Daily Updates

Is The Parabolic Blow Off In Gold Accumulation By ETFs About To Cause A Gold Price Explosion?

The closing of gold at an all time high price did not prevent GLD from purchasing 1.9 tonnes of gold on the last 24 hours. The ETF increased its gold holdings NAV from 1306.1 to 1308.

The all time record high holdings of the precious metal represent a 7.5% increase in the tonnage of gold held in the past month alone, which increased by 91 tonnes, or 7.5%, from 1217 tonnes.

As the chart below shows, we have entered into a parabolic purchasing period for not just GLD, but for all other precious metal ETFs, which struggle to keep their NAV at 1. In fact, if those who claim that ETF are among the primary sources of gold demand currently, such reindexing is now creating a positive feedback loop, whereby daily record gold prices are forcing the ETFs to purchase more and more gold to retain a mandated NAV, which in turn is leading to even higher prices on the margin. The accumulation blow off phase has begun, and with a variety of ETFs announcing either shelf or follow on offerings, with the proceeds to be used to buy gold, it is only a matter of time before the actual price blow off follows. A more suitable question is why, if the purchasing of gold has picked up so much, has the gold fixing not followed?

To view larger Chart Click on Chart or HERE

Don’t get caught in summer market volatility

Summer is almost here. The days are longer, the weather is hotter and investors are looking to add sizzle to their portfolios for a possible summer rally. However, higher-than-average volatility in equity markets suggests that investors may not want to relax while basking in the sun this summer.

….read more HERE

One page from the Bank of Montreal’s Basic Points written by Donald Coxe of Coxe Advisors LLP. This excerpt is from a 48 page Basic Points titled June Reflections : Summer’s Storms and Norms. If you would like to be referred to a BMO Capital Markets representative to obtain the entire June Reflections : Summer’s Storms and Norms please email Basic.Points@bmo.com

INVESTMENT RECOMMENDATIONS

1. Canadian bonds, equities and bank deposits are excellent investments for investors based in other currencies. Canadians should take advantage of the Loonie’s current weakness to borrow in greenbacks and otherwise hedge any risks they have to the outcome of a new global love affair with the Loon.

2. Resist the urge to buy the Macondo well-related stocks now that BP has somewhat capped the well. US trial lawyers cannot believe their luck: they will be able to sue, for treble-damages, everybody involved in the well in the infamous “hellhole” courts of Louisiana and Alabama, where the judges’ electioneering costs are paid by plaintiffs’ lawyers. BP’s $20 billion payment will prove to be just a down payment. This is, for these predators, the equivalent of getting advance advice of the winning numbers in a multi-billion-dollar lottery.

3. The oil sands producers don’t benefit as heavily as the US trial lawyers from the BP disaster, but there are two ways their stockholders benefit: by reminding the public that the large-scale alternatives to oil sands petroleum involve much greater environmental risks, they will take some heat off the beleaguered companies; secondly, an offshore oil boom that might have followed from Obama’s cautious reopening of offshore drilling has become a bust. That frees up investor capital allocated toward oil stocks to buy oil sands producers’ shares as the least-costly way to acquire multi- billion-barrel North American exposures.

4. Remain heavily overweight oil compared with natgas. Gas prices have climbed because of the cutoff of expected production from the Gulf, but this should be only a temporary price boost. As Macondo has tragically demonstrated, finding big oil deposits is a high-cost, high-risk business. Finding gigantic natgas deposits is a low-cost, low-risk business. Natgas risks becoming the hydrocarbon equivalent of political hot air: cheap, never-ending and ubiquitous.

5. Gold is more than the Bad News Bear’s New Favorite. It is the completely inverse investment to paper money and complex financial derivatives, making it the multi-millennial belief system to which modern investors can return from the financial system’s current excesses, misrepresentations, and bad politics. In a bull market for gold, the well-managed mines will outperform the bullion. A recommended alternative is the royalty companies.

6. Barring some war in the Korean Peninsula or the Mideast, or the collapse of some major European banks, this stock market pullback should continue to be a correction, not the first chapter in a new horror story. A new Crash at a time of Zero rates remains an unlikely outcome—but not as unlikely as it seemed two months ago before we found out about where all those trichinositic eurobonds were stashed.

7. Remain invested in companies which produce what China and India need. No matter what happens in the OECD, these economies will continue to grow faster than the US or Europe. Their public employees aren’t paid more than their private sector earns, and they don’t retire young. Their governments are not laden with debts that can only be serviced with economic growth at unachievable levels. In other words, they are doing the big things right—and the OECD collectively is doing them wrong. There is no reasonable doubt about which economies will grow most rapidly—with the lowest recession risk.

If you would like to be referred to a BMO Capital Markets representative for the entire Don Coxe Research June Basic Points titled June Reflections : Summer’s Storms and Norms please email Basic.Points@bmo.com

Wellington West Analyst Kevin Shaw lives in Alberta and believes there are few better places to invest than Canada’s oil- and gas-rich provinces. But he also sees attractive international opportunities in such places as Kurdistan, the North Sea and Albania. “When you’re putting a drill bit into the ground in Kurdistan,” he says, “you’re. . .’deep-sea fishing.'” In this exclusive interview with The Energy Report, Kevin explains why he’s also big on the Cardium, Notikewin, Bakken/Three Forks and the Montney shale plays.

……read more HERE

June, July and August are many times the most seasonally-weak period for the junior resource sector. This year it’s been especially tough given the fact that the new highs in gold have not been remotely reflected in the juniors.

The chart below suggests the market is attempting to make a significant bottom. Fingers and toes crossed as it’s been ugly!

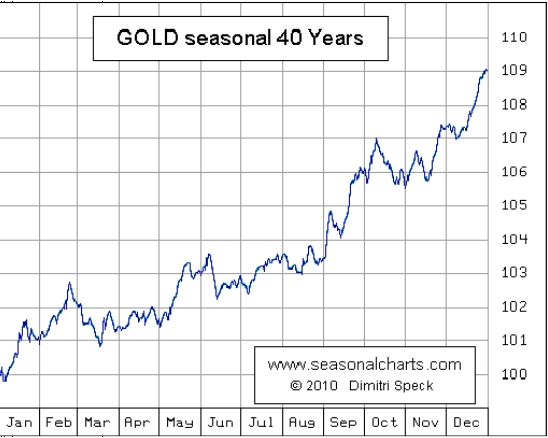

Via Dennis Gartman: IS GOLD REALLY A SEASONAL TRADE: We ran across this “seasonal” chart of gold yesterday, and if it can be believed…and we see no reason why it shouldn’t be… then gold is making a seasonal low here in mid‐June. For a Trial Subscription go to The Gartman Letter

On Major Moves, Peter Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website

To HERE Peter speak and others speak on Trading go HERE:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair