Daily Updates

The shrewd Jim Rogers was once asked why anyone should buy gold when there was seemingly no inflation. He cited the current account and Treasury deficits and said, “Just do the math.”

As a general—and very useful—rule, the days the dollar is strong are days commodities and commodity stocks are weak. History shows that the greatest commodity bull market—the 1970s—was a time of severe dollar weakness, and the Triple Waterfall Crash of commodities came during a long, strong dollar bull market.

So, we are asked, can we have a commodity bull market coexisting with a dollar bull market?

In a word: Yes.

We have come to believe that this Odd Couple can coexist if investors conclude that bonds are no haven, and economic growth remains much stronger in the key Asian economies than in the US or Europe.

Why?

Because the 1970s commodity boom was an inflation-hedge boom. US inflation surged from 4% to 14% and there were three recessions within a decade. That commodities other than gold performed well was because investors learned that buying “out month” commodity futures was a hedge against inflation. Result: base metals piled up in storage because of inflation fears, while demand was erratic because of recessions.

We try to resist “New Era” thinking, but current conditions are collectively unique:

1. OECD government fiscal deficits totaling more than $4 trillion.

2. Government bailouts totaling more than $1 trillion.

3. Debt/GDP ratios at unheard-of levels—both government debt/GDP and total debt/GDP.

4. Global economic leadership now coming from China, India, Korea and Taiwan, not from the US and Europe.

5. Housing bear markets across much of the OECD with government housing price supports at unprecedented and unsustainable levels.

6. US State and local debt ratios at horrendous levels even before realistic costing of liabilities under employee pension and medical plans. We live in Illinois, which ranks just behind California for the scale of its unfunded employee pensions. A Stanford team recently costed out the unfunded portion of California’s state pensions at $500 billion—which is roughly seven times the total amount of state general obligation bonds outstanding. Illinois and California would need years of GDP growth at China’s rate to make their existing debts manageable—and many other states are in similar crises. One example of why the Canadian dollar is so strong relative to the greenback:

Everyone has always known that Social Security was headed for trouble, but we were told its cash flow wouldn’t turn negative until 2019; then 2016. It goes negative this year and that means the “fund” is evaporating quite rapidly. (Remember when the Democrats savaged Bush’s plans for Social Security savings accounts by telling frightened voters that Bush would be taking their money from its safe piggy bank where it was being kept for them? Great politics.)

The Social Security Trust Fund, which is a mere bookkeeping entry, “invests” in Treasurys at the approximate duration of the national debt. We appeared before the US Senate Finance Committee in 1988 to testify about what was wrong with the Fund. We criticized its investing strategy, pointing out that any private plan with long-term liabilities that invested in what was then a 7-year duration would be shut down. We argued the Fund should be getting the benefit of the high interest rates available on long Treasurys. Senator Moynihan called our testimony “powerful,’ but told me he couldn’t rally any votes for it because the Treasury was saving money by paying such low yields into the fund, and if Social Security invested in long bonds it would increase the reported fiscal deficit. Result: all those years of double-digit and high-yielding Treasurys came and went and Social Security only briefly prospered.

Compare that experience to the Canada Pension Plan, which for its early years (until the 1990s) invested in 20-year provincial government bonds whose blended real yields were high, then switched, as the bonds mature, to investing in market instruments managed by skilled professionals at the Canada Pension Plan Investment Board. The CPP isn’t fully-funded, but its market rate returns mean that its assets will keep growing for decades. Chile and Norway may be the only nations with better-financed public pension systems.

We conclude that the US will continue to look somewhat attractive compared to Europe, and so there will continue to be demand for Treasurys relative to bonds issued by European governments other than the leading countries.

The commodity bull market in this decade will be driven by (1) industrial demand for raw materials; (2) sustained demand for petroleum; (3) continued protein upgrades in diets in emerging and emergent economies, and (4) greater reliance on precious metals as stores of value—not necessarily as hedges against actual inflation. Inflation could in fact come with a rush if the global economy turns strong, government deficits stay high, and real yields on government bonds turn sharply negative. At the moment, measured inflation remains subdued because of heavy unemployment and large percentages of unused capacity across the OECD.

Gold

What is the difference between a store of value and an inflation hedge? Answer: a store of value at least maintains its market value under widely varying economic conditions and widely-varying or steadily-rising inflation; an inflation hedge is an asset boughtand held to produce big profits when inflation is high and rising—and investors think it’s going to rise even faster.

Gold ran from $38 to $850 when inflation ran from 5% to as high as 14%, but annual inflation during that period averaged in the high single digits. Once gold’s price was running far faster than inflation, it ceased to be a true store of value and became a speculative hedge—ultimately against inflation that Paul Volcker was about to terminate.

Published by:

Coxe Advisors LLP.

190 South LaSalle Street, 4th Floor

Chicago, Illinois USA 60603

Distributed by BMO Capital Markets

Michael Berry: Uranium—Part of the Energy Solution

Tim McLaughlin and Karen Roche of The Energy Report 04/15/2010

President Obama has called for the development of more nuclear reactors in the coming decades. Discovery Investing pioneer Dr. Michael Berry says for that plan to work, uranium has to be part of the solution. In this exclusive interview with The Energy Report, Michael talks about the need for more uranium mining in the United States. He also explains why right now an investment in energy metals is a safer bet than investing in industrial metals.

The Energy Report: Last December, you thought inflation was still 18 to 24 months in the future. Is that still your thinking?

Michael Berry: It depends who you talk to. We don’t have any visible inflation in this economy right now. If anything, there’s still de-leveraging. There’s excess capacity out there. We’re not moving down the unemployment scale very much. We still have 9.7% unemployment, even after a lot of government intervention in the labor markets. Right now inflation is hard for me to see. We’re still that magical 18 to 24 months away, or maybe even more, from inflation.

Certainly if interest rates move up we could have that, but there’s still a lot of excess capacity. There’s a lot of debt. The Obama administration and the Bush administration really didn’t deal very well with the excess debt. They just kind of rolled it over and pushed it out. Europe seems to be following suit in Greece today.

I’m an optimist. If you’re an optimist in this market, you believe inflation is coming. If you’re a pessimist in this market, you believe that we’re going to be in a painful deflation for some time to come. I’m an optimist, so I think within the next couple of years, we’ll get some inflation.

TER: With inflation somewhere on the horizon and a continued period of recession in the meantime, part of the strategy is to be defensive. In a world where we have inflation, but we also have pressure in the U.S. strategic metals, would you consider uranium a safe investment area?

MB: Today, any energy metal is a safer investment than an industrial metal. We’re going to need uranium because the world, if not the U.S., is going nuclear. We’re probably going to need thorium eventually. In some sense, uranium is very cheap now and we have a lot of it in the U.S. and Canada. Resource nationalism is spreading around the world.

If you look at the rare earths (REE), I think the same thing applies. We have to have rare earth elements because they’re integral in many strategic applications and we don’t have much REE resource in the U.S. We don’t have a lot in Canada. Quest Uranium Corp. (TSX.V:QUC) is one rare earth company in Quebec and Avalon Rare Metals Inc. (TSX:AVL;OTCQX:AVARF) is another interesting one, with its Thor Lake deposit. Some of these energy and strategic resources are going to be more resistant to downturns. Copper is trading for $3.50 a pound and it seems to want to stay there. I’m a little nervous about copper. If we do have a major downturn, you could see the industrial metals, as opposed to the strategic or energy metals turn down.

I’d like to make one other point. Up until 2007, we had this theory of decoupling as it relates to China. Then everybody pooh-poohed it and said, oh no, China isn’t decoupling. China may well be a bubble, too. There may be a significant downturn in China. However, I think decoupling is going to come from the emerging markets. The emerging markets are where growth will emanate because we are witnessing a quality of life increase there that you aren’t going to have here and in Europe. Probably not in Canada either. Decoupling, in this case, will be the generator of demand for these metals, which is going to be stimulated from sources other than the U.S. and the OECD countries.

TER: But going with that decoupling theory, if we’re seeing expansion, then wouldn’t the industrial metals also continue up?

MB: Yes. Except that in the short run, we may see excess capacity in places like China. I don’t think you’re going to see it in India. You may see a bubble that bursts in China. There is excess capacity. On the other hand, China is a state-run economy and so they can do things that democracies cannot do. My long-term view is that there will be decoupling and that the emerging countries of the world, not just China, but India, Brazil, Argentina and others will eventually lead us out of this global recession. That is the significance of this sort of “decoupling.” Emerging countries will take the lead and they’ll outgrow us consistently over time because people in those areas need infrastructure. They want a better lifestyle and all the things that we’ve become accustomed to in the West since the end of the Second World War.

TER: With what you just said in mind, are there any companies that you’re excited about in this sector?

MB: There are a couple of companies that I think probably bear near-term attention. One is called Salares Lithium Inc. (TSX.V:LIT). I know many believe that lithium is the hottest, the latest and the greatest resource fad. There’s a lot of attention on lithium-ion batteries. Salares has perhaps the best set of brine lakes in Chile. They have seven of them in Chile; five are 100% owned. The stock is just so strong. It keeps moving. They have run geophysics over the two largest salars and can see brine that goes so deep they cannot see the bottom. They will be drilling for grade very soon. Oil people tend to understand lithium brines. There’s a strong institutional backing of the stock. Todd Hilditch is the CEO and he’s a very fine young executive who’s making his mark in the mining industry.

Another company that I really like is Goldbrook Ventures (TSX.V:GBK). In far northern Quebec, nickel is key to the new clean energy economy. There are only a handful of nickel sulphides trends worldwide. Goldbrook owns about 47% of the entire Raglan trend, which is a developing, world-class sulphide-nickel-copper-cobalt PGE deposit. Xstrata and Anglo are other big participants in the Raglan. The Chinese nickel company Jilin Jien came in and is financing Goldbrook to production on their resources there at a 75/25 carry to production. Jilin Jien is the second largest nickel producer in China. Jilin also bought out Canadian Royalties and Goldbrook has a 25% equity interest in that company, also on the Raglan. That resource of 21 million tons, 43-101, and is worth at least $2 to $3 a share to Goldbrook, at low cycle metal prices, in my opinion.

Goldbrook Ventures’ shares are now selling for $.30 a share. I really like the company. It may be unknown to most people, but this Raglan nickel belt is going to become another Thompson belt. It’s going to be another Sudbury. For any sulphide nickel aficionados this belt and GBK, in particular, is one to watch.

On the rare earth side is Avalon, which owns Thor Lake in the NWT. Thor Lake is a huge rare earth deposit of 69 million tons. Avalon is moving that along with a planned pre-feasibility study in 2010. The key is that it contains both light and heavy rare earths. It’s interesting that most of these rare earth resources are either in Canada, China or Russia. Unfortunately, for the most part they’re not in the U.S.

Stans Energy Corp. (TSX.V:RUU) has a high-grade deposit in the country of Kyrgyzstan. I’m violating my principles because I always said I’m going to stay in Canada, the U.S. and Mexico. However, I’m starting to range to places like Colombia, Guyana and Kyrgyzstan because that’s where some of these great deposits are located. The current situation in that country not withstanding, these types of assets are “company-makers.”

TER: There are lots of different types of rare earths. There are the heavy and the light. How do you compare Stans Energy to Avalon?

MB: The heavy rare earth elements, compared to the light REEs, are rare indeed. Some of the “heavies” are Europium, Terbium, Dysprosium and Yttrium, used in magnets, superconductors, ceramic and lasers. The companies probably compare favorably, actually. The heavy rare earth elements are sought after and sell for hundreds of dollars per kilogram. Avalon’s Thor Lake is a great property. This deposit has all kinds of metals in it. It has beryllium. It has thorium. It has both light and heavy rare earths and it has a lot of them. They have a great deposit and now they’re going to have to figure out how they’re going to process it.

At the same time, the Stans Energy deposit in Kyrgyzstan has a Soviet era production plant called Kutessay II in place there.

This plant produced 80% of the Soviet Union’s REEs till 1991 and it is about 50% heavy rare earths. They have lots of experience with metallurgy here as well and excellent infrastructure.

Kutessay is not running now. The Soviets open pit mined this during the Soviet Union’s heyday. They have some dysprosium and some of the heavies as well. They have a good, solid base of heavy rare earth elements there also.

I’d have to say I’d rather be in Canada, but I also like the Stans Energy deposit and plant very much, too, in Kyrgyzstan. Both projects will be developed. The other thing that is interesting is that it’s pretty much Canadians that make this mining game go. These companies are Canadian companies headquartered either in Vancouver or Toronto. Avalon and Stans Energy are both Toronto companies. The world is getting smaller for us all, and we must begin to look far afield. Canadians seem to be well received.

TER: When we were chatting before the interview, you mentioned that the rare earths are worrying Washington. Can you explain that?

MB: I do quite a bit of work with The Western Caucus, which is a group of congressmen from the Western states, mostly Republicans. The U.S. defense strategic stockpile of metals has been basically sold down. This country is more or less dependent on either what we produce internally or what we can import.

For example, we import 31% of the copper we need in this country. With rare earth metals, we have very few mines and they’re mostly light rare earth elements. China controls about 97% of that market. These are very important metals for strategic applications. Things like weapons, magnets for motors, superconductors and so on.

This issue of declining strategic resources has come to the attention of congressmen like Bishop from Utah, Forbes from Virginia and others. Anytime China has an advantage, Washington becomes concerned. You can say the same thing about molybdenum and tungsten—other metals that China basically has a grip on.

Washington’s holding hearings on these issues. It’s had a lot of hearings on them. I’m not sure exactly what they’re going to do, but most of the opportunity right now in Washington is to teach congressmen about our metal dependencies, our mining inefficiencies and domestic mining development in this country. I spend a lot of time doing that. Right now you can get everybody’s attention in Washington if you talk rare earth elements because they know we don’t really have much of a resource in that area.

TER: As far as uranium goes, are there any companies in that sector that you’re looking at?

MB: There is an American company called Uranium Energy Corp. (NYSE:UEC). UEC will be doing uranium mining in Texas. The state of Texas is a little more mining friendly. It’ll be an in situ mining operation.

The uranium issue boils down to the following. Our president has said he wants to build up to 100 more reactors over the next several decades. We import 90% of our uranium from countries like Canada and Russia. Yet, as a country, we have the fourth largest domestic resource of uranium in the world. This should be an American industry. Those are jobs. There are a lot issues that are in play here in terms of the uranium industry itself.

However, the Obama administration is going to be attempting, and will probably be successful, removing a lot of lands from mining opportunities. One of the areas they’ll likely try to remove is the Arizona Strip north of the Grand Canyon. The Grand Canyon is rich with uranium and uranium pipes. These are cylindrical pipes that are high-grade, about 0.65% U3O8. Between 1980 and 1990, six mines on the Arizona Strip produced 19 million pounds with no pollution and no deaths. One pound of uranium makes 10 small fuel pellets. Each fuel pellet replaces the energy content of 1 ton of coal. The Obama Interior Department placed 1 million acres, 2765 million pounds of uranium off-limits for exploration in July 2009.

TER: How difficult is it to get the uranium out of the ground in areas such as the Grand Canyon?

MB: It’s not very difficult. These pipes are north of the canyon and above the water table. They’re very small, very compact. The surface footprint is 20 to 25 acres. Usually a couple of million pounds each, plus or minus and they can be mined in two years and reclaimed quickly. They were mined and reclaimed in the 1980s very successfully with no known environmental damage. This is 10 to 15 miles north of the Grand Canyon. So you can’t see them from the south rim. There are hundreds and hundreds of these uranium pipes out there. Denison Mines Corp. (TSX:DML; NYSE.A:DNN) is mining a pipe called Arizona 1 and it has, I think, two other pipes. Quaterra has made three uranium discoveries up there using a new more powerful and less invasive geophysical technique.

The mining on these pipes is very straightforward. It’s underground, so there’s no open pit. There’s no scar on the landscape. If you raft down the Grand Canyon, you can actually see pipes in the walls of the canyon where they’ve been naturally eroded down. People have said, well, mining companies are going to contaminate the groundwater. In fact we’ve never seen any uranium contamination or radioactivity in the water of the Colorado River at all. It’s a pretty big issue and it means jobs. Both the governor of Arizona and the governor of Utah want see these natural resources developed in an environmentally responsible way. There’s no reason why we can’t do that.

If we’re going to have clean energy, if we’re going to have move forward and move away from carbon-based energy sources, nuclear energy has to be part of our solution. If nuclear energy has to be part of our solution, at least for the next several decades, domestic uranium has to be part of the solution. We have it. We have more uranium than most other countries domestically. Why would we again run up a deficit, pay somebody to become dependent on uranium as we’ve done with oil? We don’t need to.

TER: Thank you for your time.

Dr. Michael Berry has lived in the U.S. for 36 years but raised in Canada. A math major at the University of Waterloo in Ontario, he earned an MBA at the University of Connecticut and obtained a PhD specializing in quantitative analysis and investment finance from Arizona State University. He has specialized in the study of behavioral strategies for investing and has been published in a number of academic and practitioner journals. His definitive work on earnings surprise, with David Dreman, was published in the Financial Analysts Journal. While he was a professor of investments at the Colgate Darden Graduate School of Business Administration at the University of Virginia (1982-1990), Michael spent considerable time with some world-renowned geologists on the Carlin Trend. While a professor, he published a case book, Managing Investments: A Case Approach.

Michael also held the Wheat First Endowed Chair at James Madison University in Virginia, and managed small-and mid-cap value portfolios for Milwaukee-based Heartland Advisors and Chicago-based Kemper Scudder. His Morning Notes publication, distributed worldwide, provides analyses of emerging geopolitical, technological and economic trends, as well as identifying opportunities for the Discovery Investing strategy he developed. Read Dr. Berry’s testimony presented to a subcommittee of the Natural Resource Committee, United States House of Representatives (4/8/10).

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

Resource Stock Rally:

Will Treasuries Spoil the Party?

From the April 2010 HRA Journal

We have to give the March tug of war to the bulls based on market levels and economic news. Those of a more ursine persuasion can still rightly point out that the rally really is getting very long in the tooth.

As this is being written the resource exploration sector seems to be in for its traditional spring rally. We are being cautious about that. The TSX Venture Index, our exploration stock proxy, has been slower to regain the January high than senior indices. It just barely reached that mark on April 4. Three months peak to peak with a 10%+ drop in between at least qualifies as a respectable correction. That breather may have set the market up for another up-leg through Q2, but some further gain is required to confirm the correction is over.

Also meaningful for the exploration sector is a relatively mild and snow free winter in most of Canada. Several areas that will be very active this summer can get an earlier start this year than they normally would. That means news will start arriving sooner and will continue longer. That may help to strengthen or extend the spring bounce exploration stocks tend to get.

Senior markets, by contrast, have had three periods of consolidation in the past 12 months, though none of these were large enough to be a “correction”. That is as much a concern as anything. Even the more bearish might be willing to dip their toe in on the long side if there was a correction large enough to feel like a real shake out.

It has been improving economic stats and continued low interest rates that have kept markets buoyant. We’re not sure that combination can last much longer. Will falling bonds take the equity markets down with them?

That will depend on why they are falling. The chart below displays yields on the 10 year US Treasury for the past two years. Note that the latest print is just barely below 4%. Looking back you’ll also see that that last two times the 10 year yield reached this level a correction, or at least pullback, began in the larger markets.

The current bond move has not stalled out stock markets because there has been good news to go with it. March was finally the first month with a significantly positive jobs number in the US. While the figure was slightly below consensus the report included upward revisions to the last three months. That took the total “gain” to about 225,000 jobs. Equally important was news that hiring for the US Census was only 50,000 of those jobs, not the 100,000 that had been assumed.

Yes, we can do the math. At that rate, it would take something like seven years (!) to regain all the jobs lost to the recession. No pretence from us that it was a “good” number. It was merely a “better one”. As important was the news that consumer confidence and the ISM numbers, particularly for the larger service sector, were much better than expected. Again, not fabulous numbers but better than we have seen for over two years.

These figures account for some of the strengthening in bond yields. As long as yields continue to trend upwards due to good news on the economic front the markets will be able to shrug them off.

Cause for concern is the extent to which rates are rising due to the oversupply of debt. This may also have been part of the problem last month. Bond traders have been getting worried about declining bid-to-cover ratios for several weeks. There is also evidence that foreign central banks, particularly Asian ones, have been backing away from the market.

It’s next to impossible to confirm this directly. The US Treasury has redefined the different classifications of bidder in the bond market. Only the terminally naïve believe this is anything other than completely intentional. We’ll have to wait for flow of funds statistics to divine things.

We doubt it’s a coincidence that light bidding in bonds coincided with US politicians and a couple of Nobel economists taking Beijing to task over the Dollar/Yuan exchange rate. There has been talk of forcing the issue by imposing across the board tariffs on Chinese imports.

This would be a move we could only view as profoundly stupid. There is no good reason to think that would do anything but raise US prices. Consumers would either look for cheaper goods from elsewhere (elsewhere not including the US itself), or simply have to pay higher prices.

We’re not saying we think China is right to hold down its currency. It’s time for China to let the Yuan rise for everyone’s sake; Chinese consumers as well as US exporters. However, trying to carry a big stick to threaten the people you are simultaneously borrowing money from is simply ridiculous. A number of commentators have pulled out the “when you owe the bank a billion they are in trouble” line. Try taking the bids from China and a couple of other creditor nations out of the Treasury market and see what happens to yields. Yes, Beijing would lose money on its Treasuries, but the US would be driven into a new recession as rates exploded. Creditors would win that round. They usually do.

It now looks like Washington is holding back a report that was expected to brand China a currency manipulator. This was a relief and we hope that Beijing will let the Yuan start rising again to ensure the report just gets buried. On balance, the rise in yields has been driven by good news, but this market has to be watched. If there is a major correction in Q2 it will probably start in the bond market.

Anecdotal evidence points to improved demand in the US for a few months. That plus good export earnings should lead to growing profit numbers for the Fortune 500, which will support share prices. Rate increases in areas of better growth like Australia, India and Canada will help temper Dollar gains. This should be enough for the markets to keep levitating for a couple of months more.

Good economic stats leave room for some further gains in base metals. We continue to be surprised by the disconnect between inventories and prices. Some of this is speculative and some of it is arbitrage trades, but it’s happening across the board. Hoarding copper we could see, but hording iron ore and coal seems rather less probable.

It may simply be that the current relationship between metal prices and inventories is the “new normal”. We are not willing to assume that is the case just yet, nor does it seem is the market. Base metal miners have not seen much share price increase even though more should be putting up very strong earnings numbers.

As we’ve noted before a quarter or two of better earnings will usually drive some money down the food chain. We are watching closely for that and will add base metals explorers if it happens. For now we’ll continue to focus on precious metals. They have their ups and downs but have also held their own in the face of the uncertainty that will be with us for some time yet.

To view Eric Coffin’s latest video interview on Industry Watch with Al Korelin, please go to: http://www.youtube.com/watch?v=DXQl4DYK_Tg [April 12, 2010]

Gain access to potential gains of hundreds or even thousands of percent! HRA initiated coverage on 8 new companies in 2009. So far, the average gain on those companies is over 250%! For more information about HRA Advisories, please visit: www.hraadvisories.com

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-base expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2009 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071 Toll Free 1-877-528-3958

hra@publishers-mgmt.com http://www.hraadvisory.com

U.S. Stock Market – The final pieces to the puzzle are coming together as planned. The close above DJIA 11,000 has indeed empowered the “Don’t Worry, Be Happy” crowd. The media has been full of chest-beating bulls and the public is biting the apple again. This is just a sample of the emails I’ve received in the last 48hrs:

- “…I think you do a disservice to your followers by not recognizing the bull market that is unfolding before your eyes, tempered by your cautionary warnings. They will miss out on the opportunities that have opened since the Dow bottom at 6700. Not just owning stocks but biz opportunities, that someday be described as phenomenal, incredible and like wording…”

I might mention that this person failed to note my buy signal just one day from the bottom in March, 2009 and my consistent call for DJIA 11,000 and an economic recovery through June-July of 2010. But his extremely half-full cup view of the stock market and economy has fast become the way of the land. I fully suspect and hope it shall continue for awhile longer so I can say without reservation what the leader of the “A-Team” was famous for.

U.S. Dollar – I’ve suggested for months that the U.S. Dollar was merely in a typical and necessary “countertrend” rally within a secular bear market. Like the U.S. stock market, it too is pretty much playing out as anticipated.

I have spoken of late how momentum was failing. As you can see, we broke below an uptrend line and it’s natural for the market to rally back to that line. I continue to use 83-84 as the maximum upside potential in this bear market rally and think it’s still too early to look for a renewed decline. We could see a multi-month rather narrow trading range.

Gold – What can I say that I haven’t said already? I continue to find it amusing how continuously-wrong gold forecasters are still taken into consideration by some. The latest being the GFMS so-called forecast. Between them and the “Senior Analyst”, I can’t think of anyone who has been more consistently wrong. We remain in the “mother” of all gold secular bull markets and the number of forecasters who have called for its demise only to be trampled over just grows and grows.

U.S. Bonds – We get as close as one can get to breaking the back of the multi-decade bond bull market only to see enough of a rally to hold off the inevitable. To me, it’s a question of when, not if, a new multi-year bear market in bonds takes hold.

Northern Dynasty Minerals CEO appeared on BNN and also was picked by “Smartrend”.

Oromin Explorations had very good drill results.

As Israel continues to get painted into a corner, the world as a whole basically ignores the reality of the Iranian threat. The fuse on this geopolitical nightmare continues to shrink as activities not making the front page of news reports continue to unfold as I speak.

America has become a two-class society. The silent majority is becoming vocal and then some while President Obama continues to avoid the media.

And finally, video that wasn’t shown during the Masters broadcast.

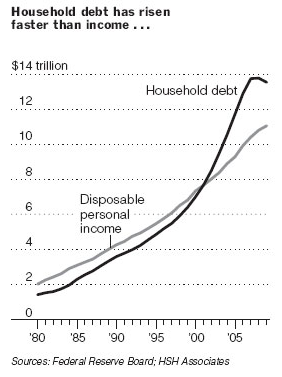

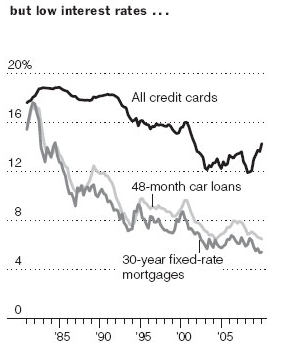

Even as prospects for the American economy brighten, consumers are about to face a new financial burden: a sustained period of rising interest rates.

Multimedia

Household Debt vs. Interest Rates

That, economists say, is the inevitable outcome of the nation’s ballooning debt and the renewed prospect of inflation as the economy recovers from the depths of the recent recession.

The shift is sure to come as a shock to consumers whose spending habits were shaped by a historic 30-year decline in the cost of borrowing.

……read more HERE

Nelson D. Schwartz is the European economics correspondent of The New York Times, based in Paris, reporting on companies and economic trends on the Continent. He joined The Times in June 2007 and worked as a feature writer for Sunday Business before heading to Europe in September 2008. A 1995 graduate of the University of Chicago, where he studied Russian and American history, Mr. Schwartz grew up in Scarsdale, N.Y., and lived on the Upper West Side in Manhattan.

From 1997 to 2007, Mr. Schwartz was a senior writer for Fortune, where he reported from New York and more than a dozen foreign countries, including Russia, Britain, Iraq, Libya, Kuwait, Argentina and Brazil. He received an honorable mention from the Overseas Press Club in 2006 for his interview with Hugo Chávez and his portrait of Venezuela’s oil industry in Fortune.

He began his career in the Washington bureau of The Baltimore Sun, and also worked for Smart Money magazine in New York covering personal finance. A keen bird watcher, he has made time for bird-watching during reporting trips in Iraq and Kuwait, as well as South America.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair