Daily Updates

This Excerpt from Mark Leibovit’s VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

Does the fact that gold barely budged in a week that, based on the strength of the equities rally, should be falling sharply, mean that gold may be at the beginning of a bigger move? BNN asks Mark Leibovit, chief market strategist, VRTrader.com.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

CANADIAN HOUSING MARKET ROLLING OVER

With all the U.S. data yesterday, it was easy to miss the Canadian economic data. The June housing data probably raised the most eyebrows … home sales fell dramatically, down 8.2% MoM and down 20% from year-ago levels.

Average home prices fell 2.5% on the month; however, are still up 5.0% YoY (quite the dramatic slowing from the double-digit price gains a few months ago). Even if prices remain flat for the next few months, we estimate that year-over-year trends will be in negative territory by the fall.

The deteriorating inventory situation could suggest that prices may decline instead of remaining stable over the coming months. In June, months’ supply ticked up to 6.9 months, the highest since March 2009. Rising inventories are not limited to the existing home market — we estimate that builders have been building inventories of new homes for about eight months or so.

…..read more Breakfast with Dave

More in this issue of Breakfast with Dave

- U.S. slowdown: there is no doubt, growth in the U.S. is moderating significantly

- Haven’t we learned? In today’s WSJ, there was an article that completely dumbfounded us

- Income theme intact: according to the latest Investment Company Institute (ICI) data, equity funds saw a net outflow of $4.2bln, while bond funds attracted $6bln

- Bullish sentiment is back, Jack! In addition to the II poll released earlier this week, the AAII survey of investor sentiment also showed bullish sentiment soaring

- Manufacturing sector continues to slow: the NY Empire and the Philadelphia Fed manufacturing indices came in weaker than expected and is suggesting a further decline to the national ISM index

- Manufacturing production in the U.S. sinks: yes, total industrial production rose 0.1% MoM in June, but what caught our eye was the 0.4% decline in manufacturing output

- Initial jobless claims — beware of the noise

- U.S. producer prices — weak to the core

…..read more Breakfast with Dave

With earnings season having kicked off this week, today’s chart provides some long-term perspective in regards to the current earnings environment by focusing on 12-month, as reported S&P 500 earnings. Today’s chart illustrates how earnings declined over 92% from its Q3 2007 peak to Q1 2009 low — the largest decline on record (the data goes back to 1936). Since its Q1 2009 low, S&P 500 earnings have surged (up over 700%) and currently come in at a level that has only been exceeded during the latter years of the dot-com and credit bubbles. Current expectations on Wall Street are that earnings reach the mid-$70 level by the end of 2011 — a level surpassed only briefly during the tail-end of the credit bubble. Where’s the Dow headed? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

Market Going Down With the Ship?

The Baltic Dry Index is Shouting “Danger, Will Robinson!” But Are Investors Listening?

The BDI most recently topped out in May. As of yesterday (Thursday), it has already dropped 35 days in a row.

That’s significant.

This string of “down days” is the longest in at least nine years, The Economist reported this week. During the crash of 2008, the index never fell 35 days in a row.

Today, the BDI is again flashing serious warning signs that not everything is as it appears. It may be warning us about the start of a “double-dip” recession, or it may be telling us that something even worse is at hand.

Historically, the Baltic Dry Index has shown itself to be the EKG of future industrial demand. And, right now, the BDI is screaming “Danger, Will Robinson!” to any investor who will read it and heed it as a true leading indicator.

If the price of refined copper is called “Dr. Copper,” for its ability to ascertain the health of the demand for growth in an economy, the BDI is the daily heartbeat for near-term future industrial demand.

Combined, those two indicators can provide investors with a view of whether the world economy is growing or shrinking, based on the big picture of world demand for growth. Currently, the BDI is flashing serious warning signs to anyone who is looking at it.

The drop in the BDI index in 2008 was one of the most obvious signs of the real impact that the so-called “Great Recession” would have. From May 20, 2008 to Dec. 3, 2008, the BDI fell from its high of 11,793 to its low of 663 – a near-freefall of 94%.

Via Jack Barnes – Jack Barnes started his career at Franklin Templeton in 1997, working with the company’s portfolio team in its fund-information department – just as the Asian contagion infected the Asian tiger countries. He launched his own RIA shop in 2003 just as the second Gulf War was breaking out. In early 2006, after logging a one-year return of nearly 83%, Forbes named Barnes the top stock picker in its “Armchair Investors Who Beat the Pros” competition. His two audited hedge funds generated double-digit returns in 2008. Last summer, Barnes retired to the beach – which is where he writes from now.]

How do I get my free Chart of the Day?

Simply enter and submit your email address HERE (we won’t share it with anyone) and you will receive one free chart per week and instantly receive the latest free Chart of the Day.

Where’s the Dow headed? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

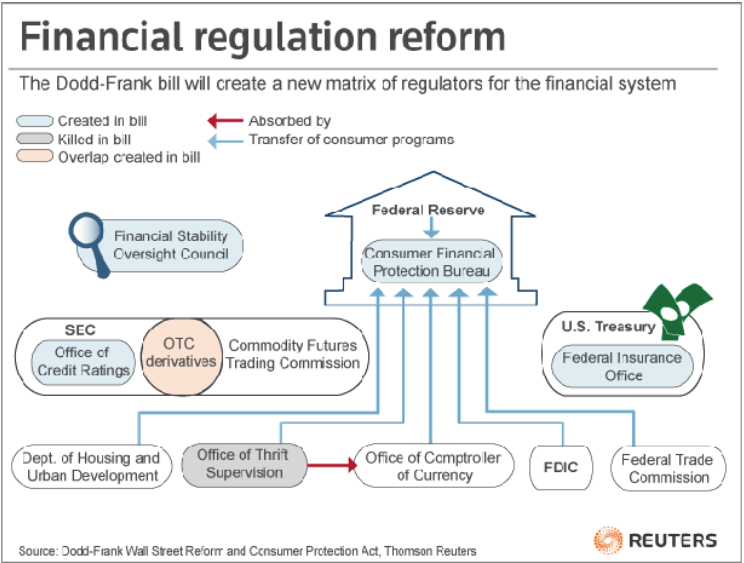

Obama’s Financial Reform

Ed Note: I include a comment on the Fed from Richard Russell Yesterday. The Article Pushing on a String is below the Wikipedia Piece

Question — Russell, you’ve been ranting against the Fed for years. Why so bitter?

Answer — My answer can be gleaned from a quote from the ancient House of Rothschild, at one time the wealthiest and most powerful family on earth. Here’s the quote that tells the story — “Let us control the money of a country, and we care not who makes the laws.” Amschel Rothschild, original head of the House of Rothschild.

Around 1913, a small group of bankers met secretly at Jekyll’s Island, where they developed a plan to establish a national bank that would take over the “task” of issuing the currency of the US. The plan was delivered to an abbreviated and sleepy Congress.

The piece below is from Wikipedia, and is so important that I’m including the whole of the piece below —

……………………………………………………………….

(Ed Note: This chart of Obama’s Financial Reform appeared in Dennis Gartman’s Letter this morning with this comment: “this legislation is simply one more example of

government becoming larger and more seriously intrusive in our lives.”

Jekyll Island and the Federal Reserve.

By John Pounders, Paradigm Publishing, Copyright 1996

My wife and I visited Jekyll Island, Georgia, in April, 1996. It immediately took on a fascination because I remembered that Jekyll is known as the birthplace of the Federal Reserve. In fact, the Clubhouse/hotel on the island has two conference rooms named for the “Federal Reserve.”

In 1886, a group of millionaires purchased Jekyll Island and converted it into a winter retreat and hunting ground, the USA’s most exclusive club. By 1900, the club’s roster represented 1/6th of the world’s wealth. Names like Astor, Vanderbilt, Morgan, Pulitzer and Gould filled the club’s register. Non- members, regardless of stature, were not allowed. Dignitaries like Winston Churchill and President McKinley were refused admission.

In 1908, the year after a national money panic purportedly created by J. P. Morgan, Congress established, in 1908, a National Monetary Authority. In 1910 another, more secretive, group was formed consisting of the chiefs of major corporations and banks in this country. The group left secretly by rail from Hoboken, New Jersey, and traveled anonymously to the hunting lodge on Jekyll Island.

The meeting was so secret that none referred to the other by his last name. Why the need for secrecy? Frank Vanderlip wrote later in the Saturday Evening Post, “…it would have been fatal to Senator Aldrich’s plan to have it known that he was calling on anybody from Wall Street to help him in preparing his bill…I do not feel it is any exaggeration to speak of our secret expedition to Jekyll Island as the occasion of the actual conception of what eventually became the Federal Reserve System.”

At Jekyll Island, the true draftsman for the Federal Reserve was Paul Warburg. The plan was simple. The new central bank could not be called a central bank because America did not want one, so it had to be given a deceptive name. Ostensibly, the bank was to be controlled by Congress, but a majority of its members were to be selected by the private banks that would own its stock.

To keep the public from thinking that the Federal Reserve would be controlled from New York, a system of twelve regional banks was designed. Given the concentration of money and credit in New York, the Federal Reserve Bank of New York controlled the system, making the regional concept initially nothing but a ruse.

The board and chairman were to be selected by the President, but in the words of Colonel Edward House, the board would serve such a term as to “put them out of the power of the President.” The power over the creation of money was to be taken from the people and placed in the hands of private bankers who could expand or contract credit as they felt best suited their needs.

Why the opposition to a central bank?

Americans at the time knew of the destruction to the economy the European central banks had caused to their respective countries and to countries who became their debtors. They saw the large- scale government deficit spending and debt creation that occurred in Europe.

Shortly after the United States gained its freedom, the Rothschilds attempted to saddle the country with a private central bank. This Bank of the United States was abolished by President Andrew Jackson with these words:

The bold effort the present bank has made to control the government, the distress it had wantonly produced…are but premonitions of the fate that awaits the American people should they be deluded into a perpetuation of this institution or the establishment of another like it.

But European financial moguls didn’t rest until the New World was within their orbit. In 1902, Paul Warburg, a friend and associate of the Rothschilds and an expert on European central banking, came to this country as a partner in Kuhn, Loeb and Company. He married the daughter of Solomon Loeb, one of the founders of the firm. The head of Kuhn, Loeb was Jacob Schiff, whose gift of $20 million in gold to the struggling Russian communists in 1917 no doubt saved their revolution.

The Fed controls the banking system in the USA, not the Congress nor the people indirectly (as the Constitution dictates). The U.S. central bank strategy is a product of European banking interests.

Back to Jekyll, the Island

National and world events of the 1930s led ultimately to the Club’s closing in 1942. Jekyll Island was purchased by the state of Georgia in 1947. 33 of the Club member cottages and Clubhouse still stand. Many have been restored to their former grandeur and are open for tours.

Pushing on a String … Again?

In the wake of the latest batch of “double-dip” chatter, the market’s attention is shifting back to the Federal Reserve. Investors are asking a simple question:

“What, if anything, will the Fed do if the economy craps out again?”

Before I give my answer to that question, I’m inclined to ask a different one:

“Who cares?”

These guys have already done just about everything they can … pulled every trick out of their hats … and bailed out and backstopped virtually the entire financial system!

While all of that free money helped boost ASSET prices, it hasn’t done a heck of a lot for the “real” economy. Unemployment remains stubbornly high. Housing continues to slump. Investment is anemic and confidence is lacking.

In other words, the Fed is pushing on a string — and more pushing isn’t going to do a darn thing for those of us living in the real world! But since the market is focusing on the Fed again, let me address the question at hand …

Is QE2 Coming?

The latest economic data clearly suggests that my double-dip scenario is becoming much more likely.

Just this week, for instance, we learned that retail sales dropped 0.5 percent in June after falling 1.1 percent in May. That was worse than economists expected and the first back-to-back decline since early 2009.

What about housing?

Well, if you believe purchase mortgage applications are a good leading indicator of demand — and I do — then you should be worried. A Mortgage Bankers Association index that tracks loan activity just fell to 163.30. That’s the lowest level going all the way back to December 1996!

Finally, as Claus noted on Wednesday, a key leading index is pointing decisively lower. The inescapable conclusion? Despite the happy talk on Wall Street and the recent market rally, the economy appears to be rolling over.

The last time the economy fell into the drink, the Fed reacted by slashing interest rates to a range of 0 percent to 0.25 percent. The federal funds rate has remained there ever since, and there’s no indication it’ll rise anytime soon.

But the Fed did much more than lower the funds rate …

It also embarked on a policy of “Quantitative Easing” (QE). That’s a fancy way of saying it printed money out of thin air and bought more than a trillion dollars of securities: Mortgage-backed bonds, Fannie Mae and Freddie Mac debt, long-term Treasuries, and so forth.

The idea was to lower mortgage rates and bond yields, thereby spurring home purchases, refinances, and corporate investment.

Did it work?

Well, mortgage rates definitely tanked. At around 4.5 percent, in fact, 30-year fixed mortgages are the cheapest they’ve been in the last century! But as I noted above, housing activity is now plumbing depths we haven’t seen since Bill Clinton’s first term in office. Bond yields did drop initially, but not much. And they subsequently rose again.

Bottom line: I’d argue the Fed didn’t accomplish much. Even some Fed officials doubt the rampant money printing and QE policy worked all that well, according to The Wall Street Journal.

That hasn’t stopped some of the Keynesian acolytes from begging for even more free money from Helicopter Ben Bernanke though. Take New York Times columnist Paul Krugman …

He lambasted the “Feckless Fed” this week, begging it to do “all it can to stop it” — the “it” being deflation. Buy government bonds? Buy private bonds? Pledge to keep short-term rates low, essentially, forever? Krugman is all for it!

So far, the Fed itself appears split. The Journal this week puts Fed governor Kevin Warsh, Richmond Fed president Jeffrey Lacker, and Kansas City Fed president Thomas Hoenig in the “No more funny money” camp.

But Boston Fed president Eric Rosengren and New York Fed president Bill Dudley appear more open to the idea. Bernanke is reportedly somewhere in the middle, preferring to just wait, watch, and let the market sort itself out.

If So, Should We Care?

But again, my answer is that whether the Fed goes hog wild printing money or not, it won’t matter much to the real economy. It’ll probably boost gold prices. It’ll likely hammer the dollar. And it could temporarily boost stocks, even in the face of lousy fundamentals.

But all the kings horses, all the kings men, and even a further ballooning of the Fed’s balance sheet — currently around $2.3 trillion vs. $900 billion before the credit crisis burst onto the scene — won’t matter to most Americans.

Private companies aren’t firing workers and hoarding cash because interest rates are too high. They’re doing so because there’s too much factory and labor capacity.

Consumers aren’t cutting back on spending because loans are too expensive. They’re doing so because they just went on the wildest debt-fueled spending binge in U.S. history, and they’re trying to repair their balance sheets.

Look, we’ve had twin bubbles in stocks and housing over the past decade and a half. They both popped. The fallout will be with us for a long, long time.

I wouldn’t be surprised in the least if a long Japan-like period of economic stagnation lies ahead. In fact, I’d invest accordingly — by paring back stock positions into rallies, and using inverse ETFs and put options to target downside profits.

And when the Fed chatter reaches a fever pitch, I have some advice: Turn off the TV and go play with your kids or grandkids. It just doesn’t matter much in the grand scheme of things.

Until next time,

Mike

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.It also embarked on a policy of “Quantitative Easing” (QE). That’s a fancy way of saying it printed money out of thin air and bought more than a trillion dollars of securities: Mortgage-backed bonds, Fannie Mae and Freddie Mac debt, long-term Treasuries, and so forth.

Out of curiosity, I ran the monthly chart of gold that you see below. The chart starts with the year 1999 and each bar represents one month’s action. You can see that gold has been advancing along a rising trendline. In late-2008, the rise accelerated, and we see a steeper ascending trendline.

My thinking is that somewhere ahead we’re going to see a third still-steeper rising trendline. (Ed Note: Russell has been Bullish Gold since below $300 and currently holds the biggest position he has ever had since 1950 in Precious Metals)

General Advice: General Advice — Stay with the primary trends. Stocks are caught in a primary bear market, so stay out of the stock market and I mean stay out. Gold is in an established primary bull market, so don’t trade gold, stay on the back of Toro and ride the bull (and ignore all warnings from know-nothing analysts who keep calling for a “gold top”).- Richard Russell Dow Theory Letters (

Gold Prices Holding Up Well

Despite Portugal’s sovereign debt being down graded the eurocrats have managed to calm the waters and keep the euro reasonably steady. Austerity is the word for the Europeans, real or imagined, whereas stimulus is the word for the United States. Interestingly the euro is steady but the dollar has lost 6.8% of its value in just over a month as the spot light once again is focused on the fundamentals of the dollar. Throw in a down grade from the Chinese and things don’t look to bright for the US sovereign debt.

Taking a quick look at the above chart we can see that apart from one bad day at the office, when gold was sold down about $40.00/oz, gold prices are holding up pretty well especially for this time of the year when the summer doldrums usually kick in and volumes drop off significantly. We can also see that the STO is heading north and the MACD looks as though it is also ending its downward slide, which all bodes well for gold prices. If gold can maintain these levels through until September then the stage will be set for a major advance and the forming of a few new all time highs.

Turning to the chart for the USD we can see that it has resumed its trek south, all as we suggested on 09 June 2010 when the USD looked a tad overbought and has since lost about 6.8% in little over a month. The technical indicators have been floored so some consolidation may be on the cards, however we expect it be short lived as the economic recovery in the United States continues to fade and the general mistrust of paper currencies compels investors to re-think their strategies.

The days of a rating agency duopoly in the United States whereby Moody’s and Standard and Poors could issue triple A status to companies on the verge of bankruptcy are now over. Making their debut is this area is the world’s first “non-Western” sovereign credit rating agency, a Chinese company named Dagone (means Big Justice in Chinese) who have down graded the US to AA with a negative outlook. This agency would appear to concentrate more on the ability to pay than the ability to borrow. The dragon has stirred from its slumbers and its influence on world affairs will be felt in every corner of the planet. However, a no nonsense, practical assessment of the state of play will be welcomed by many, especially gold bugs who are contrarian by nature and tire of big government influence in these matters.

Below is the chart we posted of USD which we posted on 09 June 2010 accompanied with a snippet of our commentary.

We could well be too early in making this call but it appears to us that the dollar may now have run its course and will now look to take a breather. As we can glean from the chart, over the last two months the Euro has been under the gun, resulting in a rally for the USD as the preferred currency. Also note the gap that is opening up between the dollar at ‘88′ and the 200dma, which stands at ‘79′. The RSI, MACD and the STO are bouncing along at the top of their respective ranges and sooner or later they will return to somewhere more in the middle of their ranges. So the dollar now appears to be a tad overbought, in our humble opinion.

For now we will be keeping a tight grip on our precious metals but will be taking a serious look at our portfolio of stocks with the view to pruning some of the poorer performers and reinvesting in quality stocks which look to have a brighter future and have responded to the movements in gold prices.

Stay on your toes and have a good one.

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. (Winners of the GoldDrivers Stock Picking Competition 2007)

For those readers who are also interested in the silver bull market that is currently unfolding, you may want to subscribe to our Free Silver Prices Newsletter.

For those readers who are also interested in the nuclear power sector you may want to subscribe to our Free Uranium Stocks Newsletter, just click here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair