Daily Updates

“Sparked by a growing recognition of sovereign risk originating from the eurozone, investors flocked to the relative safety of US Treasuries last week, driving yields on the 30 Year Bond to 4.28% and the 10 Year Treasury to 3.43% at Friday’s close. We expect this move out of risk assets and into government bonds to accelerate in the period ahead”

…..continue reading Ten Reasons to Buy Bonds HERE

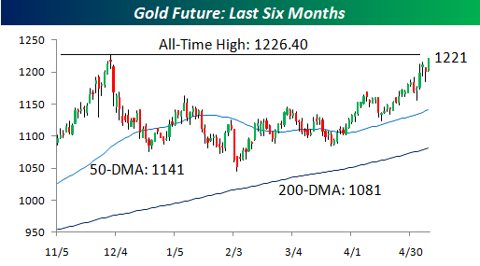

A Trillion Reasons For Gold’s Rally to New Highs

With the Euro resuming its decline following Monday’s announcement of a trillion dollar rescue fund, it should come as no surprise that gold is right back near its record highs from last year. As countries push the printing presses into overdrive, investors are running for gold.

Hourly Chart posted by Money Talks @ 8:03 PST

Think B.I.G., by Bespoke Investment Group, provides some of the most original content and intuitive thinking on the Street.

CANADIAN HOUSING: ARE BUILDERS BUILDING INVENTORY?

Another piece of strong housing data out of Canada yesterday with April housing starts edging up 1.3% MoM, to 201.7k annualized units (though slightly missing analysts’ expectations of an increase to 205k). The details were mixed with single-family starts (a good baramoter for underlying demand) dropping nearly 13% while multi-starts (ie, condos) jumped 27% on the month. If we take a step back from the monthly volatility, what is interesting to note is that household formation rates are at about 175K annualized and housing starts have been running at-or-above that level for the past seven months, suggesting that inventories of new homes are building. Using a different approach, housing starts (ie, supply) were up at whopping 80% YoY in April and existing home sales (ie, demand) are running at less than half that rate on a YoY basis. Using this approach, we estimate that supply as been outrunning demand for about 2-3 months, another indication that inventories may be building. In fact, the latest data release for existing home sales showed, on a seasonally adjusted basis, months’ supply in March were higher than in the previous four months.

We are likely to see more inventories build, especially as the frenetic demandseen in the first half of the year dries up in the second half due to higher mortgage rates, a more restrictive lending environment and the impending HST — all of which will ultimately pressure home prices downward.

From Breakfast with Dave – Market Musings and Data Deciphering – register for FREE letter’s HERE

A MUST read: read my friend, John Mauldin’s latest article, “The Center Cannot Hold,” John tells us why we could have one bang-up depression coming up. Don’t miss John’s latest, it’s a MUST! The market is telling us what. John tells us WHY” HERE – Richard Russell

The following is an excerpt from a missive that we received from Jim Sinclair this morning, who is the host of a web site called Jim Sinclair’s MineSet. He sums up the situation much better than we can so its well worth the time spent on reading what he has to say. The above link will take to his site and his updates via email are free so you have nothing to lose by signing up for them.

Here we go:

A nuclear solution to Europe’s debt problems is simply another way of saying “Quantitative Easing to Infinity.”

All national debt will be bailed out. All states of the USA will be bailed out.

Paper currencies are headed to dust.

Regardless of the first knee jerk market reaction, gold is going to $1650 and beyond due to nuclear suggestions of adding more debt to entities failing because of debt. This is the EU Helicopter Drop coming up.

Credit default swaps are herein called the “Wolfpack.” About that they are totally correct.

Now that they have challenged the “Wolfpack,” whatever additional funds might be required will have to be provided or the “Wolfpack” will slaughter the EU.

EU Preps Euro Fund to Fight ‘Wolfpack,’ Debt Crisis

….read more HERE

Todd Market Forecast for Monday May 10, 2010

Available Mon- Friday after 6:00 P.M. Eastern, 3:00 Pacific.

DOW + 405 on 2750 net advances

NASDAQ COMP + 109 on 2050 net advances

SHORT TERM TREND Bearish

INTERMEDIATE TERM TREND Bullish

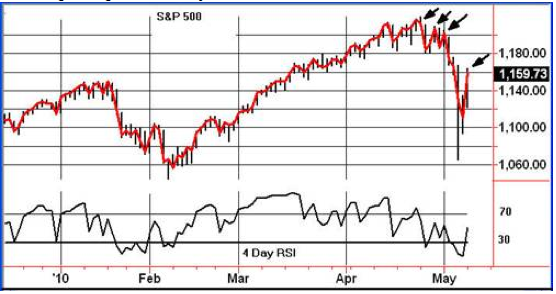

Today, the S&P 500 futures opened up over 4% for only the seventh time in history. The other times were 10/20/87, 10/21/87, 1027/87, 9/19/08, 10/13/08 and 10/28/08. In all cases, the gains were given back, most within a few days. One took almost two months.

Let’s take the three most recent. The events of Sept. 19 and October 13 were triggered by the announcement of big rescue packages for financial institutions. There was no special news for the big open on October 28.

Today, the news was a big rescue package to get European banks off the hook. Sound familiar?

When four day RSI becomes oversold and then we get a sharp rebound we look at the possibility of moving back to a short term buy signal if we have been bearish. But there are two problems. First, we still have a pattern of declining tops on the daily charts and volume was pretty anemic. Meaningful moves tend to be on impressive volume. Incidentally, the moves from September and October of 2008 weren’t on great volume either.

We can see that the declining tops are still in place in the chart below so we’ll see how things go over the next couple of days before considering a change in short term posture.

The dollar was down, but well off the lows. It seems to have aided silver, copper and crude oil to a gain. Gold was down because of the sharp gains of the last couple of days. Bonds managed a sharp down session.

.

BOTTOM LINE:

Our intermediate term systems are on a buy signal.

We sold the E-mini bought on Friday at 1121.75 for 1156.25 which was a gain of 34.50. We sold the SSO bought Friday for 38.74 at 41.09 which was a gain of 2.35.

Since we were up over 100 Dow points today with 15 minutes to go, we sold the E-mini bought this morning at 1154.00 for 1156.50 and a gain of 2.50. We sold the SSO bought this a.m at 40.87 for 41.09 and a gain of .22.

Stay in cash on Tuesday.

System 7 traders are in cash. Stay there for now.

Stephen Todd – A Short Biography www.toddmarketforecast.com

Since 1984, the editor and publisher of the Todd Market Forecast, a monthly newsletter with emphasis on the stock market, but also with sections about gold, oil, currencies and bonds.

Steve spent a number of years as an engineer in a steel mill before becoming a stock broker with a number of Firms, including E.F. Hutton, Bache and Paine Webber.

He has published articles on the economy and the stock market in the following publications: Barron’s, Stock Market Magazine, Futures Magazine, The National Educator and others.

His stock market commentary is heard on CNBC, Bloomberg, Associated Press Radio, Business Radio Network, CKNW in Vancouver, British Columbia, KFWB, Los Angeles and ROBTV in Toronto, Ontario.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair