bank of India to 558 tonnes (metric tons).

The International Monetary Fund announced this AM that it planned to sell the remaining 191.3 tonnes of gold into the open market a remnant of the original 403.3 tonne allocation.

The IMF will still control over 2,800 tonnes of gold. But the irony is that here is the world’s proxy for a central bank for the world’s poorer countries converting real money into fiat is value destroying. It must decline in value in the long run. This sale is to make loans to poor countries that will very likely never pay back, in full, these loans. Only Gordon Brown’s sale of Britain’s gold, which has been quietly swept underBritain’s rug, is more deleterious. The sale of the IMF gold to India netted ~$7.8 billion – a paltry sum when compared to the trillion dollar deficits and potential for hundred billion Euro and dollar sovereign debt defaults that now seem to be threatening globally with some regularity.

The IMF announced that it will sell these tonnes on the open market. This had the knee jerk effect of slamming precious metals prices, oil and the commodity currencies. It’s all relative of course so now the dollar defenders in Washington, as well as the talking heads on CNBC, can crow about a stronger dollar. Please do not be fooled by such short term speculation-fed manipulation. If gold declines this will be a marvelous buying opportunity.

There is likely to be even more pressure on gold however. Little noted is the recent Central Bank Gold Agreement in which the IMF has agreed to sell into the market up to 400 tonnes each year to a maximum of 2,000 tonnes in the next 5 years. These will be sold to central banks as well as on the open market.

Please realize one important fact. The IMF does not own a single ounce of this gold. All the IMF gold emanates from contributions from IMF member countries. In addition the IMF cannot sell its gold without the approval of the US – including the Congress and the Administration. So while the proceeds from such sales are dwarfed by the trillion $ liabilities that developed nations are now facing, a few billion dollars from selling IMF gold…..

…..read page 2-5 HERE

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Back on February 10(one week ago) these were the headlines:

“Bernanke Will Raise the Interest Rate When the Time Is Right”

Ben Bernanke outlined his plan for scaling back the Federal Reserve’s stimulus programs today, which included raising the interest rate back above near zero, which is where it has been since January 2008, in order to contain inflation. However, the Fed Chairman would not be pinned down on a date for such an occurrence.

“Although at present the U.S. economy continues to require the support of highly accommodative monetary policies, at some point the Federal Reserve will need to tighten financial conditions by raising short-term interest rates and reducing the quantity of bank reserves outstanding. We have spent considerable effort in developing the tools we will need to remove policy accommodation, and we are fully confident that at the appropriate time we will be able to do so effectively.”

Well, I guess old Ben was warning us that it coming sooner rather than later when he referred to an ‘appropriate time’.

Market are down sharply in overnight trading and I warned that we could see a pullback. Platinum subscribers have been in cash awaiting a retracement both in stock index ETFs and Gold related plays. Am I that smart? Not really. The market was overbought having rallied six, then seven and then eight days in a row (measured intra-day) and needed a rest. Negative Volume Reversals (r) fromed today would suggest a further correction possibly stretching into a mid-March low – though where I am sitting this morning that appears just too great a distance away.

I am buyer on a pullback, but let’s see just how much (or how little) damage is done first. The worst case is that post new lows between now and mid-March and the best case is that we only retrace part of the upleg that began off the February 5 low. In the S&P 500 a pullback to the 1080 makes a lot of sense to me.

Special offer from Mark Leibovit for Money Talks only: The intense analysis of Gold in the 10-12 page The VR Gold Letter is right now 75% off for the first month or $29.95 (regularly $125.00 a month). The weekly VR Gold Letter focuses on Gold and Gold shares.Go HERE and use the Money Talks promo code CBC12210

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

This brief initial comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail: dennis@thegartmanletter.com HERE to subscribe at his website.

“BEFORE YOU GET ALL BULLED UP: There is so much chatter these days concerning the rising Baltic Freight Index and how positive that is for the global economy and we just want to take a moment or two to say to everyone, “Hey, take a breath.

Slow down: Be calm; try not to get so excited.” The reason we bring this up is several fold, not the least of which is that the shares in the shipping industry are going absolutely nowhere, and the Baltic Freight Dry Index Itself has rally not risen all that far, no done so dramatically. – Dennis Gartman”

Short View: Reading the Baltic Dry leaves

The Baltic Dry Index, a measure of freight costs for bulk commodities such as iron ore, coal, cement, fertiliser and grains, has become the bear’s best friend. The index is down to its lowest level since October – a fall of 40 per cent in three months – and not far above the level of a year ago, giving ammunition to those investors who believe the global economy is not recovering. The bears, however, will be deeply disappointed.

For years, the index has been seen as a proxy for global economic activity, and at times it has tracked the ups and downs of global trade. Savvy investors followed it, although with some caution. Its recent weakness, however, fails to reflect global activity: the downturn is not the result of lack of demand but of the strong supply of new vessels.

Take capesizes, the largest oceanic vessels. Between 1980 and 2008, shipyards delivered on average one capesize every two or three weeks, slowly increasing the fleet, keeping supply and demand balanced and making the index a relatively useful instrument for investors.

But now shipyards are launching capesizes at an unprecedented rate on the back of massive orders placed when freight rates were high. Last year they built 112 vessels, almost one every three days. This year shipyards plan to deliver 335 capesizes, almost one every 26 hours.

True, cancellations because of lack of finance will reduce this year’s final number. But new supply is astonishingly high and it is overwhelming the otherwise robust demand for bulk commodities from China.

On the other hand, bullish investors should be cautious of any near-term turnround. Rather than a sign of stronger economic activity and commodities demand, it is likely to reflect cancelled orders, scrappage and port congestion.

For the time being, bears and bulls should leave the Baltic Dry where it belongs: to the shipping industry.

IS THE CORRECTION OVER?

There is room to have an open mind in both directions, though we believe that there is still more downside than upside risk. The problem for the bulls is that the market gains have occurred on lower volume, which was down 6% on the NYSE yesterday, and the major indices are still stuck below their 50-day moving averages (the only exception is the S&P 600).

But the bulls will note that the market now does have some technical strength (as outlined in today’s Investors Business Daily). The major averages have closed in the upper half of their daily ranges for six sessions in a row and often at or close to the highs of the day. The list of stocks hitting a new high has hit 200 versus 12 those hitting a new low. Sentiment has turned extremely negative considering that this correction was barely over an 8% down-move but indeed, before it occurred, the Investors Intelligence poll was at 52.2% bulls (18.9% bears) and at the recent lows it was at 35.6% bulls (and 27.8% for the bears). That is a contrarian positive, at least on a near-term basis. Moreover, there is a high correlation between the Euro and the S&P 500 and the short positions in the currency is at an all-time high, and as these shorts have to be covered, the dollar has softened a tad off its recent highs and this has corresponded with the rebound in the equity market.

Finally, we have 73% of companies beating their earnings estimate — this has dominated the press, and the fact that tech bellwethers like Hewlett-Packard managed to beat their estimates and raise guidance (as did Deere and Whole Foods) has also helped add some recent enthusiasm in the bullish camp. This is an exercise to see both points of view, keep an open mind; however, we have not waffling and maintain a cautious view over risk assets for 2010. This is still a technically-driven market — for confirmation of the sustainability of the rebound (recall that there were four other 5%+ declines during this bear market rally phase) we need to see:

If all the unfunded liabilities were consolidated onto one

1. Follow throughs (gains of at least 2% consecutively and on higher volume), and;

2. A move back above the 50-day moving averages for the major indices.

……read more topics HERE

……read the above topics HERE

Quotable

“Being aware of uncertainty and understanding the nature of probabilities does not equate with an ability to actually function effectively from a probabilistic perspective. Thinking in probabilities can be difficult to master, because our minds don’t naturally process information in this manner. Quite the contrary, our minds cause us to perceive what we know, and what we know is part of our past, whereas, in the market, every moment is new and unique, even though there may be similarities to something that occurred in the past.

“This means that unless we train our minds to perceive the uniqueness of each moment,

that uniqueness will automatically be filtered out of our perception.”

Mark Douglas, Trading in the Zone

FX Trading – Euro bounce? That is a big maybe! – HERE

FX Trading – Oh, that nasty British Pound – HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair