Daily Updates

Market Buzz – Slowing Growth Trend Continues, North and South

While the S&P/TSX Composite Index closed Friday down 15.21 points to 11,713.43, it ended the month 3.7% high, continuing its recovery from the relative carnage we saw in May.

Having said this, going forward, investors will have to weigh the underwhelming growth readings released today for both Canadian and U.S. economies. Statistics Canada said the country’s gross domestic product grew by 0.1% in May, better than the flat reading in April but slower than experienced in the first quarter.

In the U.S., the Commerce Department reported that the GDP grew at an annual pace of 2.4% from April to June. The number was less than the 2.5% that economists had expected.

Immediately following their releases a number of commentators indicated the twin reports suggest that Canada is maintaining a slow-but-steady recovery from the recession while the U.S. is waging a tougher battle to regain ground. For us however, the overarching theme was one the North American economy’s abrupt Q2 2010 slowdown from the first quarter’s strong growth.

The Canadian economy’s tepid growth of 0.1% seen in May, while up from a flat reading in May, is a far cry from the spectacular growth spurt that began last fall and continued into this year, when the economy grew 4.9% in the last quarter of 2009 and a decade best 6.1% in the first quarter of 2010.

While the May pace is not disastrous, it will make it difficult for the economy to match the Bank of Canada’s recent projection of 3% growth in the second quarter, which ended June 30.

Switching gears to our Canadian Small-Cap Universe (www.keystocks.com) we take a quick look at a long-time favourite of ours, Glentel Inc. (GLN:TSX), a leading provider of innovative and reliable telecommunications services and solutions in Canada and the United States. Glentel has grown to become the largest multi-carrier mobile phone retailer in Canada operating more than 280 locations.

This past week the company reported that its sales for the three months ended June 30, 2010 grew 16%, to $78.97 million from $67.85 million in the same period of 2009. Net income and basic earnings per share for the three months were $3.76 million or $0.34 per share respectively, compared to $2.64 million or $0.24 per share, for the same period in 2009.

We are happy to report the stock surged just under 10% on the news and hit a new all time high this past week.

Looniversity – Penny Stocks – Two Common Fallacies

Two common fallacies pertaining to penny stocks are that many of today’s stocks were once penny stocks and that there is a positive correlation between the number of stocks a person owns and his or her returns.

Investors who have fallen into the trap of the first fallacy believe Wal-Mart, Microsoft, and many other large companies were once penny stocks that have appreciated to high dollar values. Many investors make this mistake because they are looking at the “adjusted stock price,” which takes into account all stock splits. By taking a look at both Microsoft and Wal-Mart, you can see that the respective prices on their first days of trading were $28 and $25 even though the prices adjusted for splits is $0.09722 and $0.02444. Rather than starting at a low market price, these companies actually started pretty high, continually rising until they needed to be split.

The second reason that many investors may be attracted to penny stocks is the conception that there is more room for appreciation and more opportunity to own more stock. If a stock is at $0.10 and rises by $0.05, you will have made a 50% return. Couple this with the fact that a $1000 investment can buy 10,000 shares convinces investors that micro-cap stocks are a rapid surefire way to increase profits. Truth be told, without independent research from a company like say KeyStone Financial (www.keystocks.com) which happens to specialize in the small- and micro-cap markets, many investors end up with pennies on the dollar from investing in so-called “penny stocks.”

Put it to Us?

Q. Can you give me a quick overview of “contrarian” investing or the contrarian style of investing?

– Gabriel Wilson; Calgary, Alberta

A. Ah, the contrarian – you say black, he says white; up – down; bad – good; you get the picture. A contrarian investor is generally an individual that invests against market trends and does not follow the prevailing consensus view. Yes, a true rebel, maverick, or rogue of the intriguing world of investing – yeah, right!

Generally, a contrarian investor believes that the people who say the market is going up do so only when they are fully invested and have no further purchasing power. At this point, the market is at a peak. On the other hand, when people predict a downturn, they have already sold out, at which point the market can only go up.

The contrarian generally focuses on turnaround situations and stocks currently out of favour with low P/E ratios, practicing patience and long-term investing.

KeyStone’s Latest Reports Section

- Alternative Financial Services Provider Posts Record Q4 and Fiscal 2010 Revenue & EPS, Aggressive Growth Plan Intact – Stock Rating Upgraded (Flash Update)

- Junior Gold/Copper Producer Sees Shares Surge on Positive Mine Report & Strategic Debt Financing– Maintain Rating (Flash Update)

- Canada’s Leading Industrial Services Firm Posts Solid Q2 – Rating Maintained (Flash Update)

- Hardware & Software Communications Micro-Cap With Strong Balance Sheet Posts Top-line Growth, Bottom Line Hit by Currency – Maintain Rating (Flash Update)

- China-based Forestry Company Posted Solid Q1 2010, Rating Upgraded on Price Decline (Flash Update)

ED Note: Michael Campbell calls Greg Weldon – “The One Analyst other Analysts can’t Wait to Read.”

One of poker’s unwritten rules is … ‘you can’t bluff a novice’.

The theory provides that bluffing an inexperienced player is more-often-than-not, unsuccessful … since a novice would not understand that he might actually be beat, by numerous other hands than the one he might hold, and will thus NOT fold to a well-timed bluff. Theoretically, a more experienced player might understand that his hand is vulnerable, inducing a fold to any show of strength (bluff).

In my first book, ‘Gold Trading Boot Camp’, I hypothesized that three decades of parabolic credit growth in the US ‘household’ sector, the denouement of which was the US property bubble … was one big, unsustainable ‘bluff’ …

…with the US Consumer, in collusion with, and staked by, the US Federal Reserve, repeatedlybluffing the markets ‘with a ‘weak hand’ that failed to have the support of wage-income growth and adequate savings, relative to the degree of increasingly leveraged credit being created …

… in 1987 … 1990-91 … 1997-98 … and in 2000-01.

However, bluffing…. ‘all-in’ at all times, will eventually result in a ‘call’.

Indeed, we believe the ‘markets’ have called the current ‘bluff’ by the US consumer, who is feigning ‘strength’, hoping markets will fold, and equity markets will roar once again.

From the „top-down “macro-perspective, the hard-core data details have become increasingly ‘skewed’ towards the negative, with an abundance of ‘cracks’ developing in the (alleged) ‘recovery’.

This may spell trouble for trigger-happy equity market bulls who have surfed aboard the recent waves of rally days, which actually ‘curls’ into a ‘patterned’ counter-trend bullish move, within the context of a still-evolving bigger-picture bearish trend.

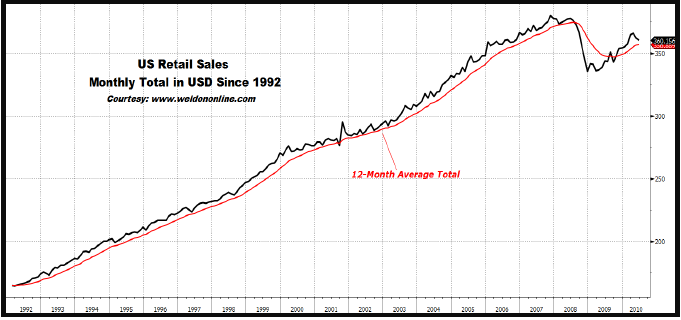

In terms of the US consumer’s current ‘bluff’ … we ‘read’ numerous signs of WEAKNESS, thanks to the data details extracted from within the June Retail Sales report, released Wednesday … revealing a (-) $1.875 billion single-month slide in final sales … which combines with a deep decline in May, versus April, for a two-month cumulative contraction of (-) $5.859 billion, in total monthly Retail Sales.

Indeed, we ‘read’ weakness, any time we see outright deflation in headline consumer final demand, in back-to-back months. Evidence the chart on display below plotting Total US Retail Sales, in dollars, per month … reflecting an ominous double-dip pattern. Any further signs of flagging demand in the US consumer-retail sector will strongly suggest that the consumer might be ‘folding’ this time around, rather than going all-in on a bluff. Such a circumstance would be signaled with a push in the Total Monthly Sales back below the 12-Month Average.

Weldon’s Money Monitor offers a FREE 30 Day Trial Subscription. For subscription information contact Eileen @Weldononline.com or Visit www.Weldononline.com for a FREE Trial.

A FREE 30 Day Trial Subscription is defined as a single Trial that is limited to a one-time Signup. Signing up for multiple trials under different names, Fraudulent contact information is illegal. Weldon’s Money Monitor takes this seriously..

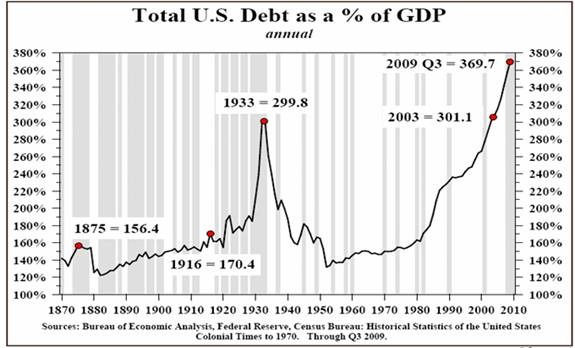

As you can see from the chart below, the total of all debt (government, business and consumer) is now somewhere in the neighborhood of 360 percent of GDP. Never before has the United States faced a debt bubble of this magnitude….

Most of us were not alive during the Great Depression, but those who were remember how incredibly painful it was for America to deleverage and bring the economic system back into some type of balance.

So if our current debt bubble is far worse, what kind of economic horror is ahead for us?

But the truth is that we are facing some circumstances that even the folks back during the Great Depression did not have to deal with….

1 – Back in the 1930s, tens of millions of Americans lived on farms or knew how to grow their own food. Today the vast majority of Americans are totally dependent on the system for even their most basic needs.

2 – A vast horde of Baby Boomers is expecting to retire, and the “Social Security trust fund” has nothing but 2.5 trillion dollars of government IOUs in it. According to an official U.S. government report, rapidly growing interest costs on the U.S. national debt together with spending on major entitlement programs such as Social Security and Medicare will absorb approximately 92 cents of every dollar of federal revenue by the year 2019. This is a financial tsunami the likes of which Americans back in the 1930s could never have even dreamed of.

3 – American workers never had to compete for jobs with workers on the other side of the world back in the 1930s. But today, millions upon millions of our jobs have been “outsourced” to China, India and a vast array of third world nations where desperate workers are more than happy to slave away for big global corporations for less than a dollar an hour. How in the world are American workers supposed to compete with that?

4 – Back in the 1930s, there was nothing like the gigantic derivatives bubble that hangs over us today. The total value of all derivatives worldwide is estimated to be somewhere between 600 trillion and 1.5 quadrillion dollars. The danger that we face from derivatives is so great that Warren Buffet has called them “financial weapons of mass destruction”. When this bubble pops there won’t be enough money in the entire world to fix it.

5 – During the Great Depression, the United States economy was relatively self-contained. But today we truly do live in a global economy. Unfortunately that means that a severe economic crisis in one part of the world is going to affect us as well. Right now, the United States is far from alone in dealing with a massive debt crisis. Greece, Spain, Italy, Hungary, Portugal and a number of other European nations are in real danger of actually defaulting on their debts. Japan (the third biggest economy in the world) is on the verge of complete and total economic collapse. So what happens to the U.S. economy when the dominoes start to fall?

The truth is that by almost any measure, we are in worse economic condition than we were right before the beginning of the Great Depression. We have been living way beyond our means and the debts we have been piling up are clearly not anywhere close to sustainable.

Did you think that we could just continue to run deficits equal to 10 percent of GDP forever?

Of course not.

The U.S. economy is being driven off a cliff, but America’s “ruling class” has insisted all along that they know better than we do.

But the truth is that in the final analysis it is not us that they care about.

What they do actually care about is getting more money and more power for themselves and for other members of the ruling class. Today, 10,000 people make 30% of the total income in the United States each year.

That leaves 70% of the pie for the remaining 99.99% of us to divide up.

The reality is that however you want to slice it, the U.S. economic system is broken. However, considering the fact that America’s ruling class has a stranglehold on both major political parties, we are not likely to see any fundamental changes any time soon.

That is very unfortunate, because time is running out on the U.S. economy.

About the author: Michael T. Snyder

Michael T. Snyder is a graduate of the McIntire School of Commerce at the University of Virginia and has two law degrees from the University of Florida. He is an attorney that has worked for some of the largest and most prominent law firms in Washington D.C. and who now resides outside of Seattle, Washington. He is a very active blogger and is also a respected researcher, writer, speaker and activist. You can follow him on his daily news blog entitled The Most Important News: http://themostimportantnews.com/

In the first few days of July, the prices of gold and silver appeared to break a five-month upward trend by drawing back about five per cent from the record June peaks. Despite many similar corrections that have occurred frequently during the long bull market in precious metals, pundits nevertheless looked to draw bold and significant conclusions from the drop. But just as investors were getting comfortable with the leading explanation – that a looming double dip recession will prevent inflation and thereby dampen demand for precious metals – the markets for both metals stabilized.

Most investors still credit the accepted orthodoxy that metals will only gain if inflation is widespread or a financial crisis encourages investors to seek safe havens. The failure of both metals to break below their upward trend lines, despite the lack of news on both fronts, should lay to rest these canards. Unfortunately, nothing appears more resilient than the belief in a gold bubble.

In my opinion, the current rise of precious metals is the direct result of the evident profligacy of governments the world over. Spendthrift politicians in Washington, London, and Tokyo, have caused people to lose faith in paper currencies. Investors, as well as an increasing number of lay citizens, understand that debts cannot be accumulated forever and that the most tempting solution will be to simply print more currency. The only alternative is an unpalatable tax hike that will only serve to reduce long-term revenue, as explained by the famed Laffer Curve.

This conflict will remain whether or not the CPI is currently spiking, and whether or not appetite for risk returns to the marketplace. So, until the political currents change or we face sovereign catastrophe, I believe gold and silver will be in a sustainable secular (long-term) bull market – not a bubble.

With the long term trend line of gold and silver still intact, but with current prices below their recent highs, many investors may be sensing buying opportunities. If so, which metal looks more attractive?

The price of gold and silver are typically influenced by several factors that do not affect prices for conventional commodities.

Gold holds the status of being the world’s ultimate store of value. Neither governments nor wealthy individuals seem to be able to sleep soundly without some cache of the yellow metal. Gold is less used in the industry and its price less easily manipulated. Therefore, the big players in the precious metals markets, especially central banks, tend to invest portions of their vast holdings into gold.

Silver is generally the province of smaller investors. It is more accessible on a price-per-ounce basis, akin to the B-shares of Berkshire Hathaway. Silver has many industrial uses, giving it exposure to the commodity and monetary markets. This means the silver price tends to be more volatile and relatively less favored as a safe haven by the big players.

During the financial panic of 2008, the fortunes of gold and silver parted drastically. In that calendar year, when nearly every asset class fell dramatically, gold lost only 29% of its value from peak to trough. Silver, on the other hand, fell much harder – down 57%. But silver has bounced back harder. Since the trough, the price of silver is up 97%, as compared to 66% for gold. What’s more, the price of silver is still below its 2008 high, while gold has been continually setting new records on a daily basis. Based on these technicals, it is likely that many investors may perceive value in silver.

Generally, the rule of thumb is that gold offers relative stability and silver offers greater upside (and downside). Therefore, the amount of additional risk an investor is willing to take will determine the gold/silver ratio in his portfolio. The other aspect is the ratio between physical metals and metal mining companies. The former are historically relatively safer, but don’t generate revenues like owning stock in a miner can. Again, the allocation to each would be up to the individual investor. Each alternative represents a different way to access what I have argued is a secular bull market in precious metals.

I believe that more and more observers will recognize the nascent sovereign debt crisis as merely the precursor to a currency collapse. If I am correct, then investors will likely continue to pour into assets with intrinsic value, including precious metals. From my vantage point, the choice between gold and silver is of secondary concern. Investors should be more wary of clinging irrationally to an anachronistic US dollar regime.

by John Browne Senior Market Strategist

New Special Report: Peter Schiff’s Five Favorite Gold & Silver Mining Stocks – Click HERE

For in-depth analysis of this and other investment topics, subscribe to The Global Investor, Peter Schiff’s free newsletter. Click HERE for more information.

John Browne is the Senior Market Strategist for Euro Pacific Capital, Inc. Working from the firm’s Boca Raton Office, Mr. Brown is a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee, as Chairman of the Conservative Small Business Committee, and as a close associate of then-Prime Minister Margaret Thatcher. Among his many notable assignments, John served as a principal advisor to Mrs. Thatcher’s government on issues related to the Soviet Union, and was the first to convince Thatcher of the growing stature of then Agriculture Minister Mikhail Gorbachev. As a partial result of Brown’s advocacy, Thatcher famously pronounced that Gorbachev was a man the West “could do business with.” A graduate of the Royal Military Academy Sandhurst, Britain’s version of West Point and retired British army major, John served as a pilot, parachutist, and communications specialist in the elite Grenadiers of the Royal Guard.

In addition to careers in British politics and the military, John has a significant background, spanning some 37 years, in finance and business. After graduating from the Harvard Business School, John joined the New York firm of Morgan Stanley & Co as an investment banker. He has also worked with such firms as Barclays Bank and Citigroup. During his career he has served on the boards of numerous banks and international corporations, with a special interest in venture capital. He is a frequent guest on CNBC’s Kudlow & Co. and the former editor of NewsMax Media’s Financial Intelligence Report and Moneynews.com.

07/22/10 Vancouver, British Columbia – The Dow fell 109 points yesterday. Gold was flat. Otherwise, all quiet on the financial front.

We’re keeping these reckonings short this week. Your editor is attending a financial conference in Vancouver. He doesn’t want to miss anything.

What have we learned so far?

….read more from Bill Bonner HERE

Golden Shell Games

07/22/10 Vancouver, British Columbia – That’s right, gold. You know, the ultimate money. Or Gold: The Once and Future Money, as our friend Nathan Lewis titled his 2007 book, for which we were privileged to write the foreword.

Hey, Wall Street can take a $250 million sewer project in Alabama and turn it into an insurmountable debt 20 times as big. So it can find a way to pervert the Midas metal, too. And the evidence is piling up: You don’t have to be partial to conspiracy theories about the “manipulation” of gold to conclude something just doesn’t look right.

That means you need to be very careful about how you hold any gold outside your physical possession – especially in a retirement account.

Of course, it’s always important to ask oneself, how much is there to these conspiracy theories, really? Well, ever since the publication of his book, Lewis has been scrutinizing them. And this year, they’ve reached a fever pitch.

- Did you hear about the 400-ounce gold bars filled with tungsten? (Tungsten’s weight is nearly identical to gold, so the deception is simple if the bar isn’t properly assayed)

- Or the one about the London metals trader turned whistle-blower who alleged JP Morgan Chase is suppressing the silver price? And how he was injured in a mysterious hit-and-run? (His injuries were minor)

- Or how the head of the Gold Anti-Trust Action Committee testified about gold manipulation before the Commodity Futures Tradition Commission and the camera conveniently malfunctioned?

You could go very far down the rabbit hole trying to separate fact from fiction with these kind of stories. And you’d be wasting your time.

Marc Faber, editor of The Gloom Boom & Doom Report stated it well in April, so well we quoted it in The 5 Min. Forecast: “If you have manipulation to keep the price down, it eventually goes ballistic. So all the people that are bitching about the manipulation of silver and gold should be happy that it is manipulated, because it still gives them an opportunity to buy it at a depressed price.”

Exactly. Manipulation stories are a source of entertainment, outrage or both. They underscore the perils of the Wall Street Fandango. But their truth or falsehood makes little difference if you hold gold in your physical possession. Or in an allocated account (the gold has your name on it) in an independent, insured depository. Or if you use a reputable electronic gold purveyor. (We like GoldMoney.com and BullionVault.com.)

But it makes a lot of difference if you hold “paper gold” in the form of an exchange-traded fund. Many people buy vehicles like GLD and IAU with the comforting illusion that what they’re buying is “good as gold.” And it’s an incredibly convenient way to get metals exposure in a retirement account.

Which brings us to the revelations of Janet Tavakoli.

Tavakoli is not a gold bug. She’s an expert in structured finance and credit derivatives who runs her own consulting firm in Chicago. Recently, she published a client report that took the format of “advice” she would give to Wall Street sharpies trying to corner the gold market. Not that they’d ever try that, of course.

Pump up the gold story. Get your friends to tell retail investors to buy some gold every month. Get your buddies in the financial business to offer exchange-traded gold funds (ETFs) that claim to buy physical gold. This will sound safe to retail investors, but in fact, the ETFs are very risky. This will serve your purpose when you are ready to start a panic. These particular ETFs will allow the “gold” to be commingled with the custodian’s gold, and the custodian can lease out the gold.

Moreover, the “gold” custodian can give it to a subcustodian that the manager doesn’t know. The subcustodian can give it to yet another subcustodian unknown to the original custodian. The manager will never audit the gold, and the gold is not “allocated” to a particular investor. Since this is an “exchange traded” gold fund, investors will probably assume the gold is regulated by the Commodities Futures Trading Commission (CFTC), but it isn’t. By the time investors wake up to the probability that there is very little actual gold backing their investment, your plan will be ready to execute.

The “plan” involves buying huge futures contracts and expecting physical delivery. If this sounds familiar, it’s pretty much what the Hunt brothers did when they tried to corner the silver market in 1980. Silver shot up to $50, however briefly. It’s never seen that territory again.

But the consequences this time around would be far more serious. It could collapse banks holding huge short positions in the futures market, accustomed to settling contracts cash only. More to our point, it would crater the ETFs: Their complex network of custodians and subcustodians would be laid bare. ETF investors would realize they have a claim on the same chunk of gold as, say, Goldman Sachs. But Goldman would have the actual metal. The ETF investor would have to settle for pennies on the dollar.

Far-fetched? Maybe. Just remember that ETFs are ultimately, like a complicated mortgage derivative, subject to counterparty risk. If the day comes when trust evaporates from the system, value will evaporate from the ETFs. If you want to play gold’s short-term ups and downs, the ETFs are an ideal instrument. Otherwise, stay away.

Addison Wiggin

for The Daily Reckoning

Addison Wiggin

Addison Wiggin is the editorial director of The Daily Reckoning, and executive publisher of Agora Financial, an independent financial research firm based in Baltimore, Maryland. His second editions of international best-sellers Financial Reckoning Day Fallout and The New Empire of Debt, which he co-authored with Bill Bonner, were updated in 2009. His third book, The Demise of the Dollar… and Why it’s Even Better for Your Investments was updated in 2008, the same year he wrote I.O.U.S.A. Read more about Wiggin’s best-selling books here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair