Daily Updates

We are drifting. We take comfort in bits of good news, but we are in dangerous waters; the Great Recession is being starkly revealed as a global crisis with the US, the traditional engine of recovery, sputtering on every cylinder.

The US government responded with dramatic financial support by transferring money to the household sector. But outside of these transfers the personal income of Americans is still declining; the residential market remains stagnant at best; consumer growth is nominal. The only real energy in the economy has come from the cessation of inventory liquidation, which is now the main factor in rising industrial output and any modest improvement in the economy.

The mood of US households is despondent. In May only 11.3 per cent believed they would see their income rise in the following six months, while 16.6 per cent thought they would see it decline. This is the first time in over four decades that more people believe they will be worse off than better. Any massive fiscal and monetary stimulus that might reverse the trend is likely to be politically unsustainable given the growing concern over the exploding national deficit.

Wherever you look the scene is bleak. Leading economic indicators fell in April – unusual at such an early stage in the up-cycle. Jobless claims were up by 25,000 to 471,000. And up again above expectations in the first three weeks of May – raising the four-week moving average to a level consistent with 100,000, or more, net job losses. For the past several months, claims have been nowhere near the levels of 400,000 and less that in the past were consistent with sustained job creation. We are not enjoying the normal cycle of economic improvement. If we were, employment would already have reached a new high and made up all of the jobs lost, as it did during the previous postwar recessions. This time we remain short of the old peak of employment, by an astounding 8.4m jobs. One in six Americans is either unemployed or underemployed. This is not a normal cycle when compared with a typical recession, which sees no more than 2m to 3m jobs lost.

….read more HERE

“For Many, Recovery Means Lower Expectations” (Associated Press)

PROSPER, Texas — Advised by a Walgreens superior that a promotion was “very highly likely” if he transferred to the drugstore chain’s Dallas division, Chris Cummings uprooted his family and bought a spacious house in this hopefully named suburb.

“The sky’s the limit,” he was told.

But instead of a promotion, the company for which Cummings had been an assistant manager three and a half years cut his hours so drastically that he had to take a second job. In March, he was laid off, and his part-time second job became full-time.

And so that is how a 40-year-old father of four with a master’s in business administration from the University of Notre Dame finds himself bagging groceries at Sprouts, a local health-food store.

Quotable

“It shouldn’t surprise anyone that the nine states without an income tax are growing far

faster and attracting more people than are the nine states with the highest income tax

rates. People and businesses change the location of income based on incentives.

“Likewise, who is gobsmacked when they are told that the two wealthiest Americans—Bill

Gates and Warren Buffett—hold the bulk of their wealth in the nontaxed form of unrealized

capital gains? The composition of wealth also responds to incentives. And it’s also simple

enough for most people to understand that if the government taxes people who work and

pays people not to work, fewer people will work. Incentives matter.” – Arthur Laffer

FX Trading – Key Long-term Themes Still in Play but there are Questions

We put together the chart below for a presentation we made back in January this year; it is a visual representation of the four primary underlying themes we think will drive the long- term dollar bull market.

To phrase it another way, global healing and a strong US dollar are mutually reinforcing and the process itself could lead to a virtuous circle of strength for the US dollar.

Global healing requires global rebalancing. Global rebalancing will be much easier if the US consumer gets back in the game (a strong dollar increases Mr. US Consumer’s purchasing power). A rebounding real economy and money flowing to the US economy are critical factors that will allow Mr. US Consumer to rebuild wealth.

Let’s briefly examine where we may be since we first presented this framework:

1) A rising dollar (falling euro) has relieved a modicum of pressure in Europe; note the increase in German exports reported today. This is not to say German exports are all that is needed, there is a very long way to go, but it is part and parcel to the story.

2) US real economy rebound driven by the force of money making it into the real economy is key to global healing. I think the jury is still out here, as small businesses still are not seeing the credit they need, or the opportunities, to drive US employment. But, because this is a relative game, I have to think the US is leading Europe and Japan on this measure (lagging Australia and Canada). But longer term we need to see improvement.

3) We expected a rising dollar, and by definition a falling euro, and improving US real economy as a way of relieving some pressure on China. To a small degree it has. But, again precisely because the US consumer spending has not rebounded, the jury is still out here. A double-dip recession i.e. falling global demand, likely means trade pressures between China and its “partners” hikes up considerably and add to systemic risk. Again, beneficial to the dollar, but only by default.

4) Lastly, US capital investment hasn’t quite yet rebounded in a way one would expect given the amount of cash and relatively strong US corporate balance sheets. However, international investors continue to find US assets a relative bargain. If risk finally normalizes globally (which still may be a ways off), international money flow to the US could surprise a lot of people. A return of long-term foreign direct investment to US shores is critical to thelong-term move in the dollar and rebound in the world’s demand driver—Mr. Consumer.

Jack Crooks

Black Swan Capital

www.blackswantrading.com

Is the Euro Doomed?

Many are worried about the US dollar. But there’s trouble brewing on the other side of the pond; the chances for a breakup of the euro have risen tremendously.

Sign up and receive our FREE daily newsletter HERE— Currency Currents and receive our Special Report on the Euro.

Black Swan Currency Currents is available FREE HERE. Stay tuned-in to our currency global macro view and our analysis of key investment themes driving currency prices.

THE E‐MINI S&P FUTURES: 1035‐ 1037 Had Better Hold: Those who are bullish had better hope that 1035‐1037 holds, for if not there is no support under this market for a very, very long way. – Dennis Gartman – For a Trial Subscription go to The Gartman Letter

Via Don Vialoux:

The mayhem in equity markets in May could extend to June

May was a troublesome month for equity markets. It was the worst May for U.S. equity markets since 1940. The loss by the Dow Jones Industrial Average reached 7.92 percent leaving many investors uncertain about the global economic recovery.

What happened in May 1940? The Dow Jones Industrial Average fell 21.7 percent that month. In June, it recovered 5.0 percent, recording one of the biggest gains in June since the dirty thirties. However, compared with the loss experienced in May, the June rebound was a mere drop in the bucket.

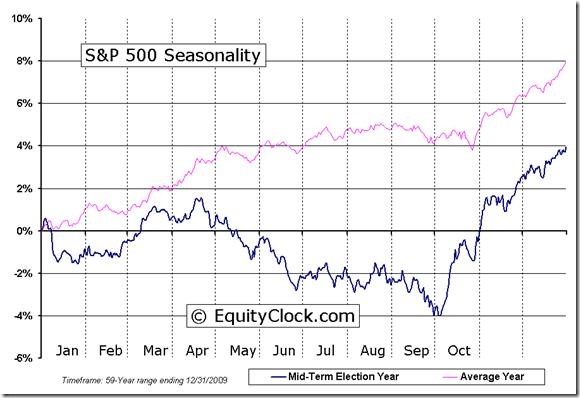

Equity market losses this May were comparable to losses recorded in 1962 when a decline of 7.81 percent was recorded. The drop in May 1962 was followed by an additional decline in June of 8.49 percent. Coincidentally, 1962 was a mid-term election year, similar to the present timeframe. Is history about to repeat?

Performance by equity markets prior to the May 1962 correction looks eerily similar to market conditions in 2009. Equity markets moved higher in 1961. The gain by the Dow Jones Industrial Average topped 18 percent before stabilizing in the first quarter of 1962. And then, the bottom fell out. The Dow Jones Industrial Average fell 30% from March to the end of June. Equity markets finally regained a firm footing in October and a Fall rally ensued.

The May-to-September period has not been favourable for equity markets in midterm election years. Uncertainty about future control over the U.S. Congress and possible changes in policy following mid-term elections creates uncertainty in the economy, which, in turn triggers uncertainties in equity markets.

History shows that a decline by the Dow Jones Industrial Average by greater than 5 percent in May has not been followed by a significant recovery since 1940. June recoveries averaged only 0.91 percent with the bulk of gains occurring outside of midterm election years. Generally, losses in May during midterm election years lead to further losses in June.

A seasonal chart on the performance of the Dow Jones Industrial Average for midterm election years during the past 81 years shows uncanny similarities to the current timeframe. A February-to-April rally turns into a Spring- through-Summer downfall followed by stability and a recovery in October.

Is the loss by the Dow Jones Industrial Average beyond its 7.92 percent decline in May expected to continue? Probability is high. The short-term rebound witnessed this past week during the Memorial Day holiday period is common during mid-term election years. A close look at the seasonal chart for mid term election years shows a similar short-term rebound during the last week of May and the first week in June, precisely until release of the crucial May jobs report. Beyond that point, declines are the norm and they usually last until the end of the month.

Bottom line is that past history does not reveal a favourable June in midterm election years. Prepare yourself for a rocky road ahead.

To View the 45+ Charts in Don’s Monday Report go HERE

Jon and Don Vialoux are authors of free daily reports on equity markets, sectors, commodities, equities and Exchange Traded Funds. Reports are available at www.timingthemarket.ca and www.equityclock.com

In today’s issue of Breakfast with Dave

• While you were sleeping: global equity markets are selling off; the commodity complex is following suit; investors are fleeing to the relative safety of Treasuries

• Bad session, bad week: U.S. stock markets plunged on Friday, and on higher volume; market volatility surging; U.S. dollar has broken out to new highs

• Volatility the hallmark of a bear phase: in the last 30 trading days, the difference between the intraday low and high in the Dow has exceeded 200 points in 23 session

• A few more disturbing U.S. employment tidbits

• Growth slowdown coming: the ECRI weekly leading index growth rate is just basis points away from going below zero

• It’s still all about deflation

• Income works in a deflationary backdrop

….read more HERE

In the last edition of Equedia Weekly, we talked about how the US government printed and borrowed another trillion dollars in less than six months right under our noses (see The Human Metal). As the economy slowly moves towards further recovery, you can bet this number will climb – and along with it, gold.

In the long run, gold should hold its value and continue a slow and steady climb. But short term traders have lots to worry about. Selloff in the summer, rise in interest rates, and positive job reports can all spur a round of profit taking, pushing gold lower. But only in the short term.

The technicals of gold remain strong and according to Michael Lewis, the head of commodities research at Deutsche Bank AG, gold may reach $1,700 in the next year, partly on demand from Asian central banks and surging investment in exchange-traded funds.

And if gold hits anywhere near that number, you can bet that gold miners and explorers will surge along with it.

Also mentioned last week was the split personality of silver – moving with both the price of gold and downturns in the economy led by falling copper prices (see The Human Metal above). This was clearly evident this past week when both silver and platinum both plunged, while gold moved up closer to $1230/oz.

But for those who believe silver is not the place to be, think again.

Silver is still above $17/oz – a number that makes many silver miners profitable. It also has the ability to deliver investors much larger gains than gold during bull markets. In many cases where gold prices have doubled, the price of silver has tripled… quadrupled… and even outperformed gold by a factor of more than six-to-one!

While the price of silver has recently been impacted by a battered global economy through industrial and fabrication demand, the increase in silver investment demand is expected to continue.

Remember, short term thinking in this market will only frustrate investors – trying to predict daily world events is no way to invest in this type of market.

Silver is already becoming one of the preferred investments to safeguard against a fragile global economy. And as investment demand continues to grow, silver prices should also rise. That’s why we believe the best time to invest in silver-related plays is now (see A Sneak Preview).

There are many ways to do this.

Silver Opportunity #1: Silver Bullion

The easiest way to invest in silver is to actually own the metal itself. This is generally done through either coins or bars.

This avenue of investment has picked up dramatically over the past year and in the last month alone, the US Silver Eagle coin reached its the highest monthly sales since 1986. But sales of silver bullion are also soaring in places such as China, where their government not only continues to strongly encourage its citizens to buy precious metals, but are selling them directly through their banks (see The Silver Conspiracy).

Both silver bars and silver coins are priced according to their weight and purity, but often carry a premium above spot silver prices. For those that can afford it, it’s better to buy silver bars over coins, as the premiums are generally lower than coins.

Silver Opportunity #2: Silver ETF’s

Exchange-traded funds (or ETFs) represent a quick and easy way for an investor to gain exposure to the silver price, without the inconvenience of storing physical bars.

Some of these ETF’s include:

Horizons BetaPro COMEX Silver Bull Plus ET (TSX: HZU): Seeks daily investment results, before fees and expenses, that endeavour to correspond to two times (200%) the daily performance of the COMEX(R) silver futures contract for a subsequent delivery month.

Horizons BetaPro COMEX Silver Bear Plus ETF (TSX: HZD): Seeks daily investment results, before fees and expenses, that endeavour to correspond to two times (200%) the inverse (opposite) of the daily performance of the COMEX(R) silver futures contract for a subsequent delivery month.

Central Fund of Canada (TSX: CEF.A) (NYSE: CEF): Has 45% of its reserves held in silver with the remainder invested in gold.

iShares Silver Trust (NYSE: SLV): One of the largest Silver ETF’s

Silver Trust (NYSE: SIVR)

PowerShares DB Silver (AMEX: DBS): holds its worth in futures contracts for physical delivery, which are later sold to silver consumers in order to roll over expiring contracts to contracts further from expiration.

ProShares Ultra Silver (NYSE: AGQ): seeks daily investment results, before fees and expenses, that correspond to twice (200%) the daily performance of silver bullion as measured by the U.S. Dollar fixing price for delivery in London.

Silver Opportunity #3: Silver Stocks

This is by far our favourite way to play the silver boom – yet it is the least direct of all investments tied to silver.

That’s because mining companies that mine silver usually mine other stuff, such as lead and zinc, and its share price is rarely dependent on the price of silver alone.

But the most enticing factor in playing the silver explorers and miners is leverage.

Aside from the price of silver, there are many factors that can substantially appreciate your investments in these companies. Things such as permitting, cost of production, and increases in resource, can all play a strong role in your return on investment. Because of this, higher prices in silver may lead to a stronger gain in a mining company’s shares.

However, there is downside. As with any company, non-market factors such as management decisions and permitting issues will affect investment.

There has been a big selloff of silver stocks over the last month. Both big name silver producers and small cap silver juniors have been hampered by the recent summer sentiment. You can bet that the markets as a whole may experience the same old summer doldrums. Some of these silver stocks have declined as much as 10, 20, and even 30 per cent in the last month.

By Equedia.com – Sign up for FREE Newsletter HERE

Equedia is a strong performing investment newsletter network and a social network aimed at the financial community, with many advanced social networking features. The equedia platform caters to companies who want to communicate with stakeholders via video content, as well as through blogs, shared calendars, and other features.

In addition, we have a strong following through our Equedia Weekly Investment Newsletter aimed at mining and resource stocks with a strong focus on the top Canadian stocks in the industry. Our newsletter features investment ideas and content from our strong performing and respected partners including N. America’s leading analysts and investment personalities.

Equedia is also a community site for media, analysts and investors, who can participate with various online publishing and rating features. Equedia also boasts a best-of-breed video transcoding and streaming architecture, and has a growing and loyal user base.

The new world of finance through Equedia’s web portal is no longer a one way street. It’s about connecting information across social networks, the people looking for it, as well as the conversations that connect them. Equedia helps the investment community by giving it a single resource that provides them with everything they need – an informative social media experience dedicated to the investment community.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair